Quick Navigation

Report Overview

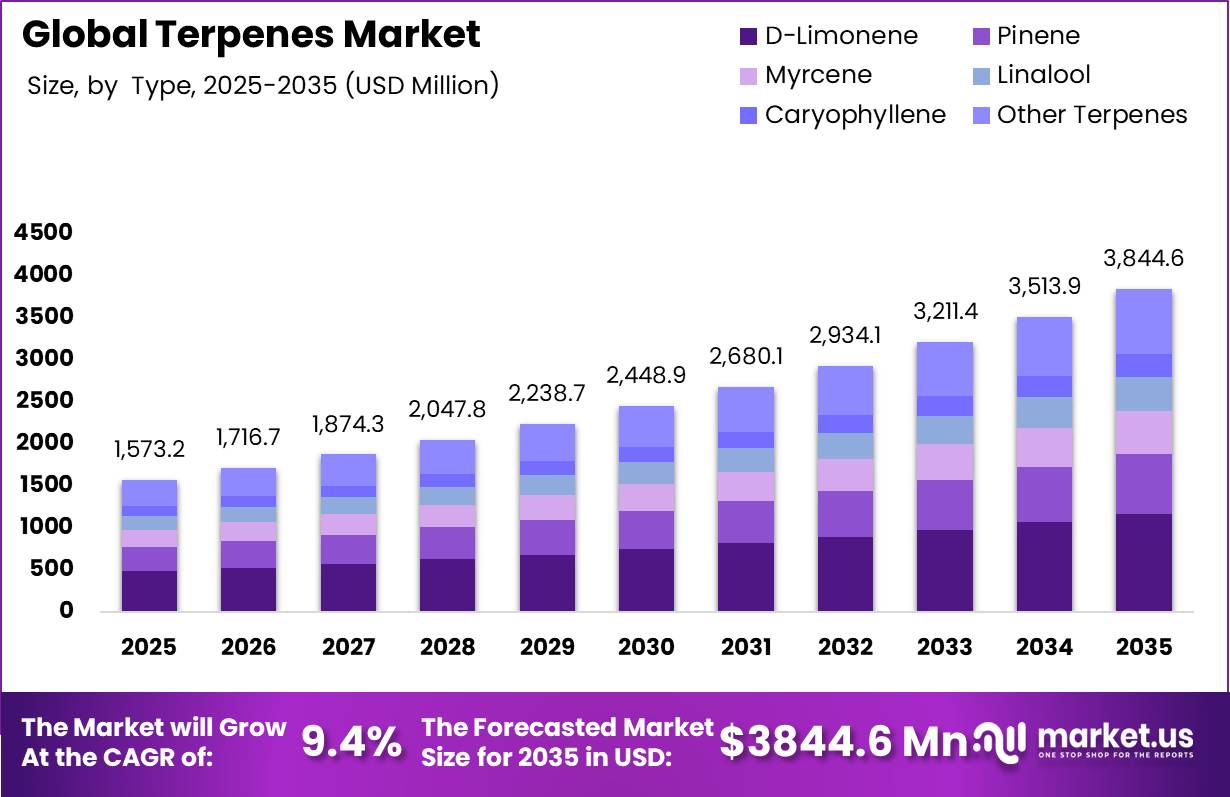

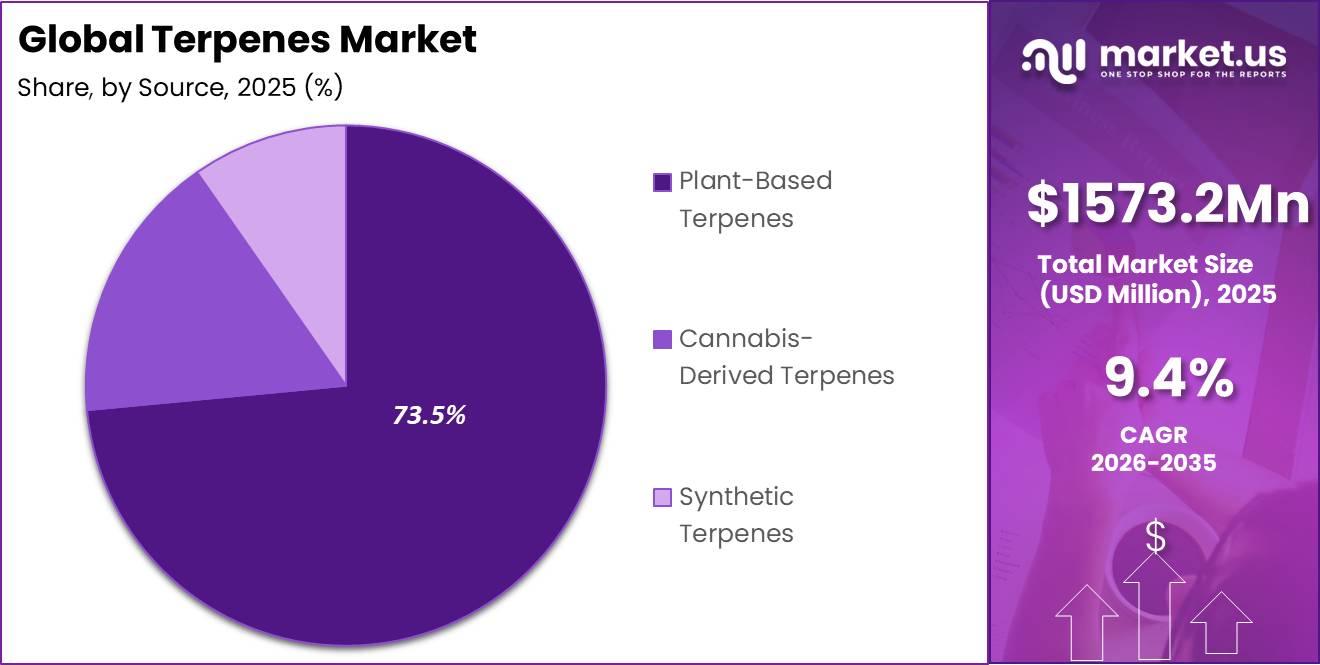

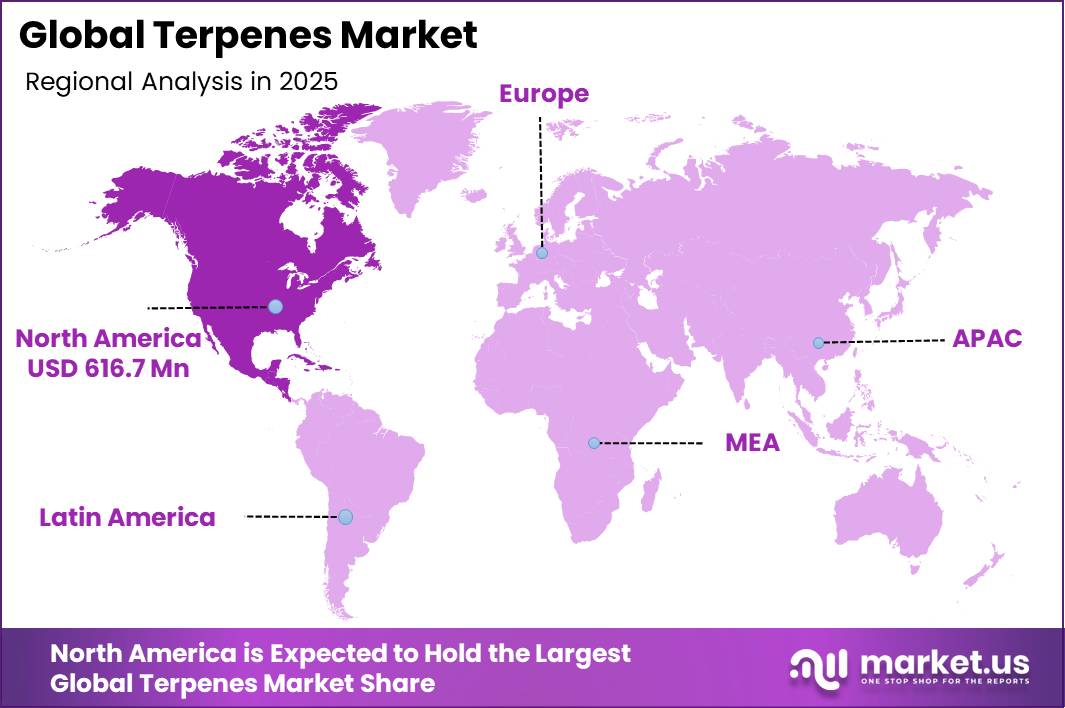

The Global Terpenes Market was valued at USD 1573.2 million in 2025 and is expected to grow to USD 3,844.6 million in 2035. Between 2025 and 2035, this market is estimated to register a CAGR of 9.4%. North America held a dominant market position, capturing more than a 39.2% share, holding USD 616.9 million in revenue.

Advances in extraction, biotechnology, and fermentation are enabling the production of highly pure terpenes for health, wellness, and specialty chemical applications. Sclareol production reached 12.9 g/L after 240 hours of fermentation, while optimized cultivation increased limonene output from 7 μg/L to 38.81 μg/L, representing an approximately 5.5-fold improvement.

Terpenes are currently used in many industries, including the manufacture of foods and drinks, cosmetics, drugs, nutraceuticals, personal care products, cannabis products, and chemical products. Organizations involved in the manufacturing of these products are increasingly adopting terpenes in their products because of the increased consumer demand for natural products.

AI-assisted enzyme design is further accelerating terpene innovation. A model trained on 79,000 terpene synthase sequences generated 28,000 candidate sequences, identified 7 promising enzymes, and experimentally confirmed activity in 2 enzymes. These developments support the production of cleaner and more consistent natural ingredients, aligning with growing consumer demand for minimally processed cold-pressed oils and wellness products.

Another key factor driving the growth of the cold-pressed oil market includes the expanding presence of health and wellness culture across regions like North America and Europe. In the case of cold pressed oil products, natural compounds such as antioxidants and essential fatty acids are highly sought after not only for the nutritional and sensory benefits they provide, but for their role in helping brands differentiate themselves in an increasingly competitive market.

Key Takeaways

- Market size in 2025 is valued at USD 1,573.2 Million, reaching USD 3,844.6 Million by 2035.

- The market is projected to grow at a CAGR of 9.40% during the forecast period from 2026 to 2035.

- By Type, D-Limonene dominated the global terpenes market, accounting for 30.40% of the total market share in 2025.

- By Source, Plant-Based Terpenes emerged as the leading segment, holding a dominant 73.50% share of the global market in 2025.

- By Application, Flavors & Fragrances led the market with a 34.70% share, making it the largest application segment in 2025.

- By End-Use Industry, Consumer Goods accounted for the largest share of the market, representing 31.30% of total revenue in 2025.

- By Distribution Channel, Direct/B2B Sales dominated the market with a 58.40% share in 2025, while Online Retail remained the fastest-growing channel due to rising digital adoption and e-commerce penetration.

- North America dominated the global terpenes market in 2025, capturing 39.20% of the total market share.

By Source Analysis

Terpenes market segmentations on a global scale are categorized into three major groups based on the source of terpenes. These include Plant-Based Terpenes, Cannabis Based Terpenes, and Synthetic Terpenes. The group that is dominating the terpenes market globally is plant-based terpenes, which represent a remarkable 73.5% market share owing to their established usage for a number of applications in industries such as flavors, fragrances, food and beverages, personal care and home care products.

Terpenes derived from the cannabis plant constitute 16.8% of the total market value and have become increasingly popular owing to the legalization of cannabis in various jurisdictions of North America and Europe, alongside rising consumer awareness about strains of cannabis characterized by unique aroma attributes and the therapeutic value of the entourage effect.

Type Analysis

D-Limonene Leads the Terpenes Market, While Caryophyllene Emerges as the Fastest-Growing Segment.

The dominant segment is D-Limonene, holding the largest share of 30.4% in the global terpenes market. Its strong market position comes as no surprise; D-Limonene is one of the most versatile and widely recognized terpenes in use today. Found naturally in citrus peels, it has earned a firm place across a broad range of industries including food and beverages, fragrances, cleaning products, and personal care.

Consumers and manufacturers alike are drawn to its fresh, citrusy profile and its natural origin, making it a go-to ingredient for brands looking to deliver both performance and a clean-label appeal. Close behind, Pinene at 18.6%, Myrcene at 13.2%, Linalool at 10.6%, and Other Terpenes at 20.0% collectively reflect the diversity of applications driving demand across the broader market, from flavored wellness products and perfumes to food manufacturing and cosmetics.

The fastest-growing segment is Caryophyllene, currently accounting for 7.2% of the market. What makes this segment particularly exciting is the direction it is heading. Caryophyllene is uniquely positioned at the intersection of two of today’s most powerful consumer trends: wellness and natural pharmaceuticals.

Application Analysis

Flavors & Fragrances Led the Terpenes Market; Caryophyllene Recorded the Highest Growth.

The global terpenes market encompasses the segments of Flavors & Fragrances, Pharmaceuticals, Cosmetics & Personal Care, Food & Beverage, Cleaning & Household Products, and Cannabis Products. The Flavors & Fragrances segment occupies the biggest place in the market, accounting for 34.7%.

Terpenes are widely applied for improving aromas and flavors of perfumes, flavors, beverages, personal care products, and cleaning products. Terpenes feature the natural aromatic composition and plant origin, making these substances an ideal option for clean-label and natural ingredient manufacturing.

The fastest-growing segment is Caryophyllene, currently holding a 7.2% share of the global terpenes market. What sets this segment apart is its unique ability to go beyond just scent or flavor. Caryophyllene is one of the few terpenes known to interact directly with the body’s endocannabinoid system, giving it a distinct functional advantage that is increasingly catching the attention of pharmaceutical and nutraceutical manufacturers.

Distribution Channel Analysis

The global terpenes market spans across distribution channels including Direct/B2B Sales, Specialty Chemical Distributors, Online Retailing, and Retail Outlets.

The dominant segment is Direct/B2B Sales, holding the largest share of 58.4% in the global terpenes market. This channel is particularly favored by large-scale manufacturers, pharmaceutical companies, food & beverage producers, and fragrance houses, and it’s easy to understand why. When you’re operating at scale and need a consistent, reliable supply of high-quality terpene products, going direct simply makes the most sense.

Specialty Chemical Distributors further support market growth by bridging the gap between terpene producers and small to mid-sized buyers across various industries, while Retail Outlets serve a comparatively smaller share of the market, catering primarily to everyday consumers.

The fastest-growing segment is Online Retail. While it may not yet match the volume of direct sales, the momentum behind this channel is hard to ignore. Small brands, independent laboratories, and wellness product developers are increasingly turning to online platforms for the flexibility and convenience they offer, particularly when sourcing smaller quantities of specialty terpenes.

End Use Analysis

Consumer Goods Leads the Terpenes Market, While Aromatherapy & Wellness Emerges as the Fastest-Growing Sector.

The global terpenes market spans five key end-use industries: Consumer Goods, Healthcare & Pharma, Food Processing, Aromatherapy & Wellness, and Industrial Applications. The Consumer Goods sector takes the top spot, holding the largest share of 31.3% in the global terpenes market.

From personal care and home care to functional beverages and wellness products, terpenes have become a go-to ingredient for brands looking to stand out, meet clean-label demands, and deliver a better sensory experience. Healthcare & Pharma follows closely, buoyed by growing clinical research and increasing industry acceptance of terpenes as effective agents in managing pain, inflammation, respiratory conditions, and mental health.

The fastest-growing segment is Aromatherapy & Wellness. In many ways, this is the segment that feels most natural for terpenes, and the numbers are beginning to reflect that. As stress, burnout, and mental well-being become increasingly central concerns for consumers around the world, the demand for effective, plant-based relaxation solutions is rising sharply.

Key Market Segments

By Type

- D-Limonene

- Pinene

- Myrcene

- Linalool

- Caryophyllene

- Other Terpenes

By Application

- Flavors & Fragrances

- Pharmaceuticals

- Cosmetics & Personal Care

- Food & Beverage

- Cleaning & Household Products

- Cannabis Products

By Source

- Plant-Based Terpenes

- Cannabis-Derived Terpenes

- Synthetic Terpenes

By Distribution Channel

- Direct/B2B Sales

- Specialty Chemical Distributors

- Online Retail

- Retail Stores

By End-User

- Consumer Goods

- Healthcare & Pharma

- Food Processing

- Aromatherapy & Wellness

- Industrial Applications

- Pesticides

- Other Industries

Market Dynamics

Challenges

The terpene industry remains highly exposed to feedstock volatility because gum turpentine, the primary source of alpha-pinene, beta-pinene, camphene, and terpineol, is produced as a co-product of rosin processing at a fixed ratio of approximately 0.13–0.25 tonnes per tonne of gum rosin. When rosin demand weakens, processing rates decline and turpentine supply contracts regardless of terpene demand. In Q1 2026, turpentine prices reached approximately USD 3,573/ton in the United States and USD 3,220/ton in Japan, contributing to downstream margin compression of roughly 12%–18% under spot procurement conditions.

Supply risks are further amplified by regional production constraints. China’s Guangdong, Guangxi, and Yunnan provinces, which collectively account for approximately 12%–13% of global gum turpentine supply, have experienced output reductions due to stricter environmental enforcement. At the same time, Brazil’s tapping season is largely limited to April–October, exposing global inventories to recurring shortfall risk during a 6–7 month period each year.

To mitigate these challenges, manufacturers are increasingly adopting multi-origin sourcing agreements, dual-supplier frameworks, and contingency logistics arrangements. However, establishing these procurement systems typically requires investments of approximately USD 0.5–1.5 million for mid-sized producers and still leaves exposure to supply disruptions and lead-time volatility of around 8–14 weeks during tight-market periods.

| Challenge | (~) % CAGR Friction Drag | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| Feedstock Supply Volatility & Co-Product Dependency | ~−1.8% | China, Brazil, Indonesia, India (key sourcing origins); North America downstream | Medium term (2–4 years) |

| Escalating Multi-Jurisdictional Regulatory Complexity | ~−1.2% | EU regulatory hubs (REACH/ECHA); North America (FDA/FEMA); cannabis-adjacent markets globally | Long term (≥4 years) |

| Climate-Driven Citrus & Pine Biomass Yield Erosion | ~−1.4% | APAC (China, India, Indonesia); Mediterranean EU; South America (Brazil) | Long term (≥4 years) |

| Biosynthetic Scale-Up & Fermentation Techno-Economic Gap | ~−0.9% | North America & EU (R&D-to-commercial pipeline); APAC contract manufacturing | Medium term (2–4 years) |

| Fragmented Quality Standardization & Adulteration Risk | ~−0.8% | Global; highest severity in APAC sourcing corridors and cannabis-derived streams | Medium term (2–4 years) |

| Specialized Talent Scarcity in Terpene Chemistry | ~−0.7% | Global; acutely in EU, North America, and emerging APAC innovation hubs | Long term (≥4 years) |

Opportunity

The terpene industry remains highly fragmented across citrus processors, essential-oil extractors, formulators, and specialty distributors, creating a significant consolidation opportunity. Rather than relying solely on organic demand growth, companies can generate value by integrating peel sourcing, terpene fractionation, downstream formulation, and global distribution networks through strategic acquisitions and portfolio optimization.

Roll-ups targeting regional assets in Brazil, Mexico, the United States, and Mediterranean Europe could deliver 6%–12% procurement savings, 3%–5% logistics savings, and approximately 200–600 basis points of margin improvement through by-product valorization and cross-selling into flavors, cleaners, and fragrance applications.

Greater scale also supports investments in fermentation partnerships, regulatory approvals, and multinational key-account management. As a result, successful consolidation and feedstock integration strategies could contribute approximately +1.9 percentage points of CAGR upside over time, although realization depends on effective M&A execution and operational integration.

| Opportunity | (~) % Potential CAGR Upside | Geographic Relevance | Execution Window |

|---|---|---|---|

| Bio-solvent substitution platforms | +2.1% | North America core, EU, China | Short term |

| Cannabis-adjacent beverage systems | +1.8% | North America core, EU selective, APAC pilots | Short term |

| Biopesticide terpene actives | +1.6% | LATAM, India, SE Asia, EU | Medium term |

| Fermentation-made terpene ingredients | +2.4% | US, EU, Japan, South Korea | Medium term |

| Flavor-to-functional nutraceuticals | +1.3% | US, EU, APAC premium | Medium term |

| Fragmented citrus terpene roll-ups | +1.9% | Brazil, Mexico, US, Mediterranean EU | Long term |

Drivers

A key growth driver for the terpene market is the improved valorization of citrus-processing by-products, particularly the extraction of d-limonene and orange terpenes from orange peel waste streams. Brazil’s 2025/26 orange crop is forecast at 330 million 90-pound boxes, equivalent to approximately 13.5 million metric tons, while global fresh orange production is expected to reach about 45.9 million tons, supported by larger harvests in Brazil and Egypt.

This recovery follows the severe 2024/25 Brazilian crop decline, when production was projected at only 232.38 million boxes, representing a 24.36% year-on-year decrease. The rebound is significant because terpene production economics are closely linked to peel availability and citrus-processing throughput.

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Natural fragrance and aroma capture in F&F formulations | +1.4% | EU core, North America core, APAC premium corridors | Medium term (2–4 years) |

| Bio-based solvent substitution in cleaners and industrial blends | +1.6% | North America core, EU core, APAC manufacturing belts | Short term (≤ 2 years) |

| Citrus by-product valorization improving d-limonene and orange terpene supply | +1.2% | Brazil, U.S., Mexico, EU import-linked markets | Short term (≤ 2 years) |

| Cosmetic compliance shifts favoring traceable natural ingredients | +0.9% | EU core, U.S., South Korea, India spill-over | Medium term (2–4 years) |

| Functional use in food, nutraceutical, and wellness formats | +1.0% | North America, EU, Japan, Australia, urban APAC | Medium term (2–4 years) |

| Process upgrades in extraction, quality control, and formulation efficiency | +0.7% | China, India, Brazil, EU specialty ingredient hubs | Long term (≥ 4 years) |

Restraints

Hazard classification and labeling requirements are creating increasing commercial friction for terpene products, particularly d-limonene-rich materials, which operate within a more closely regulated chemical safety environment in Europe and other developed markets. The European Chemicals Agency (ECHA) maintains harmonized classification requirements under the CLP Regulation, while the framework has been expanded through Delegated Regulation (EU) 2023/707, introducing additional hazard classes and compliance obligations.

The cumulative effect includes more frequent SDS updates, labeling modifications, customer EHS reviews, and additional insurance and logistics requirements. For specialty distributors, these factors can increase handling and compliance costs by approximately 4%–7%, slow qualification cycles in pharmaceutical and industrial cleaning applications, and encourage some buyers to adopt lower-complexity alternatives where performance differences are limited.

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Citrus feedstock volatility | −1.6% | Brazil core, U.S., EU importers, APAC buyers | Medium term |

| Fragrance compliance burden | −1.2% | EU core, UK aligned, global exporters to EU | Short term |

| Hazard labeling pressure | −0.9% | EU, UK, North America specialty chemicals | Medium term |

| Extraction cost inflation | −1.0% | EU, India, China, ASEAN processing hubs | Short term |

| Synthetic substitution risk | −0.8% | North America core, EU, China | Medium term |

| Traceability and sourcing friction | −0.7% | EU, Latin America supply base, APAC exporters | Long term |

Geopolitical Impact Analysis

The terpenes market around the globe faces various challenges and opportunities owing to geopolitical as well as trade issues since the production of terpenes requires agricultural sources as inputs. Usually, the extraction of terpenes takes place from sources like citrus fruits, pine trees, herbs, and cannabis plants, thereby causing fluctuations in their supply, pricing, and distribution due to various obstacles, such as trade restrictions, import tariffs, political conflicts, and transportation problems.

Another challenge that the terpenes market faces relates to regulations, since regulations concerning cannabis vary from one country to another, thus affecting the production and trade in cannabis-derived terpenes.

Certain regions have created growth opportunities by legalizing cannabis use, but others continue with their restrictive policies on cannabis use, thus posing certain restrictions on the trade and development of the terpenes market. Apart from regulations, there is an increasing interest among governments and consumers toward sustainability. Thus, it is necessary to comply with these changes in order to mitigate risks and ensure steady operations.

Regional Analysis

North America leads the global market for terpenes with a market share of 39.2%. North America’s growth drivers include the presence of cannabis, demand for natural flavors and fragrances, and usage in personal care products, wellness, food and beverages, and pharmaceuticals industries. United States is one of the key markets due to advanced extraction technologies and preference for natural and sustainable ingredients.

The Asia-Pacific region is the fastest-growing, projected to exhibit strong growth in the global terpenes market due to high consumer demand for natural products, growth in the food and beverages industry, and increasing use of botanical extracts in the cosmetic and personal care industry. Countries such as China, India, Japan, and South Korea are exhibiting strong trends for consumption of terpenes for flavors, fragrance, aromatherapy, and wellness.

Key Regions and Countries Covered in this Report

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

The terpenes industry is moderately fragmented with the presence of big flavor and fragrance makers, specialty chemicals makers, natural ingredients providers, and cannabis-focused terpene producers. Big players have a stronghold in the market owing to their advanced manufacturing capabilities, well-established distribution networks, and business relationships with food & beverages, cosmetics, pharmaceuticals, and consumer goods brands.

At the same time, the market is also seeing a growing wave of smaller, specialized players who are carving out their own space by focusing on niche applications, custom formulations, and highly targeted customer segments.

These emerging companies, particularly those operating in the cannabis, wellness, and natural personal care space, are bringing agility and innovation to the table that larger players often struggle to match. Their ability to respond quickly to shifting consumer preferences and develop tailor-made terpene solutions is gradually helping them build loyal customer bases, making the competitive landscape increasingly dynamic and one to watch closely in the years ahead.

Key Players

- Firmenich SA

- Givaudan

- Symrise AG

- International Flavors & Fragrances (IFF)

- Takasago International Corporation

- Sensient Technologies Corporation

- DSM-Firmenich

- Floraplex Terpenes

- True Terpenes

- Abstrax Tech Inc.

- Cedarome Canada Inc.

- Citrus and Allied Essences Ltd.

- Pine Mountain Botanicals

- Alpha Aromatics

- Amyris Inc.

Key Developments

- In March 2025, Givaudan expanded its natural ingredients portfolio by launching a new range of plant-derived terpene ingredients, developed in response to growing demand from flavors, fragrance, cosmetics, and wellness brands seeking cleaner and more sustainable formulations.

- In January 2025, Symrise AG introduced a series of custom terpene-based flavor and fragrance solutions targeting the premium wellness and personal care market, focusing on enhancing sensory profiles while meeting the rising consumer expectation for natural, traceable ingredients.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 1573.2 Mn |

| Forecast Revenue (2035) | USD 3844.6 Mn |

| CAGR (2026–2035) | 9.4% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020–2024 |

| Forecast Period | 2026–2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Type (D-Limonene, Pinene, Myrcene, Linalool, Caryophyllene, Other Terpenes), By Consumer (Government, Pharmaceutical, Chemicals, Paper and Pulp, Plastics, Pesticides, Water Treatment, Other Consumers), By Source (Plant-Based Terpenes, Cannabis-Derived Terpenes, Synthetic Terpenes), By Application (Flavors & Fragrances, Pharmaceuticals, Cosmetics & Personal Care, Food & Beverage, Cleaning & Household Products, Cannabis Products), By End-Use (Industry Consumer Goods, Healthcare & Pharma, Food Processing, Aromatherapy & Wellness, Industrial Applications), By Distribution Channel (Direct/B2B Sales, Specialty Chemical Distributors, Online Retail, Retail Stores) |

| Regional Analysis | North America – The US & Canada; Europe – Germany, France, The UK, Spain, Italy, Russia & CIS, Rest of Europe; APAC – China, Japan, South Korea, India, ASEAN & Rest of APAC; Latin America – Brazil, Mexico & Rest of Latin America; Middle East & Africa – GCC, South Africa, & Rest of MEA |

| Competitive Landscape | Firmenich SA, Givaudan, Symrise AG, International Flavors & Fragrances (IFF), Takasago International Corporation, Sensient Technologies Corporation, DSM-Firmenich, Floraplex Terpenes, True Terpenes, Abstrax Tech Inc., Cedarome Canada Inc., Citrus and Allied Essences Ltd., Pine Mountain Botanicals, Alpha Aromatics, Amyris Inc. |

| Customization Scope | Customization for segments and region/country-level will be provided. Moreover, customization can be tailored to the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |