Quick Navigation

Report Overview

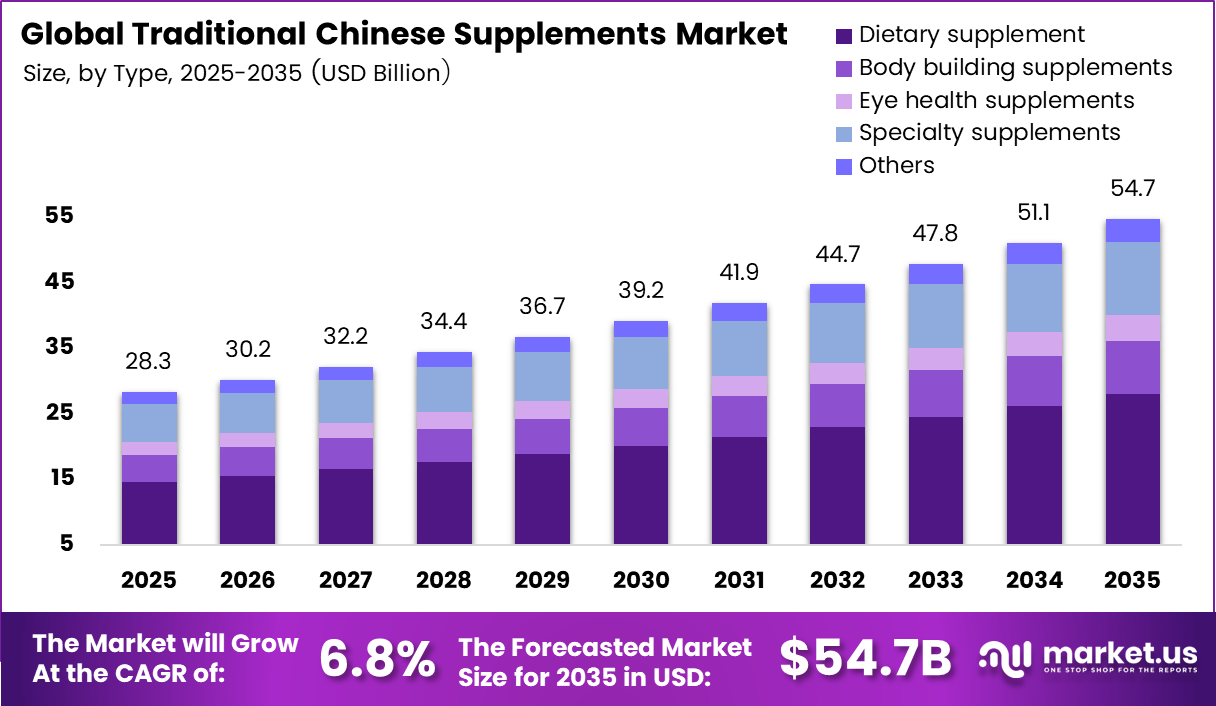

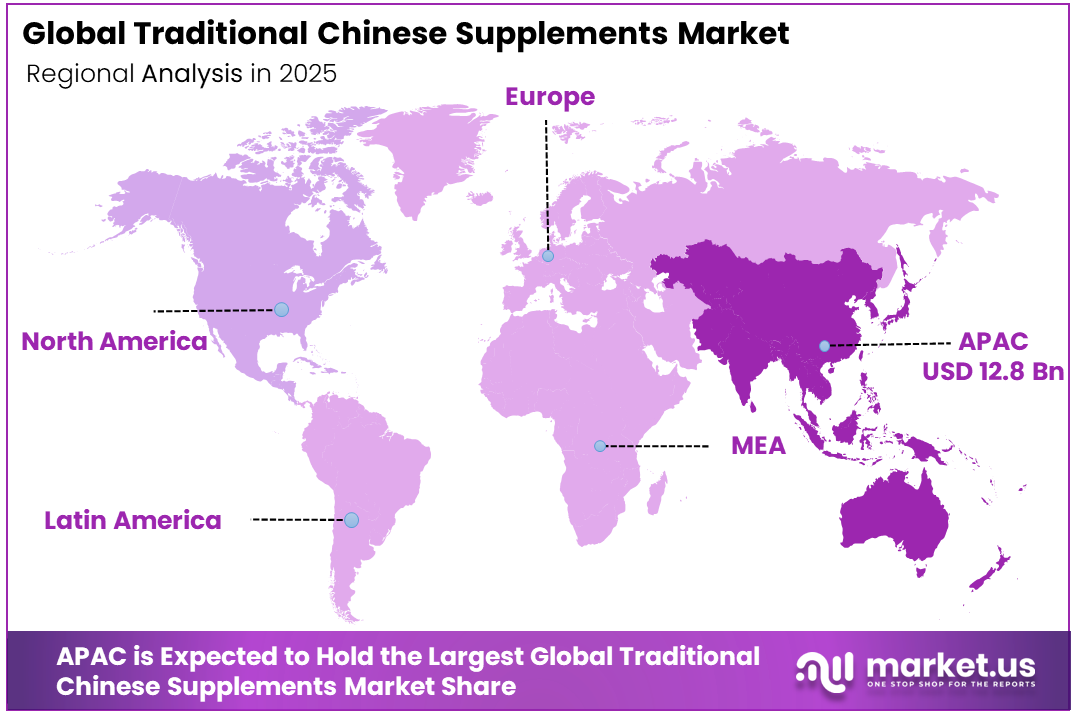

The Global Traditional Chinese Supplements Market is expected to be worth around USD 28.3 billion in 2025, growing at a CAGR of 6.8% to reach a value of USD 54.7 billion by 2035. Asia Pacific held a dominant market position, capturing more than a 45.3% share, holding USD 12.83 billion in revenue.

The Traditional Chinese Supplements (TCS) play the role of an essential ingredient of well-being through herbal extraction, botanical preparation, and nutraceutical formulation that follows the philosophy of Traditional Chinese Medicine (TCM). Unlike other supplements, the Traditional Chinese Supplements products need to adhere to the traditional pharmacopoeial requirements and exhibit efficacy results in terms of cardiology, digestion, and general wellness.

- Rising chronic disease prevalence with diabetes among Chinese adults projected to rise from 8.2% to 9.7% — alongside a population life expectancy exceeding 77 years, is compelling an estimated 300+ million aging consumers to proactively integrate TCM supplements into daily chronic disease prevention and management routines.

There has been growth in both production and consumption because of the rise in disposable income levels, awareness of immunity following the coronavirus disease, and the cultural revitalization of Traditional Chinese Medicine among the younger population. There is growth in the market presence in North America and Europe due to the support received from the WHO, as well as the preference for plant-based remedies by consumers.

The Global Traditional Chinese Supplements Market will grow owing to the increased focus on health and wellness, aging populations, and growing preference for preventive, natural health care products. Immunity awareness following the coronavirus outbreak has made a significant number of people become aware of the use of Traditional Chinese Medicine beyond the Asian continent, especially in North America and Europe.

Key Takeaways

- The global Traditional Chinese Supplements market size was USD 28.3 billion in 2025.

- The global Traditional Chinese Supplements market size is estimated to grow to USD 54.7 billion by 2035.

- The Compound Annual Growth Rate (CAGR) of the market from 2026 to 2035 will be at 6.83%.

- Based on the type segment, the market share for Dietary Supplements stood at 51.3% of the total type segment.

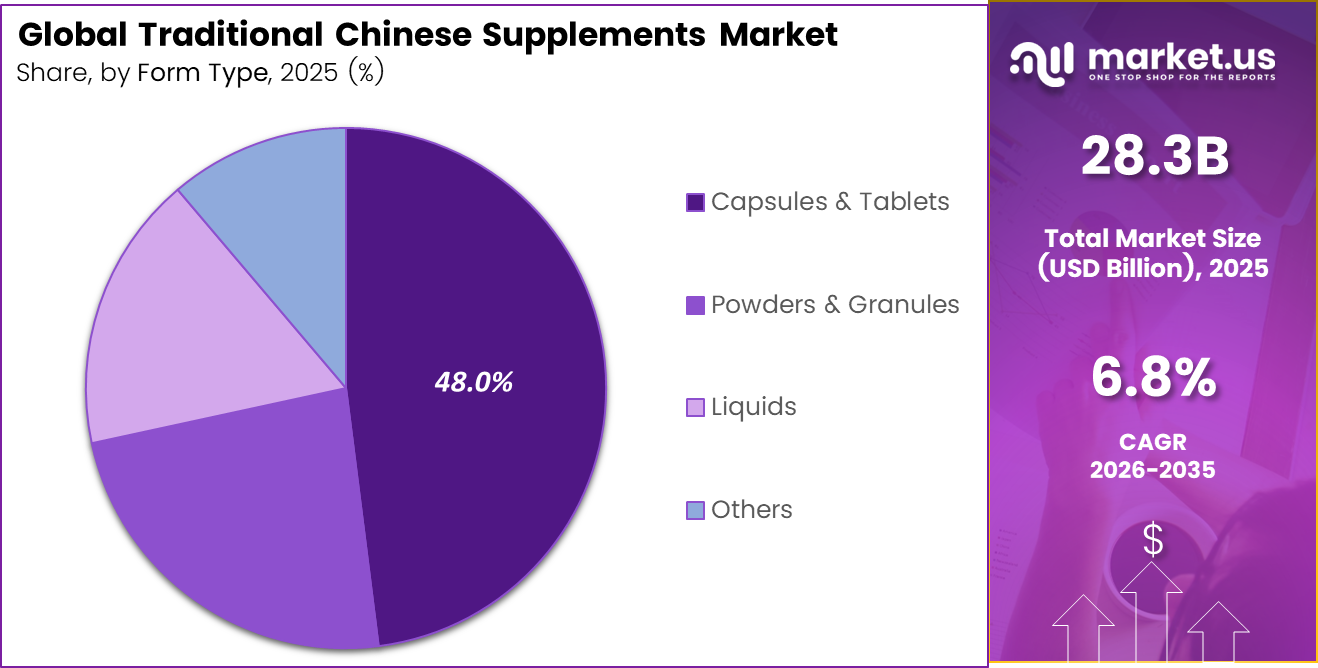

- Based on the form segment, the Capsules & Tablets segment contributed to 48.0% of the form segment.

- Based on the application segment, the leading application category was the General Wellness & Immunity segment, contributing to 45.6% of the total application revenue.

- Based on the end-user segment, the Hospitals sub-category holds a market share of 46.3% as a result of clinical applications of supplements based on traditional Chinese medicine.

- The leading regional market is the Asia Pacific, with a market share of 45.3% of total global revenue.

Type Analysis

Dietary Supplements Dominate Global Demand Through Preventive Healthcare Adoption and Strong Consumer Confidence

Dietary Supplements lead the Traditional Chinese Supplements industry, contributing 51.3% of the market share on account of their vast application in areas of immunity, heart function, metabolism, and anti-aging, which forms an integral part of TCM principles.

Clinically proven herbs like Ginseng, Astragalus, and Cordyceps have helped establish this category as the most preferred category across all markets, owing to consumer awareness, cross-border regulation approvals, and solid scientific validation of efficacy, especially for health-conscious adults over the age of 40. According to the management of BYHEALTH Co., Ltd., its TCM-based dietary supplements contributed about 60% of the total sales revenue in 2024 due to repeat purchase behavior of consumers looking for products for boosting their immunity and energy.

Specialty Supplements at 20.3% represent the fastest growing category, driven by rising demand for condition-specific TCM solutions targeting stress, sleep, and hormonal balance. Body Building Supplements (14.8%), Eye Health Supplements (7.2%), and Others (6.4%) complete the remaining segments.

Form Analysis

Capsules & Tablets Maintain Market Leadership Through Convenience, Standardized Dosage, and Regulatory Compatibility

Capsules & Tablets lead the form category with a 48.0% share owing to their standardized dosing, long shelf life, and convenience of administration, which is essential for purchase through hospitals and pharmacies worldwide. This form can encapsulate highly concentrated extracts of herbs in dosages equivalent to those of decoctions but without the hassles involved in their preparation.

OEM nutraceutical companies favour this form because of its compatibility with automation in production and regulatory acceptance in the US, EU, and China. Powders & Granules holding 23.6% share are experiencing the highest growth in terms of form type due to the rising demand from functional beverages on e-commerce websites by health-conscious consumers.

The trend for dissoluble forms that can easily be incorporated into daily wellness regimes has also led to an increased demand for the form type. For example, Infinitus (Hong Kong) Company Ltd. introduced its Astragalus-Reishi immunity blend in 2024, which was based on granules and sold more than 2 million units in six months on its online website. Liquids, holding 17.2% share, remain popular in Chinese traditional tonics and herbal syrups, while others make up 11.2%.

Application Analysis

General Wellness & Immunity Drives Market Expansion Amid Rising Global Preventive Healthcare Awareness

General Wellness & Immunity comprises 45.6% of overall application income owing to the increasing global need for better immunity and the popularity of adaptogenic Traditional Chinese Medicine Market ingredients such as reishi mushroom, schisandra, and elderberry. Hospital endorsements from China, Japan, and South Korea have enhanced the credibility of immunity-focused Traditional Chinese Medicine Market formulations while broadening the user base to include urban millennial consumers and medical practitioners.

With the growing focus on preventive healthcare post-pandemic, cultural familiarity with immunity-based Traditional Chinese Medicine Market formulations, and premium pricing power, the General Wellness & Immunity category is likely to remain dominant. For example, Eu Yan Sang International Ltd.’s wellness and immunity products have made up around 55% of its overall retail income owing to high sales of ginseng, lingzhi, and bird’s nest in Singapore, Malaysia, and Hong Kong.

Cardiology and Digestive & Liver Health are the fastest-growing segments due to rising lifestyle diseases and growing Traditional Chinese Medicine Market clinical trials. For instance, a 2024 study in China showed that Danshen-based formulations reduced cardiovascular risk markers by 28% over 12 weeks. Cognitive health, bone & joint, and women’s wellness form the remaining share.

End-User Analysis

Hospitals Lead Market Revenue Due to Expanding Institutional Integration of Traditional Chinese Medicine

Hospitals represent 46.3% of Traditional Chinese Medicine revenues due to the high level of institutional penetration of Traditional Chinese Medicine into the healthcare system, especially in China, where TCM is integrated into health care policy, and almost 95% of state-owned hospitals have their own TCM departments.

Hospitals’ purchase volumes are high, standardized, and recurrent, making them the most reliable and valuable distribution channel for TCS producers. The government’s reimbursement policy for TCM treatments in China, South Korea, and Taiwan helps to lower the financial burden of patients and increases the number of repeated prescriptions of standardized herbal supplements.

Clinics and Research Centers represent the leading end-user growth segment because of increasing integration of conventional medicine with alternative therapy, increased private use of TCM treatment, and increasing spending on clinical research worldwide. For example, over 350 clinics of integrative medicine located in the USA included Astragalus and Ginseng therapies in their immune system recovery plans and incurred expenditure totaling USD 45 million on direct purchase of TCSs in 2024.

Key Market Segments

By Type

- Dietary Supplement

- Body Building Supplements

- Eye Health Supplements

- Specialty Supplements

- Others

By Form

- Capsules & Tablets

- Powders & Granules

- Liquids

- Others

By Application

- Cardiology

- General Wellness & Immunity

- Digestive & Liver Health

- Others

By End-User

- Hospitals

- Clinics

- Research Centers

- Other

Opportunities

Silver-care bundles represent a future growth opportunity because China’s current supplement demand already reflects population aging and preventive healthcare, while the next expansion phase will come from recurring supplement-and-service packages distributed through home care, community care, rehabilitation centers, and township service networks.

China had 297 million people aged 60 and above and 217 million aged 65 and above at the end of 2023. With national elderly-service infrastructure planned for wider development through 2029 and further improvement through 2035, supplement companies could shift from individual product sales to monthly care packages, adherence programs, and caregiver-supported replenishment.

Converting only 3% to 4% of the population aged 65 and above at an annual spending level of about US$180 to US$260 could generate an additional addressable revenue pool of approximately US$1.2 billion to US$2.3 billion. Institutional distribution could also raise customer retention by 12 to 18 percentage points and reduce acquisition costs by 20% to 30%, supporting an estimated +2.4 percentage-point CAGR upside, particularly across China, East China, and lower-tier cities within the next two years.

| Opportunity | (~) % Potential CAGR Upside | Geographic Relevance | Execution Window |

|---|---|---|---|

| Silver-care bundles | +2.4% | China’s core, East China, lower-tier cities | Short term (≤ 2 years) |

| Cross-border premiumization | +1.9% | China core, HK gateway, top-tier cities | Short term (≤ 2 years) |

| Personalized digital TCM | +2.1% | China urban, North America Chinese diaspora, SEA | Medium term (2-4 years) |

| Women’s healthy-aging formats | +1.7% | China, South Korea, Singapore | Medium term (2-4 years) |

| Medical-channel granule expansion | +2.6% | China’s core provincial hospital clusters | Medium term (2-4 years) |

| Wellness tourism integration | +1.4% | China tourism hubs, Hainan, Greater Bay Area | Long term (≥ 4 years) |

Challenges

Regulatory complexity remains a continuous market friction rather than a complete sales barrier. China has resumed health food approvals and expanded functional claims, but Traditional Chinese supplement brands still face several overlapping rules. These requirements can extend product launch timelines by 12 to 24 months and reduce annual launch activity by around 15% to 25%.

Decree No. 280, effective from June 2026, adds revised registration requirements for overseas manufacturers, alongside separate CBEC, health food, dosage-form, labelling, and advertising rules. Brands may need to manage 3 to 5 regulatory pathways per product family, while compliance teams can absorb 8% to 12% of total SG&A. This creates an estimated -1.8 percentage-point CAGR drag, which may ease over 2 to 4 years as clearer precedents, digital tools, and standardized compliance systems develop.

| Challenge | (~) % CAGR Friction Drag | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| Regulatory complexity escalation | -1.8% | China core, HK routing, CBEC hubs | Medium term (2-4 years) |

| Compliance-cost inflation | -1.4% | China’s general trade, bonded zones | Medium term (2-4 years) |

| Talent and TCM know-how gap | -1.6% | China’s urban international expansion nodes | Long term (≥ 4 years) |

| Supply chain traceability burden | -1.3% | China import corridors, GBA logistics | Medium term (2-4 years) |

| Demographic and affordability tension | -1.5% | China nationwide, lower-tier cities | Long term (≥ 4 years) |

| Evidence generation and data deficit | -1.7% | Global TCM markets, export destinations | Long term (≥ 4 years) |

Drivers

China’s aging population is directly expanding demand for Traditional Chinese supplements. By the end of 2025, the country had 323.38 million people aged 60 and above, representing about 23% of the population, while 223.65 million were aged 65 or older. The 60+ population is expected to exceed 400 million around 2035, creating sustained demand for immunity, sleep, digestive, bone-joint, cardiovascular, and healthy-aging products.

This demographic shift is moving consumption from seasonal tonic purchases toward regular daily supplementation. Purchase frequency could rise from about 2.1 to 3.4 times annually, while spending per active elderly consumer may increase by RMB 180 to RMB 420. Stronger pharmacy sales, community-care distribution, and repeat purchases could support an estimated +2.3 percentage-point increase in the 2026 baseline CAGR, particularly across East China and lower-tier urban markets.

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aging-led daily wellness demand | +2.3% | China’s core, East China, lower-tier urban China | Long term (≥ 4 years) |

| Faster regulatory throughput | +1.8% | China’s core, domestic manufacturing hubs | Medium term (2-4 years) |

| Format expansion for seniors | +1.4% | China’s core, elderly-care channels, pharmacies | Short term (≤ 2 years) |

| Evidence-based TCM modernization | +1.6% | China’s core, hospital-linked markets, export spillover | Medium term (2-4 years) |

| Health-food approval normalization | +1.9% | China core, local brands, specialty retail | Short term (≤ 2 years) |

| Silver-economy service buildout | +1.5% | China nationwide, community care networks | Long term (≥ 4 years) |

Restraints

Imported registration remains an immediate restraint because Traditional Chinese supplements carrying functional claims cannot scale freely in China without registration or filing. Although China resumed imported health-food approvals in 2025 after an eight-year pause and approved 2,130 health-food registrations, foreign products still represented only a small share. Domestic companies, therefore, continue to capture most approval capacity and retail access.

Imported products may require 12 to 24 months longer than domestic filing-based launches. Testing, dossier preparation, local-agent fees, inventory holding, and delayed market entry can reduce the first two years’ IRR by an estimated 400 to 900 basis points per SKU. For portfolios planning 20 to 30 launches, this may defer RMB 50 million to RMB 150 million in annualized sales, creating an estimated -2.2percentage-point drag on the 2026 baseline CAGR.

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Imported registration bottleneck | -2.2% | China’s core, cross-border import corridors | Medium term (2-4 years) |

| Compliance-cost step-up | -1.8% | China general trade, bonded hubs, HK routing | Short term (≤ 2 years) |

| Consumer affordability ceiling | -1.7% | China’s lower-tier cities, inland provinces | Long term (≥ 4 years) |

| Evidence-linked trust limits | -1.5% | China’s premium urban, export-facing markets | Medium term (2-4 years) |

| Narrow functional claim scope | -1.3% | China’s core domestic innovation clusters | Medium term (2-4 years) |

| Channel margin dilution | -1.4% | China e-commerce, pharmacies, distributor layers | Short term (≤ 2 years) |

Geopolitical Impact Analysis

Trade Policy Dynamics, Intellectual Property Systems, and Bilateral Healthcare Treaties Altering TCS Market Structure

The geopolitical dynamics have diverse effects on the Traditional Chinese Supplements market through impacts on supply chains, regulatory acceptance, and international volumes of trade. The domination of China as the largest exporter of medicinal herbs, which makes up more than 75% of the world’s export volumes, including Ginseng, Astragalus, and Wolfberry, becomes a huge supply concentration issue when there are rising tensions between the US-China and EU-China trade relations.

The introduction of tariffs on nutraceutical raw material imports from China in the 2018–2025 trade dispute led to an increase in the cost of production for TCS manufacturers in North America by between 12% and 18%. This led to the diversification of the supplier base from China to other regions such as Vietnam, India, and South Korea.

Additionally, the BRI by China is making it easy to penetrate the TCM market in 140+ countries through bilateral health cooperation agreements, trade missions, and the setting up of TCM hospitals. The WHO ICD-11 and ASEAN harmonization initiatives have been reducing geopolitical factors that would hinder the entry of TCS in Southeast Asian and Middle Eastern markets. Protection of intellectual property for unique formulations in developing markets limits premium brand growth.

Regional Analysis

Asia Pacific Dominates the Global TCS Market, Accounting for 45.3% Revenue Share in 2025

In the Asia Pacific region, it is clear that it leads the market in revenues from the global Traditional Chinese Supplements business, accounting for 45.3% of total global market share by 2025. It continues to lead with China being the nucleus of the region as it provides almost all of the revenues in the region via its institutionalized TCM healthcare system, compulsory implementation of TCM into public hospitals, and world-class botanical ingredient manufacturing ecosystems.

The National Administration of Traditional Chinese Medicine of China has revealed that TCM services accounted for more than 1 billion visits to patients in 2023, hence creating a huge co-prescription demand for herbal supplements. In addition, the Kampo medicine of Japan and Hanbang medicine of South Korea continue to solidify the position of Asia Pacific by providing substantial institutional and retail revenues from their respective botanics-based medicines.

North America and Europe are leading secondary markets that have grown rapidly owing to growing customer preference for integrative wellness, an expanding network of traditional Chinese medicine practitioners, and increasing availability of herb-based supplements of Asian origin in the retail market. Latin America and MEA are new regions where wellness consumption among the middle class is growing, there is a growing health infrastructure investment, and the entry of TCM via BRI.

Key Regions and Countries Covered in this Report

- North America

- The US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia & CIS

- Rest of Europe

- APAC

- China

- Japan

- South Korea

- India

- ASEAN

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Suppliers in Traditional Chinese Supplement manufacturing seek to build a competitive advantage by emphasizing technological distinction, botanical quality, and channel integration for their products. Key areas of focus include innovation in formulation through the development of standardized herbal extract formulations, highly-dosed capsule technologies, and AI-powered personalized supplement offerings, which increase therapeutic value and applicability in immunity, cardiovascular, and digestive health, among other health benefits.

Further, companies have continued to make significant investments in product development based on clinical research due to the higher premiums and faster uptake of evidence-backed formulations within institutions around the globe. The vertical integration of botanical supplies from suppliers and contract manufacturing organizations ensures a degree of stability in ingredients sourcing, cost efficiency amidst high variability in the prices of herbs.

Capacity building, especially within the Asia-Pacific region, offers an advantage for alignment with strong demand from hospitals, clinics, and e-commerce distribution networks. Moreover, the emphasis on regulatory requirements spanning across multiple markets, certifications like Good Manufacturing Practice (GMP), and quality standardization ensures large-scale efficiency, while entering into long-term agreements with hospitals and pharmaceutical retailers improves consumer retention.

Market Key Players

- Herbalife

- GNC Holdings

- Amway

- Nature’s Bounty

- NOW Foods

- Optimum Nutrition

- Garden of Life

- USANA Health Sciences

- Swanson Health Products

- BYHEALTH Co., Ltd

- Infinitus (Hong Kong) Company Ltd

- Nestlé Health Science

- Blackmores Limited

- Eu Yan Sang International Ltd

- Tongrentang Technologies Co., Ltd

- Sino Biopharmaceutical Limited

- Other Key Players

Recent Development

- In February 2026, BYHEALTH Co., Ltd. launched a precision TCM supplement range that leverages AI-based constitution profiling and standardized herbal extracts, targeting 50 million personalized health consumers in China, marking a significant step toward technology-driven supplement personalization.

- In March 2026, Herbalife unveiled a clinically proven Ginseng-Astragalus immunity complex, backed by a multicentre RCT, strengthening its brand positioning in North American and European markets.

- In April 2026, Nestlé Health Science completed the acquisition of a TCM botanical extraction startup, bolstering its upstream supply chain capabilities and reinforcing its presence in the premium traditional herbal supplement segment.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 28.3 Billion |

| Forecast Revenue (2035) | USD 54.7 Billion |

| CAGR (2026-2035) | 6.83% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020–2024 |

| Forecast Period | 2026–2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Type (Dietary Supplement, Body Building Supplements, Eye Health Supplements, Specialty Supplements, and Others), By Form (Capsules & Tablets, Powders & Granules, Liquids, and Others), By Application (Cardiology, General Wellness & Immunity, Digestive & Liver Health, and Others), By End-User (Hospitals, Clinics, Research Centers, and Others) |

| Regional Analysis | North America – The US & Canada; Europe – Germany, France, The UK, Spain, Italy, Russia & CIS, Rest of Europe; APAC – China, Japan, South Korea, India, ASEAN & Rest of APAC; Latin America – Brazil, Mexico & Rest of Latin America; Middle East & Africa – GCC, South Africa & Rest of MEA |

| Competitive Landscape | Herbalife, GNC Holdings, Amway, Nature’s Bounty, NOW Foods, Optimum Nutrition, Garden of Life, USANA Health Sciences, Swanson Health Products, BYHEALTH Co., Ltd, Infinitus (Hong Kong) Company Ltd, Nestlé Health Science, Blackmores Limited, Eu Yan Sang International Ltd, Tongrentang Technologies Co., Ltd, Sino Biopharmaceutical Limited, and Other Key Players |

| Customization Scope | Segment, country, and regional customization, along with company profiling, pricing trends, CAGR updates, competitive benchmarking, and additional application or technology segmentation, can be provided as per client requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate User License (Unlimited Users and Printable PDF) |