Quick Navigation

Report Overview

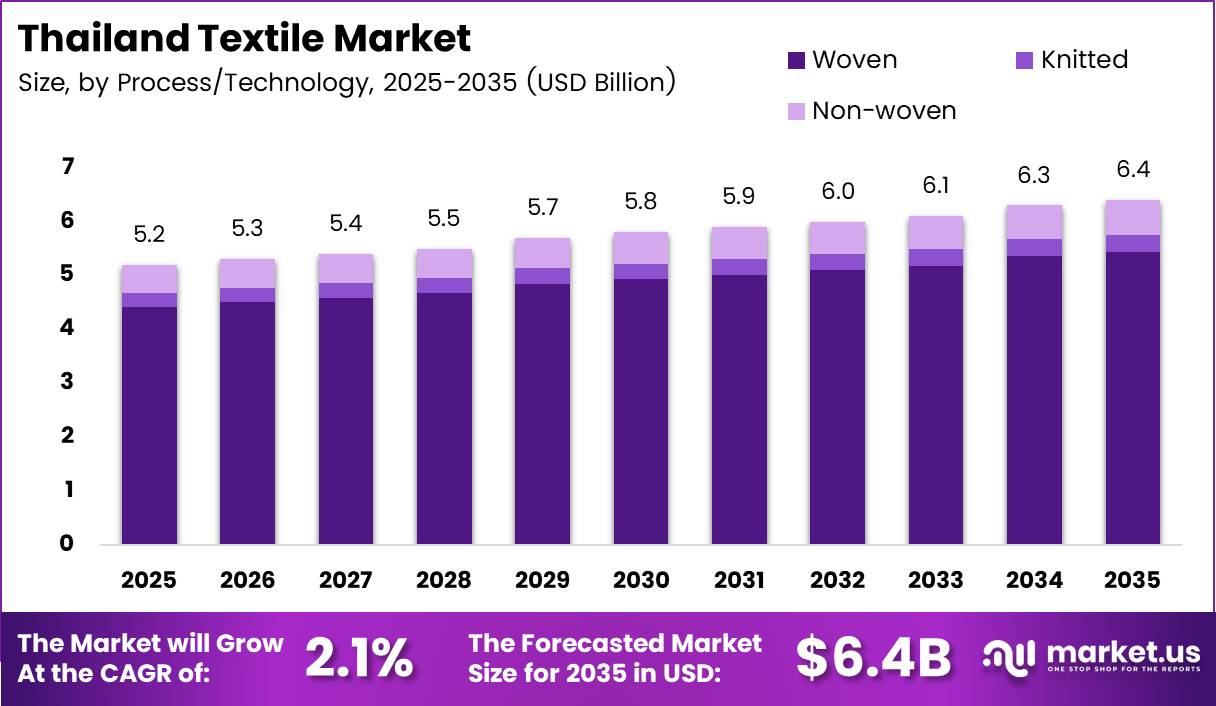

Thailand Textile Market size is expected to be worth around USD 6.4 Billion by 2035 from USD 5.2 Billion in 2025, growing at a CAGR of 2.1% during the forecast period 2026 to 2035.

Thailand’s textile sector operates as one of Southeast Asia’s most integrated manufacturing bases, spanning fiber processing, weaving, dyeing, finishing, and garment production within a single domestic supply chain. This vertical integration gives Thai producers a structural advantage over pure-assembly competitors in the region. The sector serves both domestic consumption and a well-established export network across North America, Europe, and Japan.

The market’s steady 2.1% CAGR reflects a sector in measured transition rather than stagnation. Thai manufacturers are moving up the value chain, shifting from commodity fabric production toward technical textiles, functional fabrics, and sustainable materials. This shift is deliberate. Lower-cost competitors in Bangladesh and Vietnam have captured volume business, pushing Thai producers toward higher-margin product categories where process capability matters more than labor cost.

Government policy reinforces this direction. Thailand’s industrial modernization programs actively support export competitiveness through investment incentives for advanced manufacturing equipment and energy efficiency upgrades. In March 2026, Lenzing expanded its VEOCEL™ lyocell fiber production at its Prachinburi, Thailand facility, marking the first production of nonwoven-grade lyocell fibers in Asia. This signals that Thailand is building the upstream fiber supply needed to support premium textile manufacturing at scale.

The sector’s structural transformation is visible in its workforce and establishment data. According to a Chulalongkorn University dataset used in 2025 policy planning, the number of active textile and garment establishments fell from 4,831 in 2018 to 2,355 in 2022, a decline of 51%. This consolidation means the remaining producers are larger, better-capitalized, and better positioned to invest in automation and process improvement.

Energy performance presents a parallel challenge. According to a 2025 analysis published on Academia.edu, Thailand’s textile industry energy intensity index was rising at an average of 0.86% per year under the business-as-usual baseline, meaning each unit of output requires progressively more energy without intervention. For export-focused manufacturers, this directly erodes cost competitiveness against buyers demanding lower Scope 3 emissions from their supply chains.

These two forces, consolidation and energy pressure, are reshaping investment priorities across the sector. Producers that respond with technology upgrades and sustainability credentials will retain access to premium export buyers. Those that do not will face further attrition. The 2.1% CAGR therefore masks a bifurcating market, with winners and laggards diverging sharply over the forecast period.

Key Takeaways

- The Thailand Textile Market was valued at USD 5.2 Billion in 2025 and is forecast to reach USD 6.4 Billion by 2035.

- The market grows at a CAGR of 2.1% during the forecast period 2026 to 2035.

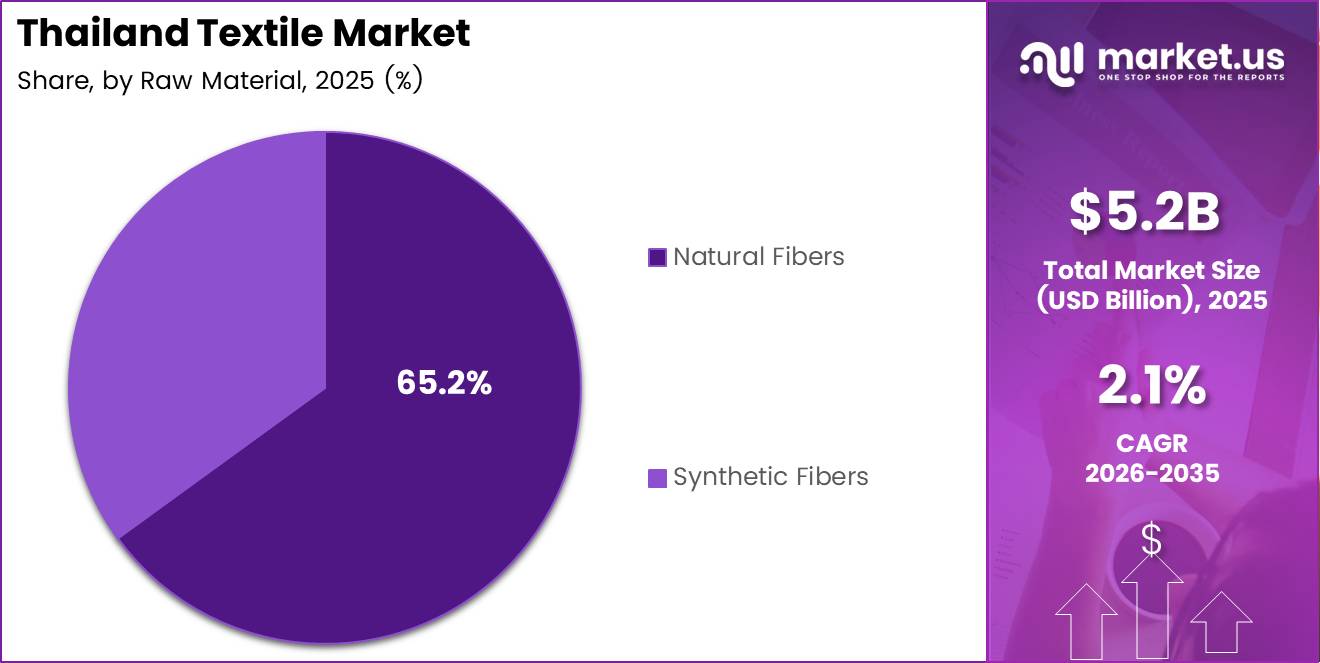

- By Raw Material, Natural Fibers holds the dominant position with a 65.2% market share in 2025.

- By Process/Technology, Woven leads with a 85.5% share, reflecting Thailand’s established weaving infrastructure.

- By Application, Fashion & Apparel commands the largest share at 65.6% in 2025.

- Active textile establishments declined by 51% from 4,831 in 2018 to 2,355 in 2022, signaling sector consolidation.

- Total textile and garment employment fell from 547,666 in 2018 to 360,098 in 2022, a reduction of 34%.

- Energy-efficiency retrofits in dyeing and finishing lines can reduce thermal energy use by 20–30%, per World Bank 2025 estimates.

- North America is the dominant export destination region for Thai textile manufacturers.

Raw Material Analysis

Natural Fibers dominates with 65.2% due to established cotton and silk supply chains.

In 2025, Natural Fibers held a dominant market position in the By Raw Material segment of the Thailand Textile Market, with a 65.2% share. Thailand’s long-standing expertise in cotton weaving and silk production underpins this dominance. According to the segmentation data, Cotton, Wool, and Silk collectively form the natural fiber base that international apparel buyers continue to prioritize for premium and mid-range product lines.

Synthetic Fibers represent the growth tier within Thai raw material consumption. Polyester, Nylon, Rayon/Viscose, Acrylic, and Polypropylene serve technical textile, automotive, and functional apparel applications where natural fibers lack the required performance specifications. Recycled Fibers within this sub-group are gaining traction as export buyers impose sustainability criteria on their sourcing decisions.

Recycled Fibers are the fastest-shifting sub-segment within the synthetic fiber category. In November 2025, Indorama Ventures formed a joint venture with Jiaren Chemical Recycling, targeting up to 100,000 tonnes of textile-recycled PET spinning capacity annually. This investment signals that recycled polyester is transitioning from a niche offering to a mainstream supply chain requirement for Thai manufacturers serving global brands.

Process/Technology Analysis

Woven dominates with 85.5% due to Thailand’s deep shuttleless loom infrastructure.

In 2025, Woven held a dominant market position in the By Process/Technology segment of the Thailand Textile Market, with a 85.5% share. Thailand’s weaving industry has invested consistently in shuttleless loom technology. According to Chulalongkorn University data used in 2025 policy planning, Thai plants upgrading from shuttle to shuttleless looms documented loom speeds rising from roughly 200 rpm to 550–650 rpm, translating to productivity gains of approximately 2.5–3.0 times per machine.

Knitted fabrics serve apparel applications where stretch, comfort, and fit are functional requirements. Sportswear, casual wear, and undergarment production rely on knit constructions that woven fabrics cannot replicate. Thailand’s knitting sector exports to brands requiring technical performance in their fabric base, making this a higher-margin niche within the broader process landscape.

Non-woven textiles cover a structurally distinct set of applications including medical, hygiene, filtration, and automotive end uses. Sub-processes within this category include Spunlaid (Spunbond/Melt-blown), Dry-laid Hydro-entangled, Wet-Laid, Needle-punched, and 3-D Weaving & Spacer Fabrics. Non-wovens represent the highest-growth process segment in Thailand, driven by medical procurement expansion and industrial demand.

Application Analysis

Fashion & Apparel dominates with 65.6% due to Thailand’s deep export apparel manufacturing base.

In 2025, Fashion & Apparel held a dominant market position in the By Application segment of the Thailand Textile Market, with a 65.6% share. Thailand’s apparel sector has supplied global retail brands for over three decades, building technical capability and compliance infrastructure that newer manufacturing locations have not yet matched. This long buyer-supplier history creates switching costs that protect Thai producers even as lower-wage alternatives exist regionally.

Industrial/Technical Textiles represent the application segment with the clearest growth trajectory over the forecast period. Automotive, filtration, construction, and defense end-uses require performance-certified fabrics that commodity textile producers cannot supply. Thai manufacturers with process capability and testing infrastructure are well-positioned to capture this demand as industrial buyers seek reliable Southeast Asian supply sources.

Household & Home Textiles serve retail buyers across bedding, upholstery, and decorative fabric categories. This segment benefits from Thailand’s established weaving capability and benefits when global brands diversify sourcing away from single-country dependence. Consistent quality standards and shorter lead times versus South Asian alternatives drive sustained buyer interest in Thai home textile producers.

Medical & Healthcare Textiles gained structural importance during and after the pandemic period, as hospitals and procurement agencies prioritized regional supply chain resilience. Non-woven substrates for masks, surgical drapes, and wound-care products use processes already present in Thailand’s manufacturing base. Expansion here requires certification investment but delivers significantly higher average selling prices than apparel fabrics.

Automotive & Transport Textiles connect directly to Thailand’s position as a major regional vehicle assembly hub. Seat fabrics, interior trim, sound insulation, and filtration components for Thai-assembled vehicles create captive demand for local textile suppliers. This proximity advantage reduces logistics cost and lead time, making domestic textile producers more competitive than import alternatives for automotive tier-1 suppliers.

Key Market Segments

By Raw Material

- Natural Fibers

- Cotton

- Wool

- Silk

- Synthetic Fibers

- Polyester

- Nylon

- Rayon/Viscose

- Acrylic

- Polypropylene

- Recycled Fibers

- Others

By Process/Technology

- Woven

- Knitted

- Non-woven

- Spunlaid (Spunbond/Melt-blown)

- Dry-laid Hydro-entangled

- Wet-Laid

- Needle-punched

- 3-D Weaving & Spacer Fabrics

By Application

- Fashion & Apparel

- Industrial/Technical Textiles

- Household & Home Textiles

- Medical & Healthcare Textiles

- Automotive & Transport Textiles

- Others

Drivers

Integrated Export Manufacturing Infrastructure and Global Brand Sourcing Create Sustained Demand for Thai Textiles

Thailand’s textile sector benefits from one of the most complete production chains in Southeast Asia, running from fiber processing through to finished garment export. This end-to-end capability reduces lead times and quality variability for international buyers. Global apparel brands sourcing from the region consistently rate supply chain reliability as a top vendor selection criterion, and Thailand scores strongly on this measure.

Government investment in industrial modernization directly supports the export competitiveness of Thai textile producers. Incentives for equipment upgrades, export facilitation programs, and trade agreements with key buyer markets in Europe and North America reduce the cost gap between Thailand and lower-wage competitors. In May 2025, Indorama Ventures expanded its deja™ sustainable textile portfolio with PET fibers manufactured from discarded textile waste, demonstrating that Thai-linked producers are actively building sustainability credentials to retain premium export buyers.

According to a Chulalongkorn University dataset used directly in 2025 industrial policy planning, total employment in the textile and garment sector fell from 547,666 workers in 2018 to 360,098 in 2022, a reduction of 34%. This labor contraction reflects accelerated automation investment across surviving mills. Fewer workers producing similar or greater output means Thai textile firms are building the productivity base needed to compete on value rather than headcount.

Restraints

Cost Pressure from Lower-Wage Competitors and Import Dependence Constrain Margin Recovery for Thai Producers

Bangladesh, Vietnam, and Cambodia offer labor cost structures that Thai textile producers cannot match for volume commodity production. International brands with cost-first sourcing mandates consistently allocate high-volume, low-complexity orders to these lower-cost destinations. Thai manufacturers that have not moved up the value chain face direct margin compression on every standard fabric category they produce.

Raw material dependence compounds the competitive pressure. Certain specialized textile segments in Thailand rely on imported fibers, dyes, and specialty chemicals that domestic suppliers do not produce at sufficient scale or specification. This import exposure creates two problems. Input costs fluctuate with currency and global commodity movements, and supply disruptions during logistics crises can interrupt production schedules for export-committed buyers.

The sector consolidation data illustrates how severe this dual pressure has become. The number of active establishments fell from 4,831 in 2018 to 2,355 in 2022, a 51% decline within four years. Many of the businesses that exited were small and mid-sized mills unable to absorb technology investment costs or weather raw material price volatility. The survivors are stronger, but the consolidation itself signals that restraining forces are real and structural rather than cyclical.

Growth Factors

Technical Textile Expansion, FDI Inflows, and Sustainability Investment Define Thailand’s Next Revenue Layer

Technical textile production for automotive, medical, and industrial applications represents the clearest path to higher revenue per unit of output for Thai manufacturers. Thailand’s vehicle assembly industry creates captive demand for seat fabrics, filtration media, and acoustic materials within domestic supply chains. Medical procurement growth creates parallel demand for certified non-woven substrates. Both segments require process capability that new entrant competitors lack.

Foreign direct investment is actively building this capability. In May 2026, Toray Industries and PTT Global Chemical announced progress on a 100% bio-based nylon 66 textile supply chain, advancing commercialization plans for sustainable textile materials derived from cassava pulp residues. This collaboration connects Thailand’s agricultural feedstock base directly to premium synthetic fiber production, opening a new materials category that neither conventional polyester nor natural fiber producers currently serve.

According to a 2025 World Bank technical decarbonization report, energy-efficiency retrofit packages for dyeing and finishing lines in Thailand can cut specific thermal energy use by 20–30% and electricity use by 10–15%, with payback periods between 3 and 6 years for most technologies. This payback profile is commercially viable for mid-sized exporters. Producers that complete these retrofits reduce operating costs while simultaneously meeting the sustainability reporting requirements that European and North American buyers are imposing on their supply chains.

Emerging Trends

Automation, Recycled Material Adoption, and Circular Textile Models Are Reshaping Thailand’s Production Landscape

Automated sewing and digital manufacturing technologies are entering Thai textile mills as the labor pool contracts and wage expectations rise. The productivity data from weaving is instructive. Upgrades from shuttle to shuttleless looms delivered speed gains from roughly 200 rpm to 550–650 rpm, a factor of 2.5–3.0 times per machine. Similar step-change improvements are now available across cutting, sewing, and inspection stages as equipment costs decline.

Recycled polyester is transitioning from a buyer preference to a supply chain requirement across major apparel categories. According to a 2025 World Bank case analysis, Thai textile mills replacing conventional jet dyeing machines with low-liquor-ratio models reduced water consumption by 30–40% per kilogram of fabric and shortened batch processing time by 15–25%. These operational improvements make recycled fiber processing commercially competitive with virgin polyester production at scale.

Circular textile production infrastructure is consolidating around Thailand. The Indorama Ventures joint venture with Jiaren Chemical Recycling targets 100,000 tonnes annually of textile-recycled PET spinning capacity for global markets. This volume positions Thailand-linked producers to supply certified recycled content at the scale that international brands need for product-line commitments, rather than limited pilot collections. Early-mover Thai manufacturers that integrate into these supply chains will hold certification and traceability advantages over slower competitors.

Key Company Insights

Thanulux PCL operates as one of Thailand’s most vertically integrated textile manufacturers, with production spanning spinning, weaving, and finished garment output. This integration allows the company to control quality and cost across the full production chain, a structural advantage when export buyers demand consistent specifications across large order volumes. Thanulux’s domestic scale positions it to absorb capital investment in automation without the financial pressure facing smaller competitors.

Textile Prestige PCL has built its market position around export-oriented woven fabric production for international apparel brands. The company’s sustained focus on fabric quality and buyer compliance requirements has created long-term relationships with European and North American customers that generate recurring order flow. This buyer concentration is both a strength and a risk, as it limits revenue diversification if any major customer shifts sourcing strategy.

Nan Yang Textile Group operates across multiple textile product categories, serving both domestic and export markets with a broad fabric portfolio. The company’s multi-category presence provides revenue diversification that single-segment competitors lack. This breadth allows Nan Yang to reallocate production capacity between segments as demand patterns shift, reducing the exposure to any single application’s cyclical or structural decline.

Thai Textile Industry PCL focuses on fabric manufacturing for the domestic apparel and retail sectors, providing a demand buffer during periods when global export markets tighten. The company’s domestic orientation means it faces different competitive dynamics than export-focused peers. However, it also means it is more exposed to Thai consumer spending cycles and less positioned to capture the sustainability-linked premium pricing that international buyers are now willing to pay for certified textile products.

Key Players

- Thanulux PCL

- Textile Prestige PCL

- Nan Yang Textile Group

- Thai Textile Industry PCL

- Erawan Textile Co Ltd

- Luckytex (Thailand) PCL

- High-Tech Apparel Co Ltd

- Hong Seng Knitting Co Ltd

- Thai Toray Textile Mills PCL

Recent Developments

- July 2024 – Indorama Ventures secured a USD 200 million loan from the International Finance Corporation (IFC) to expand sustainability initiatives, including PET recycling projects and recycling facility enhancements in Thailand.

- November 2025 – Indorama Ventures formed a joint venture with Jiaren Chemical Recycling to accelerate textile circularity, targeting up to 100,000 tonnes of textile-recycled PET spinning capacity annually for the global textile industry.

- August 2024 – Indorama Ventures joined the T-REX (Textile Recycling Excellence) Project, a major European textile recycling initiative focused on developing a closed-loop textile-to-textile supply chain infrastructure.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 5.2 Billion |

| Forecast Revenue (2035) | USD 6.4 Billion |

| CAGR (2026-2035) | 2.1% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Raw Material (Natural Fibers, Synthetic Fibers), By Process/Technology (Woven, Knitted, Non-woven), By Application (Fashion & Apparel, Industrial/Technical Textiles, Household & Home Textiles, Medical & Healthcare Textiles, Automotive & Transport Textiles, Others) |

| Competitive Landscape | Thanulux PCL, Textile Prestige PCL, Nan Yang Textile Group, Thai Textile Industry PCL, Erawan Textile Co Ltd, Luckytex (Thailand) PCL, High-Tech Apparel Co Ltd, Hong Seng Knitting Co Ltd, Thai Toray Textile Mills PCL |

| Customization Scope | Customization for segments will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |