Global Veterinary Wound Cleansers Market By Product Type (Antiseptic Solutions, Enzymatic Cleansers, Hydrogel Cleansers, Foam Cleansers, Spray Cleansers, Wipes and Pads and Others), By Animal Type (Companion Animals, Livestock Animals and Equine), By Application (Surgical Wounds, Traumatic Wounds, Chronic Wounds, Burns, Post-Operative Care, Dermatological Conditions and Others), By End User (Veterinary Hospitals, Veterinary Clinics, Animal Shelters and Others), Region and Companies – Industry Segment Outlook, Market Assessment, Competition Scenario, Trends and Forecast 2026-2035

- Published date: April 2026

- Report ID: 183802

- Number of Pages: 215

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

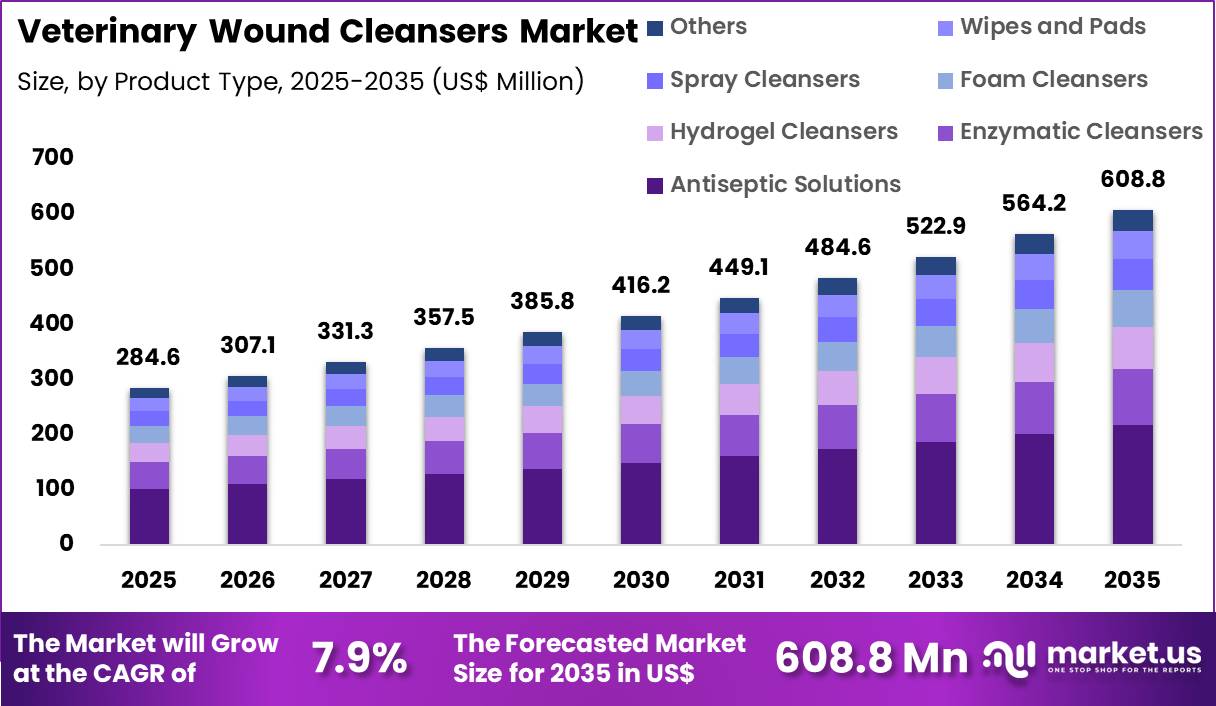

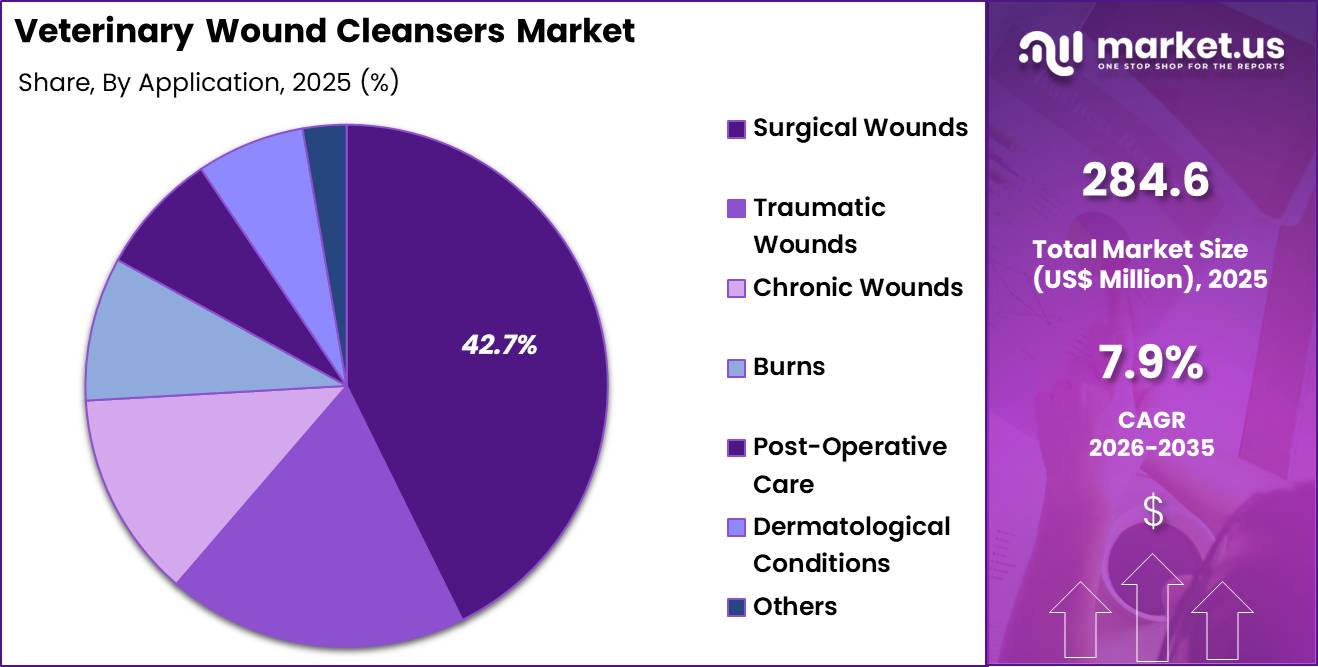

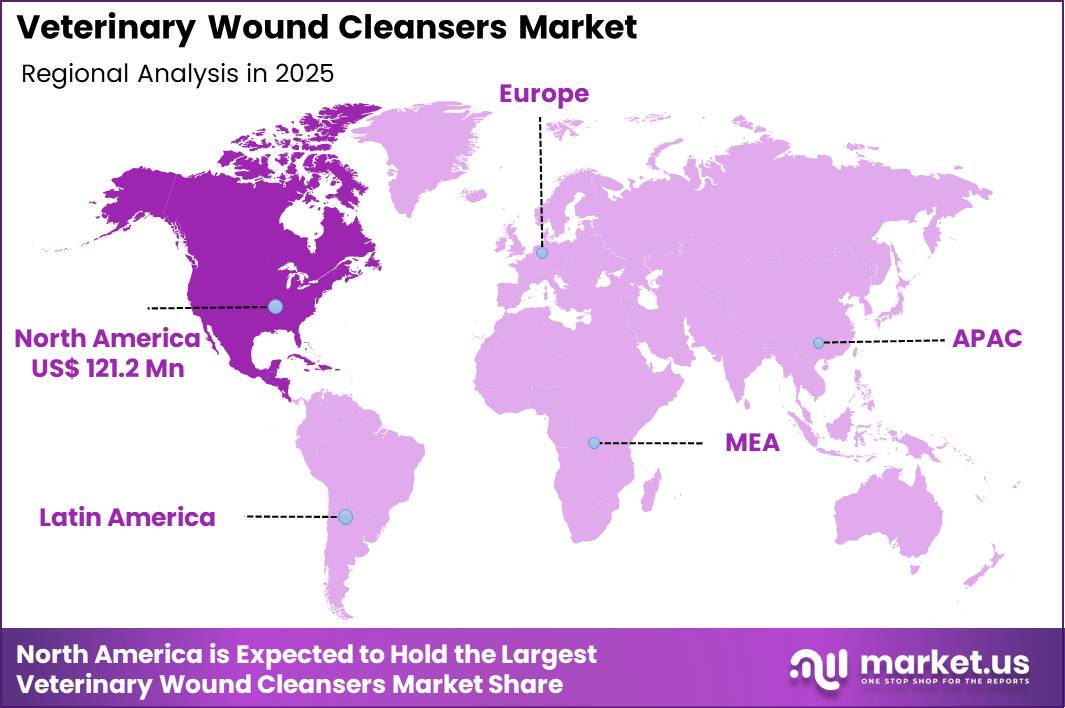

The Global Veterinary Wound Cleansers Market size is expected to be worth around US$ 608.8 Million by 2035 from US$ 284.6 Million in 2025, growing at a CAGR of 7.9% during the forecast period 2026-2035. In 2025, North America led the market, achieving over 42.6% share with a revenue of US$ 121.2 Million.

Rising incidence of traumatic injuries, surgical wounds, and chronic dermatological conditions in companion and production animals propels the Veterinary Wound Cleansers market as veterinarians require effective, gentle solutions that remove debris, reduce bacterial load, and prepare the wound bed for optimal healing.

Small animal practitioners increasingly apply antimicrobial wound cleansers containing chlorhexidine or hypochlorous acid to manage bite wounds, abscesses, and post-surgical incisions in dogs and cats, minimizing infection risk while preserving viable tissue.

These products support equine wound care by cleansing contaminated lacerations and abrasions on limbs or the body, creating a clean environment that promotes granulation and reduces the likelihood of proud flesh formation.

In livestock medicine, wound cleansers are used for foot rot and digital dermatitis in cattle and sheep, controlling bacterial proliferation and supporting recovery in herd health programs.

Exotic animal veterinarians utilize pH-balanced, non-irritating cleansers for reptiles and birds, where delicate skin and mucous membranes require careful management to avoid further tissue damage during wound care.

Manufacturers pursue opportunities to formulate advanced cleansers with biofilm-disrupting agents and natural antimicrobials, expanding applications in chronic or infected wounds where traditional solutions show limited efficacy. These developments support integration with regenerative therapies, ensuring a sterile yet biocompatible wound bed for stem cell or growth factor applications.

In early 2026, Zoetis also partnered with a Japanese biotechnology firm to co-develop allogeneic stem-cell sheet therapies for equine injuries. This collaboration is expected to accelerate demand for specialized wound preparation products that maintain sterile conditions without causing tissue irritation, supporting the effectiveness of advanced regenerative treatments.

Recent trends emphasize pH-balanced, non-cytotoxic formulations and ready-to-use delivery systems that improve compliance in both clinical and field settings, positioning veterinary wound cleansers as essential components of modern wound management protocols focused on rapid healing, infection control, and compatibility with emerging biologic therapies.

Key Takeaways

- In 2025, the market generated a revenue of US$ 284.6 Million, with a CAGR of 7.9%, and is expected to reach US$ 608.8 Million by the year 2035.

- The product type segment is divided into antiseptic solutions, enzymatic cleansers, hydrogel cleansers, foam cleansers, spray cleansers, wipes and pads and others, with antiseptic solutions taking the lead with a market share of 35.8%.

- Considering animal type, the market is divided into companion animals, livestock animals and equine. Among these, companion animals held a significant share of 58. 4%.

- Furthermore, concerning the application segment, the market is segregated into surgical wounds, traumatic wounds, chronic wounds, burns, post-operative care, dermatological conditions and others. The surgical wounds sector stands out as the dominant player, holding the largest revenue share of 42.7% in the market.

- The end user segment is segregated into veterinary hospitals, veterinary clinics, animal shelters and others, with the veterinary hospitals segment leading the market, holding a revenue share of 48.3%.

- North America led the market by securing a market share of 42.6%.

Product Type Analysis

Antiseptic solutions accounted for 35.8% of growth within product type and dominate the veterinary wound cleansers market due to their strong antimicrobial properties and widespread clinical use in preventing infection. Veterinarians rely on antiseptic formulations to clean wounds, reduce microbial load, and promote safe healing across a variety of animal species.

These solutions are expected to expand further as surgical procedures and injury cases increase in veterinary practice. Companion animal care continues to grow globally, which raises the need for effective wound management products.

Antiseptic solutions are likely to remain preferred because they act quickly and are easy to apply in both clinical and field settings.The segment benefits from broad-spectrum activity against bacteria and fungi, which supports use in diverse wound types.

Increasing awareness of infection control in veterinary care is projected to strengthen adoption. As veterinary practices prioritize safe and efficient wound treatment, antiseptic solutions are estimated to retain their leading position in this market.

Animal Type Analysis

Companion animals accounted for 58.4% of growth within animal type and dominate the veterinary wound cleansers market due to rising pet ownership and increased spending on animal healthcare. Dogs and cats frequently experience injuries, surgical procedures, and dermatological conditions that require consistent wound care management.

Veterinary studies indicate that companion animals represent a significant share of clinical visits, which drives demand for wound care products. This segment is expected to grow as pet humanization trends continue to strengthen globally.

Pet owners are likely to invest more in advanced treatment options to ensure faster recovery and comfort for their animals. The segment benefits from regular veterinary checkups and preventive care practices.

Increasing awareness of pet health and hygiene is projected to support consistent product usage. As the global pet population expands, companion animals are anticipated to remain the dominant segment in this market.

Application Analysis

Surgical wounds accounted for 42.7% of growth within application and dominate the veterinary wound cleansers market due to the increasing number of surgical interventions performed in animals. Veterinary procedures such as sterilization, orthopedic surgeries, and soft tissue operations require effective wound cleansing to prevent infection and support healing.

Surgical site management remains a critical component of post-operative care, which drives consistent demand for cleansers. This segment is expected to expand as access to veterinary surgical services improves globally.

Veterinarians are likely to prioritize antiseptic wound care to reduce complications and improve recovery outcomes. The segment benefits from standardized surgical protocols that include routine wound cleaning.

Increasing adoption of advanced veterinary procedures is projected to support further growth. As surgical care continues to expand in veterinary medicine, this application segment is estimated to maintain its leading position.

End-User Analysis

Veterinary hospitals accounted for 48.3% of growth within end user and dominate the veterinary wound cleansers market due to their ability to manage complex cases and perform surgical procedures requiring advanced wound care.

These facilities handle a high volume of patients, including emergency cases and post-operative care, which increases product usage. Veterinary hospitals are expected to remain dominant as they provide specialized care and access to trained professionals. The segment benefits from increasing investment in veterinary healthcare infrastructure and services.

Hospitals are likely to adopt standardized treatment protocols that include regular wound cleansing practices. Rising demand for high-quality animal care is projected to support growth in this segment. As veterinary services continue to advance, veterinary hospitals are anticipated to retain their leading position in the veterinary wound cleansers market.

Key Market Segments

By Product Type

- Antiseptic Solutions

- Enzymatic Cleansers

- Hydrogel Cleansers

- Foam Cleansers

- Spray Cleansers

- Wipes and Pads

- Others

By Animal Type

- Companion Animals

- Livestock Animals

- Equine

By Application

- Surgical Wounds

- Traumatic Wounds

- Chronic Wounds

- Burns

- Post-Operative Care

- Dermatological Conditions

- Others

By End User

- Veterinary Hospitals

- Veterinary Clinics

- Animal Shelters

- Others

Drivers

Increasing prevalence of wounds in companion animals is driving the Veterinary Wound Cleansers market.

The expanding companion animal population has elevated the incidence of traumatic injuries, surgical wounds, and chronic conditions requiring effective cleansing solutions. According to the American Veterinary Medical Association 2025 Pet Ownership and Demographics Sourcebook, the U.S. dog population reached 87.3 million in 2025, up from previous years, while the cat population stood at 76.3 million.

These figures reflect sustained growth in pet ownership, with approximately 66 percent of U.S. households owning at least one pet as reported in related 2024–2025 surveys. Wounds from accidents, bites, or underlying diseases such as diabetes necessitate prompt irrigation to remove debris and reduce infection risk.

Heightened owner awareness of animal well-being drives demand for specialized, non-irritating cleansers suitable for routine and emergency care. Veterinary practices increasingly incorporate advanced cleansing protocols to support faster healing and minimize complications in outpatient and hospital settings.

Public health emphasis on responsible pet care further encourages proactive wound management. The chronic nature of certain conditions in aging pets sustains recurring demand for cleansing products.

These demographic and clinical patterns directly correlate with higher utilization of veterinary wound cleansers. Consequently, this factor serves as a primary driver sustaining market expansion during the 2022–2025 period.

Restraints

High costs of advanced formulations and limited reimbursement are restraining the Veterinary Wound Cleansers market.

Premium antiseptic and bioactive cleansers command elevated pricing due to specialized ingredients and regulatory compliance requirements for veterinary use. Many pet owners and smaller clinics face budgetary constraints when selecting higher-cost options over basic saline solutions.

Reimbursement for veterinary wound care remains inconsistent or absent in most insurance plans, shifting the full expense to owners or practices. This dynamic discourages frequent adoption of advanced products despite demonstrated clinical benefits.

Training and inventory management for diverse formulations add operational overhead for veterinary facilities. Resource-limited settings in rural or developing regions particularly defer upgrades to cost-effective traditional alternatives. These economic pressures slow the replacement cycle and limit penetration of innovative cleansing technologies.

Persistent gaps in coverage frameworks hinder equitable access across patient segments. Such financial barriers moderate overall utilization rates even amid rising wound incidence. As a result, cost-related factors impose measurable restraint on accelerated market growth throughout the 2022–2025 timeframe.

Opportunities

Development of advanced and antimicrobial wound cleansers is creating growth opportunities in the Veterinary Wound Cleansers market.

Incorporation of antimicrobial agents and bioactive compounds enables sustained infection control while maintaining a moist healing environment suitable for diverse animal species. Opportunities emerge for spray and solution formats that facilitate easy application in both clinical and home-care settings.

These formulations support integration with broader wound management protocols, including dressings and debridement tools. Partnerships between manufacturers and veterinary researchers accelerate validation and customization for companion and livestock applications.

Potential exists for products tailored to specific wound types, such as diabetic ulcers or surgical sites, broadening therapeutic versatility. Alignment with preventive care trends in high-value companion animals enhances adoption among premium practices.

Expansion into emerging markets benefits from scalable, user-friendly designs that address varying infrastructure levels. These innovations generate recurring revenue through consumable usage and support differentiation in competitive segments. Overall, advancements in formulation technology unlock substantial prospects for market diversification and improved clinical outcomes.

Impact of Macroeconomic / Geopolitical Factors

Economic conditions and geopolitical shifts are redefining the operating environment for the veterinary wound cleansers market through their influence on cost inputs, distribution stability, and purchasing behavior. I

ncreased expenditure on companion animal care and stricter hygiene practices in livestock management are sustaining demand, yet persistent inflation is elevating the cost of active ingredients, packaging materials, and logistics, thereby affecting pricing decisions at the clinic and distributor level.

In parallel, fluctuations in currency and trade uncertainties are complicating sourcing strategies for manufacturers that depend on globally supplied chemical compounds. Geopolitical frictions are also introducing delays in cross-border shipments, which can disrupt inventory planning and availability in key markets.

US tariff measures on selected chemical inputs and veterinary-related supplies are adding cost pressure across the value chain, prompting firms to reassess procurement models and margin structures. Such pressures may restrict uptake in highly price-sensitive segments, particularly in large-scale animal husbandry operations.

However, these same trade dynamics are encouraging investment in localized production and diversified supplier networks, which enhances long-term supply assurance.

Taken together, while short-term cost escalation and supply variability remain concerns, the underlying demand for effective wound care and infection control is expected to support a stable and gradually strengthening market trajectory.

Latest Trends

Shift toward advanced cleansers and spray formats represents a recent trend in the Veterinary Wound Cleansers market.

In 2025, market analyses indicate that advanced cleansers gained momentum alongside traditional options, with projections highlighting faster growth trajectories for innovative formulations. Spray formats accounted for accelerated adoption due to their convenience in precise application and reduced contamination risk during wound irrigation.

Companion animals commanded a significant share of revenue in 2025, driven by heightened focus on pet health and specialized care. This development prioritizes non-cytotoxic, broad-spectrum solutions that minimize tissue damage while effectively removing pathogens.

Industry observations during 2024–2025 underscore integration of these products into routine veterinary protocols for trauma and chronic wound management. The trend aligns with overall advancements in animal healthcare emphasizing efficiency and patient comfort.

Continued emphasis on user-friendly delivery systems supports at-home use by pet owners under veterinary guidance. Prominent in the recent period, this evolution redefines standards for effective and practical wound cleansing in veterinary practice.

Regional Analysis

North America is leading the Veterinary Wound Cleansers Market

North America held 42.6% of the veterinary wound cleansers market in 2025, reflecting the region’s advanced veterinary care ecosystem and rising clinical focus on post-procedural hygiene and infection control.

Animal hospitals and specialty clinics across the United States have increasingly incorporated evidence-based wound management protocols, particularly for surgical recovery and trauma care in companion animals.

Data from the American Pet Products Association indicates that U.S. pet care expenditure exceeded USD 136 billion in 2022, signaling strong consumer willingness to invest in high-quality veterinary treatments, including wound care solutions.

Clinicians are prioritizing non-irritating and broad-spectrum cleansing formulations that support tissue healing while minimizing microbial load. The growing frequency of orthopedic and soft tissue surgeries has further elevated demand for reliable cleansing agents used in pre- and post-operative care.

In addition, increased attention to antimicrobial stewardship has encouraged the use of targeted cleansing products as an alternative to excessive antibiotic reliance. Veterinary professionals are also emphasizing early wound intervention to reduce complications and improve recovery timelines.

Product innovation, including pH-balanced and advanced antiseptic formulations, has enhanced clinical adoption across practices. Collectively, these factors have reinforced consistent market expansion across North America in 2025.

The Asia Pacific region is expected to experience the highest CAGR during the forecast period

Across Asia Pacific, the market is anticipated to advance steadily over the forecast period as veterinary services expand alongside rising animal ownership and agricultural activity.

The region hosts a substantial share of the global animal population, and the Food and Agriculture Organization notes that Asia accounts for a dominant portion of worldwide livestock, creating ongoing demand for animal health management solutions.

Veterinary practitioners in countries such as China, India, and Australia are strengthening wound care protocols to address injuries, infections, and surgical recovery in both companion and farm animals. Public health authorities are promoting improved hygiene practices in animal care to prevent disease transmission and support productivity in livestock sectors.

Expansion of private veterinary clinics and mobile care units is improving access to treatment in semi-urban and rural areas. Manufacturers are introducing affordable and locally adapted cleansing formulations that align with regional clinical requirements.

Professional training programs are enhancing awareness of proper wound management techniques among veterinarians. Additionally, rising consumer awareness regarding pet health is encouraging preventive and early-stage treatment adoption. These developments are expected to support sustained uptake of veterinary wound cleansing solutions throughout Asia Pacific.

Key Regions and Countries

North America

- The US

- Canada

Europe

- Germany

- France

- The U.K.

- Italy

- Spain

- Russia & CIS

- Rest of Europe

Asia Pacific

- China

- India

- Japan

- South Korea

- ASEAN

- Australia & New Zealand

- Rest of Asia Pacific

Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

Latin America

- Brazil

- Mexico

- Rest of Latin America

Key Players Analysis

Key participants in the Veterinary Wound Cleansers Market expand growth by developing advanced antiseptic formulations, strengthening partnerships with veterinary clinics, and introducing easy-to-apply wound care solutions that support faster healing in companion and livestock animals.

Companies invest in non-toxic, antimicrobial cleansers and spray-based products that improve infection control while ensuring safety for routine veterinary use. They also focus on expanding distribution through veterinary hospitals, retail pet care channels, and online platforms to improve product accessibility.

Virbac represents a prominent participant in the Veterinary Wound Cleansers Market and operates as a France-based animal health company that develops veterinary pharmaceuticals, hygiene products, and care solutions for companion animals and livestock.

The company emphasizes innovation in dermatology and wound care products supported by veterinary expertise. Industry competitors continue to introduce improved formulations, strengthen veterinary partnerships, and expand global reach to support effective wound management and sustained market growth.

Top Key Players

- Zoetis Inc.

- Elanco Animal Health Incorporated

- Boehringer Ingelheim International GmbH

- Merck & Co., Inc. (MSD Animal Health)

- Ceva Santé Animale

- Virbac

- Vetoquinol S.A.

- Dechra Pharmaceuticals PLC

- Bayer AG

- Johnson & Johnson

- 3M Company

Recent Developments

- In March 2026, Zoetis entered into a definitive agreement to acquire the animal genomics division of Neogen for $160 million. This acquisition supports Zoetis’ broader precision animal health strategy, which focuses on leveraging genetic insights to predict disease risks. Such advancements are expected to enable more targeted and preventive use of antiseptic wound care solutions, particularly in livestock management and breeding programs.

- During the February 2026 Animal Health Summit hosted by Bank of America, Elanco outlined its upcoming innovation pipeline. The company is prioritizing advanced pet health products, including new dermatological formulations that combine cleansing and therapeutic functions. These developments are designed to address the growing concern of antimicrobial resistance in companion animals while improving treatment outcomes.

- A notable trend through 2026 is the clinical shift away from conventional antiseptic agents such as iodine and chlorhexidine toward more advanced, low-cytotoxic alternatives like hypochlorous acid and polyhexanide. These solutions are increasingly preferred in veterinary hospital settings due to their ability to effectively manage biofilms while preserving sensitive tissue required for proper wound healing, especially in post-surgical care.

Report Scope

Report Features Description Market Value (2025) US$ 284.6 Million Forecast Revenue (2035) US$ 608.8 Million CAGR (2026-2035) 7.9% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments Segments Covered By Product Type (Antiseptic Solutions, Enzymatic Cleansers, Hydrogel Cleansers, Foam Cleansers, Spray Cleansers, Wipes and Pads and Others), By Animal Type (Companion Animals, Livestock Animals and Equine), By Application (Surgical Wounds, Traumatic Wounds, Chronic Wounds, Burns, Post-Operative Care, Dermatological Conditions and Others), By End User (Veterinary Hospitals, Veterinary Clinics, Animal Shelters and Others) Regional Analysis North America – The US, Canada; Europe – Germany, France, The U.K., Italy, Spain, Russia & CIS, Rest of Europe; Asia Pacific – China, India, Japan, South Korea, ASEAN, Australia & New Zealand, Rest of Asia Pacific; Middle East & Africa – GCC, South Africa, Rest of Middle East & Africa; Latin America – Brazil, Mexico, Rest of Latin America Competitive Landscape Zoetis Inc., Elanco Animal Health, Boehringer Ingelheim, Merck & Co., Inc., Ceva Santé Animale, Virbac, Vetoquinol S.A., Dechra Pharmaceuticals PLC, Bayer AG, Johnson & Johnson, 3M Company. Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)  Veterinary Wound Cleansers MarketPublished date: April 2026add_shopping_cartBuy Now get_appDownload Sample

Veterinary Wound Cleansers MarketPublished date: April 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- Zoetis Inc.

- Elanco Animal Health Incorporated

- Boehringer Ingelheim International GmbH

- Merck & Co., Inc. (MSD Animal Health)

- Ceva Santé Animale

- Virbac

- Vetoquinol S.A.

- Dechra Pharmaceuticals PLC

- Bayer AG

- Johnson & Johnson

- 3M Company

Our Clients

- 183802

- April 2026