Quick Navigation

Report Overview

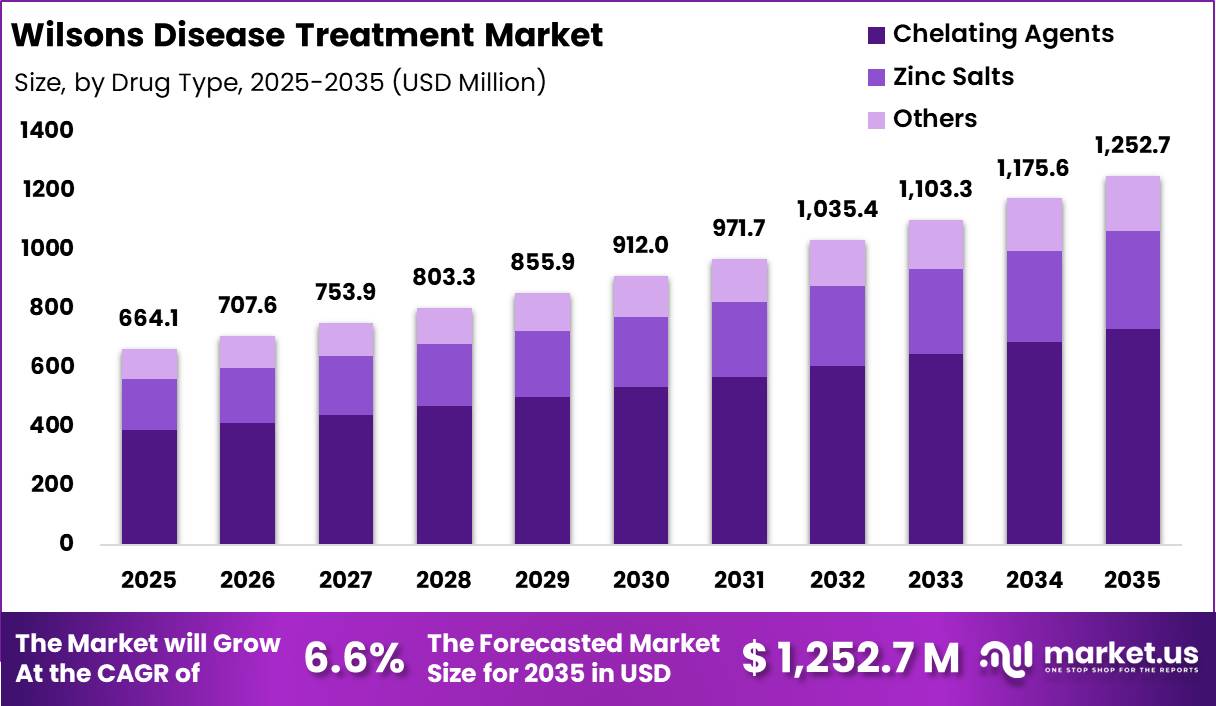

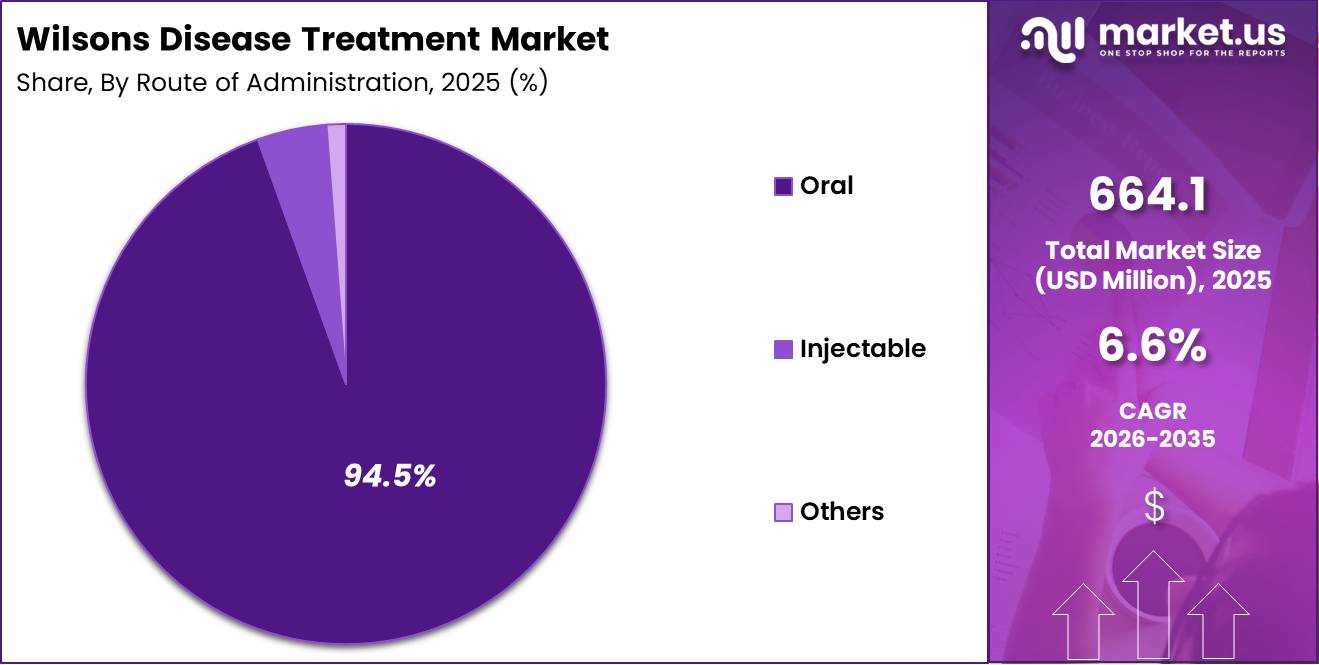

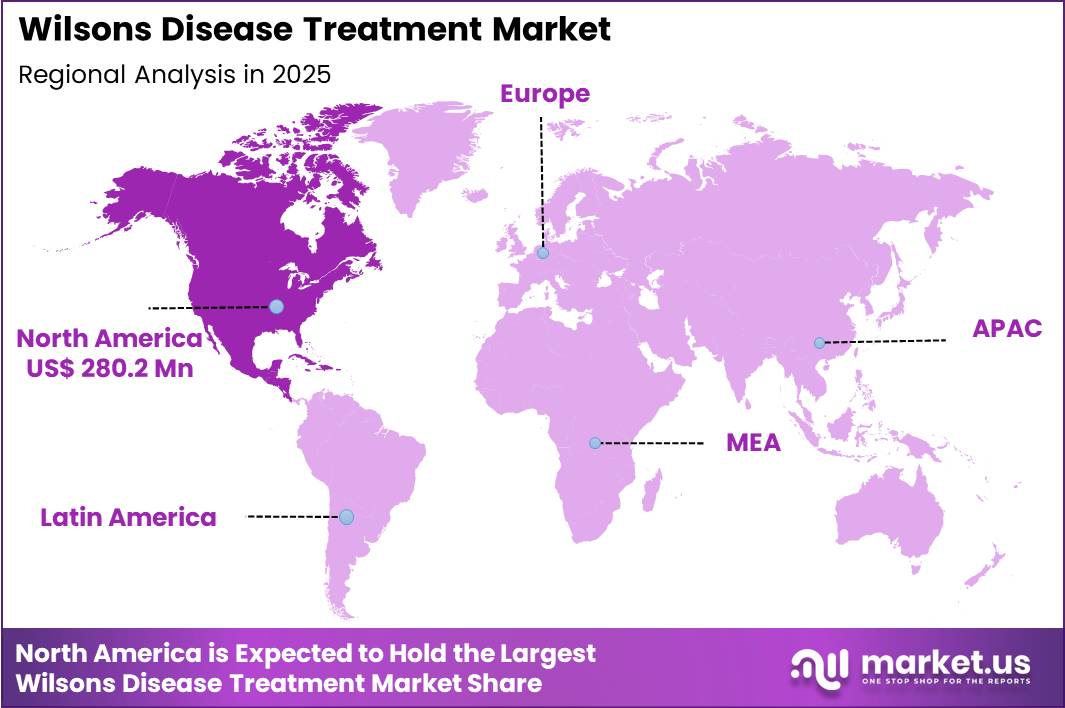

Global Wilsons Disease Treatment Market size is expected to be worth around US$ 1,252.7 Million by 2035 from US$ 664.1 Million in 2025, growing at a CAGR of 6.6% during the forecast period from 2026 to 2035. In 2025, North America led the market, achieving over 42.2% share with a revenue of US$ 280.2 Million.

