Quick Navigation

Report Overview

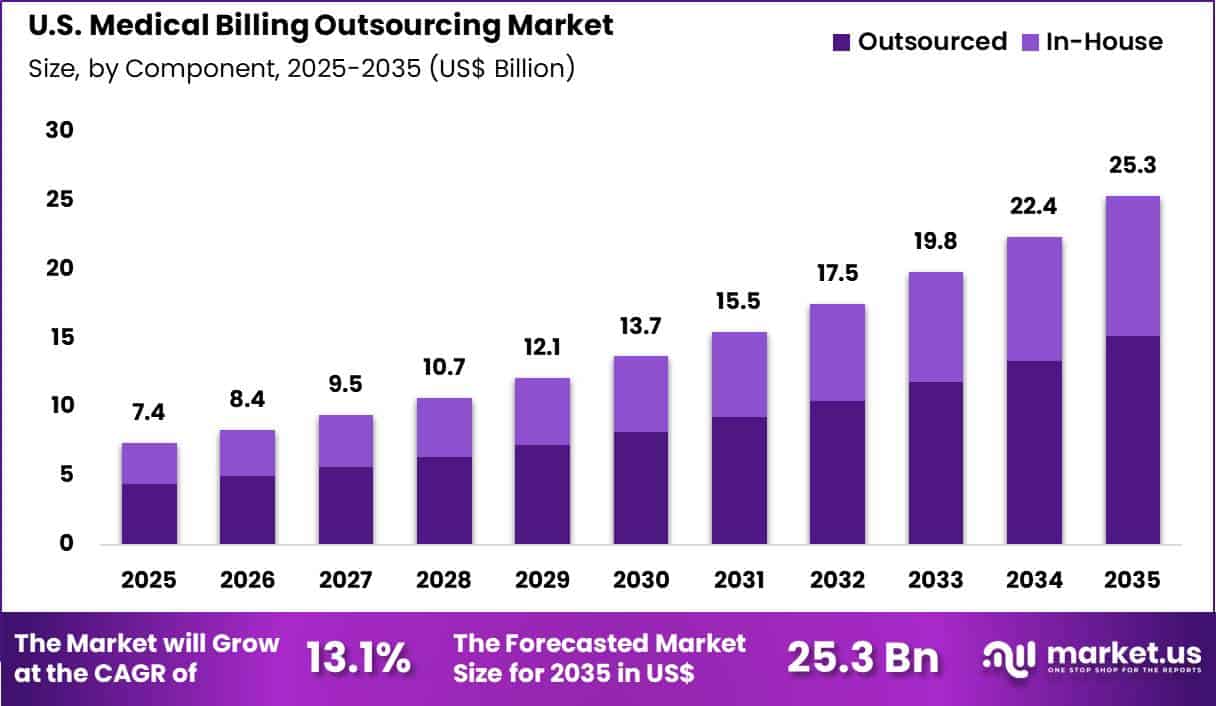

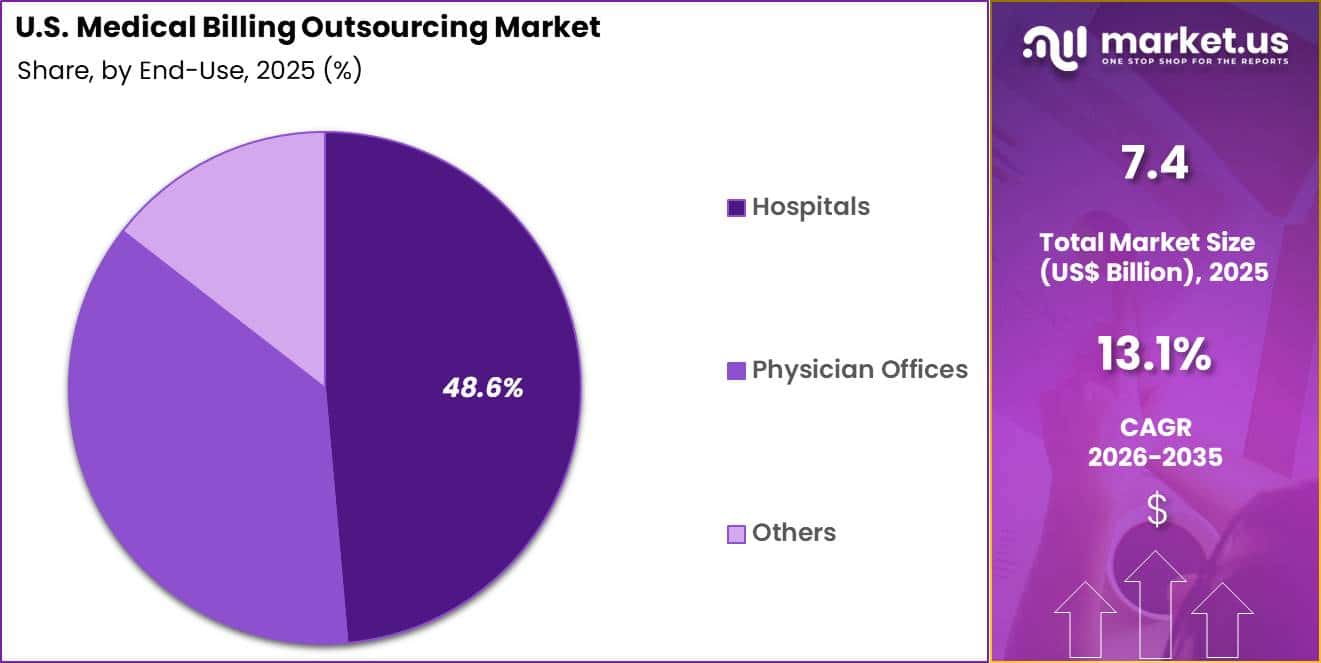

The U.S. Medical Billing Outsourcing Market size is expected to be worth around US$ 25.3 Billion by 2035 from US$ 7.4 Billion in 2025, growing at a CAGR of 13.1% during the forecast period 2026-2035.

Rising administrative burdens and escalating operational costs compel healthcare providers in the U.S. to increasingly outsource medical billing functions to specialized revenue cycle management firms that deliver expertise, scalability, and compliance assurance.

Physician practices and hospitals outsource claims submission and denial management to reduce errors in coding complex procedures such as interventional cardiology and oncology infusions, ensuring accurate reimbursement from Medicare, Medicaid, and commercial payers.

These services support denial resolution by analyzing rejection patterns and appealing underpaid or denied claims, recovering revenue that would otherwise be lost in high-volume specialties like orthopedics and emergency medicine.

Outsourcing partners handle patient eligibility verification and prior authorization processes for advanced therapies, including biologics and durable medical equipment, preventing delays and claim rejections that disrupt cash flow.

Medical groups rely on outsourced billing for patient payment collection and financial counseling, improving collections rates while maintaining positive patient relationships through transparent billing communication. These services also facilitate compliance with evolving regulations, including HIPAA security standards and payer-specific guidelines, minimizing audit risks in multi-specialty practices.

Revenue cycle management firms seize opportunities to leverage artificial intelligence and cloud-based platforms that automate error-prone tasks and enhance real-time collaboration between providers and payers. These technologies support predictive denial management by identifying potential issues before claims submission, accelerating resolution in specialties with high denial rates such as radiology and anesthesiology.

Outsourcing providers advance end-to-end solutions that integrate clinical documentation improvement with billing workflows, capturing accurate charge data for value-based care contracts and bundled payments. Opportunities emerge in analytics-driven services that optimize payer contract performance and identify underpayments in complex reimbursement models.

Companies invest in secure, interoperable systems that streamline prior authorizations and appeals for high-cost procedures. In March 2026, Optum (a division of UnitedHealth Group) expanded its strategic partnership with Microsoft to utilize advanced cloud and AI tools to streamline the claims and reimbursement experience.

This follows the 2025 rollout of Optum Integrity One, an AI-powered platform that uses Clinical Language Intelligence to automate the “middle-end” of the revenue cycle. The platform aims to eliminate administrative friction by connecting payers and providers in real-time to resolve billing discrepancies before a claim is even submitted.

Recent trends emphasize proactive, AI-enabled denial prevention and payer-provider connectivity, positioning outsourced medical billing as a strategic enabler of financial stability and operational efficiency in U.S. healthcare delivery.

Key Takeaways

- In 2025, the market generated a revenue of US$ 7.4 Billion, with a CAGR of 13.1%, and is expected to reach US$ 25.3 Billion by the year 2035.

- The service segment is divided into full-service outsourcing, hybrid outsourcing, billing software as a service (SaaS) and consulting and advisory services, with full-service outsourcing taking the lead with a market share of 42.2%.

- Considering component, the market is divided into in-house and outsourced. Among these, outsourced (vs. in-house) held a significant share of 59.8%.

- Furthermore, concerning the end-use segment, the market is segregated into hospitals, physician offices and others. The hospitals sector stands out as the dominant player, holding the largest revenue share of 48.6% in the market.

Service Analysis

Full-service outsourcing accounted for 42.2% of growth within services and dominate the U.S. medical billing outsourcing market due to increasing administrative complexity and rising healthcare reimbursement regulations. Healthcare providers increasingly rely on external billing specialists to manage coding, claims submission, denial management, and revenue cycle optimization.

The American Medical Association reports that physicians spend significant time managing administrative tasks, which reduces time available for patient care. Hospitals and clinics increasingly adopt comprehensive outsourcing models to improve billing accuracy and accelerate reimbursement cycles.

Full-service outsourcing providers integrate advanced analytics and automated coding technologies to enhance claim processing efficiency. Healthcare organizations are projected to expand outsourcing strategies as regulatory compliance requirements continue to grow.

Rising demand for efficient revenue cycle management and cost optimization is expected to strengthen adoption of full-service outsourcing solutions across healthcare providers in the United States.

Component Analysis

Outsourced components accounted for 59.8% of growth within the component segment and dominate the U.S. medical billing outsourcing market due to healthcare organizations shifting administrative workloads to specialized service providers.

Hospitals and physician practices increasingly outsource billing functions to reduce operational costs and improve claim processing efficiency. Outsourcing firms employ certified coding professionals and automated revenue cycle management platforms that help reduce claim rejection rates.

The Centers for Medicare & Medicaid Services reports that healthcare administrative spending represents a substantial portion of overall healthcare expenditures in the United States. Healthcare providers increasingly outsource billing operations to control these administrative costs and focus on core clinical services.

Outsourced solutions are anticipated to expand as healthcare systems adopt digital billing technologies and advanced data analytics. Continuous pressure to improve revenue cycle performance is likely to accelerate outsourcing adoption among healthcare providers.

End-Use Analysis

Hospitals accounted for 48.6% of growth within end-use and dominate the U.S. medical billing outsourcing market because hospitals process large volumes of complex medical claims across multiple specialties and treatment categories.

Large healthcare systems manage thousands of patient encounters each day, which generates substantial billing workloads. Outsourcing providers help hospitals manage coding compliance, claims submission, reimbursement tracking, and payer communication.

The American Hospital Association reports that the United States operates thousands of hospitals that deliver extensive inpatient and outpatient services each year. Hospitals increasingly integrate outsourced revenue cycle management solutions to maintain financial stability and reduce claim denial rates.

Healthcare organizations are projected to expand outsourcing partnerships as patient volumes and reimbursement complexities increase. Continuous investment in hospital revenue cycle optimization is expected to strengthen the adoption of outsourced medical billing services.

Key Market Segments

By Service

- Full-Service Outsourcing

- Hybrid Outsourcing

- Billing Software as a Service (SaaS)

- Consulting and Advisory Services

By Component

- In-House

- Outsourced

By End-use

- Hospitals

- Physician Offices

- Others

Drivers

Rising volume of outsourced medical billing services is driving the market.

The U.S. medical billing outsourcing market continues to expand due to sustained growth in the volume of claims processed through third-party revenue cycle management providers. Healthcare providers increasingly delegate billing functions to specialized vendors to address staffing shortages and administrative burdens.

Outsourced services handle higher claim volumes with improved first-pass resolution rates compared to in-house operations. The driver aligns with ongoing consolidation among physician groups and ambulatory surgery centers requiring scalable billing infrastructure.

Vendors report consistent increases in managed claims per client as practices expand service lines. The trend supports adoption of technology-enabled billing platforms integrated with electronic health records. Providers achieve measurable reductions in accounts receivable days through professional revenue cycle expertise.

The momentum reflects persistent pressure on operating margins necessitating cost-effective administrative solutions. Enhanced compliance with evolving payer policies further elevates demand for experienced outsourcing partners. This factor maintains steady progression in market penetration across various care settings.

Restraints

Persistent workforce shortages in medical billing roles is restraining the market.

Healthcare organizations face ongoing difficulties recruiting and retaining qualified medical coders and billers amid national labor market constraints. The shortage contributes to elevated turnover rates and increased training costs for in-house teams.

Many facilities experience delays in claim submission and follow-up due to staffing gaps. The restraint limits the ability of smaller practices to maintain efficient internal billing operations. Providers encounter challenges in keeping pace with frequent coding guideline updates without dedicated personnel.

The factor moderates the transition speed from outsourced to in-house models in certain segments. Outsourcing vendors also face competition for skilled staff to support client growth.

The dynamic influences pricing negotiations as providers weigh internal versus external cost structures. This constraint continues to temper balanced development across the revenue cycle management landscape. The limitation persists in constraining rapid scalability for some market participants.

Opportunities

Adoption of AI-enhanced denial management platforms is creating growth opportunities.

Vendors have introduced AI-driven tools that analyze denial patterns, predict rejection risks, and recommend corrective actions prior to claim submission. These platforms enable proactive intervention to reduce preventable denials and accelerate reimbursement cycles. Opportunities arise for differentiation through superior denial management performance metrics.

The technology supports scalable processing of high-volume claims with minimal manual review. Providers gain visibility into root causes of denials across payer contracts. The framework facilitates continuous performance improvement through machine learning refinements.

Outsourcing partners can demonstrate quantifiable return on investment through reduced write-offs. Such capabilities attract clients seeking measurable improvements in net revenue retention.

The opportunity fosters expansion into value-added services beyond traditional claim submission. This advancement positions participants for competitive advantage in a maturing outsourcing environment.

Impact of Macroeconomic / Geopolitical Factors

Macroeconomic conditions influence the U.S. medical billing outsourcing market through healthcare administrative budgets, provider revenue cycle priorities, and labor costs across billing operations.

Inflation increases expenses for skilled billing staff, software platforms, and compliance management, which encourages healthcare providers to reassess in-house billing operations. Higher interest rates reduce expansion capital for smaller clinics and healthcare groups, which pushes many providers toward outsourcing to control operational costs.

Geopolitical tensions affect global outsourcing networks and cross-border data service operations, creating regulatory and operational complexity for service providers. Current US tariffs on imported IT hardware and data infrastructure equipment increase technology deployment costs for billing service vendors.

These pressures can tighten margins for outsourcing firms and slow technology upgrades in the short term. At the same time, providers increasingly rely on specialized outsourcing partners to improve claim accuracy and accelerate reimbursements.

Growing demand for efficient revenue cycle management and administrative cost reduction continues to support steady and confident market growth.

Latest Trends

Increased CMS focus on prior authorization reform is driving the market.

The Centers for Medicare & Medicaid Services implemented updated prior authorization requirements in 2025 for certain Medicare Advantage plans, mandating standardized electronic submission processes. These changes require enhanced documentation and faster turnaround times from providers.

The 2025 policy adjustments increase administrative complexity for practices managing Medicare Advantage populations. Outsourcing vendors with established payer connectivity and expertise gain preference for handling these requirements efficiently.

The development aligns with broader efforts to reduce provider burden through automation and standardization. Facilities report improved compliance and reduced delay in authorization approvals through specialized support. The regulatory evolution stimulates demand for comprehensive revenue cycle management solutions.

The trend supports investment in interoperable platforms compliant with new transaction standards. Early implementations demonstrate accelerated authorization processing in affected segments. Overall, this policy advancement strengthens the strategic importance of professional billing outsourcing services.

Key Players Analysis

Key participants in the U.S. Medical Billing Outsourcing Market expand their presence by deploying advanced revenue cycle management platforms, strengthening partnerships with hospitals, and introducing AI-driven automation that improves claims processing accuracy and reimbursement efficiency.

Companies increasingly adopt cloud-based billing systems and analytics tools to reduce administrative workloads and accelerate payment cycles for healthcare providers. Strategic alliances, mergers, and service expansions also help vendors broaden their client base among physician practices and ambulatory centers.

R1 RCM Inc. represents a prominent participant in the U.S. Medical Billing Outsourcing Market and operates as a healthcare technology company that provides revenue cycle management services, coding solutions, and financial performance analytics for hospitals and physician groups across the country.

The firm focuses on automation, data analytics, and end-to-end billing solutions that streamline administrative workflows and improve collection efficiency. Major competitors such as AdvancedMD, eClinicalWorks, and Veradigm continue to invest in digital billing platforms and AI-enabled coding tools to strengthen operational efficiency and expand service adoption among healthcare providers.

Top Key Players

- R1 RCM Inc.

- Veradigm LLC

- Oracle (Cerner Corporation)

- eClinicalWorks

- Kareo, Inc.

- McKesson Corporation

- Quest Diagnostics

- Promantra Inc.

- AdvancedMD, Inc.

- eBilling Inc

Recent Developments

- In March 2025, R1 RCM launched R37, a specialized AI lab developed in exclusive partnership with Palantir Technologies. The lab is designed to overhaul labor-intensive revenue cycle operations such as autonomous medical coding and denials management. Following this launch, in May 2025, R1 secured a significant investment from Khosla Ventures to further scale these “agentic AI” solutions across its client base, which currently includes 94 of the top 100 U.S. health systems.

- In March 2026, Waystar announced an expanded collaboration with Google Cloud to integrate Gemini large language models into its AltitudeAI platform. This development focuses on achieving an “autonomous revenue cycle” by automating the generation of complex appeal letters and prior authorizations. According to company data, this AI-driven approach has already prevented over $15 billion in denied claims and reduced the time spent on recovery efforts by 90% for its 30,000 U.S. clients.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | US$ 7.4 Billion |

| Forecast Revenue (2035) | US$ 25.3 Billion |

| CAGR (2026-2035) | 13.1% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments |

| Segments Covered | By Service (Full-Service Outsourcing, Hybrid Outsourcing, Billing Software as a Service (SaaS) and Consulting and Advisory Services), By Component (In-House and Outsourced), By End-use (Hospitals, Physician Offices and Others) |

| Competitive Landscape | R1 RCM Inc., Veradigm LLC, Oracle (Cerner Corporation), eClinicalWorks, Kareo, Inc., McKesson Corporation, Quest Diagnostics, Promantra Inc., AdvancedMD, Inc., eBilling Inc. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |