Quick Navigation

Report Overview

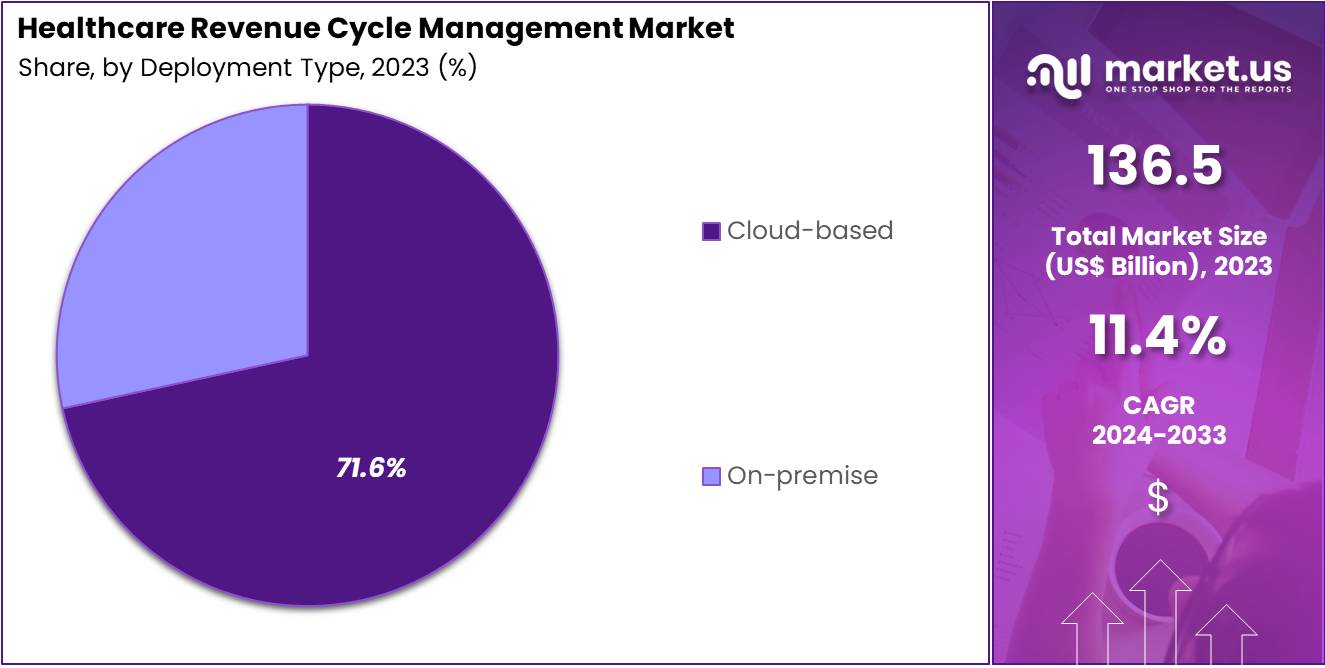

The Healthcare Revenue Cycle Management Market size is expected to be worth around US$ 401.8 billion by 2033 from US$ 136.5 billion in 2023, growing at a CAGR of 11.4% during the forecast period 2024 to 2033.

Growing complexities in healthcare billing and reimbursement processes are driving the expansion of the healthcare revenue cycle management (RCM) market. Increasing adoption of value-based care models and the rise of regulatory changes are pushing healthcare providers to streamline revenue processes for improved financial performance.

Healthcare RCM solutions encompass various applications, including patient billing, coding, claims management, payment posting, and accounts receivable management, all critical for ensuring accurate and timely reimbursement. As healthcare organizations face pressure to reduce administrative costs, RCM technologies offer substantial opportunities for operational efficiency and cost savings.

In October 2023, Omega Healthcare launched the Omega Digital Platform (ODP), which helps healthcare organizations optimize their revenue cycle operations, lower administrative overhead, and enhance financial outcomes. The growing integration of artificial intelligence and machine learning in RCM solutions is another trend, enabling predictive analytics for better decision-making and faster claims resolution.

Furthermore, the shift toward electronic health records (EHR) systems and the increasing digitization of healthcare services present new opportunities for seamless data flow, reducing human error and improving the accuracy of financial transactions. These innovations make RCM more effective, driving market growth and increasing demand for advanced revenue cycle solutions.

Key Takeaways

- In 2023, the market for Healthcare Revenue Cycle Management generated a revenue of US$ 136.5 billion, with a CAGR of 11.4%, and is expected to reach US$ 401.8 billion by the year 2033.

- The product type segment is divided into integrated and standalone, with integrated taking the lead in 2023 with a market share of 62.3%.

- Considering function type, the market is divided into payment remittance, medical coding & billing, eligibility verification, claims & denial management, and others. Among these, claims & denial management held a significant share of 44.2%.

- Furthermore, concerning the deployment type segment, the market is segregated into cloud-based and on-premise. The cloud-based sector stands out as the dominant player, holding the largest revenue share of 71.6% in the Healthcare Revenue Cycle Management market.

- The end-user segment is segregated into hospitals, physician office, diagnostic labs and ASCs, and others, with the physician office segment leading the market, holding a revenue share of 50.5%.

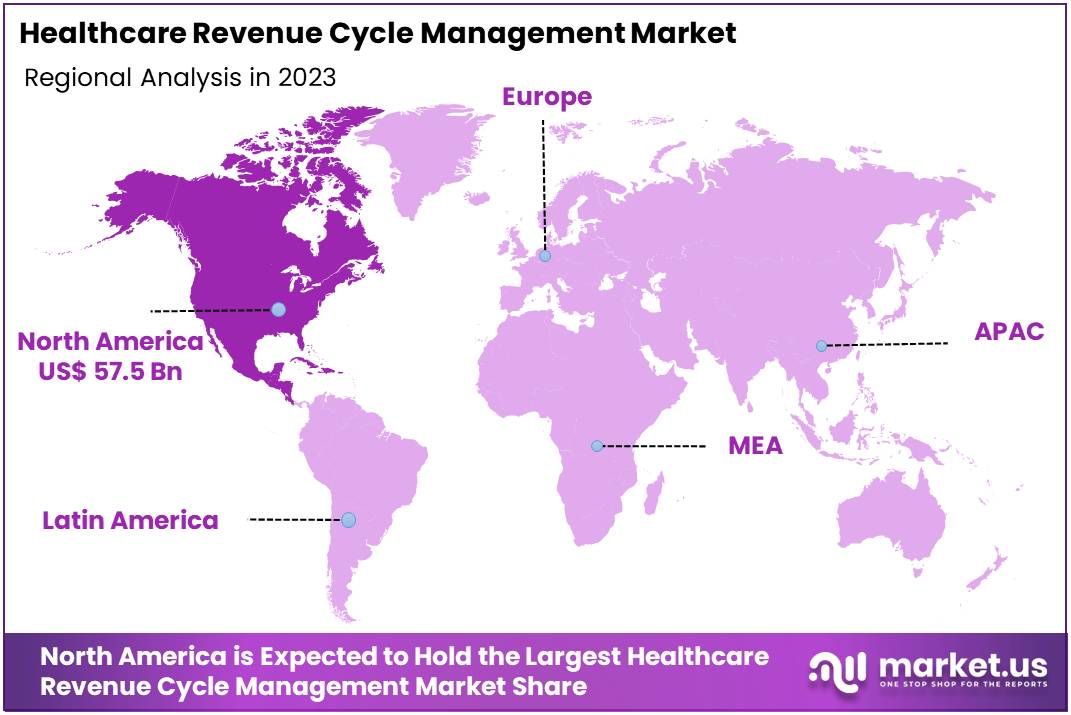

- North America led the market by securing a market share of 42.1% in 2023.

Product Type Analysis

The integrated segment led in 2023, claiming a market share of 62.3% owing to the increasing demand for more cohesive and efficient solutions. Healthcare organizations are projected to favor integrated systems that streamline various revenue cycle processes, including patient scheduling, billing, coding, and claims management, into a unified platform.

The integration of these processes helps reduce errors, improve data accuracy, and enhance operational efficiency, which is expected to be a major factor in the growing adoption of integrated solutions. The rising complexity of billing systems, regulatory requirements, and reimbursement models, along with the growing need for real-time data access and decision-making, is likely to drive the shift towards integrated systems.

Moreover, integrated solutions provide enhanced analytics capabilities, enabling providers to optimize revenue generation, reduce administrative costs, and improve cash flow management. This segment is estimated to expand as hospitals, large healthcare networks, and medical providers seek to enhance operational productivity and improve patient satisfaction.

Function Type Analysis

The claims & denial management held a significant share of 44.2% due to the increasing complexities in claims processing and the heightened focus on improving reimbursement rates. Healthcare providers are expected to invest more in claims and denial management solutions to address rising denial rates caused by coding errors, incomplete documentation, and eligibility verification issues.

The shift towards value-based care is anticipated to further accelerate the need for these solutions as providers must ensure accurate claims and timely reimbursements to sustain profitability. Denial management solutions help identify root causes of denials and streamline the appeals process, thus reducing revenue loss.

As the healthcare industry moves towards more sophisticated reimbursement models, such as bundled payments and pay-for-performance, the demand for effective claims and denial management solutions is likely to increase. Furthermore, regulatory pressures to comply with accurate billing practices are expected to drive the continued growth of this segment, especially among smaller healthcare providers seeking to optimize their revenue cycle operations.

Deployment Type Analysis

The cloud-based segment had a tremendous growth rate, with a revenue share of 71.6% owing to the increasing demand for flexible, scalable, and cost-effective solutions. Cloud-based systems offer healthcare providers the advantage of remote access, which is projected to improve operational efficiency and streamline workflows, particularly for smaller healthcare practices and outpatient facilities.

The rising adoption of electronic health records (EHR) and the need for real-time data analytics are anticipated to contribute significantly to this growth. Furthermore, cloud-based solutions reduce the burden of maintaining on-premise infrastructure and allow for seamless updates, which healthcare organizations are likely to favor to stay compliant with changing regulations.

The integration of artificial intelligence and machine learning in cloud platforms is estimated to further enhance decision-making, predictive analytics, and billing accuracy. Additionally, the growing trend toward telemedicine and decentralized healthcare models is expected to accelerate the demand for cloud-based revenue cycle management solutions, as they enable seamless coordination across multiple locations and devices.

End-user Analysis

The physician office segment grew at a substantial rate, generating a revenue portion of 50.5% due to the increasing need for efficient and cost-effective revenue cycle solutions. Physician offices are projected to adopt these solutions to streamline billing, coding, and claims processing as the complexity of insurance reimbursement increases.

The shift towards value-based care and alternative payment models is expected to further fuel this growth, as physician offices need to optimize revenue capture while minimizing errors in claims submissions. Additionally, physician offices are likely to benefit from cloud-based and integrated revenue cycle management solutions, which offer better scalability, reduced operational costs, and improved workflow efficiency.

As healthcare providers continue to focus on improving patient outcomes and satisfaction, the demand for tailored solutions that address the unique needs of physician offices is expected to rise. This segment is projected to expand as smaller practices increasingly recognize the value of technology in enhancing their financial performance and operational efficiency.

Key Market Segments

By Product Type

- Integrated

- Standalone

By Function Type

- Payment Remittance

- Medical Coding & Billing

- Eligibility Verification

- Claims & Denial Management

- Others

By Deployment Type

- Cloud-based

- On-premise

By End-user

- Hospitals

- Physician Office

- Diagnostic Labs and ASCs

- Others

Drivers

Growing Investment in Healthcare Drives the Market

Growing investment in healthcare significantly drives the healthcare revenue cycle management (RCM) market by enabling the development and adoption of more efficient, automated solutions. In June 2024, Adonis, an AI-driven RCM startup, raised US$54 million, including US$31 million in Series B funding, to enhance its platform for billing, payments, and reimbursements.

This growing investment supports innovations in RCM systems, helping healthcare providers streamline processes, reduce administrative costs, and improve financial outcomes. With increasing demand for efficient and cost-effective solutions, RCM providers are likely to continue scaling operations, leveraging technologies like artificial intelligence and automation to minimize errors and optimize workflows.

As healthcare organizations seek to improve patient experience while ensuring financial sustainability, the market for advanced RCM solutions is projected to expand. Furthermore, the focus on enhancing billing accuracy and ensuring compliance with regulatory standards creates additional opportunities for RCM technology providers. Investment in these systems helps healthcare organizations overcome challenges like staffing shortages and complex billing processes. These ongoing investments in RCM technologies are expected to propel the market forward, making it a critical component of healthcare operations.

Restraints

Complexity of Regulatory Compliance Restraining the Market

A significant restraint in the healthcare revenue cycle management market is the complexity of regulatory compliance. As healthcare systems evolve and become more global, maintaining adherence to ever-changing regulations becomes increasingly challenging. Providers must ensure that billing practices align with federal, state, and international standards, which can vary significantly. These regulations often require continuous updates to RCM systems, creating additional costs and operational burdens for healthcare organizations.

The need for ongoing training and compliance monitoring further strains resources, particularly in smaller practices with limited budgets. Additionally, the frequent updates to billing codes and insurance requirements can lead to errors and delays in reimbursements, impacting cash flow. The increasing complexity of compliance is projected to slow down the adoption of new RCM technologies, especially in regions with strict regulatory environments. This growing regulatory burden can prevent healthcare organizations from fully leveraging RCM solutions, restraining market growth.

Opportunities

Increasing Demand for Cloud-Based Software Solutions is Creating Opportunities for the Market

Increasing demand for cloud-based software solutions is creating significant opportunities for the healthcare revenue cycle management (RCM) market. Healthcare organizations are increasingly adopting cloud-based RCM solutions for their scalability, flexibility, and cost-effectiveness. These solutions allow providers to streamline billing, claims management, and payments while improving data accessibility and collaboration across multiple locations.

Cloud-based platforms also offer advanced features like real-time analytics, which help healthcare organizations make data-driven decisions and optimize their financial performance. As healthcare providers strive to improve operational efficiency and reduce overhead costs, cloud-based RCM solutions are expected to become more attractive due to their ability to minimize IT infrastructure investments.

Additionally, the ability to securely store and access patient and financial data remotely is projected to drive the adoption of cloud-based systems, particularly in the wake of increasing telehealth services. The rising trend towards digital transformation in healthcare is likely to further accelerate the shift to cloud solutions, creating substantial growth opportunities for RCM providers in the coming years.

Impact of Macroeconomic / Geopolitical Factors

Macroeconomic and geopolitical factors have a substantial influence on the healthcare revenue cycle management market. On the positive side, increasing healthcare expenditure and rising demand for healthcare services, driven by aging populations and the expansion of insurance coverage, fuel market growth. However, economic downturns or recessions can strain healthcare budgets, resulting in tighter profit margins and delayed reimbursements.

Geopolitical factors, such as trade disputes or regulatory changes, can disrupt the supply of key technologies or affect cross-border healthcare investments. The global push for healthcare reforms also introduces new complexities, increasing the regulatory burden on providers. Despite these challenges, the adoption of digital transformation and automation within revenue cycle management systems is anticipated to mitigate risks, enhance operational efficiencies, and foster market resilience, supporting long-term growth.

Trends

Integration of AI in Healthcare Revenue Cycle Management

Growing integration of artificial intelligence (AI) is a driving force in the healthcare revenue cycle management market. AI technologies are expected to enhance the accuracy and efficiency of billing, coding, and claim processing, reducing human errors and increasing operational speed. In May 2024, R1 RCM launched an AI-driven revenue cycle management platform designed to improve claim accuracy and reduce denials.

The platform utilizes predictive analytics and real-time decision support to streamline billing processes, which is likely to result in better financial outcomes for healthcare providers. AI’s capabilities in automating routine tasks, detecting anomalies, and providing actionable insights are anticipated to drastically reduce administrative costs and errors, making the healthcare revenue cycle more efficient and cost-effective. This trend is set to revolutionize the industry, driving growth and improved financial performance for providers.

Regional Analysis

North America is leading the Healthcare Revenue Cycle Management Market

North America dominated the market with the highest revenue share of 42.1% owing to technological advancements and increasing demand for operational efficiency. Healthcare providers, particularly in the United States, faced rising operational costs and the complexity of reimbursement processes, prompting greater reliance on RCM solutions.

The adoption of automation and artificial intelligence (AI) technologies has played a crucial role in improving the efficiency and accuracy of billing and coding processes. In September 2022, AGS Health launched the AGS AI Platform, combining AI with human-in-the-loop services to optimize revenue cycle management, thus enhancing overall performance for healthcare providers. The implementation of these advanced technologies has reduced claim denials and sped up payment cycles, contributing significantly to market growth.

Additionally, the rising prevalence of chronic diseases and increasing healthcare expenditures in North America have further fueled the demand for more streamlined and efficient RCM solutions. As a result, the market is expected to continue expanding as healthcare organizations prioritize financial sustainability.

The Asia Pacific region is expected to experience the highest CAGR during the forecast period

Asia Pacific is expected to grow with the fastest CAGR owing to the rapid expansion of healthcare infrastructure and services. The increasing adoption of digital health solutions, such as electronic health records (EHR) and AI-based billing systems, is expected to improve the efficiency of revenue cycle processes. In countries like China and India, where healthcare systems are modernizing at a rapid pace, the need for optimized revenue cycle management is anticipated to rise.

By 2023, China’s healthcare security system had enabled over 250 million patients to receive medical treatment, underscoring the country’s progress in healthcare access. This expansion is likely to drive a higher demand for advanced RCM solutions. Additionally, the growing number of private healthcare providers in the region is estimated to further propel market growth, as these providers seek efficient methods for managing billing, payments, and claims. The rising focus on reducing administrative costs and improving reimbursement rates is expected to be a key factor in the market’s expansion in Asia Pacific.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherland

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- New Zealand

- Singapore

- Thailand

- Vietnam

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

Key players in the healthcare revenue cycle management market employ several strategies to drive growth, including the integration of advanced technologies such as AI and machine learning to streamline processes and improve accuracy. Companies focus on expanding their service offerings, providing end-to-end solutions that address billing, coding, and patient collections. Strategic partnerships with healthcare providers and payers help strengthen market presence, while investments in cloud-based platforms enhance operational efficiency and scalability.

Many players also emphasize compliance with evolving regulations and data security, ensuring they meet industry standards. Furthermore, expanding into emerging markets with increasing healthcare digitization presents additional growth opportunities. Cerner Corporation is a key player in the healthcare revenue cycle management space, offering integrated solutions that improve financial and operational outcomes for healthcare organizations.

The company utilizes its expertise in electronic health records (EHR) and analytics to streamline billing, coding, and reimbursement processes. Cerner has a strong presence in the global market, with a focus on technology-driven improvements that enhance the efficiency and effectiveness of the revenue cycle.

Recent Developments

- In July 2024: Infinx announced the opening of its new state-of-the-art Research & Development Center in Bengaluru, India. This facility underscores Infinx’s commitment to fostering innovation and advancing healthcare revenue cycle management (RCM).

- In June 2022: Olive introduced its Autonomous Revenue Cycle Management suite, utilizing artificial intelligence to help healthcare organizations streamline administrative processes. The solution aims to accelerate payments and reduce uncompensated care risks while seamlessly integrating with existing practice management systems and electronic health records.

- In October 2022: eClinicalWorks, a cloud-based EHR provider, revealed that Advocare LLC, an independent physician group, reached US$ 1 billion in revenue by adopting eClinicalWorks’ RCM solution, demonstrating its effectiveness in optimizing revenue cycle processes.

Top Key Players in the Healthcare Revenue Cycle Management Market

- Olive

- NextGen Healthcare

- Infinx

- FinThrive

- Experian

- eClinicalWorks

- Dell Technologies

- Cognizant

- Adonis

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2023) | US$ 136.5 billion |

| Forecast Revenue (2033) | US$ 401.8 billion |

| CAGR (2024-2033) | 11.4% |

| Base Year for Estimation | 2023 |

| Historic Period | 2019-2022 |

| Forecast Period | 2024-2033 |

| Report Coverage | Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments |

| Segments Covered | By Product Type (Integrated and Standalone), By Function Type (Payment Remittance, Medical Coding & Billing, Eligibility Verification, Claims & Denial Management, and Others), By Deployment Type (Cloud-based and On-premise), By End-user (Hospitals, Physician Office, Diagnostic Labs and ASCs, and Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Olive , NextGen Healthcare, Infinx , FinThrive, Experian, eClinicalWorks, Dell Technologies, Cognizant, and Adonis. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |