Telecom Mobile Network Optimization (MNO) Market By Component (Solutions/Platforms, Services (Managed Services, Professional Services)), By Deployment Mode (Cloud-based, On-Premises), By Optimization Type (Radio Access Network (RAN) Optimization, Core Network Optimization, Transport Network Optimization, Others), By Network Technology (2G/3G, 4G/LTE, 5G), By Regional Analysis, Global Trends and Opportunity, Future Outlook By 2026-2035

The Global Telecom Mobile Network Optimization (MNO) Market generated USD 9.6 billion in 2025 and is predicted to register growth from USD 10.5 billion in 2026 to about USD 23.2 billion by 2035, recording a CAGR of 9.2% throughout the forecast span. In 2025, Asia Pacific held a dominant market position, capturing more than a 40.2% share, holding USD 3.87 Billion revenue.

Top Keytake away

Component Services account for 54.3% of the Telecom Mobile Network Optimization (MNO) market, as operators rely heavily on expert service providers for planning, optimization, and performance tuning of their networks.

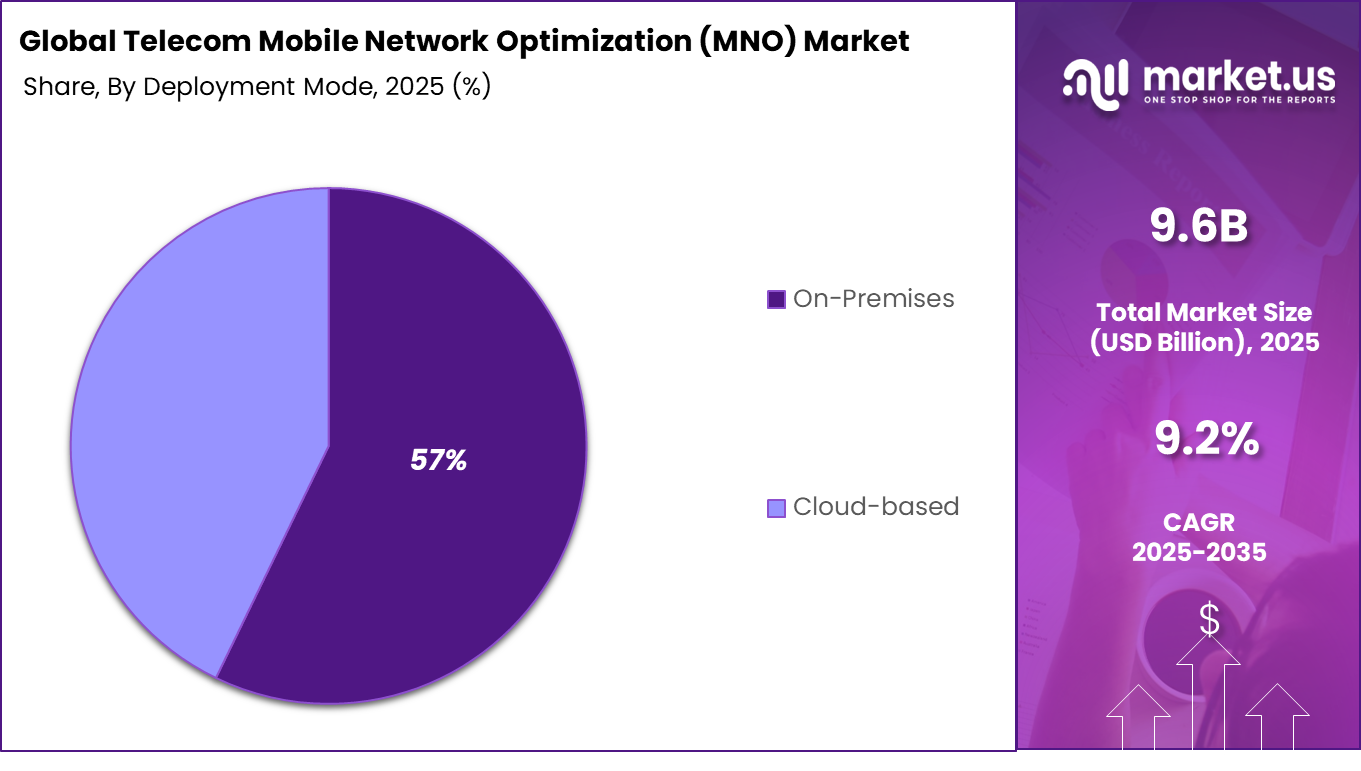

Deployment Mode On-premises holds 57.2% of the market, because many telecom operators prefer to keep optimization tools and analytics platforms within their own infrastructure for better control and data security.

Optimization Type Radio Access Network (RAN) optimization represents 62.4%, reflecting the strong focus on improving coverage, capacity, and user experience at the radio layer where most performance issues arise.

Network Technology 4G/LTE accounts for 56.3% of the market, since 4G networks still carry a large share of global mobile traffic and require ongoing optimization alongside newer 5G deployments.

Region Asia-Pacific represents 40.2% of the global market, driven by high mobile data usage, dense urban deployments, and continuous network upgrades in major countries.

Country China’s market is valued at 1.18 billion and is expected to grow at a CAGR of 5.3%, supported by large-scale operator investments in optimizing nationwide 4G/LTE and evolving 5G networks.

Telecom mobile network optimization focuses on improving the performance, capacity, and efficiency of mobile networks to deliver better service quality to users. It involves analyzing network data, adjusting configurations, and managing traffic to ensure stable connectivity, faster data speeds, and reduced congestion. As mobile networks become more complex with multiple technologies and dense deployments, optimization has become an ongoing process rather than a one time setup. Operators rely on these solutions to maintain consistent performance across urban, suburban, and rural environments.

One of the main driving factors is the rapid growth in mobile data usage driven by video streaming, cloud applications, online gaming, and connected devices. This increase in traffic creates pressure on networks to deliver high performance without interruptions. In addition, the rollout of advanced mobile technologies is increasing network complexity, requiring continuous tuning and monitoring. Operators are also focusing on improving user experience by reducing dropped calls, improving coverage, and maintaining consistent speeds. The shift toward automated and data driven network management is further supporting the use of advanced optimization tools.

Demand for mobile network optimization solutions is rising as telecom operators seek to improve efficiency while managing expanding network infrastructure. There is a strong preference for solutions that provide real time insights, predictive analysis, and automated adjustments to network parameters.

Operators are also looking for systems that can integrate with existing network management platforms and support multiple technologies. The demand is particularly strong in regions with high smartphone usage and dense network deployments where performance expectations are higher. As mobile connectivity continues to grow in importance, the need for reliable and intelligent network optimization solutions is expected to increase steadily.

Drivers Impact Analysis

Key Driver

Impact on CAGR Forecast (~%)

Geographic Relevance

Impact Timeline

Additional Insight

Rapid growth in mobile data traffic and network congestion

+3.3%

Asia Pacific, North America, Europe

Short to medium term

Higher traffic drives need for optimization

Expansion of 4G and 5G network deployments

+3.0%

Asia Pacific, Europe, North America

Medium term

New networks require continuous tuning

Increasing demand for improved network quality and user experience

+2.7%

Global

Medium term

Operators focus on reducing latency and drops

Rising adoption of cloud-native and virtualized network functions

+2.4%

Global

Medium to long term

Virtual networks need advanced optimization tools

Growth of smart devices and IoT connectivity

+2.1%

Global

Medium to long term

More connected devices increase network load

Restraints Impact Analysis

Key Restraint

Impact on CAGR Forecast (~%)

Geographic Relevance

Impact Timeline

Additional Insight

High cost of network optimization tools and deployment

-2.6%

Emerging markets

Short to medium term

Cost limits adoption for smaller operators

Complexity in managing multi-vendor network environments

-2.3%

Global

Medium term

Integration challenges slow implementation

Data privacy and regulatory constraints

-2.0%

Europe, Asia Pacific

Medium to long term

Regulations restrict data-driven optimization

Dependence on telecom operator investment cycles

-1.7%

Global

Medium term

Budget constraints delay upgrades

Limited skilled workforce for advanced network analytics

-1.5%

Global

Long term

Skill gaps affect effective use

By Component Analysis

The services segment accounted for 54.3% of the market share, reflecting its strong role in supporting network assessment, deployment, tuning, and continuous optimization activities. This dominance is supported by the need for specialized expertise to manage complex mobile networks and ensure consistent performance. Operators rely on service providers to improve coverage, reduce congestion, and maintain service quality across evolving network environments.

Another factor driving this segment is the increasing complexity of telecom infrastructure with multi-layered technologies and high data traffic. Service-based models help operators adapt quickly to changing network conditions and implement optimization strategies without large internal resource investments. This continues to strengthen demand for optimization services.

By Deployment Mode Analysis

The on-premises segment held 57% share, driven by the need for greater control over network data, performance monitoring, and system customization. Telecom operators prefer on-premises deployment to manage sensitive operational data within their own infrastructure and ensure low-latency processing. This approach supports real-time decision-making and stable system performance.

In addition, on-premises solutions allow deeper integration with existing network management systems and infrastructure. Operators benefit from enhanced security, reliability, and direct control over updates and configurations. These advantages have supported continued adoption of on-premises deployment models.

By Optimization Type Analysis

The radio access network optimization segment captured 62.4% of the market, reflecting its critical role in improving signal quality, coverage, and user experience at the network edge. RAN optimization focuses on enhancing performance between user devices and base stations, which directly impacts service reliability and speed. This makes it a key priority for telecom operators.

Furthermore, the rapid growth in mobile data usage and connected devices has increased pressure on access networks. Operators are investing in advanced RAN optimization tools to manage traffic loads, reduce interference, and maintain network efficiency. This has reinforced the leading position of this segment.

By Network Technology Analysis

The 4G LTE segment accounted for 56.3% of the market share, driven by its widespread deployment and continued reliance for mobile connectivity. Despite the emergence of newer technologies, 4G networks still carry a large portion of global mobile traffic. Optimization efforts remain focused on maintaining and enhancing performance within these networks.

Moreover, many regions continue to expand and upgrade existing 4G infrastructure to meet growing demand. Telecom operators are prioritizing optimization solutions to improve network capacity, reduce latency, and ensure consistent service delivery. This ongoing reliance has strengthened the position of 4G LTE in the market.

Investor Type Impact Analysis

Investor Type

Growth Sensitivity

Risk Exposure

Geographic Focus

Investment Outlook

Venture capital firms

Moderate to high

High

Asia Pacific, US

Investing in network analytics startups

Private equity firms

Moderate

Moderate

North America and Asia Pacific

Scaling telecom software providers

Corporate investors

High

Moderate

Global

Strategic investments in telecom infrastructure

Institutional investors

Moderate

Low to moderate

Developed markets

Prefer stable telecom technology firms

Government and public funding bodies

Moderate to high

Low

Global

Supporting digital connectivity expansion

Technology Enablement Analysis

Technology

Impact on CAGR Forecast (~%)

Geographic Relevance

Impact Timeline

Additional Insight

AI-driven network optimization and self-organizing networks

+3.6%

Asia Pacific, US, Europe

Medium to long term

Automates performance tuning

Cloud-native network optimization platforms

+3.1%

Global

Medium term

Enables scalable operations

Big data analytics for network performance monitoring

+2.8%

Global

Medium term

Improves decision-making

Edge computing integration for real-time optimization

+2.5%

Global

Medium to long term

Reduces latency at the edge

Automation and orchestration tools for network management

+2.2%

Global

Medium term

Simplifies network operations

Key Challeneges

High cost of network optimization tools and services.

Complex integration with existing telecom network systems.

Managing large volumes of network data is difficult.

Need for skilled professionals for analysis and optimization.

Performance issues in dense and high-traffic network areas.

Compatibility issues across different network equipment vendors.

Security risks in handling network data and operations.

Dependence on accurate real-time data for better optimization.

Regulatory requirements can slow network improvements.

Emerging Trends

The telecom mobile network optimization market is evolving toward more intelligent and automated performance management systems that can handle increasing network complexity. One of the key emerging trends is the use of AI driven self optimizing networks that continuously monitor traffic patterns, detect issues, and adjust network parameters in real time without manual intervention. This is helping improve service quality and reduce operational effort.

Another important trend is the integration of analytics platforms that provide deep insights into user behavior, network congestion, and service performance, allowing operators to make faster and more accurate decisions. There is also growing adoption of cloud native optimization tools that support flexible deployment and easier scaling across different network environments. In addition, the expansion of edge computing is influencing optimization strategies, as data processing moves closer to end users to reduce latency. Automation in fault detection and predictive maintenance is also gaining traction, helping prevent network disruptions before they impact users.

Growth Factors

The growth of this market is driven by the rapid increase in mobile data consumption and the need to deliver consistent network performance. As users demand faster speeds and reliable connectivity for applications such as streaming, gaming, and remote work, operators are focusing on optimizing network efficiency. The rollout of advanced mobile technologies is also increasing the complexity of network management, creating demand for sophisticated optimization solutions.

Another major factor is the need to reduce operational costs while maintaining high service standards, which is encouraging the use of automated tools. Operators are also aiming to improve customer experience and reduce service complaints, further supporting adoption. Additionally, the growing number of connected devices and applications is putting pressure on network capacity, making optimization solutions essential for maintaining smooth and efficient communication services.

Key Market Segments

By Component

Solutions/Platforms

Services

Managed Services

Professional Services

By Deployment Mode

Cloud-based

On-Premises

By Optimization Type

Radio Access Network (RAN) Optimization

Core Network Optimization

Transport Network Optimization

Others

By Network Technology

2G/3G

4G/LTE

5G

Regional Analysis

Asia Pacific accounted for 40.2% of the Telecom Mobile Network Optimization (MNO) market, supported by rapid expansion of mobile networks and increasing data traffic across the region. The growing number of smartphone users and rising consumption of video, gaming, and digital services are pushing telecom operators to improve network performance and efficiency. Optimization solutions are widely adopted to enhance coverage, reduce latency, and manage network congestion. In addition, continuous rollout of advanced wireless technologies and expansion of telecom infrastructure are strengthening demand for network optimization tools across the region.

China market reached USD 1.18 Billion and is projected to grow at a CAGR of 5.3%, driven by large-scale telecom operations and ongoing network upgrades. Operators are investing in optimization solutions to improve service quality, support high user density, and manage increasing data usage. The demand is also supported by the need to maintain stable connectivity across urban and rural areas. In addition, increasing focus on efficient spectrum utilization and network performance improvement is expected to support steady growth of the market in China over the coming years.

Key Regions and Countries

North America

US

Canada

Europe

Germany

France

The UK

Spain

Italy

Russia

Netherlands

Rest of Europe

Asia Pacific

China

Japan

South Korea

India

Australia

Singapore

Thailand

Vietnam

Rest of APAC

Latin America

Brazil

Mexico

Rest of Latin America

Middle East & Africa

South Africa

Saudi Arabia

UAE

Rest of MEA

Competitive Analysis

The competitive landscape of the 5G Smartphone Antenna Tuner Market is driven by leading semiconductor and RF component manufacturers. Companies such as Qorvo, Skyworks Solutions, Murata Manufacturing, TDK Corporation, STMicroelectronics, Analog Devices, Infineon Technologies, and NXP Semiconductors focus on advanced RF tuning solutions that improve signal performance and power efficiency in 5G smartphones.

These players invest in miniaturization, integration of multiple frequency bands, and high-speed switching technologies to support complex 5G network requirements. Their strong relationships with smartphone manufacturers and global supply chains help them maintain a leading position in the market.

At the same time, companies such as Johanson Technology, Psemi (formerly Peregrine Semiconductor), Taoglas, TE Connectivity, Amphenol Corporation, Antenova, Yageo Corporation, AVX Corporation, Vishay Intertechnology, Molex (a Koch company), Sunlord Electronics, and Pulse Electronics compete by offering specialized antenna components, passive devices, and customized RF solutions.

These players focus on compact designs, cost efficiency, and support for multi-band connectivity. Competition in this market is driven by demand for better signal quality, reduced power consumption, and the ability to deliver high-performance antenna tuning solutions for next-generation mobile devices.

The future outlook for the Telecom Mobile Network Optimization (MNO) Market looks strong as telecom operators continue to focus on improving network performance and user experience. The market is expected to grow with rising data traffic, increasing smartphone usage, and the expansion of 5G networks. Operators are anticipated to invest in advanced optimization tools to manage network congestion, improve coverage, and reduce latency. In the coming years, the use of AI, automation, and cloud-based solutions is expected to enhance real-time network management, making mobile network optimization more efficient and essential for modern telecom systems.

Recent Developments

February 2026, AT&T – AT&T is highlighted in MNO market reports as one of the largest global operators investing heavily in 5G RAN optimization, self‑optimizing networks (SON), and traffic‑management tools to keep QoE high as mobile‑data use soars.

February 2026, Vodafone – Vodafone is cited as a major European MNO focusing on RAN sharing, Open RAN, and AI‑driven optimization to cut costs and improve coverage and capacity across Europe and emerging markets.

Report Scope

Report Features

Description

Market Value (2025)

USD 9.6 Billion

Forecast Revenue (2035)

USD 23.2 Billion

CAGR(2025-2035)

9.2%

Base Year for Estimation

2024

Historic Period

2020-2024

Forecast Period

2026-2035

Report Coverage

Revenue forecast, AI impact on Market trends, Share Insights, Company ranking, competitive landscape, Recent Developments, Market Dynamics and Emerging Trends

Segments Covered

By Component (Solutions/Platforms, Services (Managed Services, Professional Services)), By Deployment Mode (Cloud-based, On-Premises), By Optimization Type (Radio Access Network (RAN) Optimization, Core Network Optimization, Transport Network Optimization, Others), By Network Technology (2G/3G, 4G/LTE, 5G)

Regional Analysis

North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Latin America; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA

Competitive Landscape

Siemens AG, Rockwell Automation Inc., Schneider Electric SE, Mitsubishi Electric Corporation, ABB Ltd., Omron Corporation, Emerson Electric Co., Honeywell International Inc., Beckhoff Automation GmbH & Co. KG, Delta Electronics Inc., Bosch Rexroth AG, Panasonic Holdings Corporation, Fuji Electric Co. Ltd., Hitachi Ltd., IDEC Corporation, Keyence Corporation, Toshiba Corporation, General Electric Company, Parker Hannifin Corporation, Eaton Corporation plc, Yokogawa Electric Corporation, Inovance Technology Co. Ltd., Hollysys Automation Technologies Ltd., WAGO Kontakttechnik GmbH & Co. KG, B&R Industrial Automation GmbH, Others

Customization Scope

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements.

Purchase Options

We have three license to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)

Market")