Wilson’s disease treatment encompasses therapeutic approaches designed to reduce the toxic accumulation of copper in the body caused by mutations in the ATP7B gene, which impair normal copper metabolism. The disease is a rare inherited disorder characterized by excessive copper deposition in the liver, brain, eyes, and other organs, leading to progressive hepatic, neurological, and psychiatric complications if left untreated.

According to the U.S. National Institute of Diabetes and Digestive and Kidney Diseases (NIDDK), Wilson’s disease requires lifelong management with copper-chelating agents and zinc therapies to prevent organ damage and maintain normal copper balance. Untreated disease can result in severe liver failure, neurological impairment, and other life-threatening complications. Recent estimates indicate that Wilson’s disease affects approximately 1 in 30,000 individuals globally, while carrier frequency is estimated at around 1 in 90 people.

The Wilson’s disease treatment market is experiencing steady growth, supported by increasing disease awareness, advancements in diagnostic technologies, and expanding genetic screening programs. Earlier identification of patients through family screening, biochemical testing, and molecular diagnostics has improved treatment initiation rates and long-term clinical outcomes. The National Institute of Diabetes and Digestive and Kidney Diseases reports that symptoms often emerge only after copper accumulates in tissues, making early diagnosis essential for preventing irreversible organ damage.

Treatment options primarily include copper-chelating drugs such as penicillamine and trientine, along with zinc salts that inhibit intestinal copper absorption. Continuous innovation in drug formulations is contributing to improved patient adherence and safety profiles. Newer therapies are being developed to minimize adverse effects, particularly neurological worsening associated with some conventional chelators.

In addition, increased healthcare expenditure on rare diseases and growing support from regulatory agencies for orphan drug development are fostering therapeutic advancements. As healthcare systems continue to emphasize early detection and lifelong disease management, demand for effective Wilson’s disease treatments is expected to expand steadily over the coming years, supporting sustained growth across the global market.

Key Takeaways

- Market Size: Global Wilsons Disease Treatment Market size is expected to be worth around US$ 1,252.7 Million by 2035 from US$ 664.1 Million in 2025.

- Market Share: The market growing at a CAGR of 6.6% during the forecast period from 2026 to 2035.

- Drug Type Analysis: Chelating agents dominated the Wilson’s disease treatment market, accounting for 58.6% of the total market share in 2025.

- Route of Administration Analysis: The oral route of administration dominated the Wilson’s disease treatment market with a 94.5% market share in 2025.

- End User Analysis: Hospitals held the largest share of the Wilson’s disease treatment market, accounting for 58.4% of total revenue in 2025.

- Regional Analysis: In 2025, North America led the market, achieving over 42.2% share with a revenue of US$ 280.2 Million.

Drug Type Analysis

Chelating agents dominated the Wilson’s disease treatment market, accounting for 58.6% of the total market share in 2025. The segment’s leadership is attributed to the established role of copper-chelating therapies as the first-line treatment for symptomatic patients. Drugs such as penicillamine and trientine are widely prescribed due to their ability to bind excess copper and facilitate its excretion from the body.

Increasing diagnosis rates of Wilson’s disease and long-term treatment requirements continue to support demand for chelating agents across developed and emerging healthcare markets. Furthermore, ongoing efforts to improve drug tolerability and patient compliance are expected to reinforce segment growth over the forecast period.

The zinc salts segment represents the second-largest share of the market. Zinc-based therapies are commonly used for maintenance treatment and in presymptomatic patients, as they reduce intestinal copper absorption and help maintain copper balance. Their favorable safety profile and suitability for long-term use contribute to growing adoption.

The others segment includes combination therapies, investigational treatments, and supportive medications used to manage disease-related complications. Continued research into novel therapeutic approaches and rare disease drug development is expected to create growth opportunities within this segment.

Route of Administration Analysis

The oral route of administration dominated the Wilson’s disease treatment market with a 94.5% market share in 2025. The segment’s strong position is primarily driven by the availability of most approved Wilson’s disease therapies in oral formulations, including chelating agents and zinc salts.

Oral medications offer significant advantages such as ease of administration, improved patient convenience, reduced hospitalization requirements, and enhanced adherence to lifelong treatment regimens. Since Wilson’s disease requires continuous management to prevent copper accumulation and organ damage, oral therapies remain the preferred option among healthcare providers and patients. Growing awareness of early diagnosis and long-term disease management further supports the dominance of this segment.

The injectable segment accounts for a relatively smaller market share and is generally utilized in specialized clinical settings, severe disease cases, or situations where oral treatment is not feasible. Although limited in adoption, injectable therapies play a critical role in acute disease management and complex patient cases.

The others segment includes alternative and emerging administration approaches currently under development. Advances in drug delivery technologies and ongoing research aimed at improving therapeutic effectiveness may contribute to gradual growth within this segment during the forecast period.

End User Analysis

Hospitals held the largest share of the Wilson’s disease treatment market, accounting for 58.4% of total revenue in 2025. The segment’s dominance is supported by the complex nature of Wilson’s disease diagnosis and management, which often requires multidisciplinary care involving hepatologists, neurologists, genetic specialists, and other healthcare professionals.

Hospitals serve as primary centers for diagnostic testing, treatment initiation, monitoring of disease progression, and management of severe complications. The availability of advanced diagnostic infrastructure and specialized treatment facilities further strengthens the position of hospitals in the market.

The specialty clinics segment represents a significant share of the market due to the growing availability of dedicated rare disease and hepatology centers. These facilities provide specialized monitoring, personalized treatment plans, and long-term patient follow-up, contributing to increasing patient preference for outpatient care.

The homecare settings segment is experiencing steady growth as oral treatment options enable patients to manage their condition outside institutional healthcare environments. Improved patient education and remote monitoring capabilities are further supporting this trend.

The others segment includes research institutions, academic medical centers, and community healthcare facilities involved in disease management and clinical research activities.

Key Market Segments

By Drug Type

- Chelating Agents

- Zinc Salts

- Others

By Route of Administration

- Oral

- Injectable

- Others

By End User

- Hospitals

- Specialty Clinics

- Homecare Settings

- Others

Driving Factors

Growing Diagnosis and Lifelong Treatment Requirement

The Wilson Disease Treatment Market is primarily driven by the increasing identification of patients through improved genetic testing, biochemical screening, and greater awareness among healthcare professionals. Wilson disease is a rare inherited disorder caused by mutations in the ATP7B gene, resulting in excessive copper accumulation in the liver, brain, and other organs.

According to the U.S. National Institute of Diabetes and Digestive and Kidney Diseases (NIDDK), untreated copper accumulation can lead to life-threatening organ damage, making early diagnosis and continuous treatment essential. Lifelong therapy with copper-chelating agents and zinc-based treatments is recommended to prevent disease progression and organ failure.

The condition affects approximately 1 in 30,000 individuals worldwide, while the carrier frequency is estimated at 1 in 90 people. Furthermore, studies suggest that genetic prevalence may be higher than clinically diagnosed cases, indicating a significant pool of undiagnosed patients.

Increased family screening programs and broader access to genetic testing are improving diagnosis rates, thereby expanding the demand for long-term pharmacological management and supporting sustained growth of the Wilson disease treatment market.

Trending Factors

Increasing Adoption of Precision Diagnostics and Genetic Screening

A significant trend shaping the Wilson Disease Treatment Market is the growing integration of genetic testing and precision diagnostics into routine clinical practice. Healthcare organizations and academic institutions increasingly recommend ATP7B mutation analysis alongside traditional diagnostic methods such as serum ceruloplasmin measurement and 24-hour urinary copper testing.

According to GeneReviews and NIH resources, screening of first-degree relatives of affected individuals is strongly recommended because early intervention can prevent irreversible liver and neurological damage. Research has identified more than 300 ATP7B mutations associated with the disease, highlighting the need for advanced molecular diagnostics. As genomic sequencing technologies become more accessible and cost-effective, clinicians are able to detect asymptomatic or pre-symptomatic patients earlier than before.

This trend is particularly important because symptoms may appear anytime from childhood to adulthood, and delayed diagnosis remains common. The increasing use of precision medicine approaches is also supporting the development of targeted therapies and personalized treatment strategies. Consequently, the combination of genetic screening, family-based testing, and early disease detection is becoming a key trend influencing treatment adoption and patient management across global healthcare systems.

Restraining Factors

Limited Disease Awareness and Diagnostic Delays

According to BMJ Best Practice, Wilson disease is frequently misdiagnosed or diagnosed late because its manifestations overlap with several liver and neurological disorders. Delayed diagnosis can lead to severe complications including cirrhosis, acute liver failure, neurological impairment, and psychiatric disorders before treatment is initiated.

Furthermore, definitive diagnosis often requires multiple laboratory assessments, ophthalmologic examinations, imaging studies, and genetic testing, which may not be readily available in all healthcare settings. In low- and middle-income regions, limited access to specialized diagnostic facilities further restricts early disease identification. These factors reduce treatment initiation rates and create challenges for healthcare providers and pharmaceutical manufacturers, thereby limiting the full growth potential of the Wilson disease treatment market.

Opportunity

Development of Novel Therapies and Expansion of Rare Disease Programs

The Wilson Disease Treatment Market presents substantial opportunities through the development of innovative therapies and expanding government-supported rare disease initiatives. Current management primarily relies on lifelong oral pharmacotherapy, including copper-chelating agents and zinc therapy. However, there remains a significant unmet need for treatments that offer improved efficacy, better safety profiles, and enhanced patient adherence.

According to NIH-supported GeneReviews, lifelong treatment is necessary because inadequate therapy can result in copper reaccumulation and disease progression. Advances in genetic research have improved understanding of ATP7B mutations, creating opportunities for gene-based and disease-modifying therapeutic approaches.

In addition, many countries are strengthening rare disease frameworks that encourage orphan drug development through regulatory incentives, research funding, and accelerated approval pathways. The NIH Genetic and Rare Diseases Information Center (GARD) recognizes Wilson disease as a rare inherited disorder requiring specialized clinical management.

Increased investment in rare disease research, coupled with rising adoption of genomic medicine, is expected to support clinical trials and therapeutic innovation. These developments create favorable conditions for new product launches and expanded treatment accessibility, generating long-term growth opportunities within the global Wilson disease treatment market.

Regional Analysis

North America dominated the Wilson’s Disease Treatment Market in 2025, accounting for over 42.2% of the global market and generating revenue of US$ 280.2 million. The region’s leadership can be attributed to its advanced healthcare infrastructure, strong presence of specialized treatment centers, and high awareness levels regarding rare genetic disorders. The widespread availability of diagnostic technologies and established screening programs has contributed to earlier detection and timely treatment initiation, supporting market growth across the region.

The United States represented the largest share within North America due to substantial healthcare expenditure, favorable reimbursement policies, and ongoing research activities focused on rare disease management. The presence of major pharmaceutical companies and active clinical development programs has further strengthened the regional market landscape. In addition, government support for orphan drug development and regulatory incentives have encouraged the introduction of innovative therapies for Wilson’s disease.

Canada also contributed significantly to regional revenue, supported by increasing access to specialized care and growing awareness among healthcare professionals regarding the diagnosis and management of Wilson’s disease. Rising investments in genetic testing and personalized medicine initiatives have enhanced treatment accessibility across the country.

Furthermore, the growing adoption of chelation therapies and zinc-based treatments, coupled with continuous advancements in rare disease research, is expected to sustain North America’s leading position throughout the forecast period. The region is anticipated to remain a key hub for innovation, clinical trials, and commercialization of novel Wilson’s disease treatment options.

Key Regions and Countries

North America

- The US

- Canada

Europe

- Germany

- France

- The U.K.

- Italy

- Spain

- Russia & CIS

- Rest of Europe

Asia Pacific

- China

- India

- Japan

- South Korea

- ASEAN

- Australia & New Zealand

- Rest of Asia Pacific

Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

Latin America

- Brazil

- Mexico

- Rest of Latin America

Key Players Analysis

The Wilson’s Disease Treatment Market is characterized by the presence of pharmaceutical companies focused on rare disease therapeutics, copper-chelating agents, and supportive treatment solutions. Key market participants compete through product innovation, regulatory approvals, strategic collaborations, and geographic expansion initiatives. Companies are increasingly investing in research and development activities to improve treatment efficacy, reduce adverse effects, and enhance patient compliance.

Leading players are concentrating on expanding their rare disease portfolios by developing next-generation therapies and exploring novel treatment mechanisms. Strategic partnerships with research institutions and healthcare organizations are enabling companies to strengthen their clinical pipelines and accelerate product commercialization. Additionally, regulatory incentives for orphan drugs have encouraged manufacturers to increase investments in Wilson’s disease treatment development.

Market participants are also focusing on improving patient access through expanded distribution networks and reimbursement support programs. The competitive landscape remains moderately consolidated, with established pharmaceutical firms leveraging their expertise in rare genetic disorders to maintain market positions. Continuous advancements in precision medicine and gene-based therapeutic approaches are expected to create new growth opportunities for key players in the coming years.

Market Key Players

- Alexion Pharmaceuticals (AstraZeneca)

- Bausch Health Companies Inc.

- Orphalan SA

- Tsumura & Company

- Apotex Inc.

- Teva Pharmaceutical Industries Ltd.

- Mylan N.V. (Viatris)

- Sun Pharmaceutical Industries Ltd.

- Dr. Reddy’s Laboratories Ltd.

- Lupin Limited

- Novartis AG

- Pfizer Inc.

- Sanofi (Kadmon Holdings LLC)

- Wilson Therapeutics AB

- Valeant Pharmaceuticals

- Others

Recent Developments

- January 2026 – Cyprium Therapeutics, a subsidiary of Fortress Biotech, received U.S. regulatory approval for CUTX-101, a copper histidinate therapy associated with rare copper metabolism disorders. The approval reinforced industry interest in copper-related rare disease therapeutics and highlighted continued investment activity within the broader copper metabolism treatment segment.

- January 2025 – Eton Pharmaceuticals strengthened its presence in the Wilson disease market through the acquisition of Galzin® (zinc acetate), an FDA-approved maintenance therapy for Wilson disease. The transaction expanded Eton’s rare disease portfolio and reinforced its commitment to supporting patients with ultra-rare metabolic disorders.

- May 2025 – Monopar Therapeutics reported new long-term efficacy and safety data for ALXN1840 (tiomolybdate choline) at the European Association for the Study of the Liver (EASL) Congress 2025. The presentation highlighted the potential of ALXN1840 as an innovative treatment option for Wilson disease and supported ongoing development efforts in this rare genetic disorder.

- June 2025 – Orphalan SA entered into a strategic partnership with MAP International and the Wilson Disease Association to expand access to Wilson disease treatment in underserved regions. Through this initiative, Orphalan committed to donating supplies of Cuvrior® (trientine tetrahydrochloride) to support patients in developing countries, strengthening global access to therapy.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | US$ 664.1 Million |

| Forecast Revenue (2035) | US$ 1,252.7 Million |

| CAGR (2026-2035) | 6.6% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Drug Type(Chelating Agents, Zinc Salts, Others) By Route of Administration (Oral, Injectable, Others) By End User ( Hospitals, Specialty Clinics, Homecare Settings, Others) |

| Regional Analysis | North America – The US, Canada; Europe – Germany, France, U.K., Italy, Spain, Russia & CIS, Rest of Europe; Asia Pacific – China, India, Japan, South Korea, ASEAN, Australia & New Zealand, Rest of Asia Pacific; Middle East & Africa – GCC, South Africa, Rest of Middle East & Africa; Latin America – Brazil, Mexico, Rest of Latin America |

| Competitive Landscape | Alexion Pharmaceuticals (AstraZeneca), Bausch Health Companies Inc., Orphalan SA, Tsumura & Company, Apotex Inc., Teva Pharmaceutical Industries Ltd., Mylan N.V. (Viatris), Sun Pharmaceutical Industries Ltd., Dr. Reddy’s Laboratories Ltd., Lupin Limited, Novartis AG, Pfizer Inc., Sanofi (Kadmon Holdings LLC), Wilson Therapeutics AB, Valeant Pharmaceuticals, Others, |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |