Quick Navigation

Report Overview

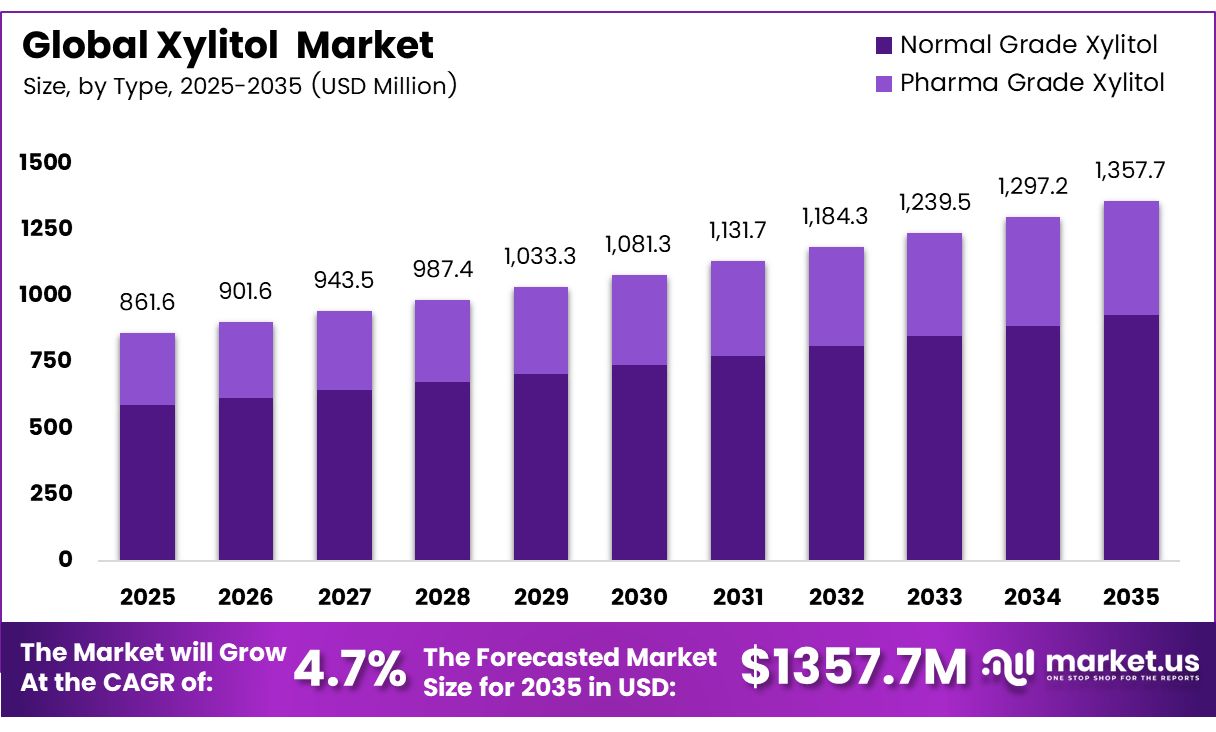

The Global Xylitol Market was valued at USD 861.6 million, and between 2026 and 2035, this market is estimated to register a CAGR of 4.7%, reaching about USD 1357.7 million by 2035. Asia Pacific held a dominant market position, capturing more than a 50% share, holding USD 430.79 million in revenue.

The World Health Organization (WHO) reported in 2024 that 2.5 billion adults aged 18 years and older were overweight globally as of 2022, including over 890 million living with obesity, representing 43% of the global adult population, with the worldwide prevalence of obesity more than doubling between 1990 and 2022. Xylitol production and consumption are concentrated in the Asia Pacific, mainly in China, due to ample corn cob resources and integrated infrastructure. Demand is growing in North America and Europe, driven by health trends and natural sweetener support.

The global xylitol is part of the ever-expanding natural and reduced-calorie sweetener segment, driven by the alignment of health-oriented consumer behavior trends, regulatory support, and increasing functional foods, medications, and personal products. Xylitol, which is a five-carbon sugar alcohol (C5H12O5) found in some fruits and vegetables, birch trees, and corn cobs, is known for being almost as sweet as sucrose and for having a low glycemic index of 7, when compared to that of sugar, which is between 60 and 70.

Xylitol has anti-caries attributes clinically proven to prevent tooth decay. The FDA has declared xylitol as a GRAS ingredient and also recognizes it as a non-cariogenic sweetener. According to the International Diabetes Federation (IDF) Diabetes Atlas 11th Edition (2025), an estimated 11.1% of the global adult population, or 1 in 9 adults aged 20–79 years, was living with diabetes in 2024, with the total number exceeding 500 million and projected to rise to nearly 853 million by 2050.

The increasing prevalence of lifestyle-related non-communicable diseases drives xylitol demand. Conditions like diabetes, obesity, and dental issues are expanding consumer interest in low glycemic sugar alternatives. Xylitol’s glycemic properties provide a clinical advantage for diabetic-friendly products, avoiding significant blood glucose or insulin level fluctuations.

Key Takeaways

- The global Xylitol market was valued at USD 861.6 million in 2025.

- The global Xylitol separator market is projected to grow at a CAGR of 4.7% and is estimated to reach USD 1357.7 million by 2035.

- On the basis of grade/type, Normal Grade Xylitol dominated the market, constituting 68.5% of the total market share.

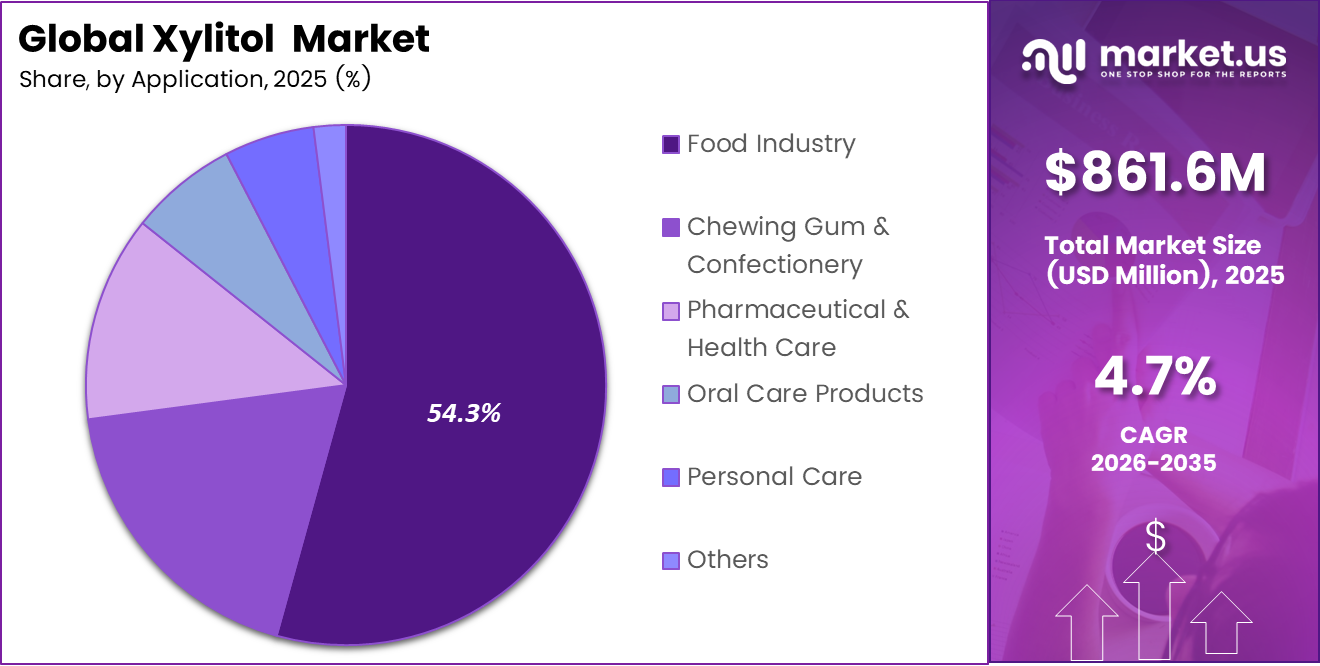

- Based on application, the Food Industry dominated the xylitol market, holding a substantial market share of 54.3%.

- Based on form, the Solid (Granules/Powder) form led the market, comprising 85.0% of the total market share.

- Based on the source, Corn Cob-Based xylitol led the market, accounting for 55.0% of the total source share, driven by cost efficiency and abundant agricultural raw material availability in the Asia Pacific.

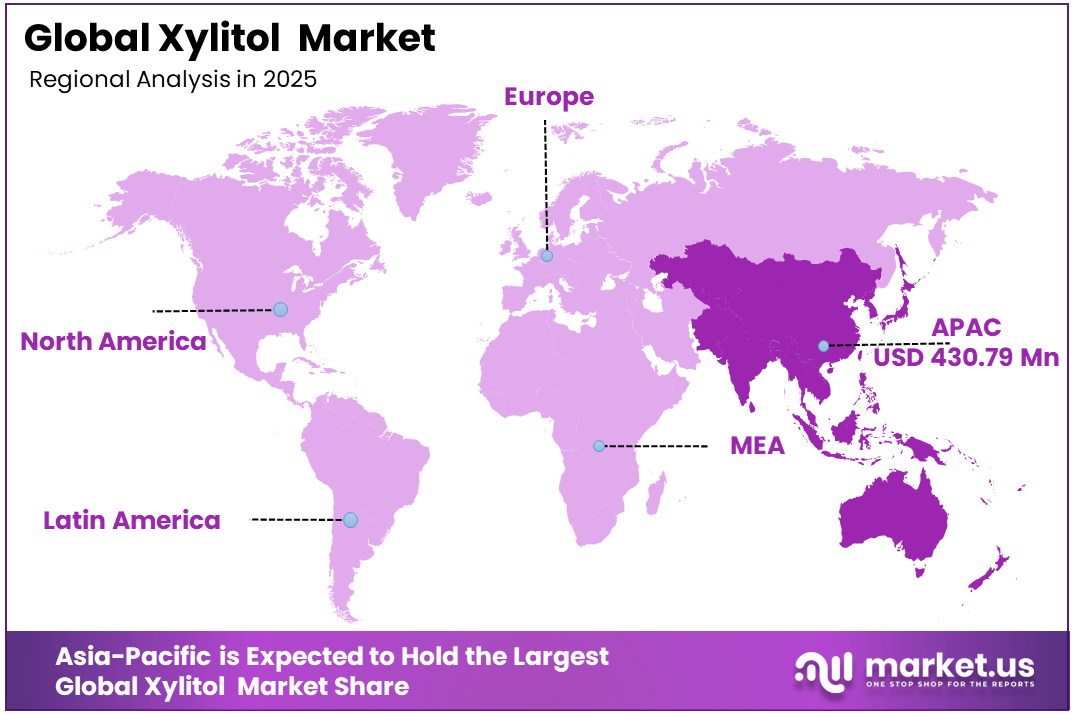

- In 2025, the Asia Pacific was the most dominant region, accounting for 50.0% of the total global xylitol market.

Grade/Type Analysis

Normal Grade Xylitol Represents the Dominant Segment in the Market

Normal Grade Xylitol dominates the global xylitol market with a 68.5% revenue share in 2025, driven by its use in food manufacturing, confectionery, oral care, and personal care. Its cost-effectiveness compared to pharmaceutical grade and adherence to food safety standards, like the United States Food and Drug Administration(FDA) Generally Recognized As Safe (GRAS) status, make it ideal for industrial use.

The segment thrives in the chewing gum and confectionery industries, offering a 1:1 sugar substitute that is equally sweet without an aftertaste and provides anti-cariogenic benefits. Increasing demand for sugar-free and reduced-calorie products, fueled by health awareness, enhances its appeal amid rising diabetes and obesity rates.

Pharma Grade Xylitol, comprising 31.5% of the market, is the fastest-growing segment due to its use in pharmaceuticals, clinical nutrition, and premium oral care. With stringent purity specifications, it’s suitable for intravenous solutions, syrups, and dietary supplements. Its low glycemic index of 7 makes it ideal for diabetic and metabolic disease management.

According to the IDF Diabetes Atlas 2025, the number of adults living with diabetes globally exceeded 500 million in 2024, with an estimated 43%, approximately 252 million individuals remaining undiagnosed, underscoring the critical and expanding need for diabetic-friendly ingredients in pharmaceutical and nutraceutical product development.

Application Analysis

The Food Sector Signifies the Leading Portion of the Market

The Food Industry comprises 54.3% of the total xylitol market, thus forming the biggest application segment due to its extensive usage in a broad range of processed food items such as baked foods, dairy foods, beverages, jam, confectionery, and artificial sweetening agents for tabletop use. Xylitol’s 1:1 substitute ratio with sugar, almost the same sweet taste profile, tasteless character, and 40% less calorie content compared to sucrose makes it commercially and technologically suitable for the production of food products.

Chewing Gum and Confectionery Applications represent a growing segment in the xylitol market, driven by rising consumer demand for sugar-free and reduced-sugar products. Xylitol is widely used in chewing gums, mints, and confectionery items due to its sweet taste, cooling effect, and oral health benefits. Increasing awareness of dental hygiene and healthier dietary choices is encouraging the adoption of xylitol-based confectionery products.

Form Analysis

Solid (Granules/Powder) Form Accounts for the Leading Segment in the Market

The solid form of xylitol, both granules and powder, occupies an 85.0% market share globally due to its excellent physical attributes, including its longer shelf life, ability to dose easily, wide acceptability for dry blending, tableting, and baking, which are common practices in food and pharmaceutical production facilities. Solid xylitol in either the form of granules or powder can be easily substituted for sugar crystals because the forms resemble each other both in appearance and performance in food manufacturing operations.

This means that no special effort needs to be made to accommodate the use of the solid xylitol in the production process of foods since it does not require many changes in the process setup. Liquid Xylitol is an emerging segment in the xylitol market, finding increasing use in beverages, liquid medicines, mouthwashes, oral care rinses, and nutritional formulations.

Its excellent solubility and ease of incorporation into liquid products make it a preferred choice for manufacturers developing sugar-free and low-calorie formulations. Growing demand for functional beverages, pediatric syrups, and oral healthcare products is supporting segment expansion. In addition, rising consumer preference for convenient liquid formulations and clean-label ingredients is creating new opportunities for liquid xylitol across the food, pharmaceutical, and personal care industries, positioning the segment for sustained future growth.

Source Analysis

Corn Cob-Based Xylitol Represents the Dominant Segment in the Market

Corn Cob-Based xylitol accounts for 55.0% of the global xylitol market by source, anchored in the large-scale availability of corn cobs as an agricultural byproduct – particularly across the Asia Pacific region, where China is among the world’s leading corn producers. Corn cobs are rich in xylan – a hemicellulosic polysaccharide – that serves as the primary feedstock for industrial xylitol production via hydrolysis and subsequent catalytic hydrogenation, translating into significant cost advantages over alternative feedstocks.

The USDA Foreign Agricultural Service has noted China’s continued government prioritization of corn as a staple crop, with stable corn production levels supported through national food security policies, which are reinforcing the long-term raw material security for corn cob-based xylitol manufacturing.

Birch Wood-Based Xylitol is a growing segment in the xylitol market, supported by increasing consumer preference for naturally sourced and sustainable ingredients. Widely recognized as the traditional source of commercial xylitol, birch wood-derived xylitol benefits from strong acceptance in premium food, oral care, and healthcare applications. Demand is rising as consumers increasingly seek clean-label sweeteners and plant-based alternatives to conventional sugar.

Key Market Segments

By Grade/Type

- Normal Grade Xylitol

- Pharma Grade Xylitol

By Application

- Food Industry

- Chewing Gum & Confectionery

- Pharmaceutical & Health Care

- Oral Care Products

- Personal Care

- Others

By Form

- Solid (Granules/Powder)

- Liquid

By Source

- Corn Cob-Based

- Birch Wood-Based

- Synthetic

Opportunities

Clinical oral-care platforms

This is an opportunity rather than a current driver because xylitol is already widely used in gum, toothpaste, and oral-care products. The untapped potential lies in positioning it as a clinically guided preventive platform distributed through dentists, pharmacies, and insurer-linked wellness programs. EFSA supports a caries-reduction framework involving around 2–3 g of xylitol gum at least three times daily after meals.

Regimen-based bundles combining gum, lozenges, rinses, and subscriptions could raise annual revenue per user from roughly $12–18 to $45–70 and improve gross margins by 600–900 basis points. Converting 8–10% of existing developed-market users by 2030 could add about $180–260 million above baseline revenue and contribute approximately +1.8 percentage points to CAGR.

Opportunities Impact Table

| Opportunity | (~) % Potential CAGR Upside | Geographic Relevance | Execution Window |

|---|---|---|---|

| Clinical oral-care platforms | +1.8% | EU, North America, Japan, South Korea | Short term (≤ 2 years) |

| Sugar-free private-label confectionery | +1.5% | EU, UK, North America, GCC | Short term (≤ 2 years) |

| Low-sugar pharma excipients | +1.2% | North America, EU, India | Medium term (2-4 years) |

| Biorefinery co-product integration | +2.1% | China, India, Brazil, Southeast Asia | Medium term (2-4 years) |

| Adjacent ENT and wellness formats | +0.9% | North America, EU, urban APAC | Medium term (2-4 years) |

| Premium “natural-origin” ingredient migration | +1.4% | EU, North America, APAC premium | Long term (≥ 4 years) |

Challenges

Feedstock purity volatility

Xylitol production depends on xylose-rich materials such as corncobs, hardwoods, and agricultural residues. However, variations in moisture, xylan content, ash, lignin, and inhibitors increase purification needs. Hemicellulose typically forms 25%–35% of lignocellulosic biomass, while seasonal feedstock changes can cause fermentable-xylose yields to fluctuate by roughly 8%–15%.

This inconsistency may create around 60–140 basis points of annual growth friction by lowering plant utilization, increasing consumable use, and delaying feedstock qualification. Producers, therefore, need multi-feedstock sourcing, local preprocessing, larger safety stocks, and digital grading systems to stabilize production costs and output quality.

Challenges Impact Table

| Challenge | (~) % CAGR Friction Drag | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| Feedstock purity volatility | -1.1% | China core, EU biomass clusters, North America processors | Medium term (2-4 years) |

| Energy-intensive conversion chain | -1.4% | EU regulatory hubs, East Asia production bases, US specialty plants | Long term (≥ 4 years) |

| Detoxification and yield losses | -0.9% | APAC manufacturing corridors, Latin America biomass sites, and emerging biorefineries | Medium term (2-4 years) |

| Crystallization consistency gaps | -0.8% | Pharma-grade export hubs, Japan-Korea quality markets, EU oral-care supply chains | Medium term (2-4 years) |

| Gastro-tolerance perception risk | -0.7% | North America packaged foods, EU clean-label brands, urban APAC confectionery | Short term (≤ 2 years) |

| Scale-up talent and process gap | -1.0% | US bioprocess ventures, China scale-up sites, European innovation clusters | Long term (≥ 4 years) |

Drivers

Sugar reduction compliance in packaged foods

The strongest near-term driver is tighter sugar labeling and food-policy scrutiny, which is pushing reformulation across confectionery, bakery, nutraceutical chewables, and reduced-sugar snacks. U.S. Nutrition Facts rules require added-sugar disclosure, while FDA guidance defines 5% Daily Value as low and 20% as high. WHO guidance also continues to support lower free-sugar consumption. This creates a strong commercial role for xylitol because it can reduce added sugar while maintaining bulk, mouthfeel, and sweetness close to sucrose. These functional benefits make it more suitable than high-intensity sweeteners alone in products where texture and volume are important.

