Quick Navigation

- Report Overview

- Key Takeaways

- Engine Placement Analysis

- Fuel Type Analysis

- Engine Capacity Analysis

- Vehicle Type Analysis

- Sales Channel Analysis

- Key Market Segments

- Regional Analysis

- Key Regions and Countries

- Market Dynamics

- Drivers

- Restraints

- Challenges

- Opportunities

- Key Company Insights

- Recent Developments

- Report Scope

Report Overview

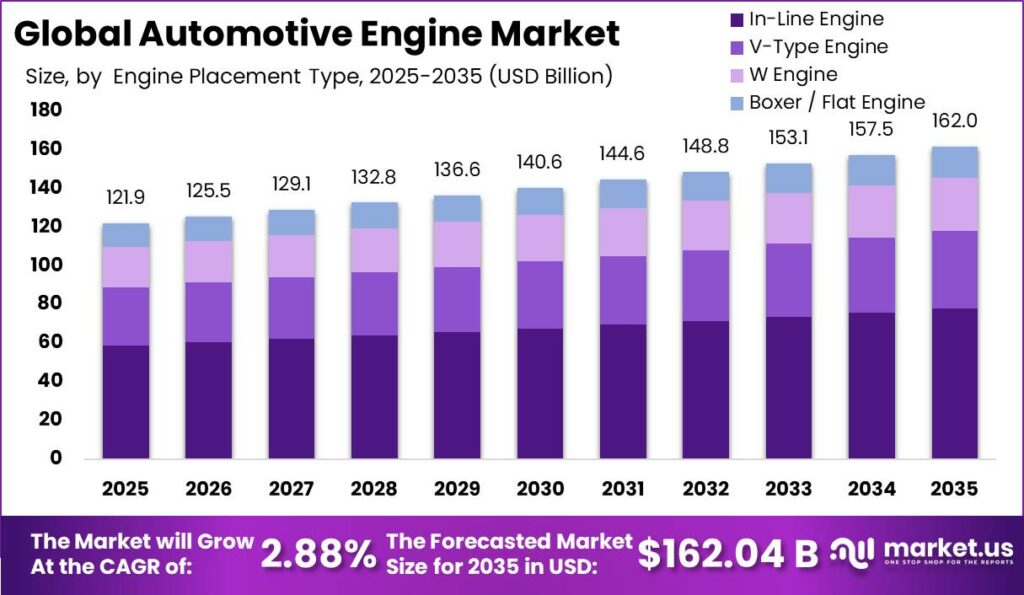

Global Automotive Engine Market size is expected to be worth around USD 162.04 Billion by 2035 from USD 121.94 Billion in 2025, growing at a CAGR of 2.88% during the forecast period 2026 to 2035. This trajectory reflects sustained demand across commercial vehicles, hybrid platforms, and emerging engine applications in developing economies. Investors and suppliers navigating this market must weigh stable volume demand against an accelerating structural shift in powertrain composition across major vehicle classes.

The Automotive Powertrain Market encompasses engines across passenger cars, commercial vehicles, two-wheelers, and off-highway applications, covering both OEM supply and the aftermarket rebuild channel. The market segments by engine placement, fuel type, engine capacity, vehicle type, and sales channel. Each segment reflects a distinct demand pool, buyer profile, and technology investment cycle, making this a structurally complex market requiring segment-level analysis rather than top-line assessment alone.

Key Takeaways

- The global Automotive Engine Market was valued at USD 121.94 Billion in 2025 and is forecast to reach USD 162.04 Billion by 2035.

- The market grows at a CAGR of 2.88% during the forecast period 2026 to 2035.

- By Engine Placement, In-Line Engine dominates with a 48.10% share in 2025.

- By Fuel Type, Gasoline/Petrol engines hold the largest share at 51.20% in 2025.

- By Engine Capacity, Below 1.5L is the leading segment with a 38.20% share in 2025.

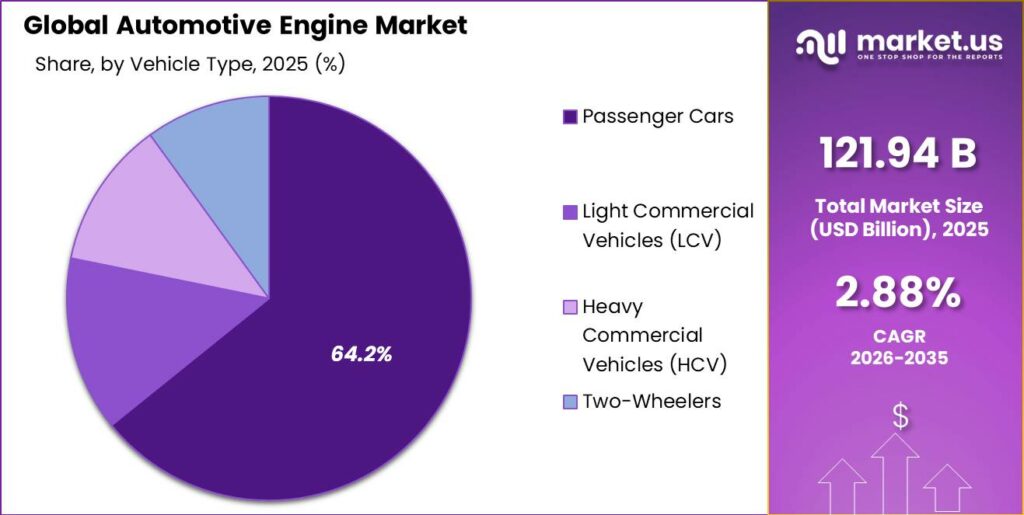

- By Vehicle Type, Passenger Cars hold the dominant position at 64.20% share in 2025.

- By Sales Channel, OEM dominates with an 86.20% share in 2025.

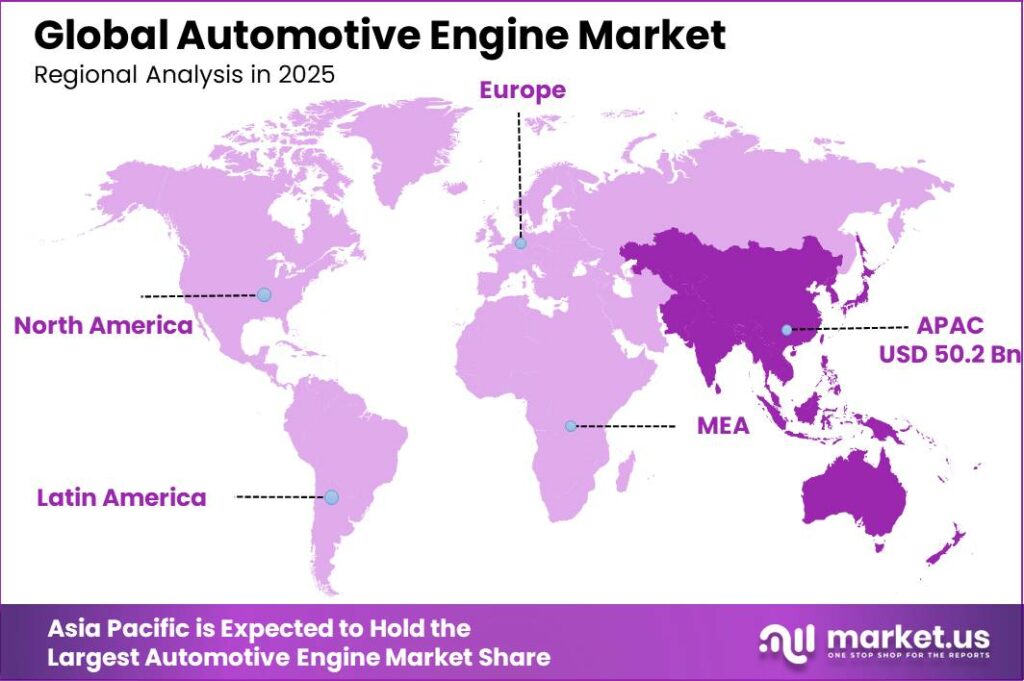

- Asia Pacific is the leading region with a 41.20% share, valued at USD 50.24 Billion in 2025.

However, government policy now plays a decisive role in shaping long-term engine platform investment across every major region. The European Commission’s December 2025 policy revision replaced the previously legislated 100% CO₂ reduction target for 2035 with a 90% threshold, explicitly permitting continued ICE and hybrid vehicle sales beyond 2035. This policy shift adds an estimated 5 to 10 years to the commercial life of engine platforms currently in development, restoring OEM confidence in programs with payback periods extending into the 2040s. Early movers who commit to compliant engine platform investment now will secure procurement commitments before competitors resume capacity planning.

In April 2026, Horse Powertrain revealed the HORSE W30, its first V6 engine designed for mild- and full-hybrid vehicles with 350 to 400 kW output, signaling continued OEM investment in high-performance hybrid engine architectures. According to the IEA, global electric car sales exceeded 17 million units in 2024, a rise of more than 25% compared with 2023. This acceleration compresses the addressable ICE passenger car market in China and Europe, pushing engine suppliers to diversify across commercial, off-highway, and electrification-adjacent segments to protect revenue. IEA data indicates that EVs displaced more than 1 million barrels of oil consumption per day globally in 2024, a figure that quantifies the fuel demand erosion already materializing beneath aggregate engine volume figures.

As per our research, the average age of vehicles in operation in the United States was 12.2 years, creating a structurally large population of aging vehicles requiring engine rebuilds and replacement parts. This aging fleet dynamic insulates aftermarket engine revenue from near-term electrification displacement, as older ICE vehicles will require engine servicing well into the 2030s. Suppliers with established aftermarket distribution networks hold a durable revenue floor that pure-OEM-focused competitors cannot easily replicate.

Engine Placement Analysis

In-Line Engine dominates with 48.10% due to cost efficiency and broad platform compatibility.

In 2025, In-Line Engine held a dominant market position in the By Engine Placement segment of the Automotive Engine Market, with a 48.10% share. This configuration is the default architecture for high-volume passenger car and light commercial vehicle production globally. Its lower manufacturing cost, simpler maintenance profile, and compatibility with both front-wheel-drive and all-wheel-drive platforms make it the preferred OEM choice. Suppliers focused on in-line engine components command the widest addressable market within this segment. In July 2025, BorgWarner secured turbocharger business for a major global OEM’s next-generation compact and light commercial combustion and hybrid vehicles in Europe and North America, directly reinforcing the sustained investment case for in-line engine platform boosting technology.

V-Type engines occupy the mid-to-premium vehicle segment, where higher cylinder counts and displacement support performance and towing applications. These engines carry substantially higher per-unit content value versus in-line alternatives, making them disproportionately valuable to Tier-1 suppliers despite lower production volumes. OEM platform rationalization pressure is concentrating V-Type engine development within a shrinking group of global powertrain groups, tightening the supplier qualification window for component manufacturers seeking new program awards.

W Engine and Boxer/Flat Engine architectures together represent niche but strategically significant configurations in the ultra-premium and brand-identity segments. W engines remain exclusive to a small number of high-displacement platforms, while Boxer engines anchor the brand identity of specific OEM groups in both passenger and performance vehicle lines. These configurations command premium aftertreatment and component pricing, offering suppliers higher margin potential per unit despite constrained volume. Their persistence reflects brand differentiation strategy rather than mass-market economics.

Fuel Type Analysis

Gasoline/Petrol dominates with 51.20% due to widespread vehicle fleet composition and infrastructure depth.

In 2025, Gasoline/Petrol held a dominant market position in the By Fuel Type segment of the Automotive Engine Market, with a 51.20% share. Gasoline engines remain the baseline powertrain across passenger cars and light commercial vehicles in North America, Europe, and much of Asia Pacific. This concentration of installed base creates durable aftermarket demand, as the global vehicle fleet remains predominantly ICE-powered. As reported by the IEA, at the end of 2024 the global electric car fleet reached almost 58 million vehicles, representing about 4% of the world’s passenger car fleet. This means that more than 96% of global passenger vehicles still operate on conventional or hybrid ICE powertrains, anchoring gasoline engine revenue for the medium term.

Diesel engines serve the commercial vehicle, off-highway, and heavy-duty segments where energy density and torque output requirements exceed gasoline engine capability. Diesel’s share of new passenger car production continues to contract in Europe and China, but commercial vehicle diesel demand remains structurally intact. Suppliers with diesel engine expertise and calibration capability for Stage V and BS6 Phase II emission standards hold defensible positions in the commercial and agricultural engine segments, where electrification timelines extend well beyond the passenger car transition curve.

Hybrid-ICE configurations, covering mild, full, and plug-in hybrid architectures, represent the fastest-evolving fuel type segment for engine content investment. These platforms retain an ICE unit while adding electrified torque-fill or range-extension capability. Data from the IEA indicates that during the first quarter of 2025, electric cars accounted for about 1 in 4 cars sold in Europe, with a large share of those being hybrids that retain combustion engine content. Engine suppliers who qualify their components for downsized, high-efficiency hybrid-cycle engines will access the segment that bridges the ICE and BEV eras, capturing per-vehicle content through both engine supply and integration engineering.

Alternative Fuels engines covering CNG, LPG, and ethanol applications serve fleet operators and emerging market vehicle buyers where fuel cost sensitivity outweighs technology novelty, while Hydrogen ICE platforms represent an early-stage but strategically significant growth vector in heavy-duty and off-highway applications. These sub-segments collectively hold the remaining share, yet attract disproportionate R&D investment from OEMs seeking fuel-flexible engine platforms. Suppliers who develop combustion hardware compatible with multiple fuel types will reduce platform dependency risk as regulatory fuel mandates evolve across different regions.

Engine Capacity Analysis

Below 1.5L dominates with 38.20% due to dominance of small-displacement vehicles in Asia Pacific.

In 2025, Below 1.5L held a dominant market position in the By Engine Capacity segment of the Automotive Engine Market, with a 38.20% share. Sub-1.5L engines power the majority of entry-level passenger cars and two-wheelers across India, Southeast Asia, China, and Latin America, where total cost of ownership determines purchase decisions. The concentration of global vehicle production growth in these markets structurally reinforces small-displacement engine demand. OEMs that offer highly refined sub-1.5L platforms with BS6 Phase II or TREM IV compliance gain procurement preference from both government fleet buyers and cost-sensitive private buyers in high-growth markets.

