Quick Navigation

- Report Overview

- Key Takeaway

- Role of Generative AI

- Investment and Business Benefits

- Regional Analysis

- Type Analysis

- Application Analysis

- Technology Analysis

- Security Level Analysis

- End-User Analysis

- Key Market Segments

- Emerging Trends

- Growth Factors

- Market Dynamics

- Key Players Analysis

- Recent Developments

- Report Scope

Report Overview

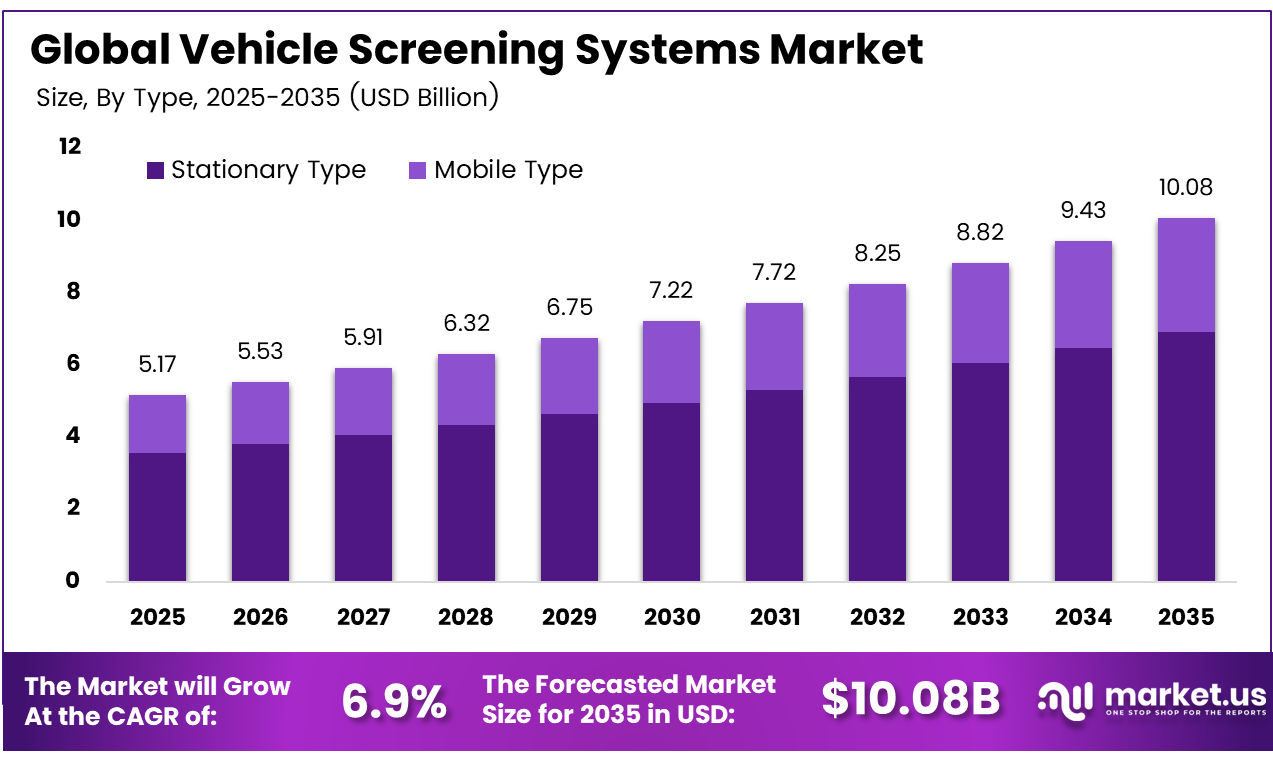

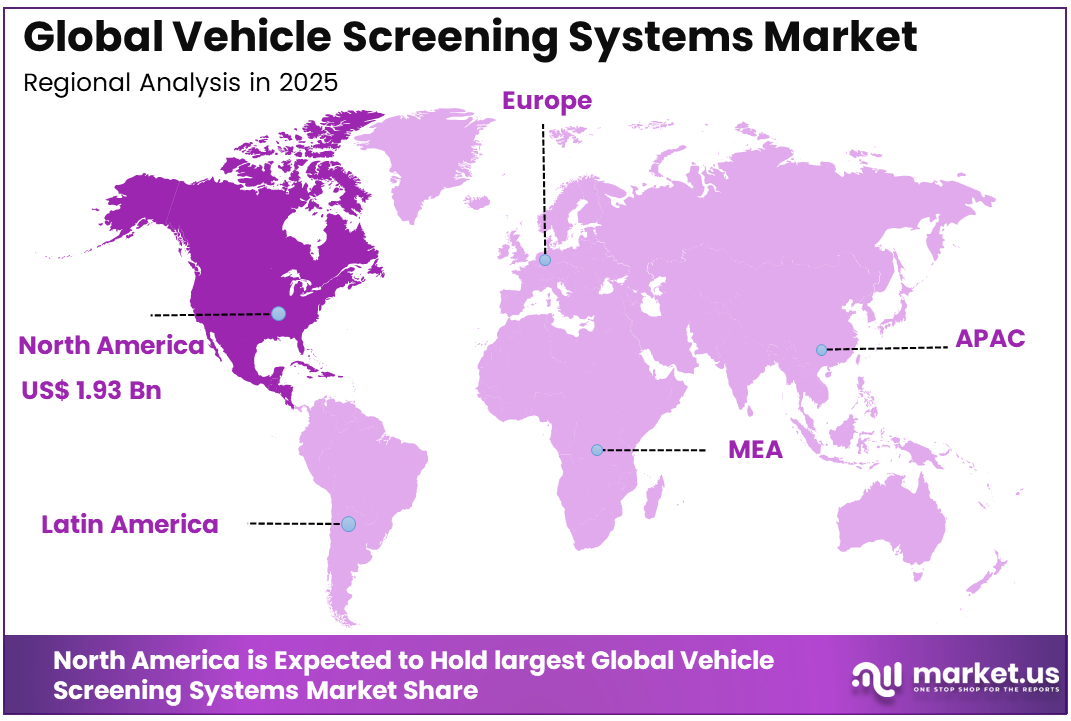

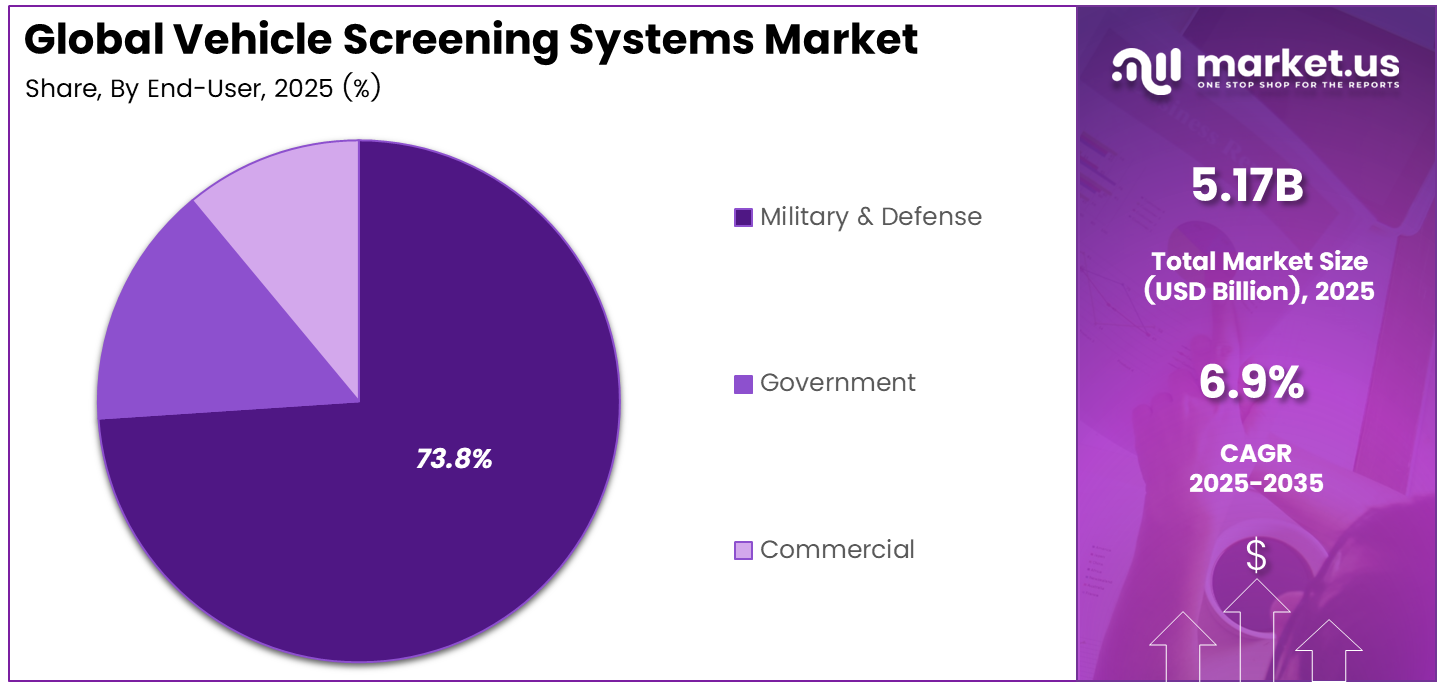

The Global Vehicle Screening Systems Market size is expected to be worth around USD 10.08 billion by 2035, from USD 5.17 billion in 2025, growing at a CAGR of 6.9% during the forecast period from 2025 to 2035. North America held a dominant market position, capturing more than a 37.4% share, holding USD 1.93 billion in revenue.

Vehicle Screening Systems refers to security solutions designed to inspect vehicles for hidden threats such as explosives, weapons, or contraband. These systems use scanners, sensors, cameras, and software to check vehicles quickly and safely at borders, airports, ports, and public venues, helping authorities improve security, reduce risk, and save time.

Security agencies are increasing vehicle screening deployments as terrorism risks intensify at borders, airports, and urban checkpoints. Vehicle-based attacks have risen by about 30% in urban areas worldwide, making rapid inspection essential. At the same time, ports and border crossings handle millions of trucks each day, so authorities need systems that can detect explosives, contraband, and hidden threats within seconds.

The market for Vehicle Screening Systems is driven by growing security needs at borders, airports, ports, and critical public infrastructure. The rising movement of commercial vehicles and cross-border trade increases the demand for faster and more reliable inspection systems. Governments and security agencies adopt these technologies to detect hidden threats, prevent illegal transportation, and maintain safety while ensuring smooth traffic flow at checkpoints.

Demand for vehicle screening systems is rising as cities grow and freight traffic expands. Truck volumes have increased by roughly 25% over the last decade, putting more pressure on roads, borders, and logistics hubs. Governments favor these systems in high-risk zones because manual checks create delays and still miss 15-20% of threats during routine inspections at busy trade corridors daily.

For instance, in March 2026, HTDS debuted portable gamma spectroscopy vehicle screening for nuclear threat detection across Europe. With 0.1 microcurie sensitivity, these French systems support NATO exercises. HTDS advances radiological screening capabilities for international security operations.

Key Takeaway

- In 2025, the Stationary Type segment held a dominant market position, capturing a 68.7% share of the Global Vehicle Screening Systems Market.

- In 2025, the Border Crossings segment held a dominant market position, capturing a 34.2% share of the Global Vehicle Screening Systems Market.

- In 2025, the X-ray Screening segment held a dominant market position, capturing a 51.4% share of the Global Vehicle Screening Systems Market.

- In 2025, the Standard Security segment held a dominant market position, capturing a 42.5% share of the Global Vehicle Screening Systems Market.

- In 2025, the Military & Defense segment held a dominant market position, capturing a 73.8% share of the Global Vehicle Screening Systems Market.

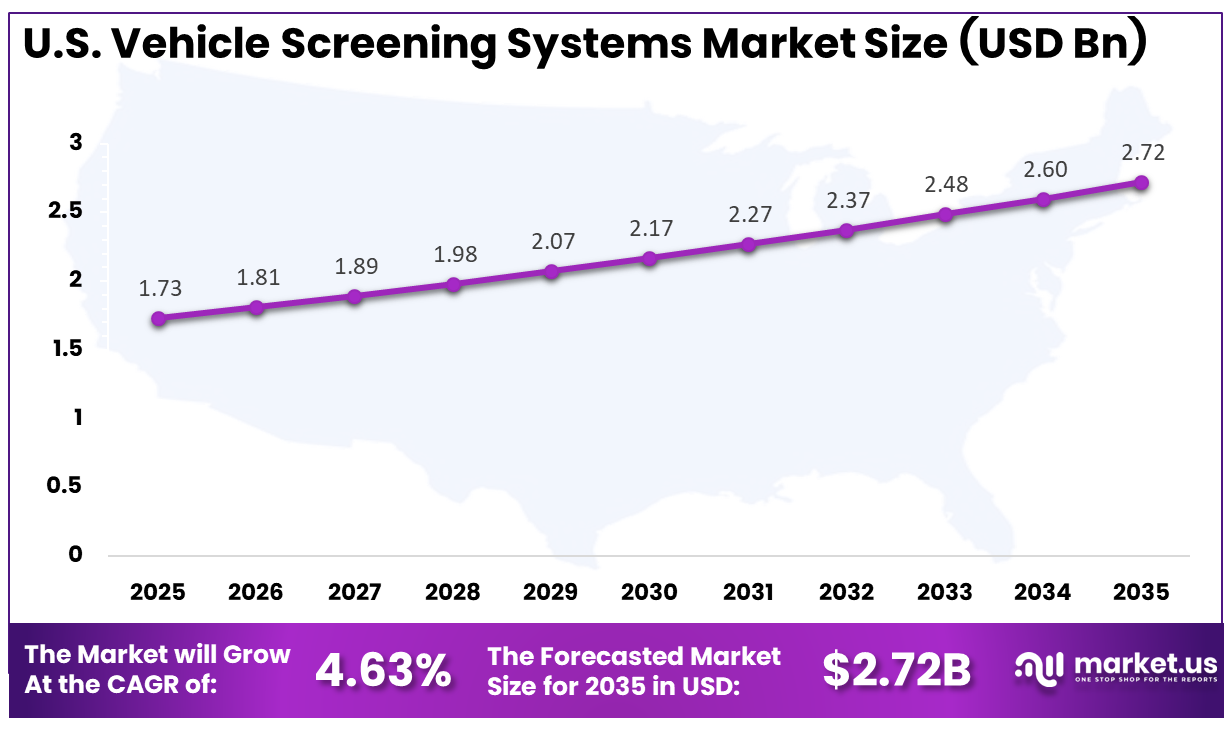

- The U.S. Vehicle Screening Systems Market was valued at USD 1.73 billion in 2025, with a robust CAGR of 4.63%.

- In 2025, North America held a dominant market position in the Global Vehicle Screening Systems Market, capturing more than a 37.4% share.

Role of Generative AI

Generative AI strengthens vehicle screening by producing synthetic data that helps train detection systems more effectively. It closes gaps in real sensor inputs from cameras and X-rays, improving threat identification in poor weather or low-light conditions. Tests show this approach reduces false alarms by 30%, supporting more reliable checkpoint decisions.

It also improves preparation for rare threat scenarios, including concealed explosives, by enabling large-scale virtual simulations. Security teams can run thousands of digital checks each day, which lowers the cost of real-world testing by 40%. This makes screening systems smarter over time and reduces dependence on constant human intervention significantly.

Investment and Business Benefits

Smart investment is moving toward mobile vehicle screening units that serve events, temporary checkpoints, and remote locations where permanent infrastructure is limited. Retrofitting legacy systems with AI add-ons can deliver fast returns by improving operational efficiency by 35% right away. Fast-growing urban regions also present strong potential for flexible, scalable solutions that match changing security and traffic demands over time.

Vehicle screening systems help organizations reduce disruption by cutting inspection times to under 30 seconds per vehicle, allowing smoother movement at gates and checkpoints. Automation also lowers labor costs by 20-30%, while reducing the risk of security failures and related penalties. Over time, these systems protect assets, strengthen compliance, and support safer, more dependable supply chains for global logistics networks.

Regional Analysis

In 2025, North America held a dominant market position in the Global Vehicle Screening Systems Market, capturing more than a 37.4% share, holding USD 1.93 billion in revenue. This dominance is because the region invests heavily in border security, airport protection, and critical infrastructure safety. Strong government spending, early adoption of advanced screening technologies, and strict inspection standards support wider deployment. High vehicle movement across trade routes and a growing focus on non-intrusive security checks also further strengthen regional demand and market leadership.

For instance, in January 2026, Leidos secured a $250M DHS contract for advanced vehicle screening systems at border checkpoints. Their AI-integrated solutions improve scan speeds and false alarm reduction, bolstering U.S. homeland security infrastructure. Leidos continues driving North America’s screening market leadership.

U.S. Vehicle Screening Systems Market Size

The market for Vehicle Screening Systems within the U.S. is growing tremendously and is currently valued at USD 1.73 billion; the market has a projected CAGR of 4.63%. The market is growing because security agencies are investing more in faster, non-intrusive inspection tools for borders, airports, ports, and public sites. Rising concerns around terrorism, smuggling, and illegal trafficking continue to strengthen demand. Growth in freight movement and cross-border trade also increases the need for quicker vehicle checks. In addition, technology upgrades such as AI-based imaging and automated detection are improving efficiency and adoption rates.

For instance, in February 2026, Rapiscan Systems strengthened U.S. dominance in vehicle screening by launching next-gen X-ray scanners for cargo and border security. Deployed at major U.S. ports, these systems enhance threat detection accuracy by 35%, supporting federal security mandates.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherlands

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Thailand

- Vietnam

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Type Analysis

In 2025, the Stationary Type segment held a dominant market position, capturing a 68.7% share of the Global Vehicle Screening Systems Market. This dominance is due to the widespread installation of fixed screening units at border checkpoints, ports, airports, and government facilities where constant monitoring is necessary. These systems allow authorities to inspect large volumes of vehicles efficiently while maintaining strong security control in permanent locations.

Stationary systems are preferred because they provide stable infrastructure and support advanced imaging technologies for detailed inspections. Security agencies rely on them to maintain consistent vehicle checks without operational disruptions. Their ability to handle continuous traffic flow while delivering reliable detection performance strengthens their adoption across high-security sites.

For instance, in March 2025, Nuctech rolled out new stationary gantry-style vehicle screening systems at a large customs complex in Asia. These fixed installations integrate with gate control and registration databases, enabling automated vehicle profiling and image analysis while minimizing manual intervention at busy inspection lanes.

Application Analysis

In 2025, the Border Crossings segment held a dominant market position, capturing a 34.2% share of the Global Vehicle Screening Systems Market. This dominance is due to the constant movement of commercial trucks, passenger vehicles, and cargo shipments across international borders. Governments rely on advanced screening systems to inspect vehicles quickly while preventing smuggling, illegal trade, and security threats.

Border security authorities also focus on improving inspection efficiency to avoid delays in trade routes. Vehicle screening technologies help officers examine vehicles without unloading cargo, which saves time and strengthens monitoring. Growing cross-border commerce and stricter customs inspections continue to support strong adoption at these locations.

For instance, in June 2025, OSI Systems secured an international contract to supply mobile and fixed vehicle inspection systems for port and border crossings, including high-energy mobile cargo check-points. The project supports flexible checkpoint relocation and rapid deployment at border zones where smuggling patterns shift frequently.

Technology Analysis

In 2025, the X-ray Screening segment held a dominant market position, capturing a 51.4% share of the Global Vehicle Screening Systems Market. This dominance is due to the technology’s ability to detect concealed items inside vehicles and cargo without requiring physical inspection. Security agencies depend on X-ray systems to identify weapons, explosives, narcotics, and other illegal materials hidden within vehicle structures.

The technology also offers clear internal imaging, which helps operators make faster and more accurate security decisions. Its non-intrusive inspection capability allows vehicles to move through checkpoints efficiently while maintaining strict security standards. These advantages support widespread deployment in security-sensitive locations.

For instance, in February 2026, Nuctech unveiled upgraded X-ray vehicle screening units featuring higher resolution imaging and improved radiation safety profiles. These systems are being piloted at several logistics hubs and border agencies that want to tighten detection without slowing down vehicle throughput.

Security Level Analysis

In 2025, the Standard Security segment held a dominant market position, capturing a 42.5% share of the Global Vehicle Screening Systems Market. This dominance is due to the large number of commercial facilities, logistics hubs, and public infrastructure locations that require regular vehicle inspection. These environments need reliable screening systems that maintain safety while allowing smooth movement of vehicles.

Standard security systems provide a balanced approach between safety and operational efficiency. They are widely used in everyday security operations where routine checks help prevent unauthorized access and transport of restricted items. Their practicality and cost effectiveness support broader deployment across civilian and commercial sectors.

For instance, in September 2025, Leidos expanded its standard-security vehicle screening offerings by integrating modular X-ray portals with basic access-control and camera systems for government and industrial sites. The approach focuses on detecting common anomalies such as hidden compartments and extra fuel tanks, rather than rare, ultra-sophisticated threats.

End-User Analysis

In 2025, the Military & Defense segment held a dominant market position, capturing a 73.8% share of the Global Vehicle Screening Systems Market. This dominance is due to the strong focus on national security and the protection of sensitive military infrastructure. Armed forces deploy vehicle screening systems at bases, border zones, and strategic facilities to detect threats and control access to restricted areas.

Defense organizations require dependable screening technologies to prevent the transportation of explosives, weapons, or unauthorized equipment into protected locations. Continuous investment in military security infrastructure encourages the adoption of advanced inspection systems that support safer operations and stronger protection of defense assets.

For instance, in January 2026, L3Harris Technologies delivered advanced vehicle screening solutions to several military installations, integrating them into existing base-security networks. The deployments emphasized robust, all-weather operations and seamless information sharing with command centers, highlighting the sector’s push toward integrated, technology-driven perimeter security.

Key Market Segments

By Type

- Stationary Type

- Mobile Type

By Application

- Airports

- Border Crossings

- Seaports

- Others

By Technology

- X-ray Screening

- Radiation Detection

- Explosives Trace Detection

By Security Level

- Standard Security

- Enhanced Security

- Critical Infrastructure

By End-User

- Military & Defense

- Government

- Commercial

Emerging Trends

Edge AI processing allows screening systems to analyze scans directly on the device, reducing the need to send information to distant servers. This cuts response delays by 25% at busy checkpoints and supports faster action. New hardware designs also bring stronger computing power into compact screening units for field deployment.

Multi-sensor fusion is becoming a key trend because it combines X-ray, radar, and AI vision into one screening process. This improves overall accuracy and helps operators catch smaller threats that single systems may overlook. Field trials have lifted detection rates to 95%, while drone integration adds real-time surveillance support nearby.

Growth Factors

Rising global trade volumes continue to increase the need for quicker vehicle screening across ports, highways, and border crossings. Ports now handle 15% more cargo yearly, so operators need systems that inspect vehicles in seconds without causing long queues. This movement of goods keeps demand strong for faster security solutions.

Stricter safety regulations are also driving market growth, as over 60% of nations now require non-intrusive vehicle inspections. These rules are pushing sites to replace older equipment with advanced systems. At the same time, user training programs make adoption easier, helping operators use new tools smoothly and confidently each day.

Market Dynamics

Drivers - Growing Security Concerns at Borders and Public Infrastructure

Security concerns at borders, airports, ports, and government facilities are increasing the need for reliable vehicle inspection systems. Authorities focus on preventing smuggling, illegal transport, and security threats before vehicles enter sensitive zones. Vehicle screening systems help security teams detect hidden risks quickly and improve protection across critical national infrastructure.

The rising movement of goods and passenger vehicles also increases pressure on security checkpoints. Manual inspections often slow operations and leave room for human error. Advanced vehicle screening technologies allow faster checks while maintaining strong protection, helping authorities manage safety requirements without disrupting transport and trade activities across busy locations.

For instance, in January 2026, OSI Systems (Rapiscan) stepped up with new contracts to secure border checkpoints using their Z Portal systems. These tools scan trucks and cargo for hidden threats, responding directly to rising risks at entry points. Authorities turned to them after recent alerts highlighted gaps in current setups, ensuring safer crossings without slowing trade.

Restraint - High Installation and Infrastructure Costs

High installation costs remain one of the main barriers to vehicle screening system adoption. Large scanning equipment requires specialized infrastructure, a stable power supply, and trained personnel for operation. Many smaller checkpoints and logistics hubs face difficulty investing in such systems due to financial limitations and operational complexity.

Maintenance and technical servicing also increase long-term operational expenses. Screening equipment must operate accurately to detect threats, which requires regular calibration and system checks. Limited technical expertise in some regions further complicates system management, slowing the adoption of advanced vehicle screening technologies in certain security environments.

For instance, in September 2025, Smiths Detection Group faced delays in a major airport rollout due to steep setup expenses for their vehicle scanners. Budget overruns from site modifications and custom integrations pushed back timelines by months. Local operators hesitated, opting for cheaper manual checks while weighing long-term value against immediate financial strain.

Opportunities - Expansion of Smart and Automated Security Technologies

The expansion of smart security technologies is creating new opportunities for vehicle screening systems. Artificial intelligence and automated analysis tools help security operators review scanning images faster and detect suspicious objects more efficiently. These technologies improve inspection accuracy while reducing the need for manual monitoring.

Automation also supports smoother traffic movement at busy checkpoints. Smart systems can quickly flag potential threats while allowing safe vehicles to pass without unnecessary delays. As governments continue modernizing security infrastructure, the demand for automated and intelligent vehicle inspection solutions is expected to increase steadily.

Challenges - Managing High Traffic While Maintaining Accurate Screening

Managing heavy vehicle traffic while maintaining strict security checks remains a major challenge. Busy border crossings and transport hubs handle thousands of vehicles daily. Security teams must inspect vehicles carefully without slowing trade or causing congestion, which creates operational pressure at many inspection points.

Environmental conditions and complex cargo loads can also affect screening accuracy. Dust, weather changes, and dense vehicle flow may interfere with scanning performance. Security agencies must ensure that systems remain reliable under such conditions so that threats are detected while minimizing unnecessary alerts during routine inspections.

For instance, in November 2025, Nuctech tackled congestion issues at a busy event venue with their high-volume portal tests. Peak crowds caused backups as scans lagged on varied vehicles, frustrating lines. Engineers adjusted algorithms on-site to balance speed and detection, learning hard lessons on real-world tweaks for non-stop accuracy.

Key Players Analysis

One of the leading players in November 2025, Smiths Detection Group acquired SecureScan for $85M, gaining under-vehicle inspection expertise. The deal strengthens their North American portfolio, now serving 40% more federal sites with combined fixed and mobile screening capabilities.

Top Key Players in the Market

- OSI Systems (Rapiscan)

- Nuctech

- Leidos

- Smiths Detection Group

- ADANI Systems

- Begood (CGN)

- Astrophysics

- VMI Security Systems

- HTDS

- Thermo Fisher Scientific

- L3Harris Technologies

- CEIA

- Gilardoni

- Eas Envimet Analytical Systems

- Leidos Holdings

- Others

Recent Developments

- In January 2026, OSI Systems (Rapiscan) launched the Eagle P60 HV, a high-volume drive-through X-ray system for ports and borders. Deployed at 15 major U.S. crossings, it cuts inspection times by 40% while boosting contraband detection. This keeps American tech ahead in cargo screening security.

- In February 2026, Nuctech unveiled its MT1210E mobile scanner with dual-view imaging for faster vehicle checks. Secured contracts worth $120M across Asian ports, expanding global reach while challenging Western dominance in high-throughput screening solutions.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 5.17 Billion |

| Forecast Revenue (2035) | USD 10.08 Billion |

| CAGR (2026-2035) | 6.9% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Type (Stationary Type, Mobile Type), By Application (Airports, Border Crossings, Seaports, Others), By Technology (X-ray Screening, Radiation Detection, Explosives Trace Detection), By Security Level (Standard Security, Enhanced Security, Critical Infrastructure), By End-User (Government, Commercial, Military & Defense) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | OSI Systems (Rapiscan), Nuctech, Leidos, Smiths Detection Group, ADANI Systems, Begood (CGN), Astrophysics, VMI Security Systems, HTDS, Thermo Fisher Scientific, L3Harris Technologies, CEIA, Gilardoni, Eas Envimet Analytical Systems, Leidos Holdings, Others |

| Customization Scope | Customization at the segment and region/country levels will be provided. Moreover, customization can be tailored to the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |