U.S. Drug Utilization Management Market By Type (Prospective Review (pDUR), Concurrent Review (cDUR) and Retrospective Review (rDUR)), By Program Type (In-house and Outsourced), By End-use (PBMs, Health Plan Provider/Payors and Pharmacies), Region and Companies – Industry Segment Outlook, Market Assessment, Competition Scenario, Trends and Forecast 2026-2035

- Published date: March 2026

- Report ID: 180187

- Number of Pages: 275

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

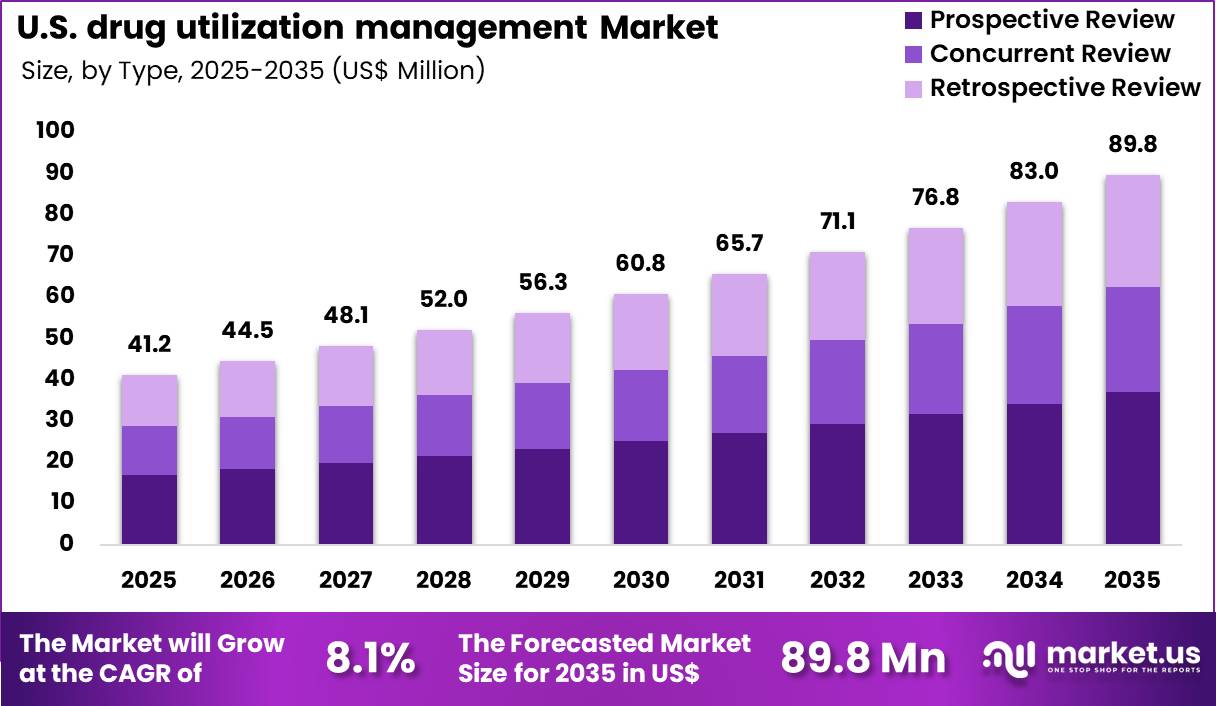

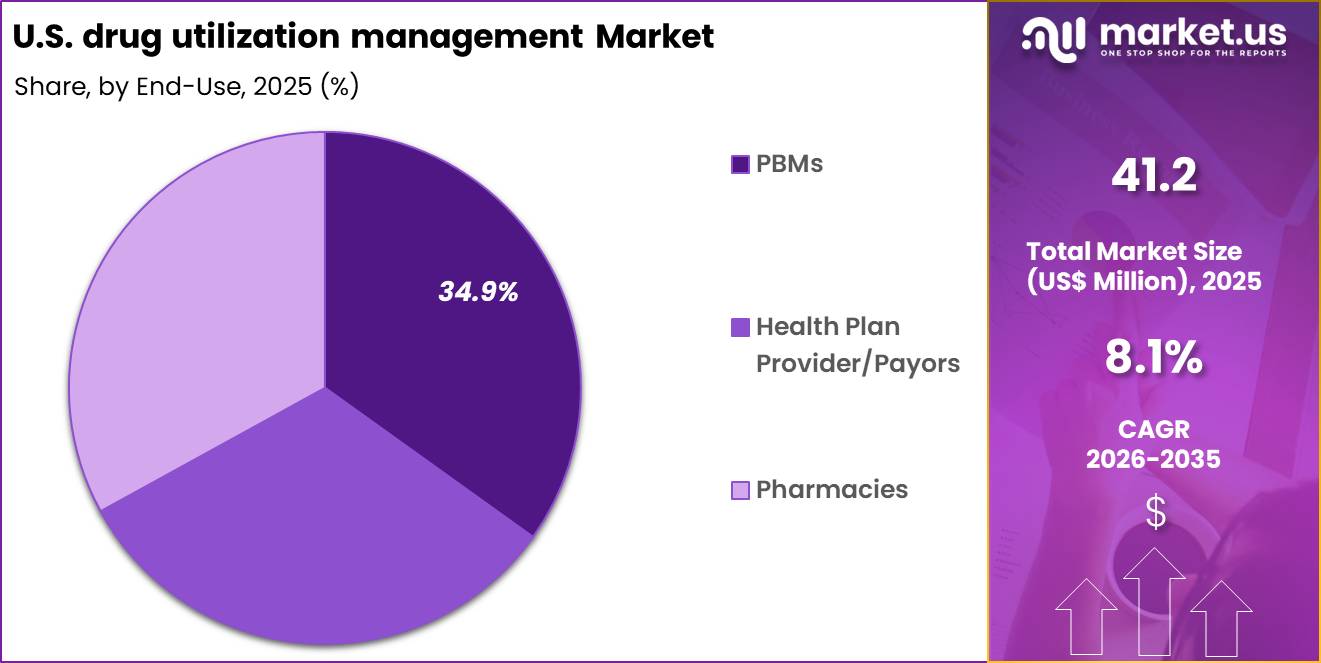

The U.S. Drug Utilization Management Market size is expected to be worth around US$ 89.8 Million by 2035 from US$ 41.2 Million in 2025, growing at a CAGR of 8.1% during the forecast period 2026-2035.

Rising healthcare expenditures and the need to ensure clinically appropriate medication use accelerate the U.S. drug utilization management market as payers implement strategies that balance cost control with optimal therapeutic outcomes.

Pharmacy benefit managers increasingly apply prior authorization protocols for high-cost specialty drugs in oncology and rare diseases, verifying medical necessity and documented response before granting coverage to prevent inappropriate utilization. These programs support step therapy requirements for chronic conditions such as rheumatoid arthritis and multiple sclerosis, directing patients to lower-cost alternatives before approving advanced biologics.

Quantity limits and dose optimization tools help manage controlled substances in pain management and ADHD treatment, reducing misuse while preserving access for patients with legitimate clinical needs. Retrospective drug utilization review processes identify suboptimal prescribing patterns in long-term care and specialty pharmacy, prompting targeted interventions to enhance adherence and safety.

Payers seize opportunities to embed artificial intelligence and real-time decision support into utilization management platforms, expanding applications in predictive modeling that flags potential adverse events or non-adherence in cardiovascular and respiratory therapies.

Developers advance automated prior authorization systems integrated with electronic health records, streamlining approvals and reducing administrative burden for physicians managing complex regimens. These advancements facilitate value-based utilization frameworks that link reimbursement to measurable clinical improvements in specialty pharmacy programs.

Opportunities emerge in pharmacogenomic-guided utilization strategies that tailor coverage decisions to individual genetic profiles. Recent trends emphasize transparent appeals processes, patient education resources, and collaborative models with providers, positioning the market for sustained growth in sustainable, evidence-driven medication management.

Key Takeaways

- In 2025, the market generated a revenue of US$ 41.2 Million, with a CAGR of 8.1%, and is expected to reach US$ 89.8 Million by the year 2035.

- The type segment is divided into prospective review, concurrent review and retrospective review, with prospective review taking the lead with a market share of 41.2%.

- Considering program type, the market is divided into in-house and outsourced. Among these, in-house held a significant share of 66.1%.

- Furthermore, concerning the end-use segment, the market is segregated into PBMs, health plan provider/payors and pharmacies. The PBMs sector stands out as the dominant player, holding the largest revenue share of 34.9% in the market.

Type Analysis

Prospective review accounted for 41.2% of growth within type and dominates the U.S. drug utilization management market due to its role in evaluating prescription appropriateness before dispensing. This process helps reduce medication errors, control costs, and ensure adherence to formulary guidelines.

Health plans and PBMs increasingly implement advanced analytics and clinical decision support to optimize patient therapy early in the treatment cycle. Segment growth is projected to strengthen as regulatory pressure for safe prescribing intensifies and as high-cost specialty drugs proliferate.

Prospective review enables real-time interventions that improve patient outcomes while limiting unnecessary expenditures. Automation of prior authorization and integration with electronic health records supports workflow efficiency. Rising emphasis on value-based care encourages proactive medication management, reinforcing adoption among managed care organizations.

Expansion of telehealth and digital pharmacy services further drives reliance on prospective review systems. Continuous updates to clinical guidelines ensure relevance and enhance clinician confidence, contributing to segment growth.

Program Type Analysis

In-house programs accounted for 66.1% of growth within program type and dominate due to their ability to offer direct control over utilization management processes. Health plans and PBMs implement in-house teams to customize review criteria, optimize cost containment strategies, and maintain compliance with federal and state regulations.

Segment growth is anticipated to continue as organizations prioritize internal expertise for high-value specialty drugs and complex treatment regimens. Integration with internal pharmacy benefit management systems improves efficiency and reporting accuracy. In-house programs facilitate tailored interventions for high-risk patient populations and enable rapid response to emerging clinical evidence.

Rising investment in data analytics and artificial intelligence enhances predictive review capabilities. Organizations increasingly leverage in-house programs to maintain operational flexibility and ensure quality oversight.

Strategic collaborations with clinical pharmacists strengthen decision-making and improve outcomes. Adoption is likely to expand as healthcare payors focus on optimizing patient safety and cost-effectiveness simultaneously.

End-Use Analysis

PBMs accounted for 34.9% of growth within end-use and dominate due to their central role in managing prescription benefits and controlling pharmaceutical spending. PBMs implement drug utilization management strategies across large patient populations to promote appropriate prescribing and reduce waste. Segment growth is projected to continue as demand for specialty medication management increases and formulary adherence becomes critical.

Advanced analytics platforms support real-time prior authorization and utilization review. PBMs provide education and intervention programs to prescribers, improving clinical outcomes and limiting avoidable costs. Rising partnerships between PBMs and health plans enhance market penetration.

Automation of administrative processes improves efficiency and scalability. Growth is likely to be reinforced by increasing emphasis on value-based contracts and patient-centric care models. Regulatory guidance on safe prescribing practices further supports PBM-led utilization management programs.

Key Market Segments

By Type

- Prospective Review (pDUR)

- Concurrent Review (cDUR)

- Retrospective Review (rDUR)

By Program Type

- In-house

- Outsourced

By End-use

- PBMs

- Health Plan Provider/Payors

- Pharmacies

Drivers

Rising specialty drug spending is driving the market.

The rapid growth in expenditures on high-cost specialty medications has significantly intensified the need for utilization management strategies to control costs while ensuring appropriate access. Payers are implementing more rigorous prior authorization and step therapy requirements to manage the financial impact of these therapies.

Pharmacy benefit managers are expanding specialty pharmacy networks to optimize dispensing and monitoring. The correlation between specialty drug approvals and budget pressures further accelerates adoption of utilization tools. Government reports highlight the increasing share of specialty drugs in total drug spending.

Utilization management programs enable payers to align coverage with clinical evidence and value. National health data document the escalating burden of specialty medications on healthcare budgets. Key payers are enhancing digital platforms to streamline prior authorization processes. This driver fosters innovation in real-time decision support and formulary design. Specialty drugs accounted for 51% of total drug spending in 2023 according to CMS National Health Expenditure data.

Restraints

Administrative burden of prior authorization is restraining the market.

The extensive paperwork and processing delays associated with prior authorization requirements have created significant operational challenges for providers and payers. Physicians report substantial time spent on appeals and documentation, diverting resources from patient care. Payers face increased administrative costs to review and adjudicate complex requests.

The correlation between authorization volume and staff workload further constrains efficiency. Government agencies have documented provider frustration with utilization management processes. Utilization management programs often lead to treatment delays that affect patient outcomes.

National surveys highlight the burden on both clinical and administrative staff. Key stakeholders are advocating for reform to reduce unnecessary administrative requirements. This restraint limits the scalability of more sophisticated management tools. The administrative burden of prior authorization remains a primary market restraint.

Opportunities

Expansion of value-based contracting models is creating growth opportunities.

The shift toward value-based agreements between payers and manufacturers presents avenues for more sophisticated utilization management approaches tied to clinical outcomes. Governmental policies supporting outcome-based reimbursement encourage the development of performance-linked coverage criteria.

Increasing focus on total cost of care amplifies potential for integrated management solutions. Partnerships between payers and pharmaceutical companies facilitate data-sharing agreements for real-world evidence. The large volume of specialty medications in value-based arrangements magnifies opportunities for advanced utilization tools.

Educational initiatives for payers promote standardized outcome measurement in contracting. This opportunity enables the creation of dynamic authorization criteria based on performance metrics. Leading organizations are investing in analytics platforms optimized for value-based models.

Overall, value-based expansion aligns with efforts to align incentives across the healthcare ecosystem. The number of value-based contracts for specialty drugs increased notably between 2022 and 2024 according to industry reports.

Impact of Macroeconomic / Geopolitical Factors

Macroeconomic conditions affect the U.S. drug utilization management market by influencing healthcare spending, insurance plan budgets, and pharmacy operations. Rising inflation and higher interest rates increase operational costs for payers and pharmacy benefit managers, which can slow the adoption of advanced management tools.

Geopolitical tensions disrupt global supply chains for specialty drugs and biosimilars, creating pricing volatility and administrative challenges. Current US tariffs on imported IT infrastructure and cloud hardware raise costs for system upgrades and analytics platforms.

Smaller pharmacy networks face tighter margins and slower technology integration under these pressures. On the positive side, increasing demand for cost containment and evidence-based prescribing drives investments in automated utilization management solutions.

Policy initiatives supporting value-based care further expand the market’s relevance and adoption. With strategic technology deployment and partnerships, the market continues to show sustainable growth and operational efficiency improvements.

Latest Trends

Implementation of real-time benefit tools is a recent trend in the market.

In 2024, payers and electronic health record vendors have accelerated deployment of real-time benefit tools that provide immediate coverage and cost information at the point of prescribing. These systems integrate with pharmacy benefit manager data to display patient-specific formulary status and out-of-pocket costs.

Manufacturers have focused on seamless connectivity to reduce prescribing friction. Clinical evaluations in 2024 demonstrated reduced prior authorization volumes with real-time tools. The implementation of real-time benefit tools is a major trend in utilization management. This development addresses longstanding challenges in medication access at the point of care.

The trend emphasizes integration with electronic prescribing workflows for immediate feedback. Regulatory guidance in 2024 supported adoption of these tools in clinical systems. Industry collaborations refine data accuracy and timeliness for prescribers. These innovations aim to improve medication adherence while optimizing utilization management efficiency.

Key Players Analysis

Market leaders in the U.S. drug utilization management sector drive expansion by enhancing analytics capabilities, reinforcing payer–provider integrations, and developing predictive models to curb inappropriate prescribing. They secure long-term contracts with health plans and pharmacy benefit managers while refining prior authorization workflows to improve cost control and patient outcomes.

CVS Health’s pharmacy benefit services unit oversees utilization protocols, leverages real-world evidence, and serves a broad base of commercial, government, and employer clients across the country. The organization prioritizes investments in automation and clinical decision support to streamline approvals and reduce administrative burden.

Other competitors adopt specialty drug monitoring tools and collaborative care networks to strengthen formulary adherence and utilization efficiency. These concerted actions help firms deepen market penetration, optimize therapy value, and sustain revenue growth.

Top Key Players

- Prime Therapeutics LLC

- MedicusRx

- EmblemHealth

- Optum, Inc.

- Point32Health, Inc.

- AssureCare LLC

- MindRx Group

- Agadia Systems, Inc

- Elevance Health (CarelonRx)

- ExlService Holdings, Inc.

- MRIoA

- S&C Technologies, Inc.

- In-House Providers

- Ultimate Health Plans

Recent Developments

- In October 2025, the Centers for Medicare & Medicaid Services (CMS) released formal guidance confirming the annual data submission requirements for Medicare Advantage utilization management through the Health Plan Management system. The agency also indicated that evaluations of internal coverage criteria could be incorporated into future program audit processes.

- In May 2025, Quantum Health expanded its Premier Pharmacy platform to include Vida Health’s GLP-1–based weight management solution for self-insured employers. The enhancement is designed to monitor utilization management trends, improve prescribing efficiency, and support better clinical and member engagement outcomes related to weight loss therapies.

Report Scope

Report Features Description Market Value (2025) US$ 41.2 Million Forecast Revenue (2035) US$ 89.8 Million CAGR (2026-2035) 8.1% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments Segments Covered By Type (Prospective Review (pDUR), Concurrent Review (cDUR) and Retrospective Review (rDUR)), By Program Type (In-house and Outsourced), By End-use (PBMs, Health Plan Provider/Payors and Pharmacies) Competitive Landscape Prime Therapeutics LLC, MedicusRx, EmblemHealth, Optum, Inc., Point32Health, Inc., AssureCare LLC, MindRx Group, Agadia Systems, Inc, Elevance Health (CarelonRx), ExlService Holdings, Inc., MRIoA, S&C Technologies, Inc., In-House Providers, Ultimate Health Plans. Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)  U.S. Drug Utilization Management MarketPublished date: March 2026add_shopping_cartBuy Now get_appDownload Sample

U.S. Drug Utilization Management MarketPublished date: March 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- Prime Therapeutics LLC

- MedicusRx

- EmblemHealth

- Optum, Inc.

- Point32Health, Inc.

- AssureCare LLC

- MindRx Group

- Agadia Systems, Inc

- Elevance Health (CarelonRx)

- ExlService Holdings, Inc.

- MRIoA

- S&C Technologies, Inc.

- In-House Providers

- Ultimate Health Plans

Our Clients

- 180187

- March 2026