The 1.5L to 3.0L segment covers the broadest range of vehicle applications, spanning compact cars, mid-size SUVs, light commercial vehicles, and entry-level performance vehicles. This capacity band is the primary battleground for hybrid-ICE integration, as most mild and full hybrid systems use downsized engines within this displacement range. Suppliers who optimize components for this range, including turbocharger hardware, thermal management systems, and lightweight valvetrain components, serve the highest-volume, highest-content-value tier of the market, where per-unit engineering investment is most defensible.

Above 3.0L engines serve premium passenger vehicles, full-size commercial trucks, and heavy-duty off-highway equipment. These engines carry the highest per-unit component value in the market, with longer development cycles and lower volume sensitivity to short-term demand fluctuations. Supplier relationships in this tier are long-term and qualification-intensive, meaning incumbents hold structural advantages over new entrants. OEM platform rationalization may reduce the number of distinct Above 3.0L engine families over the forecast period, concentrating supplier revenue among fewer, larger programs.

Vehicle Type Analysis

Passenger Cars dominate with 64.20% due to global fleet scale and high OEM production volumes.

In 2025, Passenger Cars held a dominant market position in the By Vehicle Type segment of the Automotive Engine Market, with a 64.20% share. Passenger car engine volumes reflect the largest single pool of global engine production. As per our research, nearly 22 million electric cars were produced globally in 2025, an increase of more than 25% compared with 2024. This production ramp in BEVs progressively removes engine content from the passenger car segment, accelerating the need for engine suppliers to realign revenue toward commercial and off-highway applications. Figures from the EPA show that in Model Year 2024, 66% of new US light-duty vehicles were classified as light trucks, including SUVs and pickups, sustaining demand for mid-to-large displacement engines in the world’s most profitable automotive market.

Light Commercial Vehicles represent the segment where ICE engine content is most durable against electrification displacement, as range requirements, payload capacity, and infrastructure limitations constrain BEV adoption in urban delivery and last-mile logistics applications. LCV engine demand is supported by e-commerce logistics growth and fleet renewal cycles across Europe, India, and Southeast Asia. Engine suppliers with LCV-specific calibration capability and compliance engineering for Euro 7 and BS6 Phase II serve a segment that is growing in volume while maintaining high ICE engine penetration rates.

Heavy Commercial Vehicles and Two-Wheelers together account for the remaining vehicle type share and represent distinct strategic sub-markets. HCV engine demand is driven by freight volume growth and infrastructure development spending across Asia Pacific, Africa, and Latin America, where diesel remains the dominant fuel with long replacement cycles. Two-Wheeler engines, concentrated in India, Southeast Asia, and Sub-Saharan Africa, represent extremely high-unit-count, low-displacement production volumes, where emission compliance investment per OEM is concentrated and aftermarket demand is structurally large.

Sales Channel Analysis

OEM dominates with 86.20% due to captive production volumes and direct manufacturer supply contracts.

In 2025, OEM held a dominant market position in the By Sales Channel segment of the Automotive Engine Market, with an 86.20% share. OEM supply captures new vehicle production volumes across all engine types, vehicle classes, and geographies, making it the primary revenue channel for every major engine and Tier-1 component manufacturer. Based on EPA data, the average real-world fuel economy of new US vehicles reached a record 27.2 miles per gallon in Model Year 2024, reflecting OEM-driven efficiency investment that translates directly into engine technology upgrade cycles. EPA data also shows that average fuel economy of new US vehicles improved by 41% since Model Year 2004, indicating two decades of sustained OEM engine engineering investment that defines the technology baseline for the current platform generation.

The Aftermarket channel holds the remaining share and serves the global fleet of in-service vehicles requiring engine rebuilds, replacement units, and component servicing. This channel is structurally insulated from near-term electrification displacement because it serves vehicles already on the road. Aftermarket engine revenue is highest in markets with aging fleets, lower new vehicle affordability, and established independent service networks. Suppliers who build dual-channel capability across both OEM and Aftermarket supply strengthen their revenue resilience, since aftermarket volumes are counter-cyclical to new vehicle production downturns.

Key Market Segments

By Engine Placement

- In-Line Engine

- V-Type Engine

- W Engine

- Boxer / Flat Engine

By Fuel Type

- Gasoline / Petrol

- Diesel

- Hybrid-ICE (Mild, Full, Plug-in)

- Alternative Fuels (CNG, LPG, Ethanol)

- Hydrogen ICE

By Engine Capacity

- Below 1.5L

- 1.5L to 3.0L

- Above 3.0L

By Vehicle Type

- Passenger Cars

- Light Commercial Vehicles (LCV)

- Heavy Commercial Vehicles (HCV)

- Two-Wheelers

By Sales Channel

- OEM

- Aftermarket

Regional Analysis

Asia Pacific Dominates the Automotive Engine Market with a Market Share of 41.20%, Valued at USD 50.24 Billion

Asia Pacific holds the commanding position in the global Automotive Engine Market, driven by the scale of vehicle production across China, India, Japan, South Korea, and Southeast Asia. China alone anchors the region through its dual role as the world’s largest vehicle producer and the fastest-adopting BEV market, creating simultaneous demand for both conventional and hybrid engine systems. India’s commercial vehicle and two-wheeler production base, combined with TREM IV and BS6 Phase II compliance investment, sustains substantial engine technology upgrade spending that benefits both OEM and aftermarket engine suppliers across the region.

North America is the fastest-growing region for premium and high-displacement engine applications, supported by a structurally large ICE fleet base and sustained light truck and SUV demand. According to data from Alliance for Automotive Innovation, the United States had 283.97 million registered light-duty vehicles as of December 31, 2024, with 97.9% powered by ICE or hybrid powertrains. The US also recorded 15.79 million new vehicle registrations in 2024, sustaining strong OEM engine supply volume. In May 2026, Volvo Trucks announced an all-new combustion engine platform designed to operate on multiple renewable fuels, underscoring continued manufacturer investment in combustion technology for North American commercial applications.

Europe, Latin America, and the Middle East and Africa collectively represent the remaining regional share, each with distinct demand drivers. Europe’s engine market faces the most acute policy transition pressure from Euro 7 compliance requirements effective November 2026, yet the EU’s revised 2035 CO₂ target restores medium-term planning confidence for engine platform investment. Latin America and Middle East and Africa sustain ICE engine demand through fleet age dynamics, infrastructure constraints on BEV adoption, and commercial vehicle growth, offering engine suppliers durable volume outside the electrification-pressured passenger car segments in mature markets.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East and Africa

- GCC

- South Africa

- Rest of MEA

Market Dynamics

Market Opportunity Analysis - Aging fleets, underserved channels, and emerging market compliance gaps offer entry points for engine suppliers

The aftermarket engine channel remains structurally underpenetrated by OEM-branded certified programs, with independent rebuilders capturing an estimated 65 to 75% of engine rebuild volume in mature markets. This gap is most pronounced in the United States, EU, India, and Middle East and Africa, where the aging vehicle fleet creates sustained rebuild demand without a corresponding OEM-controlled supply response. Suppliers and OEMs who establish branded remanufacturing programs with certified core collection logistics can displace independent rebuilders from a high-margin channel that is growing faster than new engine production volumes.

The Below 1.5L engine capacity segment dominates Asia Pacific production with a 38.20% share, yet the aftermarket service and component supply infrastructure for sub-1.5L engines in Sub-Saharan Africa and parts of Southeast Asia remains thin relative to the installed fleet. This creates a distribution gap for suppliers who can establish localized parts availability and engine rebuild networks in markets where the ICE vehicle fleet will remain dominant for the duration of the forecast period. By contrast, BEV adoption timelines in these regions extend well beyond 2035, giving early entrants in aftermarket engine distribution a long and uncontested runway.

The Two-Wheeler vehicle type sub-segment in India and Southeast Asia represents an extremely high-unit-count, low-displacement engine production base that commands focused aftermarket attention. Two-wheeler engines face faster service intervals and higher replacement frequency than passenger car engines, generating disproportionately high parts and rebuild revenue relative to engine unit value. Suppliers who localize two-wheeler engine component manufacturing or distribution in India, Vietnam, and Indonesia address a segment where established aftermarket relationships translate directly into recurring revenue with minimal OEM program dependency.

The HCV segment in Latin America and Middle East and Africa offers a durable entry point for engine manufacturers seeking volume outside electrification-pressured passenger car markets. Infrastructure development spending and freight growth in these regions sustain diesel HCV demand through the forecast period, with low BEV displacement risk in the near term. Suppliers who develop compliance-ready HCV engine components for these markets ahead of regional emission standard upgrades will secure incumbent supplier positions before competitive pressure intensifies.

Technology and Innovation Landscape - Hydrogen combustion, hybrid integration, and connected diagnostics define the engine technology investment frontier

Hydrogen internal combustion engine technology is advancing from concept to validation-phase investment, as demonstrated by MAHLE Powertrain’s February 2025 entry into the testing phase of Project Cavendish, a £9.8 million UK government-funded program to convert existing heavy-duty truck engines to hydrogen combustion. H2ICE technology offers a combustion-compatible path to near-zero tailpipe emissions in heavy-duty and off-highway applications where hydrogen fuel cell powertrains face infrastructure and cost constraints. Suppliers who develop H2ICE combustion hardware, injector systems, and thermal management solutions now will access a technology window that opens well before mass hydrogen fuel cell adoption in the commercial vehicle segment.

Hybrid-optimized engine boosting technology represents a near-term innovation priority for suppliers serving the electrification-adjacent engine segment. Garrett Motion’s April 2025 presentation of its 3-in-1 E-Powertrain, E-Cooling Compressor, and hybrid-optimized boosting solutions at Auto Shanghai 2025 illustrates that turbocharger and thermal management suppliers are developing integrated electrified modules specifically for downsized hybrid-cycle engines. These systems replace multiple discrete components with a single integrated unit, reducing BOM complexity for OEMs while improving transient torque response in mild and full hybrid architectures. Suppliers who qualify integrated hybrid engine modules on OEM platforms during the current development cycle lock in content per vehicle on the fastest-growing powertrain architecture category.

The Automotive Engine Management System Market is converging with connected vehicle data platforms to enable predictive maintenance and digital service SaaS models. Fleet operators and commercial vehicle OEMs are increasingly specifying engine management systems capable of real-time condition monitoring, fault prediction, and remote calibration updating. This convergence creates a recurring revenue opportunity for engine and component suppliers who embed connectivity hardware and software service capability at the component level, transforming one-time hardware sales into multi-year data service contracts with fleet operators across the US, EU, China, and India.

Engine platform multi-fuel flexibility is emerging as a defining innovation axis for commercial vehicle and off-highway engine manufacturers. In May 2026, Volvo Trucks announced an all-new combustion engine platform designed to operate on multiple renewable fuels, including future hydrogen applications, as part of its next-generation powertrain lineup. This multi-fuel architecture approach reduces OEM exposure to single-fuel regulatory risk while extending the commercial life of combustion engine investment across different regional fuel availability scenarios. Suppliers who develop fuel-agnostic combustion hardware, compatible with diesel, HVO, CNG, and hydrogen fuel blends, serve OEMs with the longest and most defensible combustion engine investment horizon in the market.

Drivers

The European Commission’s December 2025 policy revision, replacing the hard 100% CO₂ reduction mandate for 2035 with a 90% threshold that permits continued ICE and hybrid vehicle sales, is the most consequential active driver restoring OEM and supplier confidence in long-dated engine platform investment. This change extends the commercial life of engine platforms in development by an estimated 5 to 10 years, making program economics viable at OEM board level again. A typical new passenger car engine family requires €400 to €900 million in development investment over 4 to 6 years, with viability dependent on a minimum 10 to 12 year post-production life. The revised target makes that threshold achievable, reactivating Tier-1 supplier order books across crankshaft, cylinder head, fuel injection, and thermal management component categories.

Rising commercial vehicle and two-wheeler production in India, Southeast Asia, and Africa further reinforces the engine market’s volume base. Hybrid vehicle platform proliferation across China, Europe, the United States, Japan, and South Korea sustains ICE engine content per electrified vehicle at approximately 40 to 65% of full ICE platform value per unit. The expanding global vehicle aftermarket, an aging global fleet, and TREM IV and BS6 Phase II compliance investment in India add further demand layers. ACEA estimates that each percentage point of European new vehicle sales retained on ICE or hybrid represents approximately 50,000 to 80,000 engine supply chain jobs, underlining the political durability of pro-ICE policy continuity.

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EU 2035 ICE Phase-Out Reversal Restoring Long-Horizon Engine Platform Investment Confidence | +1.2% | EU (all 27 member states), UK, Norway, cascading to global OEM platform planning | Short term (≤ 2 years) |

| Rising Commercial Vehicle & Two-Wheeler Production in India, Southeast Asia & Africa | +1.0% | India, Vietnam, Indonesia, Thailand, Nigeria, Kenya, Brazil | Short term (≤ 2 years) |

| Hybrid Vehicle Platform Proliferation Sustaining ICE Engine Content Per Electrified Vehicle | +0.9% | China, Europe, United States, Japan, South Korea | Short term (≤ 2 years) |

| Expanding Global Vehicle Aftermarket Driving Engine Replacement & Overhaul Demand | +0.7% | Global, led by India, China, Middle East, Sub-Saharan Africa, Latin America | Short term (≤ 2 years) |

| TREM IV & BS6 Phase II Emission Compliance Driving Engine Technology Upgrade Investment | +0.5% | India (off-highway, tractor & commercial vehicle segments) | Short term (≤ 2 years) |

| Aging Global Vehicle Fleet Sustaining ICE Engine Rebuild & Parts Demand | +0.4% | United States, EU, Middle East, Sub-Saharan Africa | Medium term (2–4 years) |

Restraints

The accelerating displacement of ICE vehicle sales by battery electric vehicles is the single most consequential structural restraint on the automotive engine market. Every vehicle sold as a pure-BEV removes an estimated $800 to $2,500 in engine system value from the supply chain, covering block assembly, cylinder head, fuel system, and thermal management content. China alone accounted for over 10 million pure-BEV units in 2024, a market where ICE engine content per new passenger car has structurally collapsed. Companies deriving 50 to 70% of revenue from passenger car ICE components in China and Europe face book-of-business erosion at rates of approximately 3 to 7% annually in BEV-penetrated segments.

The US 25% auto parts tariff inflates engine component import costs across global supply chains, compressing margins for OEMs and Tier-1 suppliers reliant on cross-border procurement. Euro 7 compliance, effective November 2026, adds engineering and validation CapEx that competes directly with engine technology investment budgets. Raw material cost inflation across steel, aluminum, and rare earths compounds margin pressure at every level of the engine supply chain. Suppliers who fail to absorb or pass through these cumulative cost pressures risk losing program competitiveness at OEM re-sourcing events, accelerating consolidation among mid-tier component manufacturers.

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| BEV Sales Penetration Structurally Eliminating Engine Content on Pure-Electric Platforms | -2.0% | China, Europe, United States, South Korea, Norway | Short term (≤ 2 years) |

| U.S. 25% Auto Parts Tariff Inflating Engine Component Import Costs Across Global Supply Chains | -1.3% | United States; cascading to Mexico, Japan, South Korea, Germany, Canada | Short term (≤ 2 years) |

| Euro 7 (November 2026) Engine Compliance CapEx Burden Compressing OEM R&D Budgets | -0.9% | EU, UK (aligned Euro 7 adoption from November 2026) | Short term (≤ 2 years) |

| Passenger Car Engine Volume Decline in Western Europe & China Due to Accelerating Electrification | -0.7% | Western Europe, China | Medium term (2–4 years) |

| High Raw Material & Forged Component Cost Inflation (Steel, Aluminum, Rare Earths) | -0.5% | Global — impacting all engine OEMs and Tier-1 component suppliers | Short term (≤ 2 years) |

Challenges

EU Regulation 2024/1257 (Euro 7) introduces two technically demanding compliance obligations for engine manufacturers. The first reduces the regulated particulate number size threshold from PN23 nm to PN10 nm, effectively mandating gasoline particulate filter fitment on virtually all gasoline engines and adding approximately €80 to €150 per vehicle in GPF hardware cost. The second doubles durability requirements from 100,000 km / 5 years to 200,000 km / 10 years, with Conformity Factor 1.0 applied on-road. Diesel engines face upgraded DPF specification costs of €40 to €90 per vehicle above Euro 6d levels.

These compliance obligations extend engine development cycles by an estimated 18 to 30 months and increase validation CapEx per program by approximately €30 to €80 million versus Euro 6 programs. OEMs facing the November 2026 type-approval deadline have pushed several mid-tier engine programs to Euro 6e carryover with late-cycle GPF integration, creating a second-wave compliance cost event in 2027 to 2028. This phased compliance pattern fragments OEM engineering budgets and creates a predictable cost spike that will pressure mid-tier suppliers less capable of absorbing multi-program validation investment simultaneously.

| Challenge | (~) % CAGR Friction Drag | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| Euro 7 PN10 & Extended Durability Compliance | -1.4% | EU, UK — all new M1/N1 engine types from November 2026 | Medium term (2–4 years) |

| ICE-Trained Engineering Talent Attrition | -1.1% | Global, most acute in Europe, United States, Japan | Long term (≥ 4 years) |

| Combustion Engine Supply Chain Consolidation Risks | -0.8% | Global, particularly Tier-2/3 forging, casting & machining supply chains | Medium term (2–4 years) |

| Thermal Efficiency Ceiling in Conventional ICE Architectures | -0.6% | Global — limits competitive positioning of ICE vs. hybrid and EV on total cost metrics | Long term (≥ 4 years) |

| OEM Engine Platform Rationalization & Shared-Architecture Cost Pressure | -0.4% | Global, particularly multi-brand OEM groups consolidating engine platforms | Medium term (2–4 years) |

Opportunities

Engine remanufacturing represents the largest structurally underexploited revenue opportunity for OEM engine manufacturers. The automotive remanufacturing market grew at approximately 9.9% CAGR through 2025 to 2026, yet OEM-branded certified remanufactured engine programs capture only an estimated 25 to 35% of engine rebuild volume, with the independent rebuilder channel holding 65 to 75%. Remanufactured engines require approximately 40 to 60% of the energy input and 15 to 25% of the raw material input of new production, while generating gross margins of an estimated 35 to 50% versus 20 to 28% on new engine equivalents. OEMs investing $20 to $80 million per engine family in certified remanufacturing infrastructure convert scrap-value cores into premium-margin revenue streams.

Hydrogen ICE development for heavy-duty and off-highway applications, range-extender and DHT engine modules for electrification-adjacent platforms, and off-highway engine market penetration under Tier 4 Final and Stage V compliance frameworks represent three additional high-potential opportunity vectors. Connected engine predictive maintenance and digital service SaaS models create recurring revenue streams that extend supplier relationships beyond the initial hardware sale. These opportunities are executable across medium and long-term horizons in the EU, US, Japan, South Korea, India, and Sub-Saharan Africa, rewarding suppliers who begin platform qualification and channel development ahead of mainstream adoption.

| Opportunity | (~) % Potential CAGR Upside | Geographic Relevance | Execution Window |

|---|---|---|---|

| Engine Remanufacturing & Circular Economy Rebuild Market Expansion | +1.5% | United States, EU, India, China, Middle East & Africa | Medium term (2–4 years) |

| Hydrogen Internal Combustion Engine (H2ICE) for Heavy-Duty & Off-Highway Applications | +1.2% | EU, Japan, South Korea, United States, India (heavy-duty road & off-highway) | Long term (≥ 4 years) |

| Electrification-Adjacent Engine Portfolio Expansion — Range-Extender & DHT Engine Modules | +0.9% | China, Europe, United States | Medium term (2–4 years) |

| Off-Highway & Agricultural Engine Market Penetration (Tier 4 Final & Stage V) | +0.7% | India, Southeast Asia, Sub-Saharan Africa, Latin America, Eastern Europe | Medium term (2–4 years) |

| Connected Engine Predictive Maintenance & Digital Service SaaS | +0.5% | United States, EU, China, India — fleet & commercial vehicle operators | Medium term (2–4 years) |

Key Company Insights

Toyota Motor Corporation holds a structural advantage across the hybrid-ICE transition through its decades-long investment in hybrid powertrain architecture, spanning mild, full, and plug-in hybrid configurations that retain combustion engine content across an electrifying passenger car fleet. Toyota’s hybrid systems are qualified across a wider model range than any other OEM, giving its engine supply chain partners durable volume as BEV penetration compresses pure-ICE program pipelines. As per our research, global EV sales are expected to exceed 20 million units in 2025, representing 25% of all new car sales. Toyota’s hybrid-dominant strategy positions it to capture the remaining 75% of the market where engine content is retained or partially retained per vehicle.

Volkswagen AG faces a more complex strategic position, having committed heavily to battery-electric platform development while simultaneously managing a large ICE and hybrid engine program portfolio across its multi-brand group structure. In April 2025, Garrett Motion presented its 3-in-1 E-Powertrain, E-Cooling Compressor, and hybrid-optimized boosting solutions at Auto Shanghai 2025, illustrating that Tier-1 suppliers are developing electrification-adjacent engine technologies specifically targeting OEM groups like Volkswagen that bridge ICE and BEV architectures. Volkswagen’s engine platform rationalization strategy reduces per-program supplier diversity but concentrates program risk, meaning suppliers who secure a position on a shared platform gain disproportionate volume while those excluded face abrupt revenue loss across the entire brand group.

Key Players

- Toyota Motor Corporation

- Volkswagen AG

- General Motors Company

- Ford Motor Company

- Hyundai Motor Company

- Honda Motor Co., Ltd.

- Stellantis N.V.

- BMW AG

- Mercedes-Benz Group AG

- Cummins Inc.

- Renault S.A.

- Daimler Truck AG

Recent Developments

- February 2025 – MAHLE Powertrain entered the testing phase of Project Cavendish, a £9.8 million UK government-funded project to convert existing heavy-duty truck engines to hydrogen combustion, advancing the H2ICE technology readiness level for commercial vehicle applications.

- September 2025 – DENSO signed an agreement to transfer its spark plug and exhaust gas sensor business to Niterra, covering key internal combustion engine components and signaling continued specialization and portfolio restructuring among major Tier-1 engine component suppliers.

- October 2025 – Cummins announced it would spotlight its new 4.5-liter structural engine at Agritechnica 2025, alongside the B6.7 and Next Gen X15 off-highway engines, reinforcing its position across the agricultural and off-highway engine segments under Tier 4 Final compliance frameworks.

- May 2026 – Rolls-Royce Power Systems began developing a hybrid haul-truck powertrain combining mtu diesel engines, batteries, and electric drive systems for the mining sector, opening a new application frontier for diesel engine integration within hybrid off-highway drivetrain architectures.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 121.94 Billion |

| Forecast Revenue (2035) | USD 162.04 Billion |

| CAGR (2026-2035) | 2.88% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Market Opportunity Analysis, Technology and Innovation Landscape, Competitive Landscape, Recent Developments |

| Segments Covered | By Engine Placement (In-Line Engine, V-Type Engine, W Engine, Boxer/Flat Engine); By Fuel Type (Gasoline/Petrol, Diesel, Hybrid-ICE (Mild, Full, Plug-in), Alternative Fuels (CNG, LPG, Ethanol), Hydrogen ICE); By Engine Capacity (Below 1.5L, 1.5L to 3.0L, Above 3.0L); By Vehicle Type (Passenger Cars, Light Commercial Vehicles (LCV), Heavy Commercial Vehicles (HCV), Two-Wheelers); By Sales Channel (OEM, Aftermarket) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East and Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | Toyota Motor Corporation, Volkswagen AG, General Motors Company, Ford Motor Company, Hyundai Motor Company, Honda Motor Co., Ltd., Stellantis N.V., BMW AG, Mercedes-Benz Group AG, Cummins Inc., Renault S.A., Daimler Truck AG |

| Customization Scope | Customization for segments, region/country-level will be provided. Additional customization can be done based on requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |