Global Video Game Developer Market Size, Share and Analysis By Developer Type (AAA Game Studios, Independent Game Studios, Mobile Game Developers, Others), By Platform (PC, Console, Mobile, Others), By Genre (Action & Adventure, Role-Playing Games, Strategy & Simulation, Casual & Social, Others), By Regional Analysis, Global Trends and Opportunity, Future Outlook By 2025-2035

- Published date: March 2026

- Report ID: 180363

- Number of Pages: 350

- Format:

-

keyboard_arrow_up

Quick Navigation

- Report Overview

- Key Takeaway

- Key Statistics

- Role of Generative AI

- Investment and Business Benefits

- China Market Size

- Developer Type Analysis

- Platform Analysis

- Genre Analysis

- Growth Factors

- Emerging Trends

- Key Market Segments

- Driver Analysis

- Restraint Analysis

- Opportunity Analysis

- Challenge Analysis

- Key Players Analysis

- Recent Developments

- Report Scope

Report Overview

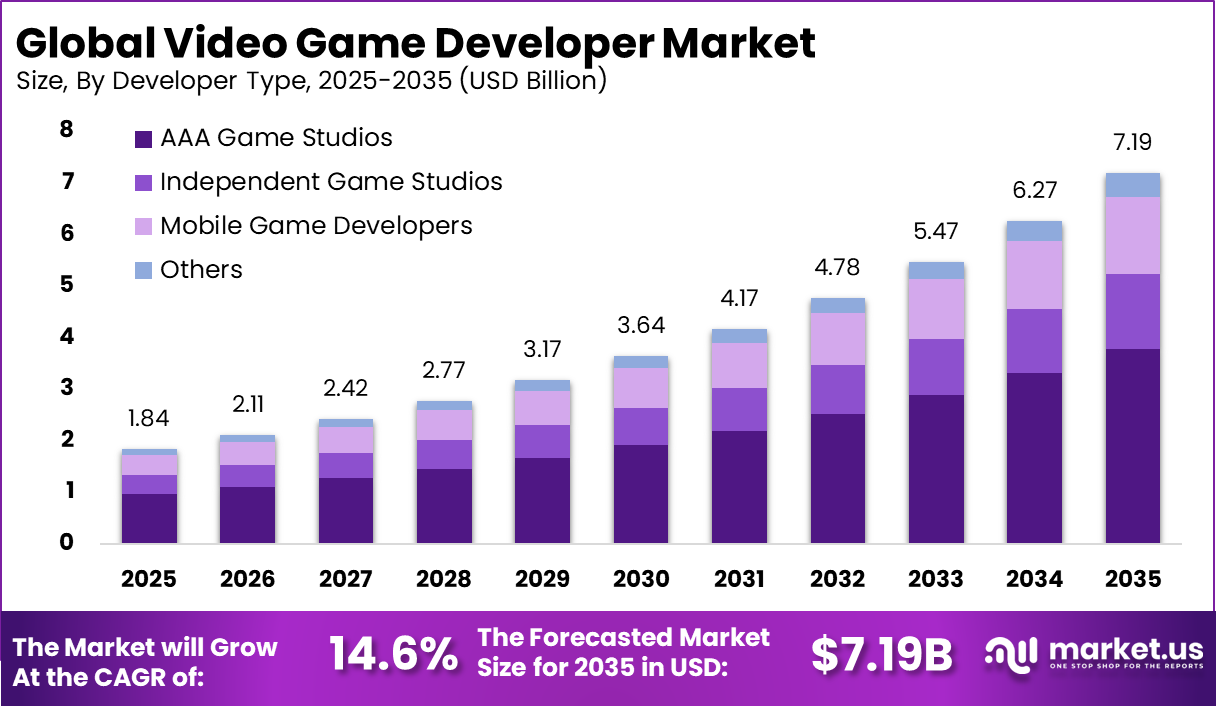

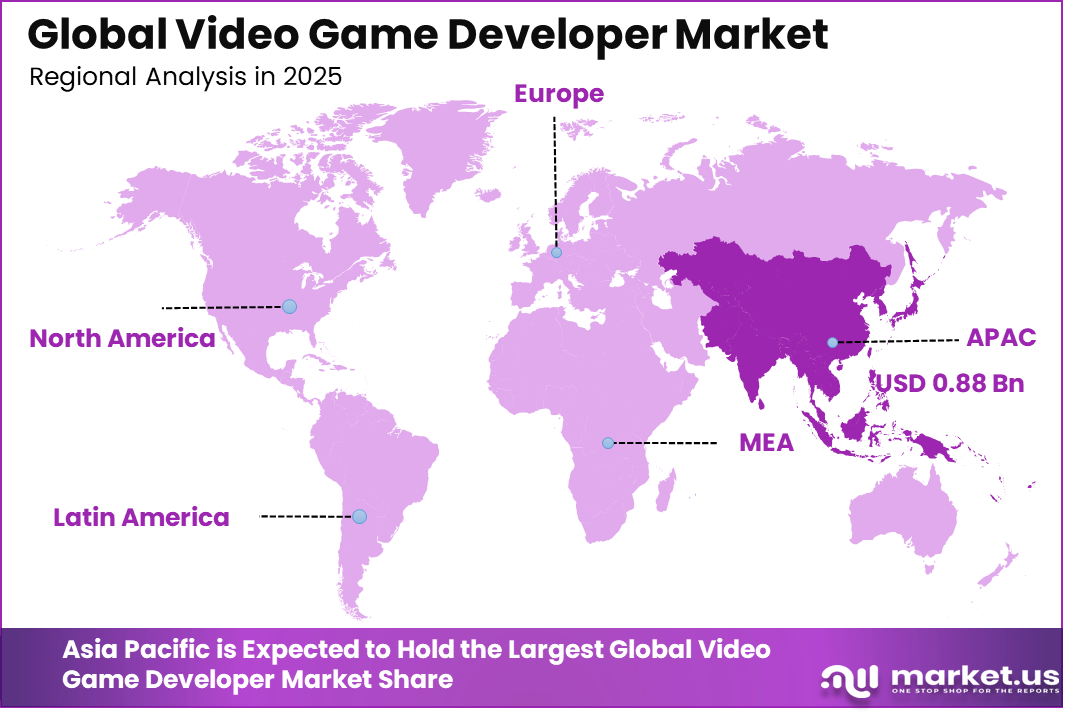

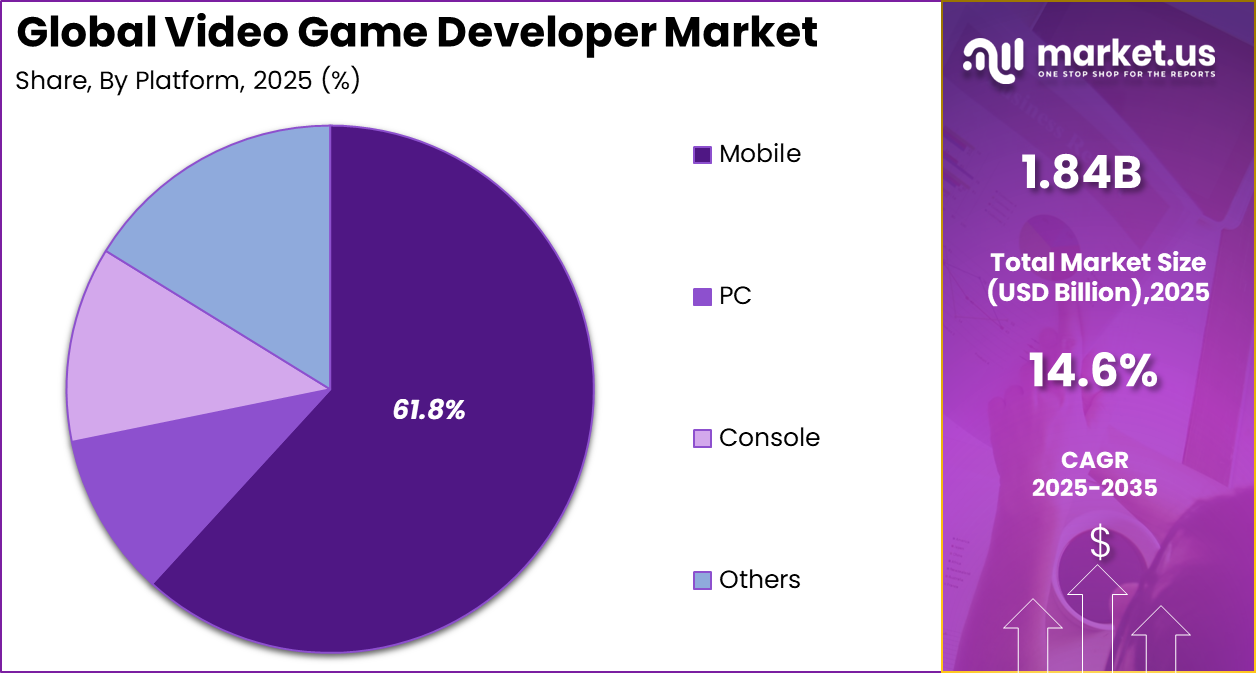

The Global Video Game Developer Market size is expected to be worth around USD 7.19 billion by 2035, from USD 1.84 billion in 2025, growing at a CAGR of 14.6% during the forecast period from 2025 to 2035. Asia Pacific held a dominant market position, capturing more than a 48.3% share, holding USD 0.88 billion in revenue.

A video game developer refers to a professional or a team responsible for designing, building, and maintaining video games across platforms such as consoles, computers, and mobile devices. They combine programming, storytelling, graphics, and sound to create engaging experiences. Developers also test, update, and improve games to ensure smooth gameplay and long term player engagement.

Rising player expectations for deeper storytelling and smoother gameplay are pushing game developers to innovate constantly. Around 65% of gamers now prefer immersive and interactive worlds rather than simple action formats. Improved graphics engines and smart development tools help teams create complex environments faster by simplifying testing, animation, and design tasks. Additionally, mobile gaming has surged, accounting for nearly 50% of daily game sessions worldwide.

The market for Video Game Developer is driven by the rising popularity of digital entertainment and the growing number of people who play games across mobile phones, computers, and consoles. Faster internet connectivity, powerful gaming engines, and online multiplayer features continue to attract new players. Strong interest in esports, interactive storytelling, and social gaming experiences also encourages developers to create more engaging and innovative titles.

Demand continues to grow as younger audiences spend significant time on games each day, especially in social and multiplayer environments. Nearly 70% of gamers prefer multiplayer modes that allow interaction and shared experiences with friends. Esports tournaments now attract viewership comparable to major sports events, increasing demand for competitive titles. In addition, about 40% of players switch between mobile phones and consoles, increasing the need for cross-platform game development.

For instance, in March 2026, Microsoft Gaming expanded Xbox Game Pass to 50 million subscribers after acquiring Bethesda’s remaining indie studios. Strategic cloud gaming investments reinforce U.S. subscription model supremacy, generating $3.2 billion quarterly revenue from multi-platform content delivery.

Key Takeaway

- In 2025, the Independent Game Studios category maintained a leading position in the Global Video Game Developer Market, accounting for 52.7% of the overall industry share.

- In 2025, the Mobile platform emerged as the primary development focus within the Global Video Game Developer Market, representing 61.8% of total activity.

- In 2025, the Action and Adventure genre remained the most widely developed category in the Global Video Game Developer Market, securing 38.5% of the total share.

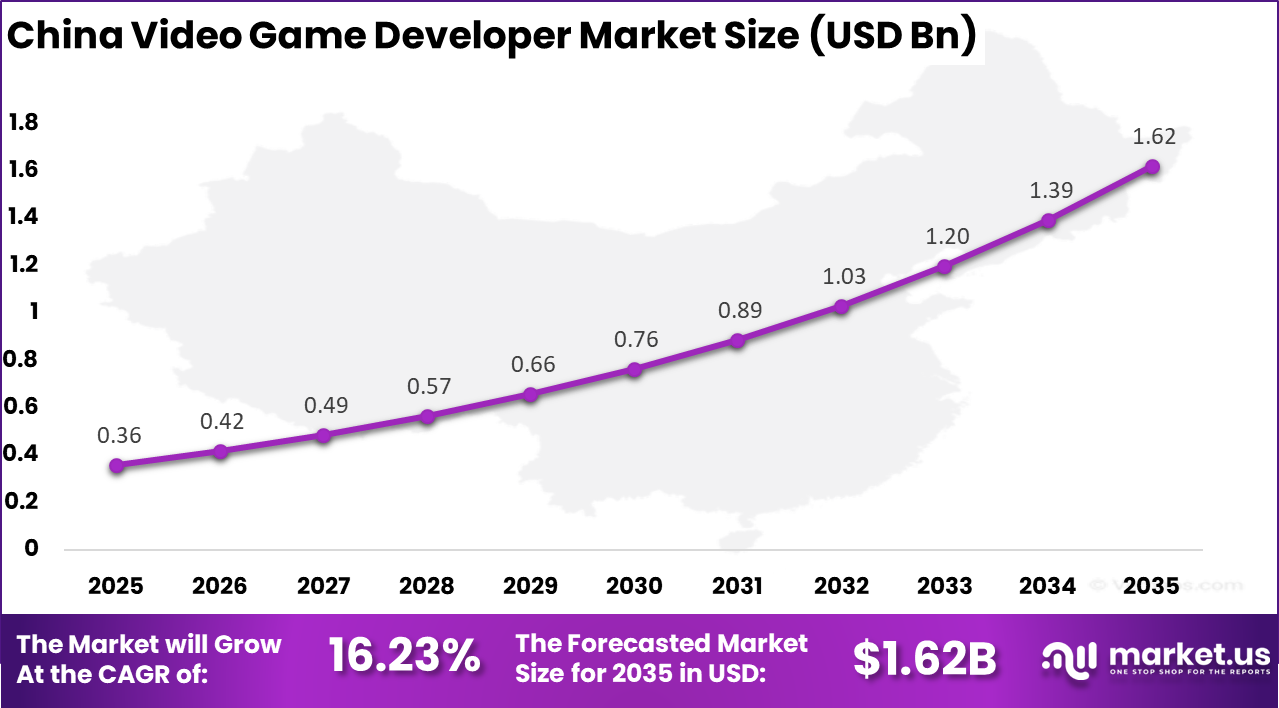

- The China Video Game Developer Market reached a valuation of USD 0.36 Billion in 2025 and is expected to expand at a strong 23% CAGR over the coming years.

- In 2025, Asia Pacific continued to lead the Global Video Game Developer Market, capturing more than 48.3% of the total market share.

Key Statistics

- About 65% of game studios are developing titles for PC, with mobile platforms following closely in development activity.

- Nearly 58% of developers are focusing on multiplayer games, reflecting rising demand for social and interactive gaming experiences.

- More than 85% of total gaming revenue is generated through free to play models supported by microtransactions and in game purchases.

- Around 30% of developers are currently using generative AI tools in game development despite ongoing ethical discussions.

- The online gaming industry is expected to grow by 26%, reaching approximately USD 37.2 billion by 2030.

- The gaming livestreaming market is projected to expand by about 23% as gaming continues to evolve into a social entertainment activity.

- Approximately 77% of game developers show no interest in blockchain technologies, including NFTs and Web3 systems.

- Only about 2% of studios currently use blockchain technology within their game development processes.

- The PC platform dominates upcoming releases, with 156 of the 200 most anticipated games scheduled for launch on PC.

- PlayStation 5 and Xbox Series X/S show similar game availability, with 115 and 113 major titles respectively.

Role of Generative AI

Generative AI is transforming how video game developers produce creative content. It helps teams quickly generate characters, environments, dialogue, and visual assets that previously required long manual work. Nearly 65% of developers now rely on AI tools during early prototyping stages, helping studios reduce development timelines and experiment with ideas faster.

The technology also enhances player interaction by supporting adaptive gameplay elements. AI powered non playable characters react more naturally to player actions, creating more immersive experiences. Game studios report stronger engagement when such systems are used, with around 42% of players spending longer periods in titles that include AI-driven characters and dynamic environments.

Investment and Business Benefits

Investment interest is rising in technologies that accelerate game development and connect creators with funding platforms. Mobile-first game designs and esports-oriented features are receiving strong financial backing as player bases expand globally. Live-service games that evolve with regular updates also attract investors because they provide long-term revenue streams. Around 55% of new capital is directed toward tools and systems that support continuous content updates.

Operating in the gaming industry allows companies to generate revenue from multiple sources, such as game sales, in-game purchases, advertising, and subscriptions. This diversified income model helps studios maintain steady earnings. Strong player communities also encourage repeat engagement and organic promotion. Industry surveys indicate that more than 75% of gaming companies view stronger relationships with players and loyal communities as a major advantage.

China Market Size

The market for Video Game Developers within China is growing tremendously and is currently valued at USD 0.36 billion, the market has a projected CAGR of 16.23%. This market is growing due to strong mobile gaming adoption, expanding digital entertainment demand, and continuous investments in game studios.

China has one of the largest gaming populations, supported by widespread smartphone access and fast internet infrastructure. Growing esports popularity and government support for digital creative industries also encourage local developers to produce innovative and globally competitive games.

For instance, in January 2026, NetEase captured significant China gaming market share with the Marvel Rivals mobile version optimized for Asian networks, generating $2.8 billion annually. Hangzhou’s cloud gaming tech led APAC latency reduction by 60%, establishing dominance in cross-platform multiplayer experiences.

In 2025, the Asia Pacific held a dominant market position in the Global Video Game Developer Market, capturing more than a 48.3% share, holding USD 0.88 billion in revenue. This dominance is due to the region’s large gaming population, strong mobile gaming culture, and expanding digital infrastructure.

Countries such as China, Japan, and South Korea host many active game studios and esports communities. Rising smartphone usage, supportive digital policies, and growing demand for online entertainment continue to strengthen game development activities across the region.

For instance, in January 2026, Sony Interactive Entertainment strengthened Asia Pacific leadership through PS6 pre-launch hype and exclusive God of War titles optimized for Japanese audiences. Their Tokyo studio partnerships drove 25% regional sales growth, with VR integration cementing Japan’s console dominance in the video game developer market.

Developer Type Analysis

In 2025, Independent game studios account for 52.7% of the market, reflecting the growing role of smaller development teams in the global gaming ecosystem. Advances in development engines, digital distribution channels, and crowdfunding platforms have reduced entry barriers for independent creators. These studios are able to produce innovative titles while maintaining lower operational costs compared with large publishers.

Independent developers often focus on unique gameplay mechanics, creative storytelling, and niche gaming communities. Digital storefronts allow these studios to reach global audiences without relying heavily on traditional publishing networks. As consumer demand for diverse gaming experiences increases, independent studios continue to play a significant role in shaping the market.

For Instance, in January 2026, Tencent ramped up support for indie creators through its Venture Lab program, offering hands-on guidance to early-stage teams. This move helps small studios polish their ideas into viable projects, fostering a wave of fresh talent that challenges traditional development paths. It’s all about giving independents the tools to compete on an equal footing.

Platform Analysis

In 2025, the Mobile segment held a dominant market position, capturing a 61.8% share of the Global Video Game Developer Market. Smartphones have become the most common device for gaming because they are widely available and easy to use. Players can access games instantly, making mobile gaming a popular option for short and frequent play sessions throughout the day.

Developers are increasingly focusing on mobile platforms due to their broad reach and active player base. Mobile games can be updated regularly with new content, events, and features that keep users engaged. The combination of app stores, improved mobile internet connectivity, and affordable smartphones continues to strengthen mobile gaming growth.

For instance, in March 2026, NetEase launched a slate of mobile-first titles with seamless cross-play features. Players jump between devices effortlessly, boosting daily logins and keeping casual audiences hooked. This keeps mobile at the forefront by blending accessibility with deeper engagement.

Genre Analysis

In 2025, Action and adventure games account for 38.5% of the market, reflecting their strong popularity among global gaming audiences. These games often combine fast paced gameplay with narrative driven exploration, which appeals to both casual and dedicated players. The genre supports immersive storytelling and complex game mechanics that maintain player engagement.

Developers frequently invest in high quality graphics, realistic environments, and interactive gameplay elements within action and adventure titles. The genre is widely distributed across mobile platforms, personal computers, and gaming consoles. As gaming audiences continue to expand, action and adventure games remain one of the most commercially successful segments in the market.

For Instance, in January 2026, Sony Interactive Entertainment revealed a new adventure with open-world exploration. Players dive into vast lands full of choices and combat twists. It builds on fan love for immersive stories, pulling crowds back for more.

Growth Factors

One of the major growth factors driving the video game developer market is the expanding global gaming audience. Improved internet connectivity and the widespread adoption of smartphones have significantly increased the number of players worldwide. As gaming becomes accessible to diverse age groups and demographics, developers are producing a larger variety of content to meet different player interests.

Another growth factor is the continuous improvement in game development technologies. Modern game engines provide advanced rendering capabilities, physics simulations, and development tools that simplify the creation of complex gaming environments. These technologies allow developers to produce high-quality games more efficiently and reduce the technical barriers associated with game production.

Emerging Trends

One emerging trend in the video game developer market is the integration of artificial intelligence into gameplay design. AI technologies are increasingly used to create intelligent non-player characters, adaptive game environments, and personalized gaming experiences. These capabilities enhance player engagement by making gameplay more dynamic and responsive to individual player behavior.

Another trend is the growth of cloud-based gaming infrastructure. Cloud platforms allow players to stream games directly without requiring high-performance hardware. This development expands access to high-quality gaming experiences and encourages developers to design games that can operate across multiple devices and platforms seamlessly.

Key Market Segments

By Developer Type

- AAA Game Studios

- Independent Game Studios

- Mobile Game Developers

- Others

By Platform

- Mobile

- PC

- Console

- Others

By Genre

- Action & Adventure

- Role-Playing Games

- Strategy & Simulation

- Casual & Social

- Others

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherlands

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Thailand

- Vietnam

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Driver Analysis

Expanding Digital Entertainment Ecosystem

A primary driver of the video game developer market is the rapid growth of digital entertainment platforms. Online distribution channels, streaming platforms, and gaming communities allow developers to interact directly with players and continuously update their games. This digital ecosystem increases visibility and helps developers maintain long-term player engagement.

Another driver is the popularity of multiplayer and online gaming experiences. Social interaction and competitive gameplay encourage players to spend more time in gaming environments. Developers respond by creating interactive features such as live events, cooperative missions, and global leaderboards that strengthen player communities.

For instance, in October 2025, Sony pushed its PlayStation Network with free-to-play weekends aimed at casual gamers in India and Africa. The event pulled in waves of first-time users who stuck around for multiplayer modes. It showed how a bigger global player base lets firms like Sony expand reach without heavy marketing spends.

Restraint Analysis

Rising Development Costs and Market Competition

One restraint affecting the video game developer market is the rising cost of game production. High-quality graphics, advanced gameplay mechanics, and large development teams require substantial investment. Smaller studios may struggle to secure the resources needed to compete with major development companies.

Another restraint is the high level of competition within the gaming industry. Thousands of new games are released annually across digital platforms, making it challenging for developers to capture player attention. Marketing efforts and strong community engagement strategies have become increasingly important for achieving commercial success.

For instance, in July 2025, EA paused development on an open-world sports title overwhelmed by procedural generation tools and real-time weather systems. The extra layers clashed with tight deadlines, forcing cuts to core mechanics. This restraint hits when innovation meets mounting technical hurdles.

Opportunity Analysis

Cross-Platform Gaming and Immersive Technologies

A significant opportunity lies in the development of cross-platform gaming environments. Players increasingly expect to access games across multiple devices including smartphones, consoles, and personal computers. Developers who design games with cross-platform compatibility can reach broader audiences and increase player engagement.

Another opportunity exists in immersive technologies such as virtual reality and augmented reality. These technologies enable developers to create highly interactive environments and new gameplay formats. As hardware and software capabilities continue to improve, immersive gaming experiences are expected to attract new player segments.

For instance, in February 2026, Roblox expanded its cloud-hosted worlds to support cross-device creation tools, where builders tweak experiences on laptops and then test on mobiles. User-generated content flourished with zero install barriers. Cloud growth here fuels endless community-driven expansion.

Challenge Analysis

Talent Shortages and Complex Development Cycles

A key challenge in the video game developer market is the demand for highly skilled development professionals. Game development requires expertise in programming, animation, visual effects, sound design, and storytelling. Recruiting and retaining professionals with these skills can be difficult, particularly for smaller studios.

Another challenge involves managing complex development timelines. Modern games often require years of development and extensive testing to ensure performance stability and gameplay balance. Coordinating multidisciplinary teams while maintaining creative vision and technical efficiency remains a major challenge for development studios.

Key Players Analysis

The Video Game Developer Market is dominated by large multinational publishers that control globally recognized gaming franchises and large development ecosystems. Tencent, Sony Interactive Entertainment, Microsoft Gaming, and Nintendo maintain strong positions through extensive game studios, digital distribution platforms, and console ecosystems.

Leading game publishers also play a central role in shaping competitive dynamics. Activision Blizzard, Electronic Arts, Epic Games, Ubisoft, and Take-Two Interactive develop large scale franchises that generate strong engagement across console, PC, and mobile platforms. Their strategies focus on live service games, in game monetization models, and global esports ecosystems.

Asian developers and emerging digital gaming platforms further increase market diversity. Bandai Namco, NetEase, Square Enix, Sega, Roblox Corporation, and Niantic contribute innovative gameplay models and mobile first strategies. These companies emphasize user generated content platforms, augmented reality gaming, and social gaming experiences.

Top Key Players in the Market

- Tencent

- Sony Interactive Entertainment

- Microsoft Gaming

- Nintendo

- Activision Blizzard

- Electronic Arts

- Epic Games

- Ubisoft

- Take-Two Interactive

- Bandai Namco

- NetEase

- Square Enix

- Sega

- Roblox Corporation

- Niantic

- Others

Recent Developments

- In February 2026, Sony Interactive Entertainment launched PlayStation 6 with the exclusive God of War Ragnarök sequel, selling 12 million units in the first month. Their VR integration and cloud streaming advancements solidify North American hardware leadership, outpacing competitors in immersive gaming experiences.

- In February 2026, Epic Games rolled out Fortnite’s metaverse hub with 900 million registered users, partnering with Disney for branded worlds. Unreal Engine licensing to 80% of AAA studios underscores North Carolina’s tech infrastructure leadership.

Report Scope

Report Features Description Market Value (2025) USD 1.8 Bn Forecast Revenue (2035) USD 7.1 Bn CAGR (2026-2035) 14.6% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue forecast, AI impact on Market trends, Share Insights, Company ranking, competitive landscape, Recent Developments, Market Dynamics and Emerging Trends Segments Covered By Developer Type (AAA Game Studios, Independent Game Studios, Mobile Game Developers, Others), By Platform (PC, Console, Mobile, Others), By Genre (Action & Adventure, Role-Playing Games, Strategy & Simulation, Casual & Social, Others) Regional Analysis North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Latin America; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA Competitive Landscape Tencent, Sony Interactive Entertainment, Microsoft Gaming, Nintendo, Activision Blizzard, Electronic Arts, Epic Games, Ubisoft, Take-Two Interactive, Bandai Namco, NetEase, Square Enix, Sega, Roblox Corporation, Niantic, Others Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three license to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)  Video Game Developer MarketPublished date: March 2026add_shopping_cartBuy Now get_appDownload Sample

Video Game Developer MarketPublished date: March 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- Tencent

- Sony Interactive Entertainment

- Microsoft Gaming

- Nintendo

- Activision Blizzard

- Electronic Arts

- Epic Games

- Ubisoft

- Take-Two Interactive

- Bandai Namco

- NetEase

- Square Enix

- Sega

- Roblox Corporation

- Niantic

- Others

Our Clients

- 180363

- March 2026