Quick Navigation

Report Overview

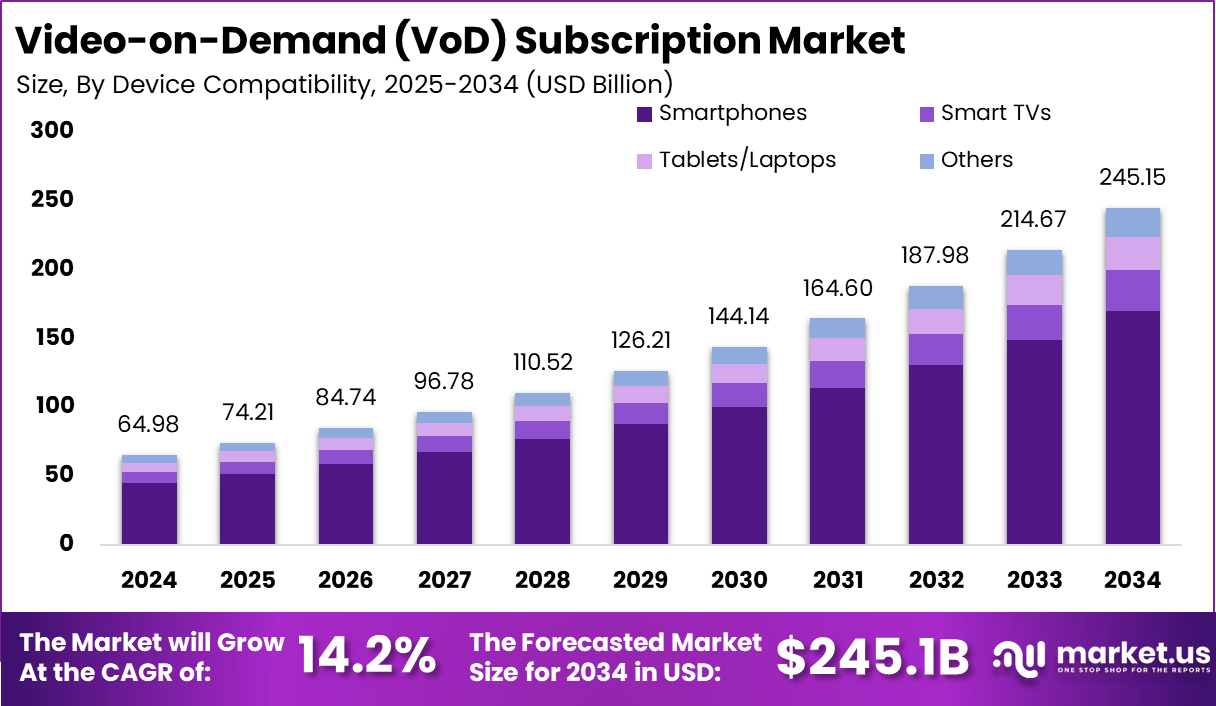

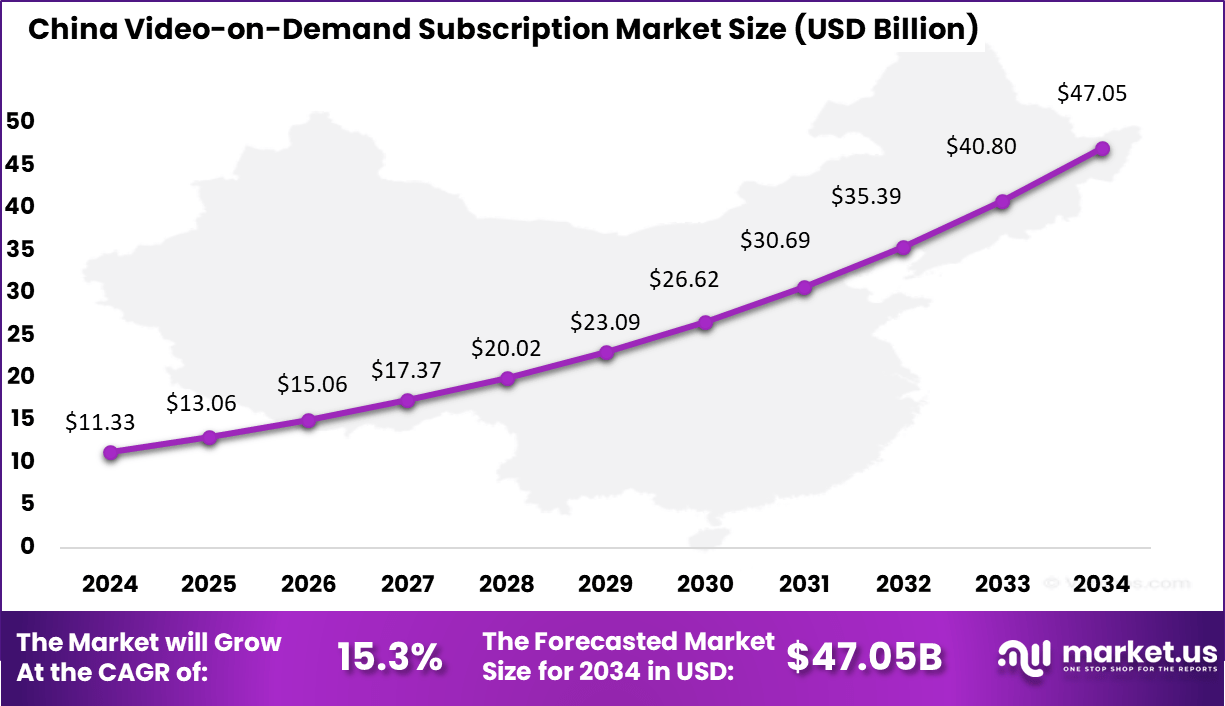

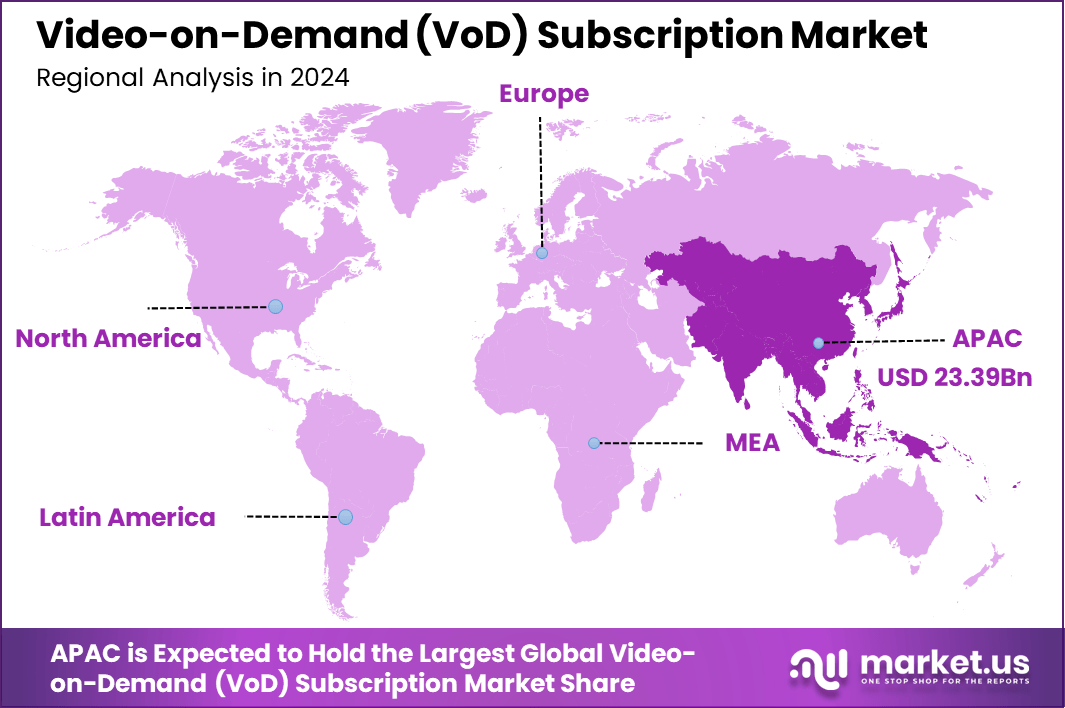

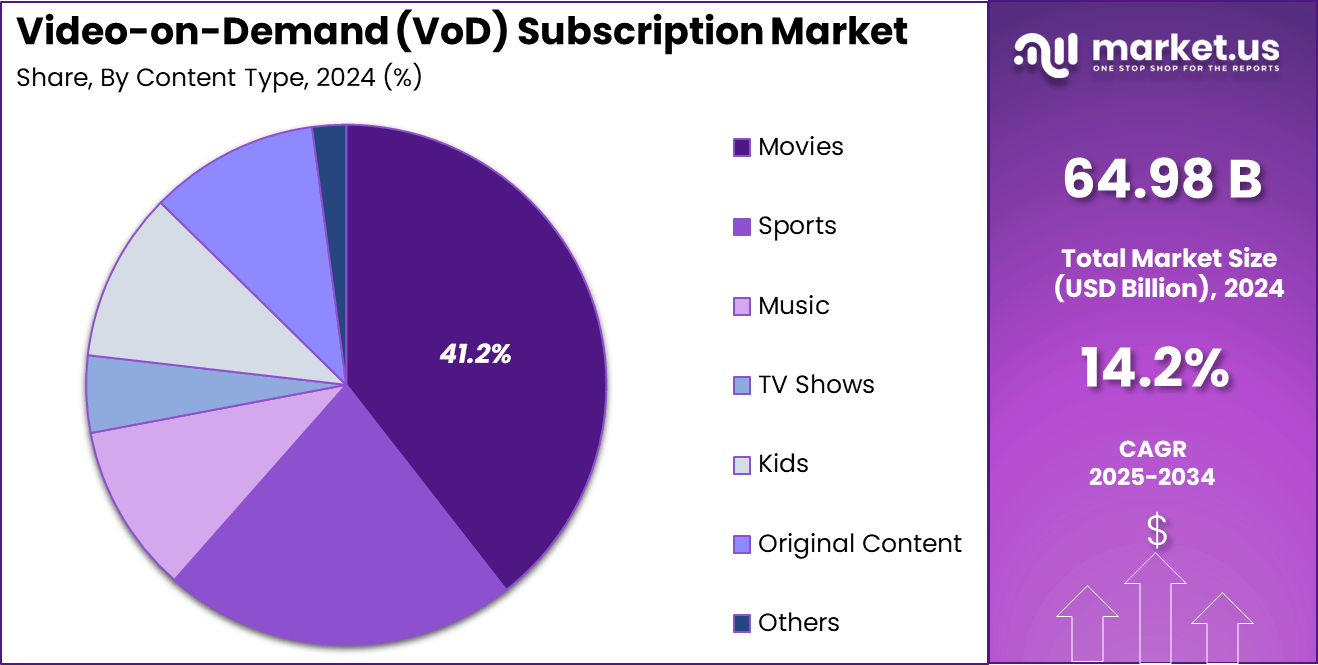

The Global Video-on-Demand (VoD) Subscription Market size is expected to be worth around USD 245.15 Billion By 2034, from USD 64.98 billion in 2024, growing at a CAGR of 14.2% during the forecast period from 2025 to 2034. In 2024, APAC held a dominant market position, capturing more than a 43.7% share, holding USD 28.39 Billion revenue. In China, the VoD subscription market reached USD 11.33 billion in 2024, growing at a CAGR of 15.3%.

The Video‑on‑Demand (VoD) Subscription Market is undergoing a significant transformation as streaming services mature into dominant modes of entertainment delivery. The shift away from traditional cable toward on‑demand accessibility is supported by abundant high‑speed internet, affordability of connected devices, and continuous investment in original content. Consumers now expect flexible multi‑device access and personalized content, driving VoD platforms to deepen their content catalogs and refine user experiences.

The Top Driving Factor accelerating market growth is the widespread adoption of broadband and mobile internet, especially 4G and 5G networks. As smartphones and smart TVs proliferate, viewing habits have changed fundamentally. Audiences now gravitate toward VoD services for convenience, comprehensive libraries, and on‑demand flexibility. This infrastructural improvement has reshaped entertainment consumption worldwide.

The Increasing Adoption of Technologies such as AI‑powered recommendation engines, cloud streaming, and adaptive bitrate delivery has enhanced user experience and scalability. These tools enable platforms to deliver content efficiently, with minimal buffering across varying network conditions. Experimental features like multi‑screen synchronization, interactive storytelling, and subscription bundling are gaining traction for customer retention.

According to industry report, around 1.4 billion people worldwide are expected to use video streaming services in 2025. Netflix projects its revenue to reach between USD 43.5 billion and USD 44.5 billion that year. The global average revenue per VOD user is estimated at USD 114.60 in 2025. Subscription-based VOD (SVOD) is forecast to account for nearly 70% of OTT revenues by 2030. In India, users reportedly spend an average of 180 minutes per day on streaming platforms.

Key Reasons for Adopting These Solutions include cost‑effectiveness, content diversity, and convenience. Consumers perceive stronger value in on‑demand models compared with traditional cable – especially as subscription and ad‑supported tiers remain competitive in price . These platforms also respond to anti‑piracy concerns by enhancing legal access and convenience, further boosting usage

Key Takeaways

- The Global VoD Subscription Market was valued at USD 64.98 Billion in 2024 and is projected to reach USD 245.15 Billion by 2034, expanding at a robust CAGR of 14.2% over the forecast period.

- The Asia-Pacific (APAC) region held the leading regional position, capturing over 43.7% of the global share and generating USD 28.39 Billion in 2024, supported by rapid digital adoption and mobile-first user behavior.

- China emerged as a key market within APAC, with its VoD subscription industry valued at USD 11.33 Billion in 2024 and forecasted to grow at a CAGR of 15.3%, driven by strong local content production and rising mobile video consumption.

- Movies dominated the content type segment, accounting for 41.2% of market share, as global consumers continue to prioritize film-based entertainment across subscription platforms.

- Smartphones led device compatibility with a commanding 69.4% share, reflecting the dominance of mobile viewing habits and the growing availability of affordable high-speed internet.

Impact of AI

The integration of AI into VoD platforms has significantly enhanced subscriber experiences and retention through sophisticated personalization and enhanced content delivery. AI-driven recommendation engines, leveraging machine learning and network-based clustering, have been shown to increase click-through rates by 63% and view completion rates by 24%, while achieving a 17% uplift in user satisfaction.

Additionally, around 58% of subscription services have introduced AI-generated personalized trailers, which have been observed to accelerate subscriber acquisition and deepen engagement. Such algorithms optimize content delivery, reduce choice overload, and tailor viewing suggestions to individual preferences, thereby reducing churn and fostering sustained loyalty.

Moreover, AI has facilitated operational efficiencies that support scalable service expansion. AI‑enhanced encoding algorithms improve compression efficiency and video quality, reducing buffering and infrastructure strain. Automated metadata tagging, captioning, and search optimization also streamline content discovery, yielding more seamless navigation experiences.

China Market Expansion

The China Video-on-Demand (VoD) Subscription Market is valued at approximately USD 11.33 Billion in 2024 and is predicted to increase from USD 23.09 Billion in 2029 to approximately USD 47.05 Billion by 2034, projected at a CAGR of 15.3% from 2025 to 2034.

In 2024, the Asia‑Pacific (APAC) region secured a dominant position in the global Video‑on‑Demand (VoD) subscription market, commanding over a 43.7 % market share with revenues reaching approximately USD 28.39 billion. This leading performance was driven by several interrelated factors.

First, the proliferation of affordable smartphones and mobile-first behavior across APAC have enabled rapid subscriber growth. With mobile broadband networks expanding and 5G rollout accelerating in countries such as India, China, South Korea, and Japan, consumers increasingly turned to on‑demand streaming services for entertainment on the go.

Second, regional platforms tailored to local preferences, including investments in domestic content like anime in Japan and Chinese‑language series in China, significantly improved subscriber acquisition and retention. Government policies in China favoring domestic VoD services and regional content quotas further fueled the emergence of local players.

Third, APAC’s pricing strategies – such as lower monthly subscription fees compared to Western markets – paired with the widespread adoption of ad-supported models and hybrid bundles, enhanced affordability and broadened market reach. Both global giants like Netflix and Disney+ and strong regional services such as India’s Hotstar, Japan’s U‑Next, and regional niche platforms intensified investment in Originals and genre‑specific content.

Content Type Analysis

In 2024, the Movies segment held a dominant market position in the global Video-on-Demand (VoD) subscription market, capturing more than 41.2% share. This leadership can be attributed to several key factors.

First, consumer preference for feature films remains strong due to their wide appeal across age groups, cultures, and genres – ranging from big-screen blockbusters to indie gems. Second, major streaming services have invested heavily in film libraries and theatrical releases, creating a differentiated offering that drives subscriber acquisition and retention.

For example, platforms like Netflix, Disney+, and Amazon Prime Video consistently premiere high-profile movies alongside licensed catalogs. Further supporting this dominance, a specific analysis of the Subscription VoD (SVOD) market estimated that the movie segment accounted for over 44% of global SVOD share in 2024, underscoring its relative scale compared to other categories such as TV shows or originals.

The Movies segment’s leading position is reinforced by consumer behavior: films are typically shorter commitments than bingeable series, enabling more flexible viewing and a perception of greater value. Additionally, the emotional impact and production quality of cinema-grade content foster higher viewer satisfaction and word-of-mouth promotion.

Summary of Leading Segment – Movies

| Key Drivers | Details |

|---|---|

| Broad Audience Appeal | Movies cater to diverse demographics and genres, ensuring mass engagement. |

| High Content Investment | Streaming platforms prioritize movies in content acquisition and production. |

| Shorter Viewing Commitment | Films require less time than series, supporting flexible and casual viewing. |

| Cinematic Experience | High production quality and emotional storytelling enhance viewer satisfaction. |

| Cross-Platform Popularity | Movies perform well across mobile, TV, and laptop screens, ensuring wide reach. |

Device Compatibility Analysis

In 2024, the Smartphones segment held a dominant market position in the global Video-on-Demand (VoD) subscription market, capturing more than a 69.4% share. This pre‑eminence is attributed to the ubiquity of mobile devices and the universality of high‑speed mobile internet.

Smartphones enable consumers to access content at their convenience – during commuting, breaks, or travel – thus aligning with modern lifestyle demands. The portability and personal nature of smartphones foster continuous engagement and frequent usage, which serve as crucial drivers for service providers aiming to maximize viewing hours and reduce churn .

Furthermore, Smartphone dominance is reinforced by the demographic trends in emerging markets where mobile-first consumption is prevalent. VoD platforms have optimized their user interfaces and data usage models for mobile networks, ensuring seamless streaming even under variable connectivity conditions.

Strategic partnerships between streaming services and telecom operators, such as bundled subscriptions and zero‑rating, further incentivize smartphone-based consumption. These tailored approaches have solidified the segment’s leadership and driven its substantial market share in 2024.

Summary of Leading Segment – Smartphones

| Key Drivers | Details |

|---|---|

| Accessibility & Convenience | Portable viewing enables anytime/anywhere consumption |

| Tailored Experiences | Optimized UIs, data plans, telecom bundles enhance mobile usage |

| Emerging Markets | Mobile-first behavior prevalent in high-growth regions |

Key Market Segments

By Content Type

- Sports

- Music

- TV Shows

- Kids

- Movies

- Original Content

- Others

By Device Compatibility

- Smartphones

- Smart TVs

- Tablets/Laptops

- Others

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherlands

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Thailand

- Vietnam

- Rest of Latin America

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Emerging Trends

Rise of Ad-Supported VoD Models

A prominent trend reshaping the Video-on-Demand (VoD) Subscription Market is the increasing shift toward hybrid monetization, particularly ad-supported video-on-demand (AVoD) tiers. Many consumers, especially younger demographics such as Gen Z, are now showing a preference for free or lower-cost content access in exchange for viewing ads.

This model has proven attractive in price-sensitive markets and regions with slower SVOD saturation. Platforms are responding by launching or expanding ad-backed tiers to widen their user base while preserving revenue flow. The trend is further reinforced by declining subscription growth rates in some mature markets.

As users experience subscription fatigue from maintaining multiple paid services, ad-supported models offer a compelling alternative. This shift is not only revitalizing growth in saturated regions but also allowing VoD players to gather deeper user behavior insights through ad-targeting technologies.

Driver

Increasing Internet and Smart Device Penetration

The global expansion of high-speed internet and mobile networks, particularly 4G and 5G, has been a powerful driver for VoD subscription growth. As broadband infrastructure improves, even in emerging markets, access to high-quality, buffer-free video streaming becomes widely available. This access has enabled a large population to shift from traditional TV viewing to more flexible and personalized VoD services.

Moreover, the affordability of smart TVs, tablets, and mobile devices has fueled multi-screen consumption behavior. Users now expect content to be available anywhere, on any device, and at any time. The fusion of mobile-first habits and connected home environments has made VoD services a staple of daily media consumption. These advancements in infrastructure and device accessibility are laying a strong foundation for sustained market growth.

Restraint

Content Saturation and Subscription Fatigue

As VoD platforms compete to acquire and retain users, an overwhelming volume of content has flooded the market. While variety is generally considered beneficial, excessive options can lead to choice fatigue among users. The duplication of content across services, and the fragmentation of premium content into exclusive ecosystems, has begun to frustrate subscribers who feel compelled to maintain multiple accounts to access desired shows or movies.

Simultaneously, rising monthly fees and the proliferation of paywalled content have triggered a phenomenon known as subscription fatigue. Consumers are becoming more selective about which platforms they subscribe to, especially during economic downturns. This shift is prompting VoD providers to reconsider pricing strategies, reduce churn through bundling, and explore flexible access models such as pay-per-view or limited-access subscriptions.

Opportunity

Local Language and Regional Content Expansion

An attractive opportunity lies in the creation and distribution of localized and regional content tailored to specific audiences. With global markets diversifying, VoD platforms that invest in region-specific genres, dialects, and cultural narratives are seeing significant user growth. Consumers increasingly favor relatable, community-rooted stories over global blockbusters, especially in Asia, Latin America, and the Middle East.

By tapping into underserved linguistic markets and highlighting local creators, streaming companies can cultivate loyalty while gaining competitive edge. Government support for digital content creation and growing mobile consumption in Tier 2 and Tier 3 cities further magnify this opportunity. Regional content also performs strongly on both SVOD and AVoD models, creating a versatile asset for monetization.

Challenge

Increasing Piracy and Platform Fragmentation

A major challenge for the VoD subscription market remains content piracy, which erodes both revenue and consumer trust. As premium content becomes more exclusive and costly, unauthorized sharing through torrent sites and illicit streaming apps continues to attract a portion of the market, especially in regions lacking strict copyright enforcement.

This undermines revenue streams and affects the willingness of investors to fund high-budget productions. Platform fragmentation is another persistent obstacle. With exclusive content spread across dozens of apps, consumers often find the experience inconvenient and unaffordable.

Switching between interfaces, managing payments, and searching across ecosystems create friction in the user journey. The absence of an industry-wide content aggregation or subscription consolidation system keeps this issue unresolved, despite growing user dissatisfaction.

Key Player Analysis

Amazon strengthened its content offering following the successful integration of MGM into its Amazon Prime Video ecosystem. In early 2025, the company expanded its original content pipeline through an expanded deal with Paramount+, ensuring exclusive streaming rights for select blockbuster titles.

After the WarnerMedia–Discovery merger, AT&T oversaw a strategic reorganization of Warner Bros. Discovery. In June 2025, the decision was made to split the streaming and traditional networks into two independent entities. This move enumerates a sharper strategic focus on VoD and studio content under one business unit, expected by mid‑2026, and separates legacy linear assets.

Comcast accelerated its VoD strategy via Peacock, bundling new premium-tier content such as exclusive series and live events. In May 2024, the company launched its “Xfinity StreamSaver™” bundle that paired Peacock Premium with Netflix and Apple TV+, offering significant annual savings for Xfinity customers

Top Key Players Covered

- Amazon.com, Inc.

- Hulu LLC (The Walt Disney Company)

- AT&T, Inc. (Warner Media, LLC and Discovery, Inc.)

- Netflix, Inc.

- Apple, Inc.

- Comcast Corporation

- Facebook, Inc.

- Telefonaktiebolaget LM

- Ericsson

- Verizon Communications Inc.

- Others

Recent Developments

- In June 2025, Disney finalized its acquisition of Hulu by paying Comcast an additional $438.7 million, bringing the total to $9.2 billion. This ends years of joint ownership and allows Disney to fully integrate Hulu with Disney+ and ESPN’s streaming services, promising a more seamless experience for subscribers.

- In January 2024, Amazon introduced ads on Prime Video in the US, starting with 2-3.5 minutes per hour. By June 2025, ad loads had doubled to 4-6 minutes per hour. This move aligns Prime Video with other ad-supported streamers and aims to boost ad revenue.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 64.98 Bn |

| Forecast Revenue (2034) | USD 245.15 Bn |

| CAGR (2025-2034) | 14.2% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue forecast, AI impact on market trends, Share Insights, Company ranking, competitive landscape, Recent Developments, Market Dynamics and Emerging Trends |

| Segments Covered | By Content Type (Sports, Music, TV Shows, Kids, Movies, Original Content, Others), By Device Compatibility (Smartphones, Smart TVs, Tablets/Laptops, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Latin America; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Amazon.com, Inc., Hulu LLC (The Walt Disney Company), AT&T, Inc. (Warner Media, LLC and Discovery, Inc.), Netflix, Inc., Apple, Inc., Comcast Corporation, Facebook, Inc., Telefonaktiebolaget LM, Ericsson, Verizon Communications Inc., Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three license to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |

Subscription Market")