Drivers Impact Table

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Sugar reduction compliance in packaged foods | +1.4% | North America core, EU core, APAC urban markets | Short term (≤ 2 years) |

| Oral care efficacy and claim-led adoption | +1.1% | EU core, North America core, Japan, South Korea | Short term (≤ 2 years) |

| Low-glycemic and diabetic-friendly formulation shift | +0.9% | North America, GCC, India metros, Southeast Asia | Medium term (2-4 years) |

| Feedstock circularity from corncob, oat hull, and bagasse | +1.3% | China, the Nordics, India, broader EU | Medium term (2-4 years) |

| Fermentation yield gains and process intensification | +0.8% | China, India, EU specialty ingredients base | Medium term (2-4 years) |

| Premium clean-label polyol positioning in functional foods | +0.7% | EU, North America, developed APAC | Long term (≥ 4 years) |

Restraints

Feedstock cost volatility

Xylitol production remains exposed to agricultural cost volatility because it relies heavily on xylose-rich biomass such as corn cobs. Although global coarse-grain output is expected to rise, unstable acreage, farm-input costs, and regional procurement spreads limit cost relief. The NCGA estimated that average U.S. corn planting costs could reach $917 per acre in 2026, increasing by $27 year over year.

A 6%–10% increase in feedstock procurement costs could reduce merchant-grade xylitol EBITDA margins by roughly 120–220 basis points. Higher raw-material costs, yield losses, and longer working-capital cycles may force price increases that confectionery and oral-care buyers resist, delaying contracts and tender wins while creating an estimated -1.3 percentage-point drag on forward CAGR.

Restraints Impact Table

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Feedstock cost volatility | -1.3% | China, the core, North America, and the EU importers | Short term (≤ 2 years) |

| Energy-intensive conversion economics | -0.9% | China, EU, Japan, Korea | Medium term (2-4 years) |

| Labeling and compliance tightening | -0.8% | EU, South Korea, premium APAC | Short term (≤ 2 years) |

| Freight and corridor disruption | -0.7% | EU import markets, North America, MENA | Short term (≤ 2 years) |

| Capacity concentration in China | -1.0% | Global, especially the EU and North America | Medium term (2-4 years) |

| Reputation and demand-side caution | -0.6% | North America core, EU, developed APAC | Medium term (2-4 years) |

Geopolitical Impact Analysis

US–China Trade Tensions and Supply Chain Concentration Risks Reshaping the Global Xylitol Market

The global xylitol market is highly vulnerable due to its reliance on China, which produces around 50% of xylitol. This concentration invites supply chain risks as escalating US-China trade tensions disrupt agricultural commodity flows and pricing. In 2025, China’s new tariffs on US corn, wheat, and other agricultural goods introduce cost volatility for xylitol manufacturers reliant on stable corn cob supplies. Additionally, China’s Export Control Law, imposing dual-use material restrictions, adds regulatory unpredictability, further complicating supply chains dependent on Chinese production.

- According to the USDA Foreign Agricultural Service, US agricultural exports to China accounted for approximately USD 25 billion in 2024, around 14% of total US agricultural exports, underscoring the scale of bilateral agricultural trade interdependence now subject to sustained disruption risk from escalating tariff measures on both sides.

Meanwhile, the Russia-Ukraine war is increasing the risk associated with the volatility of agricultural commodity prices, especially corn and grains, adding another layer of uncertainty to the procurement cost of corn cob, which is required in xylitol manufacturing. All these factors together have led to a fast-tracking of diversification efforts by buyers from North America and Europe.

Regional Analysis

Asia Pacific Held the Largest Share of the Global Xylitol Market

As of 2025, the Asia Pacific led the world’s xylitol market, accounting for 50.0%, with its dominance attributed to the well-developed production system that exists in China, the largest producer and exporter of the commodity, with support from an abundance of corn cob raw material source, efficient cost-effective mass production systems, and a fast-growing health-conscious consumer population within the region. The xylitol production in China not only meets the domestic demands, but is also exported to major countries such as the USA, Europe, India, and other South Asian nations.

In addition to this, growth in urban areas, an increase in the number of diabetics, as well as the adoption of sugar-free confectionery, chewing gums, and nutraceuticals in India, Japan, South Korea, Thailand, and Vietnam, is adding to the dominance of the Asia Pacific region in the production as well as consumption of the commodity.

According to the IDF Diabetes Atlas 2025, the Western Pacific region had 215.4 million adults with diabetes in 2024, while South-East Asia had 106.9 million, creating a combined regional diabetic population of about 322.3 million adults. This supports the structural demand base for low-glycemic and sugar-reduction ingredients such as xylitol across the Asia Pacific.

Key Regions and Countries Covered in this Report

- North America

- The US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia & CIS

- Rest of Europe

- APAC

- China

- Japan

- South Korea

- India

- ASEAN

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Competitively speaking, the international xylitol industry demonstrates high concentration, with its production mainly dominated by relatively few large-scale Chinese players along with several well-known Western multinational companies.

Chinese companies can capitalize on the availability of cheap production through the use of corn cobs as raw material sources, an ample supply of domestic raw materials, and huge annual production capacity. Major competitive strategies in the xylitol industry include investments in increased production capacity, vertical integration to ensure raw material supply, and product diversification into different grades of xylitol.

The major global firms have a differentiation advantage because of their technological expertise in the production process, compliance with pharmaceutical grade standards, and their long-term contracts with major food, candy, oral care, and pharmaceutical companies. The western multinational firms enjoy a premium position in high-value pharmaceutical and functional foods, thanks to their superior research and development facilities, vertical integration, and distribution channels.

Key Players

- Danisco (DuPont)

- Roquette Frères

- Futaste Pharmaceutical Co., Ltd.

- Huakang Pharmaceutical Co., Ltd.

- Shandong Longlive Bio-Technology Co., Ltd.

- Shandong LuJian Biological Technology Co., Ltd.

- Zhejiang Huakang Pharmaceutical Co., Ltd.

- Anyang Yuxin Pharmaceutical Co., Ltd.

- Cargill, Incorporated

- Ingredion Incorporated

- Mitsubishi Shoji Foodtech Co., Ltd.

- NovaGreen

- Thomson Biotech (Xiamen) Co., Ltd.

- Others

Key Development

- In March 2024, Roquette Frères announced a definitive agreement to acquire IFF’s Pharma Solutions business unit for an enterprise value of up to USD 2.85 billion, strengthening its pharmaceutical excipient portfolio and expanding drug delivery formulation capabilities globally.

- In May 2025, Roquette Frères successfully completed the acquisition of IFF Pharma Solutions, officially integrating the business and reinforcing its position as a leading global provider of pharmaceutical excipients and oral dosage solutions.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 861.6 Mn |

| Forecast Revenue (2035) | USD 1357.7 Bn |

| CAGR (2026–2035) | 4.7% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020–2024 |

| Forecast Period | 2026–2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Grade/Type (Normal Grade Xylitol and Pharma Grade Xylitol), By Application (Food Industry, Chewing Gum & Confectionery, Pharmaceutical & Healthcare, Oral Care Products, Personal Care, and Others), By Form (Solid and Liquid), By Source (Corn Cob-Based, Birch Wood-Based, and Synthetic) |

| Regional Analysis | North America – The US & Canada; Europe – Germany, France, The UK, Spain, Italy, Russia & CIS, Rest of Europe; APAC- China, Japan, South Korea, India, ASEAN & Rest of APAC; Latin America- Brazil, Mexico & Rest of Latin America; Middle East & Africa- GCC, South Africa, & Rest of MEA |

| Competitive Landscape | Danisco (DuPont), Roquette Frères, Futaste Pharmaceutical Co., Ltd., Huakang Pharmaceutical Co., Ltd., Shandong Longlive Bio-Technology Co., Ltd., Shandong LuJian Biological Technology Co., Ltd., Zhejiang Huakang Pharmaceutical Co., Ltd., Anyang Yuxin Pharmaceutical Co., Ltd., Cargill, Incorporated, Ingredion Incorporated, Mitsubishi Shoji Foodtech Co., Ltd., NovaGreen, Thomson Biotech (Xiamen) Co., Ltd., Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |