Global Unsupervised Learning Market Size, Share, Growth Analysis By Technology (Natural Language Processing (NLP), Computer Vision, Speech Processing, Others), By Deployment Mode (On-premise, Cloud), By Enterprise Size (Large Enterprises, Small and Medium-sized Enterprises), By End-User Industry (BFSI, IT and Telecom, Retail and E-commerce, Healthcare, Government, Automotive and Transportation, Others), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2025-2035

- Published date: Feb 2026

- Report ID: 179007

- Number of Pages: 397

- Format:

-

keyboard_arrow_up

Quick Navigation

- Report Overview

- Effective Takeaways

- Industry Adoption

- By Technology

- By Deployment Mode

- By Enterprise Size

- By End-User Industry

- Key Market Segments

- Regional Analysis

- US Market Size

- Driving Factors

- Restraint factors

- Growth Opportunities

- Trending factors

- Competitive Analysis

- Future Predictions

- Recent Developments

- Report Scope

Report Overview

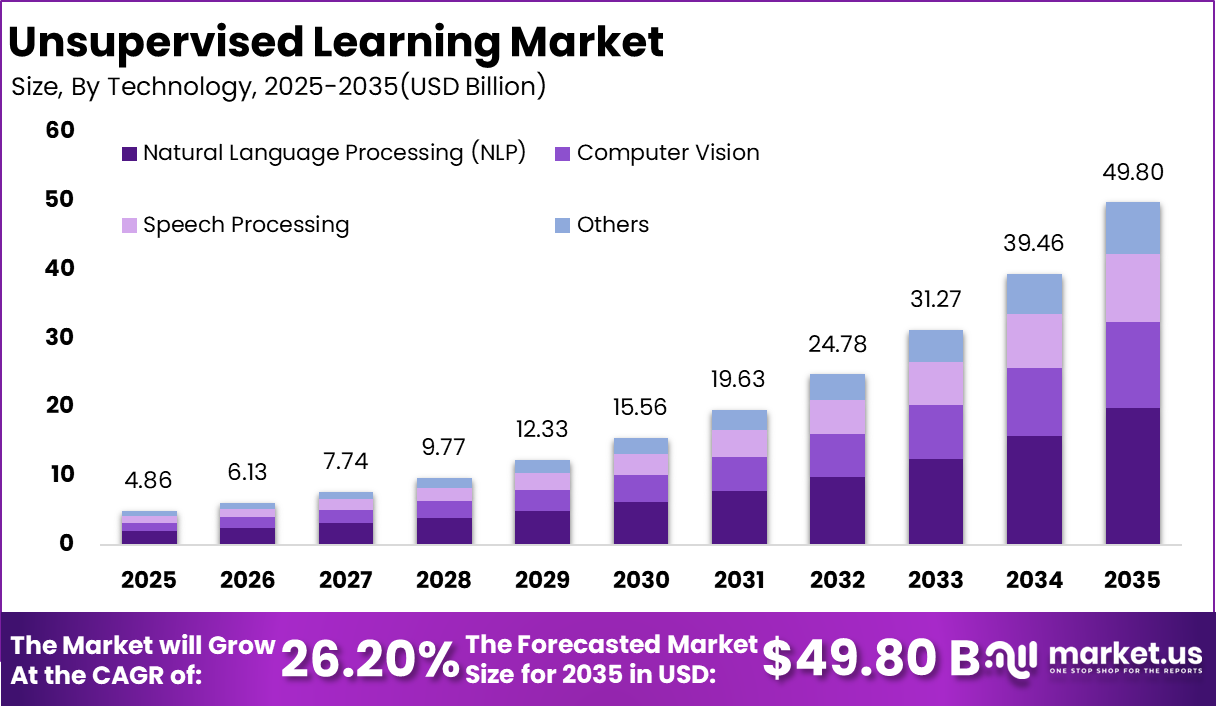

As someone seriously evaluating potential research investments, I find the outlook for the Unsupervised Learning Market compelling and strategically vital. In 2025, this market is forecast to be valued at USD 4.86 billion, and with a robust compound annual growth rate (CAGR) of 26.20%, it is projected to expand substantially to approximately USD 49.80 billion by 2035.

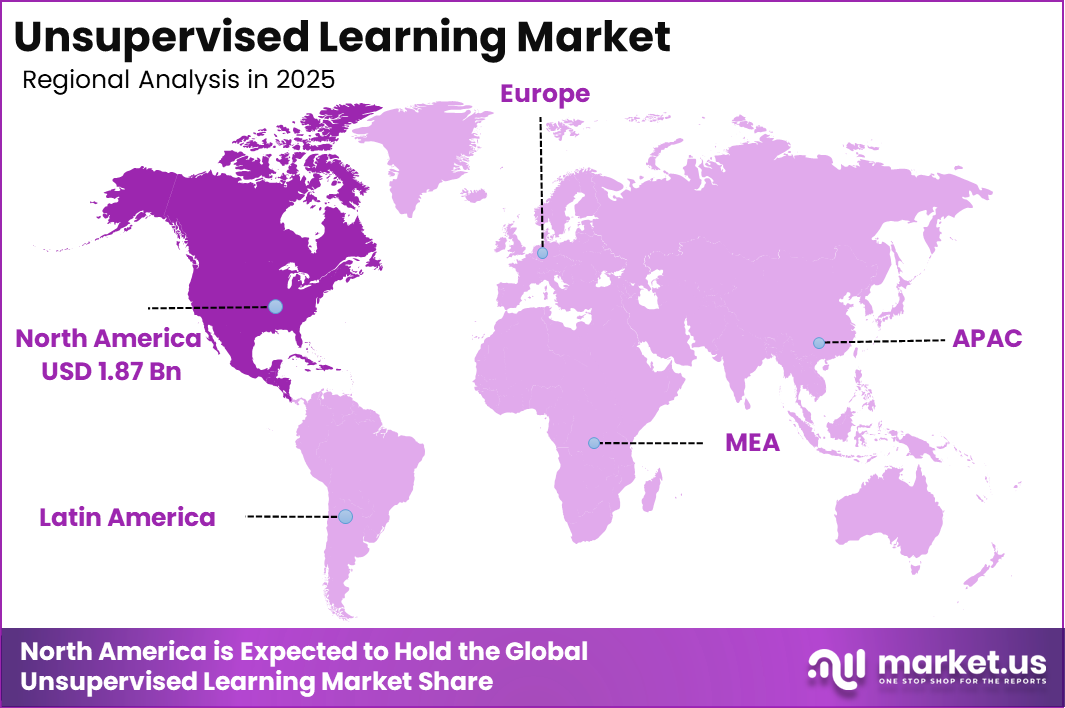

Such a growth trajectory highlights not only accelerating adoption across industries but also a significant shift toward advanced analytical methods that can extract insights from data without predefined labels. From a regional perspective, North America dominates with a 38.5% share of the market, amounting to USD 1.87 billion in 2025.

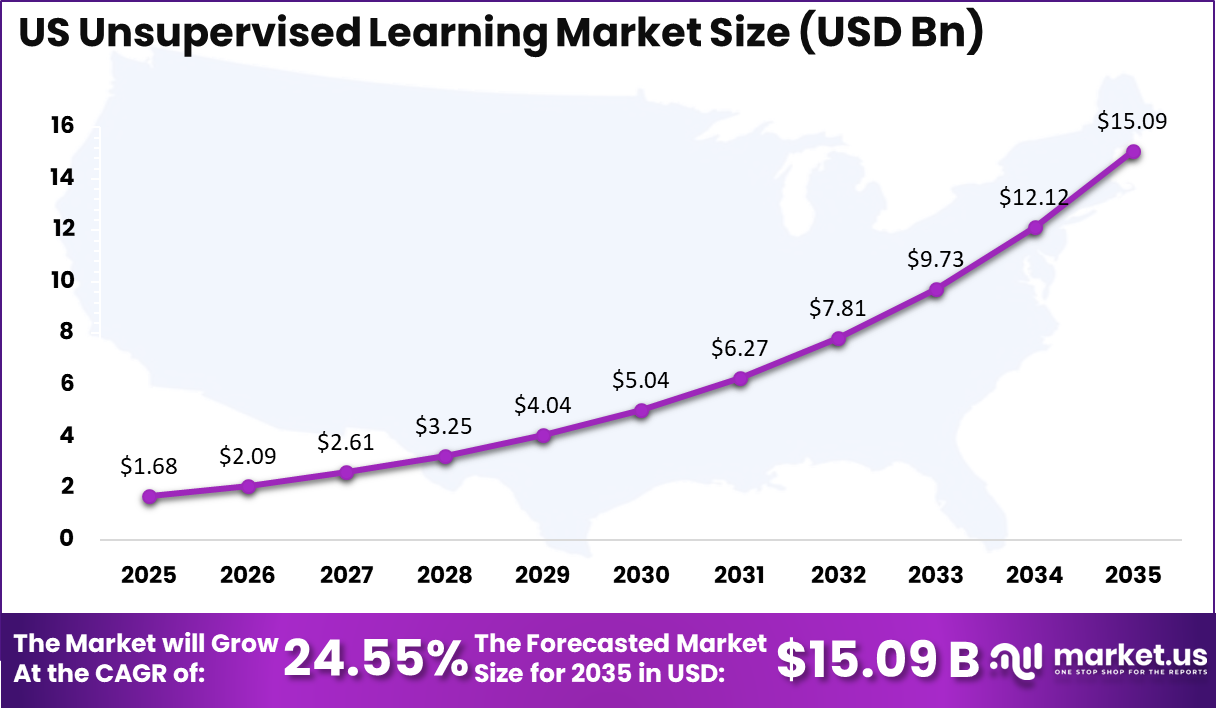

Within this region, the United States is particularly influential, representing USD 1.68 billion of the North American total. By 2035, the U.S. segment alone is projected to reach USD 15.09 billion, with a strong CAGR of 24.55% over the forecast period, underscoring enduring demand from enterprises seeking competitive advantage through intelligent data processing.

These figures signal substantial opportunity for stakeholders looking to understand market dynamics, competitive positioning, and investment potential in unsupervised learning technologies. The growth of the Unsupervised Learning Market reflects a broader industry trend where organizations increasingly prioritize data-driven decision-making and automation.

Businesses are leveraging unsupervised learning algorithms to uncover hidden patterns, detect anomalies, and optimize operations without relying on labeled datasets, making these solutions highly versatile across sectors such as finance, healthcare, retail, and manufacturing.

The accelerating adoption is further supported by advancements in computational power, cloud infrastructure, and AI frameworks, which make implementation more feasible and cost-effective for enterprises of all sizes.

For investors and decision-makers, understanding the regional nuances, particularly the dominance of North America and the United States, is crucial for identifying strategic opportunities, tailoring market entry approaches, and forecasting long-term returns in this high-growth segment. This market’s trajectory indicates not only technological evolution but also an expanding ecosystem of applications that can transform organizational intelligence and operational efficiency.

Effective Takeaways

- The Unsupervised Learning Market is expected to grow from USD 4.86 billion in 2025 to USD 49.80 billion by 2035 at a CAGR of 26.20%.

- North America holds the largest regional share at 38.5%, valued at USD 1.87 billion in 2025.

- The United States dominates within North America, reaching USD 15.09 billion by 2035 with a CAGR of 24.55%.

- Natural Language Processing (NLP) is the leading technology, accounting for 40.0% of the market.

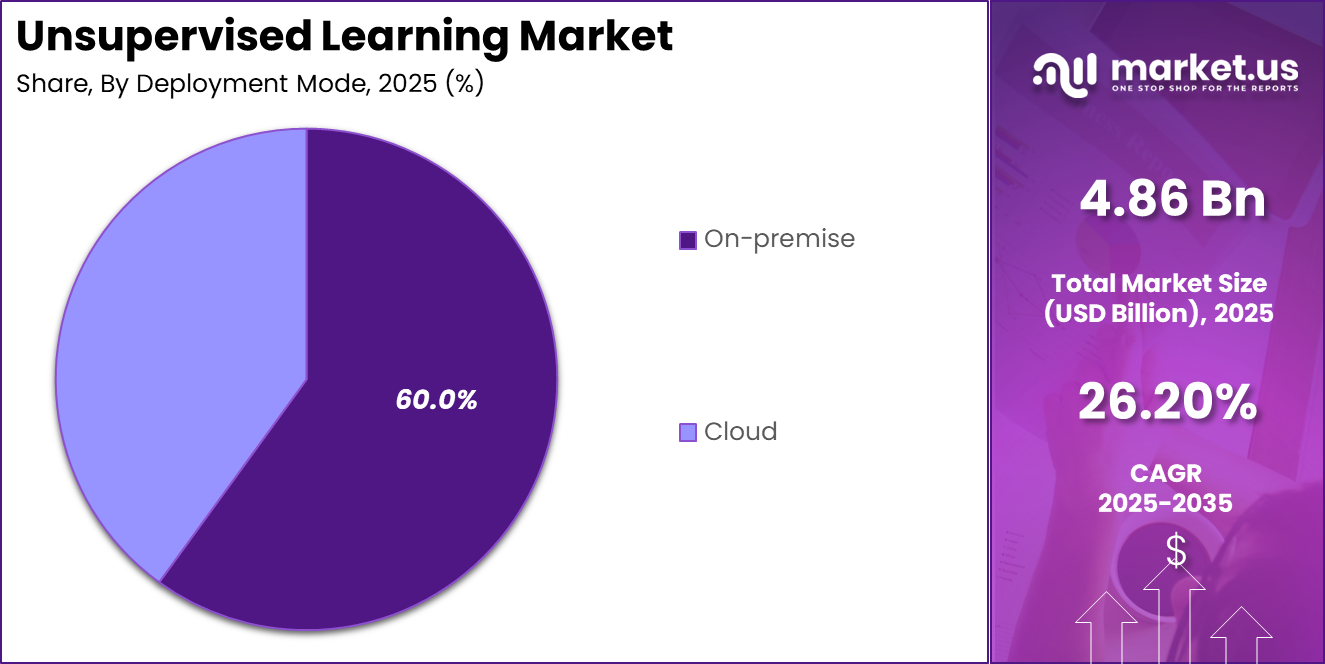

- On-premise deployment remains the preferred mode, representing 60.0% of implementations.

- Large enterprises are the primary adopters, comprising 66.7% of the market.

- BFSI is the top end-user industry, contributing 33.6% to the market.

Industry Adoption

Industry adoption of unsupervised learning is gaining strong traction as organizations across key sectors increasingly seek automated, data‑driven insights. In 2025, more than 58 % of global enterprises reported deploying unsupervised models for critical functions such as cybersecurity and fraud detection, underscoring widespread practical uptake beyond experimental use.

Over 71 % of Fortune 500 firms utilize unsupervised techniques for tasks including network monitoring, customer segmentation, and operational analytics, reflecting robust enterprise‑level commitment to the technology. North America’s leadership position is supported by substantial AI infrastructure, with the U.S. hosting a significant concentration of hyperscale data centers and enterprise deployments.

BFSI firms, in particular, are leveraging unsupervised learning to enhance fraud monitoring and risk profiling, building on broader AI adoption where machine learning models analyze over 1.2 billion transactions and cut error rates substantially. Healthcare providers are also adopting clustering and dimensionality‑reduction models for patient stratification and diagnostic workflows.

Meanwhile, sectors such as IT services and telecommunications apply unsupervised learning for large‑scale anomaly detection and network optimization, with notable adoption in predictive maintenance and quality control in manufacturing. This cross‑industry embrace of unsupervised learning demonstrates its role as a core component of enterprise analytics strategies, driven by the need to manage vast, unlabeled data and extract actionable insights at scale.

By Technology

Natural Language Processing (NLP) is the dominant technology in the Unsupervised Learning Market, capturing 40.0% of the market share in 2025. Organizations increasingly rely on NLP to analyze large volumes of unstructured text data, enabling automated insights, sentiment analysis, topic modeling, and information extraction.

Financial institutions use NLP-driven unsupervised models to detect fraudulent activities, monitor compliance, and understand customer feedback from emails, chat logs, and social media. Healthcare providers leverage NLP for clinical documentation analysis, patient record structuring, and identifying hidden patterns in medical literature, improving decision-making efficiency.

Computer Vision represents another key segment, applied in manufacturing, retail, and autonomous vehicles for defect detection, object recognition, and surveillance, with adoption accelerating due to improved image processing frameworks. Speech Processing supports voice assistants, call center automation, and real-time transcription services, where unsupervised learning identifies patterns in audio data without extensive labeled datasets.

The ‘Others’ category includes anomaly detection, clustering, and recommendation systems that provide cross-industry value in IT, telecommunications, and logistics. The growing availability of pre-trained language models, cloud-based NLP platforms, and robust computational infrastructure further drives adoption.

Enterprises are increasingly integrating NLP with other AI technologies, creating hybrid solutions that enhance accuracy and scalability, positioning NLP as a critical driver of the unsupervised learning ecosystem over the next decade.

By Deployment Mode

On-premise deployment leads the Unsupervised Learning Market with a 60.0% share in 2025, reflecting enterprises’ preference for greater control, security, and compliance over sensitive data. Organizations in highly regulated sectors such as BFSI, healthcare, and government favor on-premise solutions to ensure data privacy, meet stringent regulatory requirements, and maintain internal governance over AI models.

On-premise deployments also allow customization of infrastructure and algorithms to align with specific operational needs, enabling seamless integration with existing IT ecosystems. Cloud-based deployment, while secondary, is growing steadily as companies seek scalability, flexibility, and reduced upfront infrastructure costs.

Cloud solutions facilitate rapid experimentation, model training, and collaboration across geographically distributed teams, supporting initiatives such as predictive analytics, anomaly detection, and large-scale natural language processing. The choice between on-premise and cloud often depends on enterprise size, data sensitivity, and cost considerations.

Large enterprises continue to dominate on-premise adoption due to their extensive data handling requirements and compliance obligations, whereas small and medium-sized businesses increasingly adopt cloud deployments to leverage AI capabilities without heavy capital investment. Overall, deployment mode selection significantly shapes adoption strategies, operational efficiency, and long-term ROI in unsupervised learning implementations.

By Enterprise Size

Large enterprises dominate the Unsupervised Learning Market, holding 66.7% of the market share in 2025, driven by their extensive data resources, advanced IT infrastructure, and capacity to invest in sophisticated AI technologies. These organizations leverage unsupervised learning to optimize operations, enhance customer insights, detect anomalies, and support strategic decision-making across multiple departments.

Sectors such as BFSI, healthcare, and retail deploy these models at scale to manage complex data pipelines and extract actionable intelligence from vast unstructured datasets. Small and medium-sized enterprises (SMEs) are gradually adopting unsupervised learning, though their share remains limited due to budget constraints, limited in-house AI expertise, and smaller data volumes.

However, cloud-based solutions and pre-trained models are enabling SMEs to access scalable and cost-effective AI capabilities, helping them enhance operational efficiency and competitiveness. Large enterprises continue to lead adoption because they can justify higher investments in on-premise infrastructure, robust security frameworks, and specialized AI talent.

The market outlook indicates that while SMEs will increasingly integrate unsupervised learning for specific use cases, large enterprises will remain the primary drivers of market growth, shaping technological advancements, deployment practices, and industry-wide adoption trends.

By End-User Industry

BFSI is the leading end-user industry in the Unsupervised Learning Market, accounting for 33.6% of the market in 2025, driven by the sector’s critical need for fraud detection, risk assessment, customer segmentation, and compliance monitoring. Banks, insurance companies, and financial services firms deploy unsupervised learning models to analyze massive volumes of transaction data, identify anomalies, and uncover hidden patterns without relying on labeled datasets.

IT and telecom companies adopt these technologies to optimize network performance, enhance predictive maintenance, and improve cybersecurity measures, supporting service reliability and customer satisfaction. Retail and e-commerce businesses leverage unsupervised learning for personalized recommendations, inventory management, and demand forecasting, extracting insights from purchase histories and browsing behavior.

Healthcare providers utilize clustering and pattern recognition for patient stratification, medical imaging analysis, and operational efficiency. Government agencies apply unsupervised models for public safety, policy analysis, and anomaly detection in large administrative datasets. Automotive and transportation sectors explore applications in autonomous vehicles, predictive maintenance, and traffic optimization.

The ‘Others’ category includes logistics, energy, and manufacturing industries, which use unsupervised learning for operational optimization and anomaly detection. Overall, BFSI leads adoption due to high-value data assets, stringent risk requirements, and the critical need for timely, actionable insights.

Key Market Segments

By Technology

- Natural Language Processing (NLP)

- Computer Vision

- Speech Processing

- Others

By Deployment Mode

- On-premise

- Cloud

By Enterprise Size

- Large Enterprises

- Small and Medium-sized Enterprises

By End-User Industry

- BFSI

- IT and Telecom

- Retail and E-commerce

- Healthcare

- Government

- Automotive and Transportation

- Others

Regional Analysis

North America holds a dominant position in the Unsupervised Learning Market, accounting for 38.5% of the global share in 2025, with a market value of USD 1.87 billion. The region’s leadership is driven by the presence of advanced technological infrastructure, a mature AI ecosystem, and a concentration of large enterprises and startups investing heavily in artificial intelligence.

The United States plays a pivotal role, contributing the majority of the regional market, as organizations increasingly adopt unsupervised learning for applications such as fraud detection, customer behavior analysis, predictive maintenance, and operational optimization. Strong government support for AI initiatives, substantial venture capital funding, and the availability of skilled AI professionals further accelerate adoption.

Canada is also witnessing growth, particularly in healthcare and financial services, where unsupervised models are used to analyze complex datasets for insights and risk management. The BFSI, IT, healthcare, and retail sectors drive demand, leveraging unsupervised learning to enhance efficiency, reduce costs, and improve customer experiences.

With the increasing need for real-time analytics, scalable AI infrastructure, and data-driven decision-making, North America is projected to maintain its market dominance over the forecast period. The region’s robust regulatory frameworks and innovation-driven environment create a favorable landscape for continued investment and technological advancement in unsupervised learning.

US Market Size

The United States represents the largest and most influential segment of the Unsupervised Learning Market in North America, with a market size of USD 1.68 billion in 2025. The country’s adoption is driven by a combination of advanced technological infrastructure, extensive enterprise data resources, and a strong focus on artificial intelligence and machine learning integration across industries.

Financial services, healthcare, IT, and retail sectors are at the forefront of adoption, deploying unsupervised learning algorithms for fraud detection, customer segmentation, predictive analytics, and operational optimization. By 2035, the U.S. market is projected to reach USD 15.09 billion, growing at a CAGR of 24.55% over the forecast period, reflecting sustained investment and expanding applications.

Large enterprises dominate adoption due to their capacity to invest in robust IT infrastructure, skilled AI professionals, and on-premise deployment solutions, while SMEs increasingly leverage cloud-based platforms to implement cost-effective AI solutions. The strong growth trajectory is supported by continuous advancements in natural language processing, computer vision, and speech recognition, which enhance the effectiveness and scalability of unsupervised models.

Government initiatives promoting AI research, combined with active venture capital funding and innovation hubs, further accelerate market expansion. Overall, the United States remains a critical driver of global unsupervised learning growth, offering significant opportunities for technology providers and enterprise adopters.

Regional Analysis and Coverage

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherlands

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Thailand

- Vietnam

- Rest of Latin America

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Driving Factors

Industry adoption of unsupervised learning is being driven by several quantifiable, market‑validated factors that are making these technologies indispensable for modern enterprises. A key driver is the explosion of unstructured data – organizations now generate vast amounts of text, transactional, and sensor data that cannot be efficiently labeled manually.

Unsupervised models such as clustering and dimensionality reduction offer scalable pattern discovery without labeled inputs, enabling insights that traditional methods cannot deliver. In fact, over 58 % of global enterprises are already using unsupervised models for applications such as cybersecurity and fraud detection, demonstrating real‑world deployment beyond experimentation.

Advancements in AI infrastructure are another major force. Increasing computational power, cloud‑based platforms, and AI hardware have reduced barriers to implementation, allowing even mid‑sized enterprises to adopt sophisticated unsupervised techniques.

Across industries, over 61 % of large enterprises deploy unsupervised models for high‑value functions like customer segmentation and network monitoring, illustrating enterprise‑level commitment. Operational efficiency gains also fuel adoption. Organizations report up to 42 % improvements in efficiency and significant reductions in manual data labeling costs by leveraging unsupervised methods, strengthening business cases for investment.

Restraint factors

Despite strong growth momentum, the Unsupervised Learning Market faces several restraining factors that could slow broader adoption and impact deployment outcomes. One of the most significant challenges is model interpretability and transparency: unsupervised algorithms often generate patterns or clusters that lack clear explanation or context, making it difficult for decision‑makers to trust and act on results, especially in regulated industries such as finance and healthcare, where explainability is critical.

Another restraint stems from data quality and evaluation complexity. Unsupervised learning operates without labeled outputs, which means organizations cannot easily measure performance against ground truth or standardized accuracy metrics. This lack of clear evaluation makes validating model outputs subjective and often reliant on domain expertise, increasing implementation risk.

High computational and resource requirements are also barriers; many unsupervised techniques require powerful hardware and extensive preprocessing to handle large, high‑dimensional datasets, driving up costs and limiting adoption by smaller organizations. Skill shortages further hinder growth, as implementing and tuning unsupervised models demands advanced data science expertise that many enterprises struggle to recruit and retain.

Growth Opportunities

The Unsupervised Learning Market presents significant growth opportunities driven by evolving technology trends, expanding use cases, and increasing enterprise demand for advanced analytics. One major opportunity lies in the explosive growth of unstructured data: global data creation is projected to reach hundreds of zettabytes in the coming years, creating a pressing need for solutions that can efficiently extract insights without labeled datasets.

This fuels demand across industries such as IT, healthcare, finance, and manufacturing, where pattern recognition, anomaly detection, customer segmentation, and predictive analytics are increasingly strategic. Integration with emerging technologies such as edge AI, federated learning, and hybrid AI models unlocks new avenues for deployment.

Edge‑based unsupervised learning enables real‑time analytics on IoT devices, reducing data transfer costs and supporting smart infrastructure applications in manufacturing and autonomous systems. Federated learning frameworks enhance privacy‑preserving model training across decentralized data sources, particularly relevant in regulated sectors like healthcare and banking.

platforms and AutoML solutions also lower barriers to entry, enabling small and medium‑sized enterprises to adopt unsupervised learning without heavy upfront infrastructure or specialized talent, broadening the addressable market. Rapid innovation in self‑supervised transformers, contrastive learning, and multimodal models further expands capabilities, allowing organizations to tackle complex, cross‑domain problems and drive improved operational decision‑making.

Trending factors

- Growing use of self‑supervised and foundation models that can learn from massive unlabeled datasets is accelerating deployment in multimodal tasks such as text, image, and audio analysis, improving model utility across applications.

- The expansion of cloud and edge computing platforms is enabling more scalable and real‑time unsupervised learning workloads, reducing latency and enabling analytics closer to where data is generated.

- Federated and privacy‑preserving learning approaches are gaining traction, allowing organizations in regulated industries like healthcare and finance to train unsupervised models on sensitive data without moving or exposing raw information.

- AutoML and democratized ML tools are lowering technical barriers, allowing non‑expert users and SMEs to deploy unsupervised learning with minimal coding or specialized expertise.

- There’s a noticeable trend toward hybrid learning approaches that combine unsupervised with supervised techniques to boost accuracy and reduce dependence on labeled datasets.

- Increasing emphasis on explainability and interpretability helps organizations trust unsupervised outcomes and meet regulatory requirements, especially in BFSI and healthcare.

- Sustainable AI initiatives and efficient algorithm design are becoming important, as organizations aim to lower energy use and resource costs in model training and deployment.

Competitive Analysis

The competitive landscape of the Unsupervised Learning Market is shaped by a mix of global technology leaders and specialized AI innovators, with the top 5 companies controlling an estimated 48–52% of overall market influence as of 2025.

Major industry players such as IBM, Microsoft, Google, Amazon Web Services (AWS), SAP, Oracle, H2O.ai, DataRobot, NVIDIA, Intel, Salesforce, SAS Institute, and Databricks dominate the development and deployment of unsupervised learning tools and enterprise platforms. These firms leverage deep pockets in R&D, extensive AI ecosystems, and broad customer bases to secure leadership positions.

IBM’s Watson platform provides sophisticated unsupervised analytics capabilities that are widely used for clustering, dimensionality reduction, and anomaly detection across sectors such as finance and healthcare, reinforcing its competitive edge.

Microsoft and Google continue to expand unsupervised learning services through Azure AI and Google Cloud, respectively, often integrating AutoML and foundation models to simplify deployment. AWS competes strongly with scalable cloud‑native solutions supporting diverse unsupervised workloads.

Specialized vendors like DataRobot and H2O.ai focus on automated machine learning frameworks, helping enterprises accelerate model building with minimal coding overhead, while NVIDIA’s hardware innovations optimize large model training. Strategic partnerships, product enhancements, and cloud integrations are common tactics among these competitors to deepen market penetration and enhance analytics performance.

Top Key Players in the Market

- Microsoft Corporation

- IBM Corporation

- Amazon.com, Inc.

- Google LLC

- SAP SE

- Oracle Corporation

- H2O.ai

- RapidMiner

- TIBCO Software Inc.

- Databricks

- Cloud Software Group, Inc.

- Fair Isaac Corporation

- Salesforce, Inc.

- SAS Institute Inc.

- Hewlett-Packard Enterprise Company

- Others

Future Predictions

Looking forward, emerging technologies, including self‑supervised learning, hybrid AI models, and foundation model integration, are expected to enhance model accuracy and expand capabilities across multimodal datasets. Cloud-native deployments and edge AI solutions will support real-time analytics in IoT, autonomous systems, and smart infrastructure applications.

Federated learning and privacy-preserving frameworks will unlock adoption in regulated sectors like healthcare and financial services, where centralized data storage is restricted. Increasing emphasis on explainable AI and more efficient algorithm design will reduce barriers related to interpretability and operational cost. Collectively, these trends indicate that unsupervised learning will become an integral part of enterprise analytics and automation strategies, driving innovation and competitive advantage over the next decade.

The increasing availability of cloud platforms, AutoML solutions, and scalable computational infrastructure is enabling small and medium-sized enterprises to implement these models without extensive in-house expertise. Combined with the accelerating development of hybrid AI models and real-time analytics solutions, these factors are expected to make unsupervised learning a core component of enterprise AI strategies, driving long-term value creation, operational efficiency, and competitive differentiation across industries worldwide.

Recent Developments

- In June 2025, H2O.ai was named a Visionary in the 2025 Gartner Magic Quadrant for Data Science & Machine Learning Platforms for the third consecutive year, highlighting continued innovation in secure enterprise‑grade AI and automated machine learning, with its h2oGPTe agentic AI platform achieving a top global benchmark score of 75%.

- In March 2025, IBM announced an expanded collaboration with NVIDIA, planning integrations of NVIDIA AI Data Platform technologies across IBM’s hybrid cloud and watsonx offerings to enhance unstructured data processing and support large‑scale AI workloads, including retrieval‑augmented generation and advanced unsupervised reasoning.

- In late 2025, H2O.ai released major enhancements to its Driverless AI platform, adding features such as model checkpointing, improved large‑workload support, and expanded unsupervised algorithms (K‑Means, PCA, SVD) for feature engineering, enabling faster retraining, lower memory footprint, and broader use cases in fraud detection and cyber‑threat prevention.

Report Scope

Report Features Description Market Value (2025) USD 4.86 Billion Forecast Revenue (2035) USD 49.80 Billion CAGR(2025-2035) 26.20% Base Year for Estimation 2024 Historic Period 2020-2024 Forecast Period 2025-2035 Report Coverage Revenue forecast, AI impact on Market trends, Share Insights, Company ranking, competitive landscape, Recent Developments, Market Dynamics, and Emerging Trends Segments Covered By Technology (Natural Language Processing (NLP), Computer Vision, Speech Processing, Others), By Deployment Mode (On-premise, Cloud), By Enterprise Size (Large Enterprises, Small and Medium-sized Enterprises), By End-User Industry (BFSI, IT and Telecom, Retail and E-commerce, Healthcare, Government, Automotive and Transportation, Others) Regional Analysis North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Latin America; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA Competitive Landscape Microsoft Corporation, International Business Machines Corporation, Amazon.com, Inc., Google LLC, SAP SE, Oracle Corporation, H2O.ai, RapidMiner, TIBCO Software Inc., Databricks, Cloud Software Group, Inc., Fair Isaac Corporation, Salesforce, Inc., SAS Institute Inc., Hewlett Packard Enterprise Company, Others Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF)  Unsupervised Learning MarketPublished date: Feb 2026add_shopping_cartBuy Now get_appDownload Sample

Unsupervised Learning MarketPublished date: Feb 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- Microsoft Corporation

- International Business Machines Corporation

- Amazon.com, Inc.

- Google LLC

- SAP SE

- Oracle Corporation

- H2O.ai

- RapidMiner

- TIBCO Software Inc.

- Databricks

- Cloud Software Group, Inc.

- Fair Isaac Corporation

- Salesforce, Inc.

- SAS Institute Inc.

- Hewlett-Packard Enterprise Company

- Others

Our Clients

- 179007

- Feb 2026