Global Vitamin C Serum Market Size, Share, Growth Analysis By Formulation Type (Stabilized Derivatives, Pure Ascorbic Acid, Blended Serums), By Concentration (10% to 20%, Below 10%, 20% and Above), By Distribution Channel (Online, Hypermarkets & Supermarkets, Specialty Stores, Pharmacies & Drugstores, Others), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2026-2035

- Published date: March 2026

- Report ID: 181668

- Number of Pages: 305

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

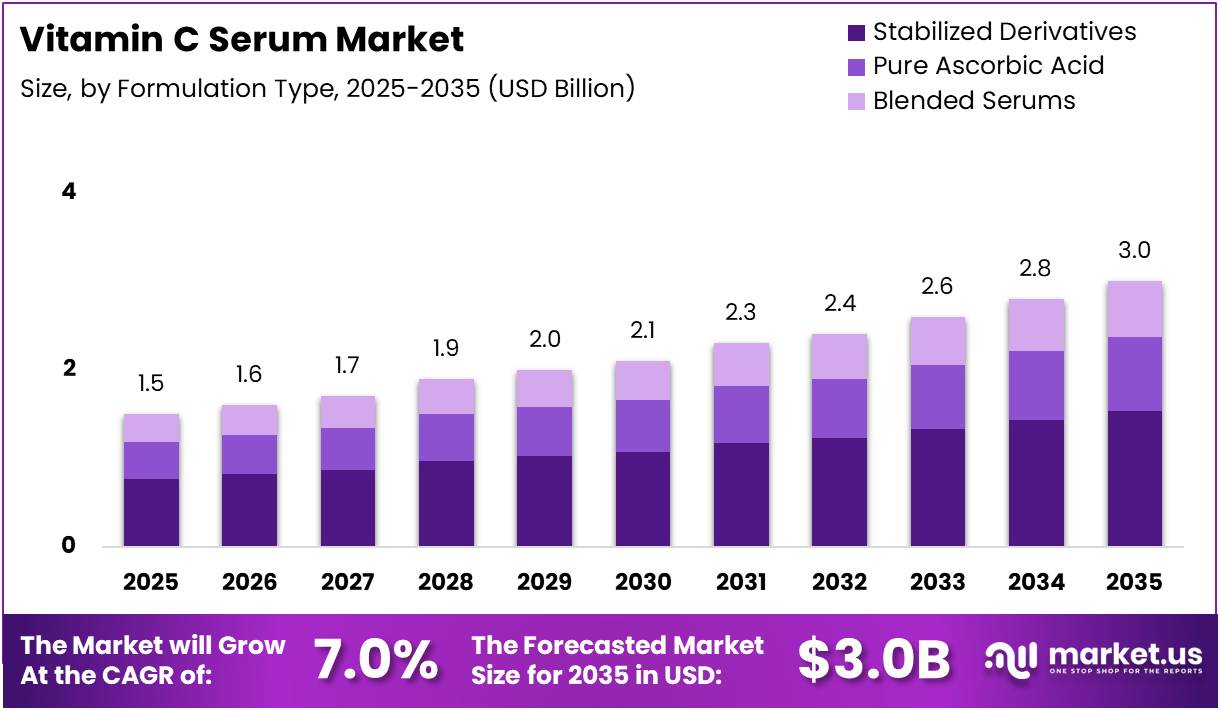

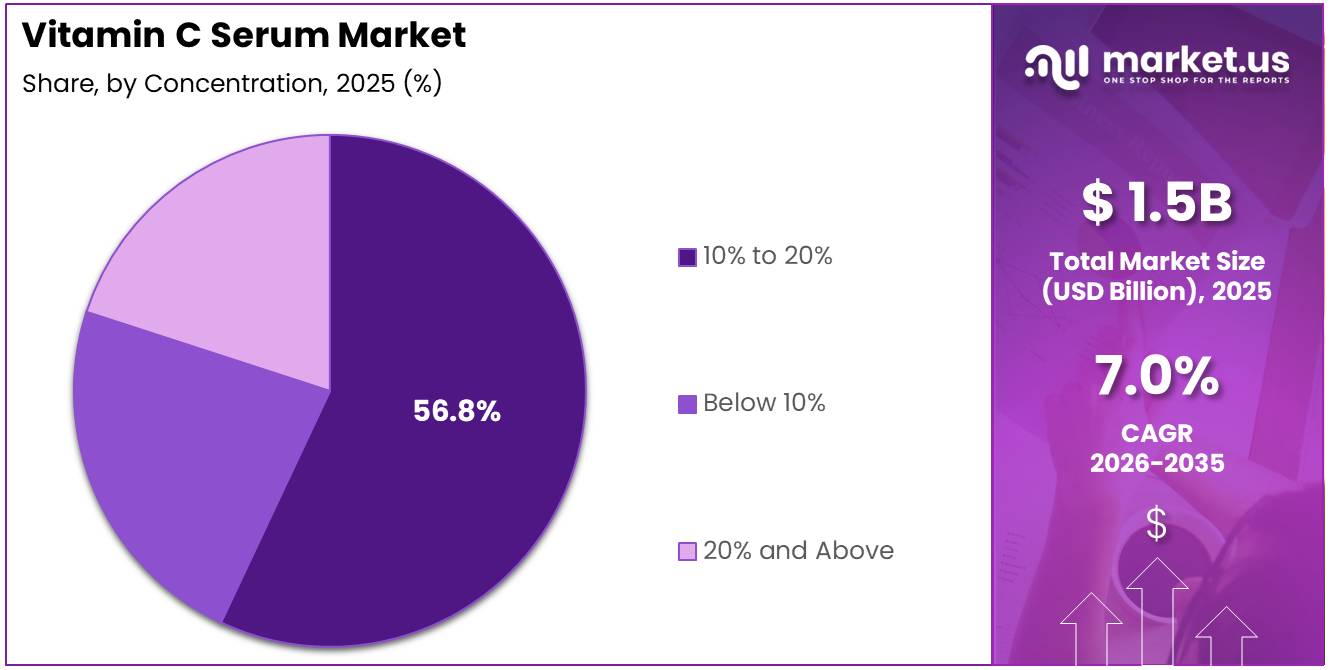

The Global Vitamin C Serum Market size is expected to be worth around USD 3.0 Billion by 2035 from USD 1.5 Billion in 2025, growing at a CAGR of 7.0% during the forecast period 2026 to 2035.

Vitamin C serums are topical skincare formulations containing ascorbic acid or its stabilized derivatives. These products are widely used to brighten skin tone, reduce hyperpigmentation, and protect against environmental damage. Moreover, they represent one of the fastest-growing categories in the global premium skincare segment.

Consumer interest in science-backed and dermatologist-recommended skincare ingredients has risen sharply in recent years. Growing awareness of antioxidant benefits is driving strong demand for Vitamin C serums worldwide. Consequently, brands are expanding their product lines to meet the diverse needs of aging-conscious, anti-aging product seeking and skin-brightening consumers globally.

The market presents considerable opportunities in both developed and emerging economies. Rising disposable incomes, growing beauty consciousness, and greater access to skincare education are key enablers. Additionally, the rapid expansion of e-commerce platforms has made premium Vitamin C serum products accessible to a much wider global consumer base.

Regulatory bodies such as the FDA and the European Medicines Agency continue to establish guidelines for cosmetic ingredient safety and efficacy. These frameworks build consumer trust and improve product quality standards across markets. Therefore, well-formulated and compliant Vitamin C serums maintain a stronger position in regulated markets across North America and Europe.

According to affordable.skin, 45% of users under age 30 use Vitamin C serums daily, while 38% of consumers aged 30 to 50 incorporate them regularly into their routines. Additionally, 30% of users aged 50 and above also use these products, reflecting broad multi-generational appeal across global skincare consumers.

According to sfc.ac.in, 37.2% of consumers choose Vitamin C specifically for skin brightening, ranking it above creams and alternative treatments as the top method. Furthermore, according to journal.pandawainstitute.com, a Vitamin C derivative serum demonstrated a 20.35% increase in skin firmness and a 13.71% reduction in wrinkles in clinical assessments.

These findings reinforce the clinical credibility of Vitamin C-based formulations in the global skincare industry. Brands investing in dermatologically validated and stabilized products are well-positioned to build long-term consumer loyalty. Consequently, the global Vitamin C serum market is expected to sustain strong momentum throughout the forecast period.

Key Takeaways

- The Global Vitamin C Serum Market is valued at USD 1.5 Billion in 2025 and is projected to reach USD 3.0 Billion by 2035.

- The market is growing at a CAGR of 7.0% during the forecast period 2026 to 2035.

- By Formulation Type, Stabilized Derivatives holds the dominant position with a 51.3% market share in 2025.

- By Concentration, the 10% to 20% segment leads with a 56.8% share in 2025.

- By Distribution Channel, the Online segment captures the largest share at 56.8% in 2025.

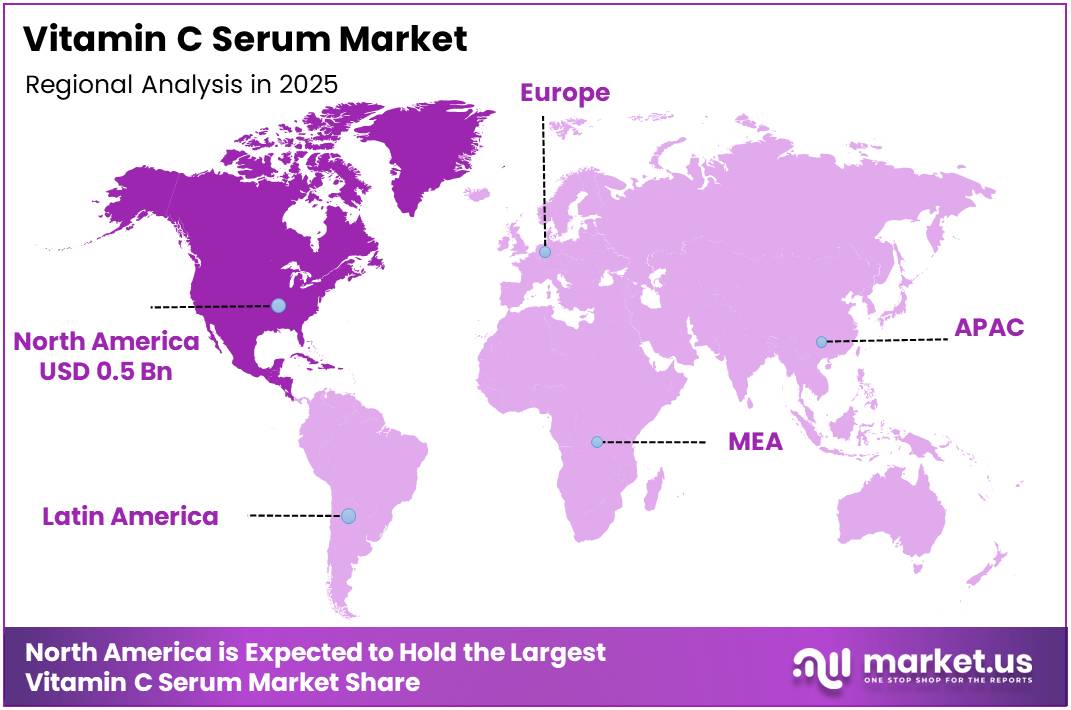

- North America dominates the regional landscape with a 37.90% market share, valued at USD 0.5 Billion in 2025.

By Formulation Type Analysis

Stabilized Derivatives dominates with 51.3% due to enhanced product stability, reduced oxidation risk, and broader consumer compatibility.

In 2025, Stabilized Derivatives held a dominant market position in the By Formulation Type segment of the Vitamin C Serum Market, with a 51.3% share. These formulations offer superior shelf stability and reduced sensitivity to light and air. Moreover, they are widely preferred by brands for delivering consistent performance and a better experience across diverse skin types.

Pure Ascorbic Acid remains a well-recognized and clinically potent form of Vitamin C in topical skincare. However, its high sensitivity to oxidation presents formulation and storage challenges for both brands and consumers. Consequently, it appeals primarily to results-driven users who are informed about proper product usage and storage practices.

Blended Serums combine Vitamin C with complementary ingredients such as hyaluronic acid, niacinamide, or peptides to address multiple skin concerns simultaneously. This sub-segment is gaining traction among consumers seeking simplified yet effective skincare routines. Additionally, blended formulations provide brands with a meaningful opportunity to differentiate their offerings in a competitive market.

By Concentration Analysis

10% to 20% concentration dominates with 56.8% due to its proven balance of visible efficacy and tolerability across skin types.

In 2025, 10% to 20% held a dominant market position in the By Concentration segment of the Vitamin C Serum Market, with a 56.8% share. This concentration range is widely recommended for delivering visible brightening and anti-aging results without causing skin irritation. Moreover, it remains the most broadly tolerated option across a wide range of consumer skin types globally.

Below 10% concentration serums are formulated specifically for individuals with sensitive or reactive skin. These gentle products are often recommended for first-time Vitamin C users and those prone to redness or irritation. Therefore, they are commonly positioned as entry-level skincare options that allow cautious consumers to build tolerance gradually and safely.

20% and Above concentration serums are designed for experienced users seeking intensive and faster-acting results. According to GQ, higher concentrations such as 23 to 30% deliver quicker improvements for dark spots but are best suited for those confident in their skin’s tolerance. Consequently, this sub-segment appeals to a specialized and results-oriented consumer base.

By Distribution Channel Analysis

Online channel dominates with 56.8% due to convenience, wide product access, and the growing influence of digital beauty content.

In 2025, Online held a dominant market position in the By Distribution Channel segment of the Vitamin C Serum Market, with a 56.8% share. E-commerce platforms and direct-to-consumer models offer consumers convenient access to a wide range of serum options at competitive prices. Additionally, influencer-driven campaigns, personalized digital consultations, and subscription-based skincare models are further accelerating online serum discovery and sales globally.

Hypermarkets and Supermarkets serve as key mass-market retail channels for Vitamin C serums, offering broad product visibility and wide consumer accessibility. These outlets attract value-conscious shoppers and support mainstream skincare product discovery at significant scale. Moreover, in-store promotions, bundled offers, and prominent shelf placement continue to drive impulse purchases among everyday beauty consumers.

Specialty Stores provide a carefully curated selection of premium and professional-grade Vitamin C serums to well-informed skincare consumers. These retail environments support expert-guided purchasing decisions and attract shoppers seeking higher-end formulations with proven efficacy. Furthermore, trained beauty consultants and exclusive product ranges give specialty stores a strong competitive advantage in the premium skincare segment.

Pharmacies and Drugstores play a significant role in distributing dermatologist-recommended and clinically backed Vitamin C serums to consumers. Shoppers rely on these trusted retail channels for regulated and safety-verified skincare products that meet established quality standards. Moreover, pharmacist guidance and in-store consultations further support informed purchasing decisions among health-conscious skincare consumers.

Others category encompasses beauty salons, spas, and direct sales channels serving specialized consumer needs. This segment supports niche skincare preferences and enables personalized product recommendations in professional settings. Additionally, direct-to-consumer sales through brand-owned outlets and wellness centers are gradually expanding the reach of premium Vitamin C serum products globally.

Key Market Segments

By Formulation Type

- Stabilized Derivatives

- Pure Ascorbic Acid

- Blended Serums

By Concentration

- 10% to 20%

- Below 10%

- 20% and Above

By Distribution Channel

- Online

- Hypermarkets & Supermarkets

- Specialty Stores

- Pharmacies & Drugstores

- Others

Drivers

Rising Demand for Skin Brightening, Antioxidant Protection, and Science-Backed Ingredients Drives Vitamin C Serum Market Growth

Consumer focus on achieving brighter and more even skin tones has become a primary skincare goal across multiple age groups and demographics. Vitamin C serums are widely regarded as effective solutions for reducing hyperpigmentation and improving overall skin clarity. Consequently, demand for targeted brightening formulations has grown steadily across both premium and mass-market skincare segments globally.

Growing awareness of pollution and UV-related skin damage has prompted consumers to prioritize antioxidant-rich skincare in their daily routines. Vitamin C is increasingly valued for its free radical neutralizing properties and photoprotective benefits. Therefore, urban consumers and those in high-pollution environments are adopting Vitamin C serums as essential protective skincare products.

The increasing preference for dermatologist-recommended and scientifically validated skincare ingredients is supporting broader market adoption. Consumers are becoming more ingredient-aware and selective when evaluating product efficacy claims. Moreover, clinical endorsements and greater formulation transparency are reinforcing consumer confidence and sustaining the long-term growth trajectory of the Vitamin C serum market.

Restraints

Stability Issues and Formulation Complexity Limit Market Growth for Vitamin C Serums

Vitamin C, particularly in its pure ascorbic acid form, is highly sensitive to light, air, and temperature fluctuations. This oxidation susceptibility significantly reduces product shelf life and overall effectiveness over time. Consequently, consumers may experience diminishing results with improperly stored or older products, leading to dissatisfaction and reduced brand loyalty.

Developing a stable and consistently effective Vitamin C serum requires advanced formulation expertise and specialized packaging solutions. Many brands struggle to maintain uniform potency across product batches, resulting in variable consumer experiences. Therefore, inconsistent product performance can erode consumer trust and limit repeat purchases, particularly in the competitive mid-tier skincare segment.

The combination of stability challenges and formulation complexity also increases manufacturing costs for brands. Smaller companies and new market entrants may find it difficult to achieve both affordability and product quality simultaneously. Additionally, the need for specialized storage and distribution conditions adds further logistical and financial burdens throughout the supply chain.

Growth Factors

Advanced Stabilized Formulations, Personalized Skincare, and E-Commerce Expansion Drive Vitamin C Serum Market Growth

The development of advanced stabilized Vitamin C derivatives is among the most significant growth catalysts for the market. Innovations such as encapsulated ascorbic acid and next-generation derivatives offer improved absorption, longer shelf life, and enhanced efficacy. Consequently, these advancements are attracting both new consumers and existing skincare users seeking higher-performing daily serum solutions.

Growing consumer interest in personalized skincare tailored to individual skin types and specific concerns is creating new market opportunities. Brands offering customized Vitamin C formulations are gaining a meaningful competitive advantage in crowded market environments. Moreover, advances in skin diagnostic technology are enabling more targeted product recommendations, driving adoption across a broader range of consumer profiles.

The rapid growth of e-commerce platforms and direct-to-consumer skincare brands is creating new and efficient distribution pathways for manufacturers. Online channels allow brands to reach previously underserved markets cost-effectively and at greater speed. Additionally, subscription-based skincare models and digital consultations are supporting consistent sales volumes and improving long-term customer retention in the Vitamin C serum category.

Emerging Trends

Clean Beauty, Social Media Influence, and Combination Formulas Shape Emerging Trends in the Vitamin C Serum Market

The clean beauty movement is reshaping consumer expectations across the global skincare industry at a rapid pace. Shoppers increasingly demand ingredient transparency, minimal synthetic additives, and ethically sourced components in their Vitamin C serums. Consequently, brands prioritizing clean label formulations and open communication about ingredient sourcing are earning stronger consumer trust and retention.

Social media platforms and beauty influencers continue to play a major role in shaping skincare purchasing decisions globally. Product endorsements, tutorial content, and before-and-after results shared by influencers drive strong consumer interest in Vitamin C serums. Moreover, user-generated content and peer reviews on platforms like Instagram and TikTok are accelerating product discovery and widespread adoption.

Consumers are increasingly seeking multi-benefit serums that combine Vitamin C with complementary active ingredients such as hyaluronic acid and niacinamide. These combination formulas address multiple skin concerns simultaneously, offering greater value and routine simplicity. Therefore, innovation in blended formulations is becoming a key differentiator for brands competing in the premium and science-backed skincare segment.

Regional Analysis

North America Dominates the Vitamin C Serum Market with a Market Share of 37.90%, Valued at USD 0.5 Billion

North America leads the global Vitamin C Serum Market, accounting for a 37.90% share valued at USD 0.5 Billion in 2025. The region benefits from high skincare awareness, strong consumer spending power, and a well-established omnichannel retail infrastructure. Moreover, growing demand for dermatologist-recommended and science-backed formulations continues to support robust market growth across the United States and Canada.

Europe Vitamin C Serum Market Trends

Europe represents a mature and innovation-driven market for Vitamin C serums, with consumers in Germany, France, and the UK showing strong preference for clinically validated and clean beauty formulations. Strict EU regulatory standards ensure high product quality and safety, building widespread consumer confidence. Furthermore, premium skincare adoption continues to grow steadily across established European markets.

Asia Pacific Vitamin C Serum Market Trends

Asia Pacific is the fastest-growing regional market for Vitamin C serums, driven by rising middle-class incomes and a strong beauty culture across China, Japan, South Korea, and India. The influence of K-beauty trends and expanding social media adoption are fueling demand for brightening skincare products. Consequently, this region presents significant opportunities for both global and local brands.

Middle East and Africa Vitamin C Serum Market Trends

The Middle East and Africa market for Vitamin C serums is expanding gradually, supported by rising urbanization and growing awareness of skincare routines. Consumers in GCC countries are increasingly adopting premium brightening skincare products. However, price sensitivity across parts of Africa may limit the near-term penetration of premium-tier formulations in these developing consumer markets.

Latin America Vitamin C Serum Market Trends

Latin America is an emerging market for Vitamin C serums, with Brazil and Mexico serving as the primary demand drivers in the region. Rising disposable incomes, growing beauty awareness, and increased digital access are supporting market expansion. Additionally, the growth of local skincare brands is improving product availability and affordability for a broader regional consumer base.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

L’Oréal S.A. is one of the world’s leading beauty and skincare conglomerates, maintaining a prominent position in the global Vitamin C Serum Market. The company leverages extensive research and development capabilities to deliver high-performance formulations across its diverse brand portfolio. Moreover, its strategic acquisitions and digital-first approach continue to reinforce its leadership in the premium skincare segment.

Galderma S.A. brings a strong dermatological heritage to the Vitamin C serum category, offering clinically backed and physician-endorsed skincare solutions. Its focus on science-driven formulations gives it a distinct advantage across medical and professional skincare distribution channels. Consequently, Galderma remains a trusted and credible name among consumers and dermatologists seeking proven Vitamin C-based treatments.

Amorepacific Group Inc. is a key player in the Asia Pacific skincare market, recognized for its innovation in K-beauty-inspired formulations. The company combines traditional ingredient knowledge with modern biotechnology to deliver effective brightening serum solutions for consumers. Furthermore, its growing international footprint and strong digital marketing strategy are expanding its presence across North America and European markets.

KOSÉ Corporation is a well-established Japanese cosmetics company with a diversified portfolio that includes advanced Vitamin C serum formulations. Known for its emphasis on skincare research and product quality, KOSÉ integrates Japanese beauty philosophy into its broader skincare range. Additionally, continued investment in product innovation and global distribution channels supports its strong competitive position in the Vitamin C serum market.

Key Players

- L’Oréal S.A.

- Galderma S.A.

- Amorepacific Group Inc.

- KOSÉ Corporation

- Clarins Inc.

- Unilever plc

- Shiseido Company Limited

- Beiersdorf AG

- Estée Lauder Companies Inc.

- Procter & Gamble Co.

Recent Developments

- March 2026 – Cymbiotika and Ulta Beauty announced a strategic retail partnership, bringing the “Beauty-From-Within” product range to over 1,000 Ulta Beauty stores nationwide. This collaboration represents a significant expansion of Cymbiotika’s physical retail presence across the United States skincare market.

- February 2026 – Rodan + Fields unveiled its Pure C Serum, a new breakthrough Vitamin C formulation specifically designed to support skin longevity and long-term brightness. The product targets consumers seeking clinically effective brightening and anti-aging performance in a single daily serum.

- September 2025 – Vivier affirmed its skincare legacy with the launch of Serum 30, a first-to-market high-concentration Vitamin C breakthrough. The advanced formula is designed to deliver measurable improvements in skin radiance, firmness, and overall luminosity for discerning skincare consumers.

- August 2025 – Neutrogena launched its new Collagen Bank Pure 15% Vitamin C Serum in collaboration with beauty influencer Serena Kerrigan. The product targets consumers seeking a science-backed, high-concentration Vitamin C solution positioned within an accessible and competitive price range.

- June 2025 – L’Oréal announced plans to acquire a majority stake in Medik8, a British skincare brand recognized for its advanced clinical formulations. This acquisition is expected to strengthen L’Oréal’s position in the science-backed and dermatologist-recommended skincare segment across global markets.

Report Scope

Report Features Description Market Value (2025) USD 1.5 Billion Forecast Revenue (2035) USD 3.0 Billion CAGR (2026-2035) 7.0% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Formulation Type (Stabilized Derivatives, Pure Ascorbic Acid, Blended Serums), By Concentration (10% to 20%, Below 10%, 20% and Above), By Distribution Channel (Online, Hypermarkets & Supermarkets, Specialty Stores, Pharmacies & Drugstores, Others) Regional Analysis North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) Competitive Landscape L’Oréal S.A., Galderma S.A., Amorepacific Group Inc., KOSÉ Corporation, Clarins Inc., Unilever plc, Shiseido Company Limited, Beiersdorf AG, Estée Lauder Companies Inc., Procter & Gamble Co. Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)

-

-

- L'Oréal S.A.

- Galderma S.A.

- Amorepacific Group Inc.

- KOSÉ Corporation

- Clarins Inc.

- Unilever plc

- Shiseido Company Limited

- Beiersdorf AG

- Estée Lauder Companies Inc.

- Procter & Gamble Co.

Our Clients

- 181668

- March 2026