Global Tilt Sensor Market Size, Share, Growth Analysis By Material (Non-Metal, Metal), By Technology (MEMS, Fluid-filled, Force Balanced, Others), By Type (Single-Axis, Dual-Axis, Multi-Axis Tilt Sensors), By End Use Industry (Construction & Mining, Automotive & Transportation, Aerospace & Defense, Telecommunications, Others), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2026-2035

- Published date: Mar 2026

- Report ID: 180936

- Number of Pages: 264

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

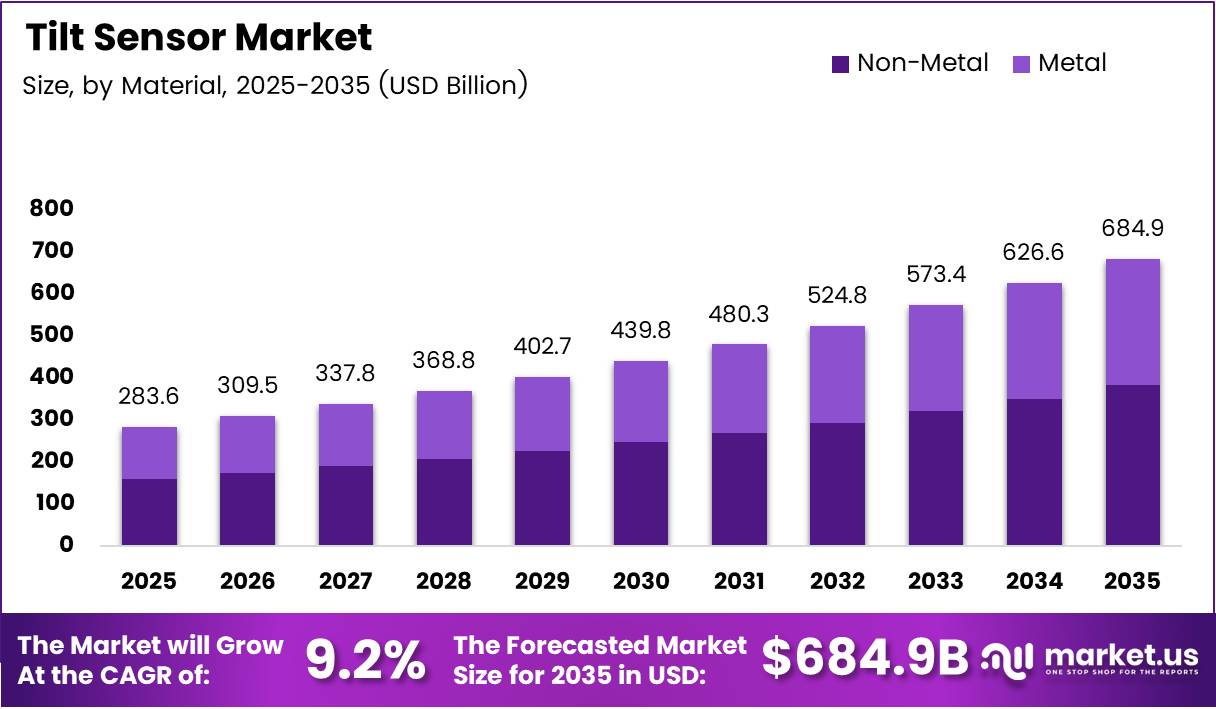

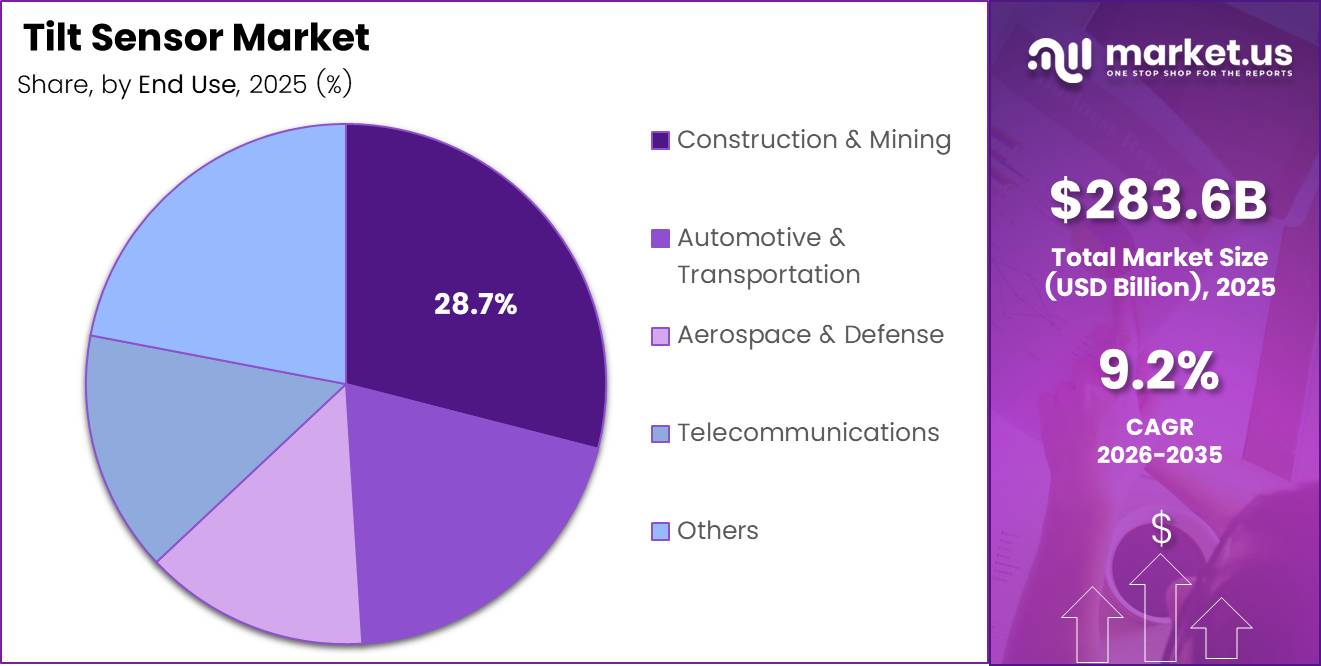

Global Tilt Sensor Market size is expected to be worth around USD 684.9 Billion by 2035 from USD 283.6 Billion in 2025, growing at a CAGR of 9.2% during the forecast period 2026 to 2035.

Tilt sensors measure angular displacement and inclination across a surface relative to gravity. These devices serve critical functions in industrial automation, construction equipment, automotive safety, and aerospace systems. The shift from mechanical angle measurement to MEMS-based electronic sensing defines the current technology transition reshaping this market.

MEMS-based inclinometers now account for the dominant share of new tilt sensor deployments. Their advantages over fluid-filled and force-balanced alternatives include lower power draw, smaller form factors, and digital output compatibility. This shift matters because it lowers integration barriers for OEMs embedding tilt sensing into compact embedded systems.

Construction and mining equipment represent the largest end-use base, capturing 28.7% of demand. Precision angle monitoring in cranes, excavators, and drilling rigs directly reduces accident risk and equipment downtime. As safety regulations in these sectors tighten, tilt sensors shift from optional add-ons to compliance-critical components.

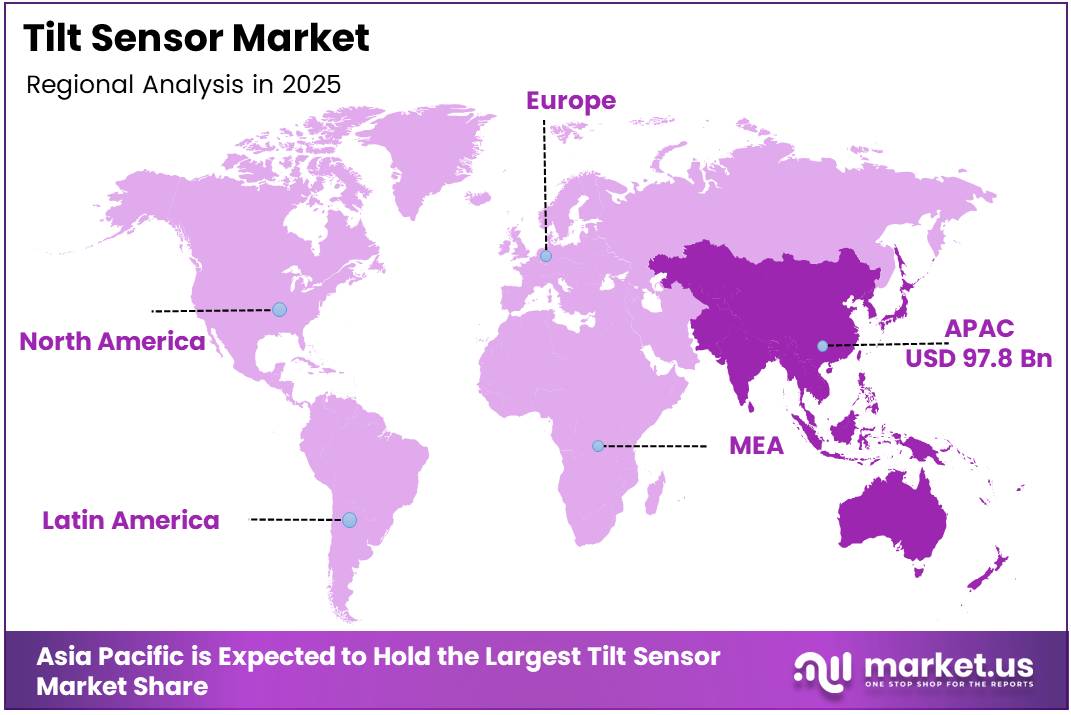

Asia Pacific leads the global market with 34.5% share, valued at USD 97.8 Billion. China and Japan drive this position through high-volume manufacturing of industrial robots, construction machinery, and consumer electronics — all of which require tilt and orientation sensing at scale.

The 9.2% CAGR over the forecast period reflects accelerating replacement of legacy angle-measurement methods across multiple verticals simultaneously. When automotive, construction, and renewable energy sectors all upgrade their sensor infrastructure in parallel, demand compounds in a way that single-vertical growth cycles cannot replicate.

According to STMicroelectronics, the IIS2ICLX tilt sensor delivers ultralow noise performance of 15 µg/√Hz. This specification matters because it enables deployments in precision industrial and automotive applications where signal-to-noise ratio directly determines system reliability — expanding the addressable market beyond general-purpose use cases.

According to Althen Sensors, the ASC TS-91V1/TS-91V5 MEMS capacitive tilt sensors offer resolution of 0.005° and long-term bias stability of 0.1° per year. This level of precision signals that MEMS technology now meets the accuracy thresholds previously reserved for much costlier mechanical or optical systems — compressing the premium segment’s pricing power.

Key Takeaways

- The global Tilt Sensor Market is valued at USD 283.6 Billion in 2025 and forecast to reach USD 684.9 Billion by 2035.

- The market grows at a CAGR of 9.2% during the forecast period 2026 to 2035.

- By Material, Non-Metal tilt sensors lead with 55.4% market share in 2025.

- By Technology, MEMS-based tilt sensors dominate with 52.3% share.

- By Type, Single-Axis Tilt Sensors hold the largest share at 40.3%.

- By End Use Industry, Construction and Mining leads with 28.7% share.

- Asia Pacific dominates regionally with 34.5% share, valued at USD 97.8 Billion.

Product Analysis

Non-Metal dominates with 55.4% due to lower cost and corrosion resistance.

In 2025, Non-Metal held a dominant market position in the By Material segment of the Tilt Sensor Market, with a 55.4% share. Polymer and composite housings reduce unit cost while delivering adequate protection in standard industrial and consumer environments. This cost advantage makes non-metal sensors the default choice for high-volume OEM integrations where price sensitivity outweighs ruggedization requirements.

Metal tilt sensors carry a structural advantage in high-stress deployments. Applications in heavy construction equipment, offshore machinery, and defense systems require enclosures that withstand mechanical impact and extreme temperature cycling. Metal-bodied sensors command a price premium, but their reliability in harsh conditions makes them non-negotiable for safety-critical installations.

In 2024, Shanghai SIBO M&E Co. launched the IS60 inclinometer series with customizable MEMS-based measurement specifically targeting industrial automation and engineering machinery — a segment where metal-housing durability remains a core procurement criterion.

Technology Analysis

MEMS dominates with 52.3% due to miniaturization and digital output compatibility.

In 2025, MEMS (Micro-Electro-Mechanical Systems) held a dominant market position in the By Technology segment of the Tilt Sensor Market, with a 52.3% share. MEMS sensors integrate mechanical sensing elements directly onto silicon chips, enabling compact designs with low power consumption. According to DigiKey, Amphenol Piher dual-axis MEMS tilt sensors support inclination ranges up to ±180° — a measurement range that covers virtually all real-world angular displacement scenarios and removes the need for multi-sensor configurations.

Fluid-filled tilt sensors serve legacy industrial applications where simplicity and low cost matter more than digital integration. These sensors use electrolyte-based chambers to detect angle changes, offering reliable performance in low-frequency measurement environments. However, their analog output and susceptibility to temperature-related fluid viscosity changes limit their adoption in modern embedded control systems requiring precise digital feedback.

Force Balanced tilt sensors occupy a specialized niche in high-accuracy measurement applications. Their servo-controlled mechanism maintains the sensing mass at a null position, delivering exceptionally stable output in low-vibration laboratory, geotechnical, and aerospace environments. The performance advantage justifies a significant cost premium, but the addressable market remains narrow compared to MEMS-based alternatives.

Others in the technology segment include optical, fiber Bragg grating, and capacitive variants. These technologies serve specialized research and infrastructure monitoring applications where standard MEMS resolution is insufficient. Their adoption remains limited by higher unit costs and more complex integration requirements compared to mainstream MEMS solutions.

Type Analysis

Single-Axis Tilt Sensors dominate with 40.3% due to simplicity and cost efficiency in directional monitoring.

In 2025, Single-Axis Tilt Sensors held a dominant market position in the By Type segment of the Tilt Sensor Market, with a 40.3% share. These sensors measure tilt along one plane, making them the practical choice for applications requiring straightforward angle monitoring — such as conveyor inclination, antenna positioning, and platform leveling. Their lower cost and simpler signal processing make them the volume leader in price-competitive industrial applications.

Dual-Axis Tilt Sensors serve applications requiring simultaneous measurement across two perpendicular planes. Construction machinery, agricultural equipment, and vehicle stability systems frequently require this capability to monitor forward-backward and side-to-side tilt simultaneously. The additional measurement axis increases both unit cost and processing complexity, but the richer positional data justifies the premium in safety-critical deployments.

Multi-Axis Tilt Sensors represent the highest complexity tier within this segment. These sensors capture three-dimensional orientation data and are increasingly embedded in autonomous systems, robotics, and drone navigation platforms. As autonomous machinery and UAV deployments scale commercially, multi-axis sensors shift from niche components to standard platform requirements — signaling the fastest growth trajectory within the type segment.

End Use Industry Analysis

Construction and Mining dominates with 28.7% due to mandatory safety monitoring in heavy equipment.

In 2025, Construction and Mining held a dominant market position in the By End Use Industry segment of the Tilt Sensor Market, with a 28.7% share. Cranes, excavators, drilling rigs, and load platforms require continuous angle feedback to prevent tip-overs and maintain structural safety. As worksite automation increases, tilt sensors transition from standalone safety devices to integrated data sources within broader machine control architectures.

Automotive and Transportation represents the fastest-integrating end-use vertical in terms of sensor volume per platform. Electronic stability control, active suspension, and ADAS features all rely on tilt and inclination data to function accurately. As vehicle platforms embed more active safety systems, each unit shipped carries an increasing number of tilt sensor nodes — multiplying demand per vehicle rather than just per model year.

Aerospace and Defense applications demand the highest specification tilt sensors in the market. Flight control surfaces, UAV stabilization, satellite attitude control, and missile guidance systems require sensors with extreme accuracy, shock resistance, and reliability over wide temperature ranges. This end-use segment drives premium pricing and funds R&D that subsequently migrates down to industrial-grade products.

Telecommunications relies on tilt sensors primarily for antenna orientation management and tower structural monitoring. Base station antennas require precise tilt angle control to optimize signal coverage and minimize interference. As 5G densification increases tower counts globally, the cumulative sensor demand from telecommunications infrastructure grows proportionally with network build-out budgets.

Others in the end-use segment includes healthcare devices, consumer electronics, renewable energy systems, and smart infrastructure monitoring. These applications are individually smaller but collectively represent a broad and diversifying demand base — reducing the market’s concentration risk from dependence on any single vertical.

Key Market Segments

By Material

- Non-Metal

- Metal

By Technology

- MEMS (Micro-Electro-Mechanical Systems)

- Fluid-filled

- Force Balanced

- Others

By Type

- Single-Axis Tilt Sensors

- Dual-Axis Tilt Sensors

- Multi-Axis Tilt Sensors

By End Use Industry

- Construction & Mining

- Automotive & Transportation

- Aerospace & Defense

- Telecommunications

- Others

Drivers

ADAS Integration and Industrial Automation Fuel Tilt Sensor Adoption Across High-Volume Platforms

Automotive manufacturers now embed tilt sensors into multiple vehicle subsystems simultaneously — electronic stability control, active suspension, and ADAS all require precise inclination data. According to DigiKey, Amphenol Piher TSDA series tilt sensors deliver accuracy better than ±0.5° with IP69K environmental protection. This specification enables deployment in under-hood and chassis locations previously inaccessible to standard sensors.

Industrial automation and robotics amplify this demand further. Smart manufacturing lines require continuous positional feedback from robotic arms, conveyor systems, and automated guided vehicles. Tilt sensors embedded in these systems reduce positioning errors and enable real-time correction — translating directly into higher throughput and lower scrap rates for manufacturers operating precision assembly operations.

In July 2025, STMicroelectronics announced an agreement to acquire NXP Semiconductors’ MEMS sensor business for up to USD 950 million. This acquisition signals that leading semiconductor companies view MEMS tilt and motion sensing as a strategic growth asset — not a commodity business. Consolidation at this level reshapes supplier relationships and pricing dynamics for OEM buyers across automotive and industrial verticals.

Restraints

Extreme Environmental Conditions and MEMS Calibration Complexity Limit Deployment in Critical Applications

High-vibration environments remain a fundamental challenge for MEMS-based tilt sensors. Construction equipment, mining machinery, and heavy transport vehicles generate mechanical noise that can mask or corrupt angular measurement signals. This performance boundary forces engineers to choose between adding vibration isolation hardware — increasing system cost — or accepting reduced measurement accuracy in the most demanding field conditions.

Thermal stability compounds this challenge. According to STMicroelectronics, the IIS2ICLX inclinometer achieves stability over temperature of less than 0.075 mg/°C. While this represents strong performance for a commercial MEMS device, applications operating at the boundaries of the −40°C to +105°C industrial range still experience measurable drift — requiring calibration routines that add software complexity and commissioning time for system integrators.

Advanced MEMS integration also demands specialized firmware expertise from buyers. Unlike simple analog sensors, digital MEMS inclinometers with embedded machine learning cores require configuration, filtering algorithm selection, and output validation before deployment. This technical barrier slows procurement cycles in smaller industrial operations without dedicated sensor engineering resources — effectively limiting the addressable market to better-resourced buyers.

Growth Factors

Renewable Energy Systems and IoT-Based Predictive Maintenance Open New Revenue Channels for Tilt Sensor Vendors

Solar panel tracking systems represent one of the clearest structural growth opportunities for tilt sensor vendors. Single-axis and dual-axis solar trackers use inclination feedback to follow the sun’s arc, improving energy yield by 20-30% compared to fixed-panel installations. As utility-scale solar capacity expands globally, each installed megawatt creates a proportional demand for precision angle monitoring components embedded in tracker actuators.

In 2024, POSITAL introduced its next-generation Dynamic TILTIX inclinometer products with enhanced signal processing and dual-axis sensing specifically designed for dynamic measurement environments. This product launch targets wind turbine pitch control and solar tracker applications — two renewable energy segments where measurement accuracy under mechanical stress directly determines energy output efficiency and equipment lifespan.

IoT-based predictive maintenance platforms create a multiplier effect on sensor demand. According to STMicroelectronics, the IIS2ICLX tilt sensor operates at approximately 0.42 mA current consumption while delivering full dual-axis performance. This low power draw enables battery-operated wireless tilt nodes on infrastructure assets — making continuous structural monitoring of bridges, towers, and buildings economically viable without wired power infrastructure.

Emerging Trends

Wireless, AI-Enabled, and Multi-Axis Tilt Sensing Redefine Performance Expectations Across Industrial Verticals

Wireless tilt sensors eliminate the cabling requirements that historically limited sensor deployment on moving machinery and remote infrastructure. The shift to low-power wireless protocols enables tilt monitoring on equipment where permanent wiring is impractical — expanding the viable installation base beyond fixed industrial assets to mobile platforms, temporary structures, and geographically distributed infrastructure.

AI-enabled analytics layered onto tilt sensor data streams transforms raw angle measurements into actionable equipment diagnostics. Real-time pattern recognition identifies abnormal inclination behavior that precedes mechanical failure — shifting maintenance models from scheduled service intervals to condition-based intervention. According to ScienceDirect, a research prototype dual-axis fiber Bragg grating tilt sensor demonstrates sensitivity of approximately 229.8 pm/° and measurement accuracy of 0.48°, illustrating the precision frontier that next-generation commercial sensors are approaching.

In September 2025, Gefran showcased the GSH-A multivariable sensor with integrated tilt angle measurement at GIS 2025, supporting CANopen output and MEMS inclinometer technology for mobile hydraulics applications. This product development reflects a broader trend: sensor vendors increasingly combine multiple measurement functions — position, tilt, and vibration — into single integrated units, reducing system complexity for machine builders and opening new specification categories where standalone tilt sensors previously competed on single-function merit.

Regional Analysis

Asia Pacific Dominates the Tilt Sensor Market with a Market Share of 34.5%, Valued at USD 97.8 Billion

Asia Pacific holds 34.5% of the global tilt sensor market, valued at USD 97.8 Billion. China, Japan, and South Korea anchor this position through large-scale production of industrial robots, construction equipment, and consumer electronics — all of which embed tilt sensors at high unit volumes. The region’s concentration of electronics manufacturing capacity also compresses supply chain lead times for sensor integration.

North America Tilt Sensor Market Trends

North America represents a mature but technology-intensive market for tilt sensing. Defense procurement, advanced automotive ADAS systems, and large-scale renewable energy infrastructure drive demand for premium-specification sensors. The region’s strong semiconductor and sensor manufacturing base supports rapid technology refresh cycles, giving North American OEMs early access to next-generation MEMS products ahead of other geographies.

Europe Tilt Sensor Market Trends

Europe combines automotive engineering leadership with strict industrial safety standards — two forces that consistently expand tilt sensor content per machine platform. Germany’s mechanical engineering sector, France’s aerospace industry, and the UK’s defense procurement programs all maintain structural demand for high-accuracy inclination measurement. EU industrial automation investment further supports sensor density per production line across the continent.

Middle East and Africa Tilt Sensor Market Trends

Middle East and Africa present demand concentrated in construction, oil and gas, and telecommunications infrastructure. Large-scale project activity in the GCC — including smart city development and energy diversification programs — creates installation volumes for tilt sensors in structural monitoring, crane operations, and antenna management. South Africa’s mining sector adds a secondary demand base for ruggedized inclination sensors in underground equipment.

Latin America Tilt Sensor Market Trends

Latin America’s tilt sensor demand centers on mining operations in Chile and Peru, agricultural machinery in Brazil, and growing telecommunications infrastructure across the region. Brazil’s agritech sector increasingly embeds precision sensors into harvesting and planting equipment, creating a developing but structurally consistent demand channel. Infrastructure investment programs across multiple countries contribute additional deployment opportunities in civil engineering monitoring applications.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

TE Connectivity Ltd. positions itself as a full-spectrum connectivity and sensing solutions provider with deep penetration across automotive, industrial, and aerospace end markets. Its scale advantage enables TE Connectivity to serve OEM customers with integrated sensor and connector assemblies — reducing the vendor count for large platform programs and creating switching costs that protect its installed base from lower-cost component specialists. In 2024, POSITAL expanded its analog inclinometer lineup with improved MEMS accelerometer performance and enhanced firmware features — a product category where TE Connectivity’s distribution reach creates a parallel competitive channel.

Sick AG builds its market position on industrial automation expertise, combining tilt sensors with broader machine safety and factory automation sensor portfolios. This integrated approach allows Sick AG to sell tilt sensing as part of complete safety system solutions rather than competing on standalone sensor specifications. For manufacturing customers buying entire sensor suites for new production lines, this bundling strategy compresses the evaluation process and favors established automation suppliers over niche tilt sensor specialists.

Murata Manufacturing Co., Ltd. leverages world-class MEMS fabrication capabilities to deliver high-volume tilt sensors for consumer electronics and automotive applications. Murata’s strength lies in production scale and component miniaturization — capabilities that align directly with the trend toward embedding tilt sensing in compact wearables, smartphones, and vehicle control modules. Its vertical integration from MEMS chip design through packaging positions Murata to capture margin across the value chain rather than competing solely on sensor price.

Pepperl+Fuchs Vertrieb GmbH & Co. KG focuses on industrial sensor solutions for process automation and hazardous area applications. Its tilt sensor offerings target environments where intrinsic safety certification and explosion-proof ratings determine procurement decisions — a specification niche where general-purpose MEMS suppliers cannot compete without significant additional certification investment. This regulatory barrier creates a defensible market position in oil and gas, chemical processing, and mining applications where safety compliance is non-negotiable.

Key Players

- TE Connectivity Ltd.

- Sick AG

- Murata Manufacturing Co., Ltd.

- Pepperl+Fuchs Vertrieb GmbH & Co. KG

- Level Developments Ltd.

- IFM Electronic GmbH

- Balluff GmbH

- Jewell Instruments LLC

- The Fredericks Company

- DIS Sensors BV

- Gefran S.p.A.

- MEMSIC Inc.

- Analog Devices, Inc.

- Honeywell International Inc.

- Bosch Sensortec GmbH

- Parker Hannifin Corporation

- Omron Corporation

- Sensata Technologies, Inc.

- Tokyo Sokushin Co., Ltd.

- Posital Fraba Inc.

- Other Key Players

Recent Developments

- September 2025 – Gefran showcased the GSH-A multivariable wire position transducer with integrated tilt angle measurement at GIS 2025. The product supports CANopen output and MEMS inclinometer technology, with variants offering up to 12.5 m stroke and high shock/vibration resistance for mobile hydraulics and lifting machine safety applications.

- July 2025 – STMicroelectronics announced an agreement to acquire NXP Semiconductors’ MEMS sensor business, which includes electromechanical sensors relevant for tilt and motion sensing. The transaction is valued at up to USD 950 million, marking one of the largest MEMS sensor consolidation moves of the year.

- 2024 – POSITAL introduced its next-generation Dynamic TILTIX inclinometer products with enhanced signal processing and dual-axis tilt sensing. The new lineup is designed for dynamic measurement environments and includes next-gen analog inclinometers with improved MEMS accelerometer performance and enhanced firmware features.

- 2024 – Shanghai SIBO M&E Co. launched the IS60 inclinometer sensor series, its first inclinometer product offering customizable MEMS-based tilt measurement. The IS60 targets industrial automation and engineering machinery applications, expanding the competitive field in the Asia Pacific inclinometer segment.

Report Scope

Report Features Description Market Value (2025) USD 283.6 Billion Forecast Revenue (2035) USD 684.9 Billion CAGR (2026-2035) 9.2% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Material (Non-Metal, Metal), By Technology (MEMS, Fluid-filled, Force Balanced, Others), By Type (Single-Axis, Dual-Axis, Multi-Axis Tilt Sensors), By End Use Industry (Construction & Mining, Automotive & Transportation, Aerospace & Defense, Telecommunications, Others) Regional Analysis North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) Competitive Landscape TE Connectivity Ltd., Sick AG, Murata Manufacturing Co. Ltd., Pepperl+Fuchs Vertrieb GmbH & Co. KG, Level Developments Ltd., IFM Electronic GmbH, Balluff GmbH, Jewell Instruments LLC, The Fredericks Company, DIS Sensors BV, Gefran S.p.A., MEMSIC Inc., Analog Devices Inc., Honeywell International Inc., Bosch Sensortec GmbH, Parker Hannifin Corporation, Omron Corporation, Sensata Technologies Inc., Tokyo Sokushin Co. Ltd., Posital Fraba Inc., Other Key Players Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)

-

-

- TE Connectivity Ltd.

- Sick AG

- Murata Manufacturing Co., Ltd.

- Pepperl+Fuchs Vertrieb GmbH & Co. KG

- Level Developments Ltd.

- IFM Electronic GmbH

- Balluff GmbH

- Jewell Instruments LLC

- The Fredericks Company

- DIS Sensors BV

- Gefran S.p.A.

- MEMSIC Inc.

- Analog Devices, Inc.

- Honeywell International Inc.

- Bosch Sensortec GmbH

- Parker Hannifin Corporation

- Omron Corporation

- Sensata Technologies, Inc.

- Tokyo Sokushin Co., Ltd.

- Posital Fraba Inc.

- Other Key Players

Our Clients

- 180936

- Mar 2026