Quick Navigation

Report Overview

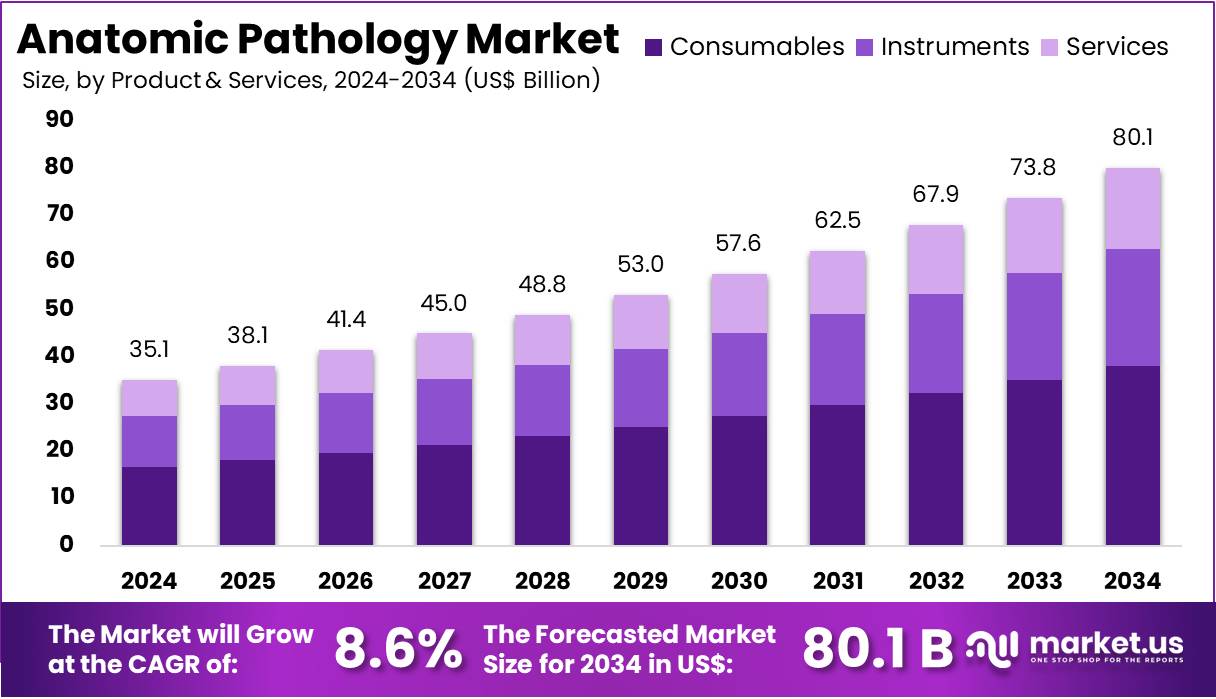

The Anatomic Pathology Market size is expected to be worth around US$ 80.1 billion by 2034 from US$ 35.1 billion in 2024, growing at a CAGR of 8.6% during the forecast period 2025 to 2034. North America held a dominant market position, capturing more than a 40.3% share and holds US$ 14.1 Billion market value for the year.

Growing demand for precise and early disease diagnosis is driving expansion in the anatomic pathology market. The increasing prevalence of cancer, infectious diseases, and chronic conditions is fueling the need for advanced pathology solutions to improve diagnostic accuracy and treatment planning. In April 2021, Leica Biosystems teamed up with AI-driven medical technology firm Paige to develop next-generation computational pathology solutions. This collaboration sought to integrate artificial intelligence into Leica’s digital pathology portfolio, accelerating advancements in automated image analysis and diagnostic precision.

Rising adoption of digital pathology platforms is streamlining workflow efficiency and enabling remote consultations among pathologists. The growing role of artificial intelligence in anatomic pathology is enhancing tissue sample analysis, reducing diagnostic errors, and facilitating personalized treatment strategies. Increasing healthcare investments in biomarker research and molecular pathology are driving innovations in precision medicine. The expanding use of anatomic pathology in drug development and clinical trials is strengthening its market potential.

Rising demand for automated immunohistochemistry (IHC) and in situ hybridization (ISH) techniques is improving cancer detection and prognosis accuracy. The growing shift toward minimally invasive biopsies is encouraging advancements in tissue processing and slide preparation technologies. Increasing regulatory approvals for AI-powered pathology tools are fostering innovation and market growth. The rising emphasis on data integration and interoperability is enhancing collaboration between pathology labs and healthcare institutions.

Expanding applications of anatomic pathology in neurology, dermatology, and hematology are broadening its clinical scope. The growing need for real-time diagnostic insights is accelerating the development of cloud-based and AI-assisted pathology solutions. As technology continues to advance and healthcare providers prioritize early disease detection, the anatomic pathology market is expected to experience sustained growth in the coming years.

Key Takeaways

- In 2023, the market for Anatomic Pathology generated a revenue of US$ 35.1 billion, with a CAGR of 8.6%, and is expected to reach US$ 80.1 billion by the year 2033.

- The product & services segment is divided into instruments, consumables, and services, with consumables taking the lead in 2023 with a market share of 47.6%.

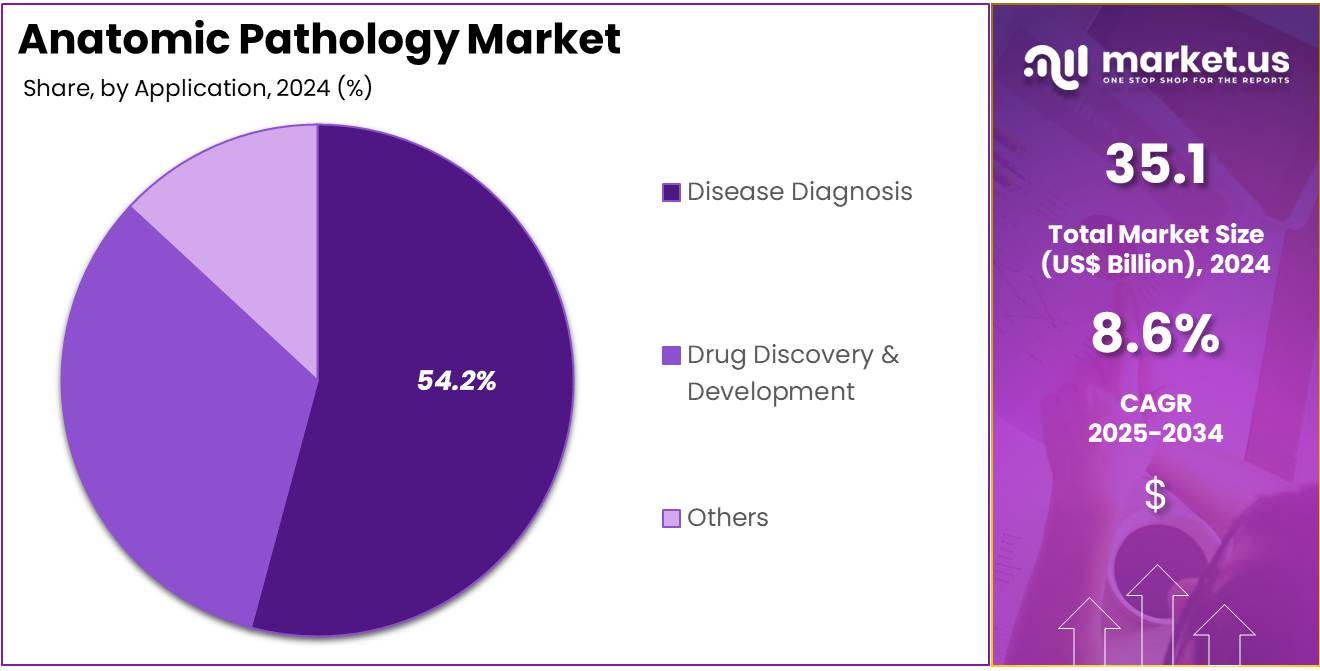

- Considering application, the market is divided into disease diagnosis, drug discovery & development, and others. Among these, disease diagnosis held a significant share of 54.2%.

- Furthermore, concerning the end-user segment, the market is segregated into hospitals, research laboratories, diagnostic laboratories, and others. The hospitals sector stands out as the dominant player, holding the largest revenue share of 49.8% in the Anatomic Pathology market.

- North America led the market by securing a market share of 40.3% in 2023.

Product & Services Analysis

The consumables segment led in 2023, claiming a market share of 47.6% owing to the increasing demand for diagnostic tools and reagents that support accurate and timely diagnoses. The growing number of chronic diseases, including cancer, cardiovascular diseases, and neurological disorders, is expected to drive the demand for consumables such as biopsy reagents, staining chemicals, and laboratory consumables.

These products are integral to pathologists’ ability to perform tests and analyses essential for diagnosing and monitoring diseases. The expansion of healthcare infrastructure, particularly in developing regions, will further contribute to the increased usage of consumables in diagnostic laboratories and medical facilities, driving growth in this segment.

Application Analysis

The disease diagnosis held a significant share of 54.2% as healthcare providers focus on early detection and accurate identification of diseases. Advances in diagnostic technologies, particularly in molecular and genetic diagnostics, will significantly enhance the ability to diagnose complex conditions such as cancer, autoimmune disorders, and infectious diseases.

The growing preference for personalized medicine, which relies on accurate disease diagnostics, will further boost the market for anatomic pathology services. Additionally, the increasing adoption of digital pathology tools, such as whole-slide imaging, is expected to improve diagnostic precision, leading to further growth in this segment.

End-User Analysis

The hospitals segment had a tremendous growth rate, with a revenue share of 49.8% owing to the increasing demand for diagnostic and pathological services in hospitals. The rise in hospital admissions for both chronic and acute diseases, along with the expansion of hospital infrastructure, will contribute to the demand for pathology services.

Hospitals, especially those with specialized departments such as oncology and neurology, rely heavily on anatomic pathology for disease diagnosis and treatment planning. Furthermore, the trend toward offering comprehensive diagnostic services within hospitals will drive growth, as hospitals seek to enhance their diagnostic capabilities and improve patient outcomes by investing in advanced pathology services and technologies.

Key Market Segments

By Product & Services

- Instruments

- Microtomes & Cryostat

- Tissue Processors

- Automatic Stainers

- Whole Slide Imaging (WSI) Scanners

- Others

- Consumables

- Antibodies

- Primary Antibodies

- Secondary Antibodies

- Kits & Reagents

- Stains & Solvents

- Fixatives

- Others

- Probes

- Others

- Antibodies

- Services

By Application

- Disease Diagnosis

- Cancer

- Breast Cancer

- Gastrointestinal Cancer

- Lung Cancer

- Prostate Cancer

- Others

- Other Diseases

- Cancer

- Drug Discovery and Development

- Others

By End-user

- Hospitals

- Research Laboratories

- Diagnostic Laboratories

- Others

Drivers

Increasing Prevalence of Chronic Diseases Driving the Anatomic Pathology Market

Rising cases of chronic illnesses are expected to drive demand for anatomic pathology as healthcare providers prioritize early disease detection and personalized treatment approaches. In 2021, the World Health Organization (WHO) reported that noncommunicable diseases (NCDs), such as cardiovascular diseases, cancers, chronic respiratory diseases, and diabetes, were responsible for 71% of all deaths globally. This high prevalence underscores the growing demand for anatomic pathology services to diagnose and manage these conditions.

As cancer cases continue to rise, pathologists play a crucial role in identifying tumor types and molecular markers, guiding targeted therapies. The increasing need for biopsy-based diagnostics contributes to market expansion, particularly in oncology, neurology, and gastroenterology. Healthcare advancements emphasize precision medicine, further integrating pathology into multidisciplinary treatment plans. Population aging also fuels demand, with elderly individuals more susceptible to chronic illnesses requiring histopathological evaluation.

Expanding healthcare infrastructure in emerging economies facilitates greater access to pathology services. Technological innovations, including automated staining and digital imaging, enhance efficiency and accuracy in pathology laboratories. Government initiatives promoting cancer screening programs contribute to the rising adoption of pathology-based diagnostic techniques.

The growing preference for minimally invasive diagnostic methods supports biopsy-based pathology, reducing patient discomfort. Investments in pathology education and training strengthen workforce capacity, addressing the growing demand for skilled professionals. Research collaborations between academic institutions and diagnostic companies continue to advance pathology techniques, improving disease characterization and prognosis.

Restraints

High Cost of Advanced Equipment as a Restraint in the Anatomic Pathology Market

Rising costs of sophisticated pathology instruments are expected to limit market expansion by creating financial challenges for smaller laboratories and healthcare facilities. High-end equipment, including digital pathology scanners, automated slide processors, and immunohistochemistry analyzers, require substantial capital investment.

Many pathology labs, especially in low- and middle-income countries, struggle to afford these advanced technologies, restricting their adoption. Maintenance and calibration costs add financial burdens, further increasing operational expenses. Upgrading pathology systems often necessitates additional staff training, raising personnel costs.

Limited reimbursement policies for pathology services in some regions discourage healthcare providers from investing in costly diagnostic infrastructure. The need for specialized storage and IT systems to handle digital pathology data further escalates expenses. While technological advancements improve diagnostic capabilities, cost constraints remain a significant barrier to widespread adoption, particularly in resource-limited settings.

Opportunities

Growth of Digital Pathology and AI Integration as an Opportunity in the Anatomic Pathology Market

Rising adoption of digital pathology solutions is expected to create significant opportunities as AI-driven technologies enhance diagnostic precision and laboratory efficiency. In 2022, the US Food and Drug Administration (FDA) approved the first artificial intelligence (AI)-based software designed to assist pathologists in detecting prostate cancer. This approval highlights the increasing integration of AI into digital pathology, aiming to enhance diagnostic accuracy and efficiency.

AI algorithms assist in analyzing histopathological slides, identifying patterns that may be challenging for human pathologists to detect. Digital pathology platforms facilitate remote consultations and second opinions, improving accessibility to expert diagnoses. Automated slide analysis speeds up workflow, reducing turnaround times for critical diagnoses, particularly in oncology. Advancements in cloud-based pathology solutions allow seamless data sharing between healthcare institutions, fostering collaboration.

AI-powered pathology tools help reduce human errors and standardize diagnostic processes across laboratories. Growing investments in AI research support the development of machine learning models tailored for pathology applications. Regulatory approvals and expanding clinical validation of AI-driven pathology software further strengthen market potential.

Rising demand for precision diagnostics and personalized medicine aligns with the capabilities of AI-enhanced pathology systems. Healthcare providers recognize the value of AI-assisted pathology in optimizing patient outcomes and streamlining laboratory operations. Ongoing partnerships between pathology labs and AI technology firms accelerate innovation in digital pathology, transforming diagnostic workflows.

Impact of Macroeconomic / Geopolitical Factors

Macroeconomic and geopolitical factors play a crucial role in shaping the anatomic pathology market. On the positive side, the growing focus on healthcare infrastructure in emerging markets drives the adoption of advanced diagnostic tools and anatomic pathology services, as governments seek to address the increasing burden of chronic diseases and cancer. Additionally, global healthcare investments, particularly in developed regions, support the growth of laboratories and diagnostic facilities.

However, geopolitical instability, trade restrictions, and regulatory challenges can slow down the market’s expansion, especially in regions heavily dependent on imported medical equipment and reagents. While budget constraints may limit the accessibility of advanced diagnostic services, the overall demand for pathology testing is likely to continue rising as more patients require accurate diagnoses for complex conditions.

As healthcare systems evolve to become more comprehensive and efficient, the market is expected to benefit from increasing investments in technology and diagnostic services, which should enhance accessibility and affordability in the long run.

Trends

Shift Toward Personalized and Molecular Pathology Driving Market Growth

Rising demand for personalized and molecular pathology is a recent trend significantly driving the market. High advancements in molecular diagnostics and precision medicine have made pathology increasingly focused on personalized treatment strategies. This shift is expected to improve the accuracy of diagnoses and therapeutic outcomes, allowing for better-targeted treatments. Personalized pathology, which tailors healthcare interventions to individual genetic profiles, has gained significant momentum in the medical community.

The trend is likely to grow as molecular pathology tests provide deeper insights into disease mechanisms, particularly cancer. In 2023, the National Institutes of Health (NIH) launched the All of Us Research Program, which aims to gather health data from over one million people to accelerate research in personalized medicine. This initiative highlights the importance of molecular pathology, paving the way for tailored treatments based on individual patient profiles, thus further driving the anatomic pathology market.

Regional Analysis

North America is leading the Anatomic Pathology Market

North America dominated the market with the highest revenue share of 40.3% owing to advancements in digital pathology and increasing cancer diagnostics. F. Hoffmann-La Roche Ltd’s launch of a next-generation digital pathology platform in September 2021 enhanced collaboration among medical professionals by enabling the seamless sharing of high-resolution pathology images. The integration of whole-slide imaging technology improved diagnostic accuracy and accelerated research advancements in disease detection.

The rising prevalence of cancer, neurodegenerative diseases, and autoimmune disorders fueled demand for precision pathology solutions. The widespread adoption of artificial intelligence-assisted image analysis improved workflow efficiency and reduced diagnostic errors. Expanding investments in laboratory automation and telepathology further strengthened accessibility to advanced diagnostic tools.

Additionally, government initiatives supporting early disease detection and precision medicine encouraged hospitals and research institutions to adopt cutting-edge pathology solutions, reinforcing North America’s leadership in diagnostic innovations.

The Asia Pacific region is expected to experience the highest CAGR during the forecast period

Asia Pacific is expected to grow with the fastest CAGR owing to increasing cancer cases and expanding healthcare infrastructure. Rising investments in laboratory modernization across China, India, and Japan are expected to improve access to high-quality diagnostic services. Government initiatives promoting early disease detection and personalized medicine are likely to accelerate the adoption of digital pathology systems.

Collaborations between international technology providers and regional healthcare institutions are anticipated to enhance diagnostic accuracy and efficiency. The growing use of AI-driven image analysis tools is projected to improve pathology workflow and reduce turnaround times. Increasing demand for telepathology solutions in remote and underserved areas is expected to strengthen access to specialized pathology expertise. Additionally, the expansion of medical research and clinical trials in the region is likely to drive demand for sophisticated pathology platforms, supporting continued market growth in Asia Pacific.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherland

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- New Zealand

- Singapore

- Thailand

- Vietnam

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

Key players in the bioanalytical testing services market focus on expanding capabilities in biomarker analysis, pharmacokinetics, and immunogenicity testing to support drug development. Companies invest in advanced analytical techniques such as LC-MS and PCR to enhance accuracy, efficiency, and regulatory compliance. Strategic partnerships with pharmaceutical and biotechnology firms help drive demand for contract research services and streamline clinical trial processes.

Emphasis on automation, data integrity, and high-throughput screening strengthens market position and accelerates drug approval timelines. Many players also expand geographically to provide comprehensive testing solutions for global biopharmaceutical clients. Charles River Laboratories is a leading company in this market, offering specialized bioanalytical testing solutions for preclinical and clinical drug development.

The company focuses on scientific innovation, regulatory expertise, and strong client collaborations to advance therapeutic research. Charles River’s commitment to quality and precision establishes it as a key player in the bioanalytical services industry.

Top Key Players in the Anatomic Pathology Market

- Quest Diagnostics Incorporated

- PHC Holdings Corporation

- Koninklijke Philips N.V.

- EmeritUS$X

- Danaher

- Cardinal Health

- BioGenex

- Bio SB

Recent Developments

- In June 2022, EmeritUS$X, a cancer diagnostics company, expanded its operations by acquiring Freedom Pathology Partners. This move was aimed at strengthening its capabilities in molecular diagnostics, anatomic pathology, and fluorescence in situ hybridization, further enhancing its national presence in precision oncology testing.

- In April 2021, Koninklijke Philips N.V. entered into a partnership with Ibex Medical Analytics, a company specializing in artificial intelligence for pathology. The collaboration was aimed at promoting AI-powered digital pathology solutions in hospitals, healthcare systems, and diagnostic labs worldwide, improving efficiency and accuracy in cancer detection.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | US$ 35.1 billion |

| Forecast Revenue (2034) | US$ 80.1 billion |

| CAGR (2025-2034) | 8.6% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments |

| Segments Covered | By Product & Services (Instruments (Microtomes & Cryostat, Tissue Processors, Automatic Stainers, Whole Slide Imaging (WSI) Scanners, and Others), Consumables (Antibodies (Primary Antibodies and Secondary Antibodies), Kits & Reagents (Stains & Solvents, Fixatives, and Others), Probes, and Others), and Services), By Application (Disease Diagnosis (Cancer (Breast Cancer, Gastrointestinal Cancer, Lung Cancer, Prostate Cancer, and Others) and Other Diseases), Drug Discovery & Development, and Others), By End-user (Hospitals, Research Laboratories, Diagnostic Laboratories, and Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Quest Diagnostics Incorporated, PHC Holdings Corporation, Koninklijke Philips N.V., EmeritUS$X, Danaher, Cardinal Health, BioGenex, and Bio SB. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |