Global Telecom Edge Load Balancer Market Size, Share, Growth Analysis By Component (Hardware, Software, Services), By Deployment Mode (On-Premises, Cloud, Hybrid), By Application (Network Function Virtualization, Content Delivery Networks, IoT, 5G Networks, Others), By End-User (Telecom Operators, Enterprises, Data Centers, Others), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2025-2035

- Published date: Mar 2026

- Report ID: 181859

- Number of Pages: 291

- Format:

-

keyboard_arrow_up

Quick Navigation

- Report Overview

- Core Key Insights

- Market Outlook

- Future Predictions

- Key Market Segments

- Research-Based Segments

- By Component

- By Deployment Mode

- By Application

- By End-User

- Regional Analysis

- US Market Size

- Driving Factors

- Restraint Factors

- Growth Opportunities

- Trending Factors

- Competitive Analysis

- Recent Developments

- Report Scope

Report Overview

The Telecom Edge Load Balancer Market is expanding rapidly as telecom operators and network providers focus on improving network performance, reducing latency, and supporting the growing demand for real time digital services.

Edge load balancers play a critical role in distributing network traffic efficiently across edge computing environments, ensuring faster data processing and improved user experience. These solutions are widely used in 5G networks, content delivery systems, IoT deployments, and cloud-based telecom infrastructure, where high speed and reliability are essential.

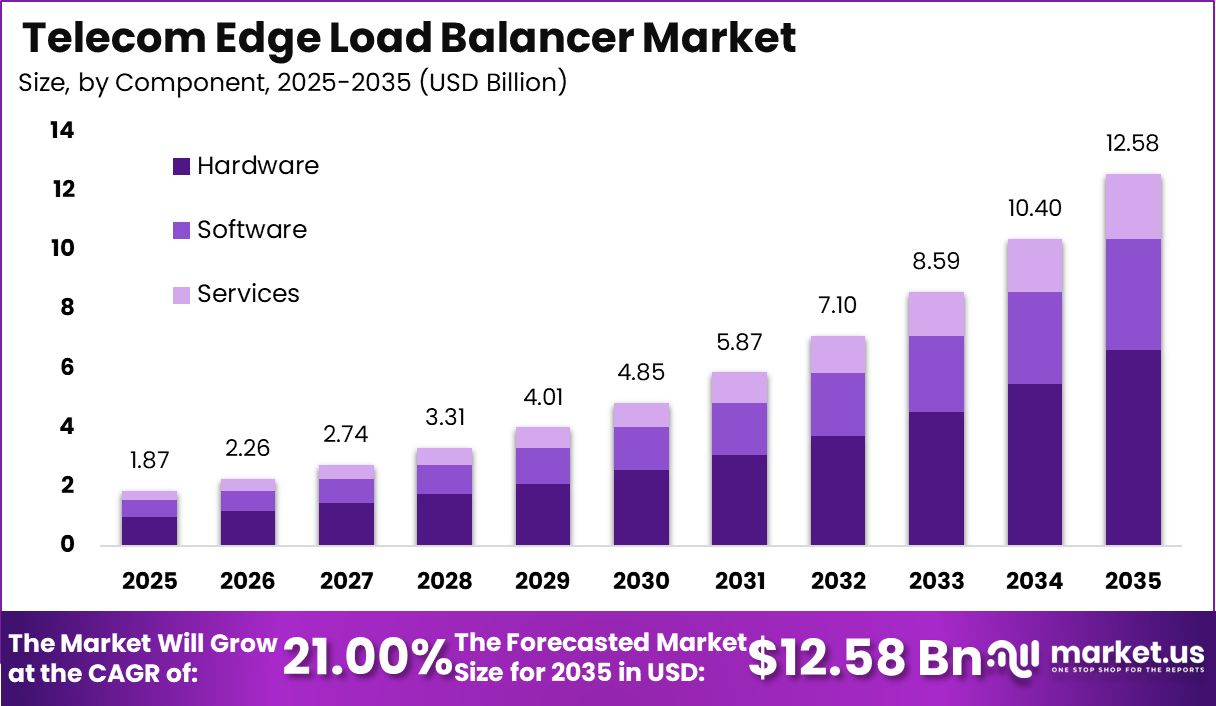

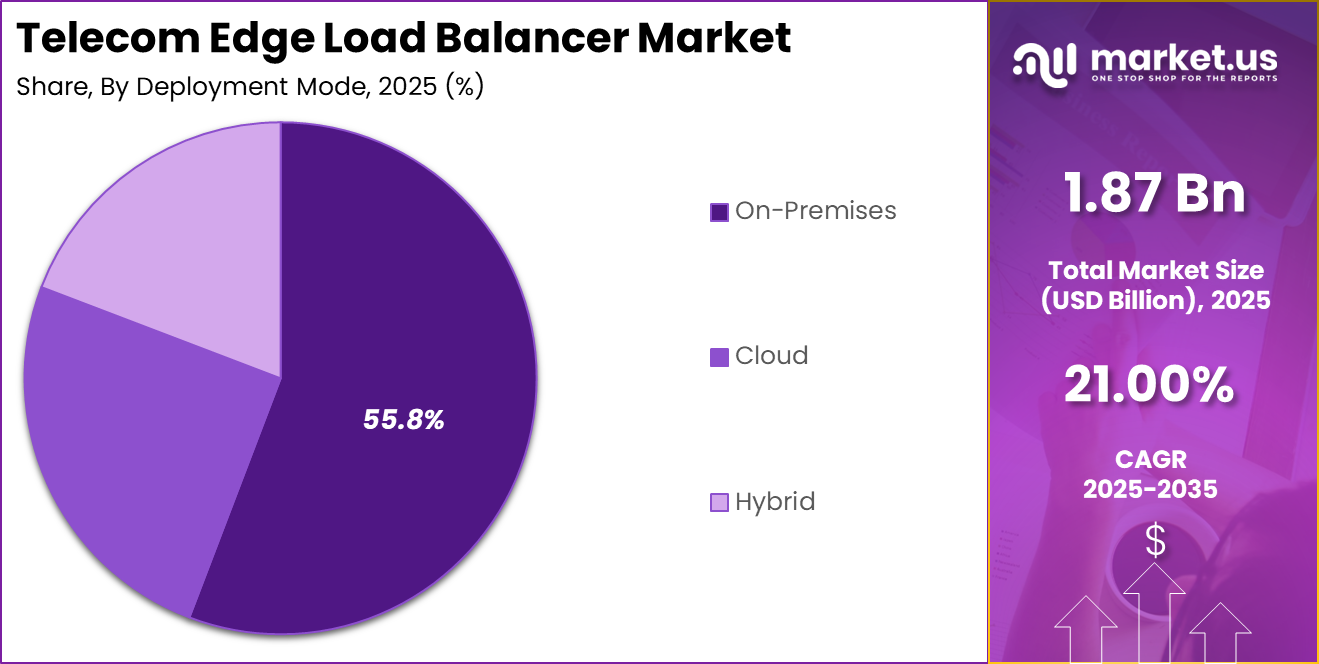

In 2025, the global Telecom Edge Load Balancer Market is valued at approximately USD 1.87 billion. The market is expected to grow at a strong compound annual growth rate of 21.00%, reaching an estimated value of around USD 12.58 billion by 2035. This growth is driven by the rapid deployment of 5G networks, increasing data traffic, and the rising adoption of edge computing technologies across telecom ecosystems.

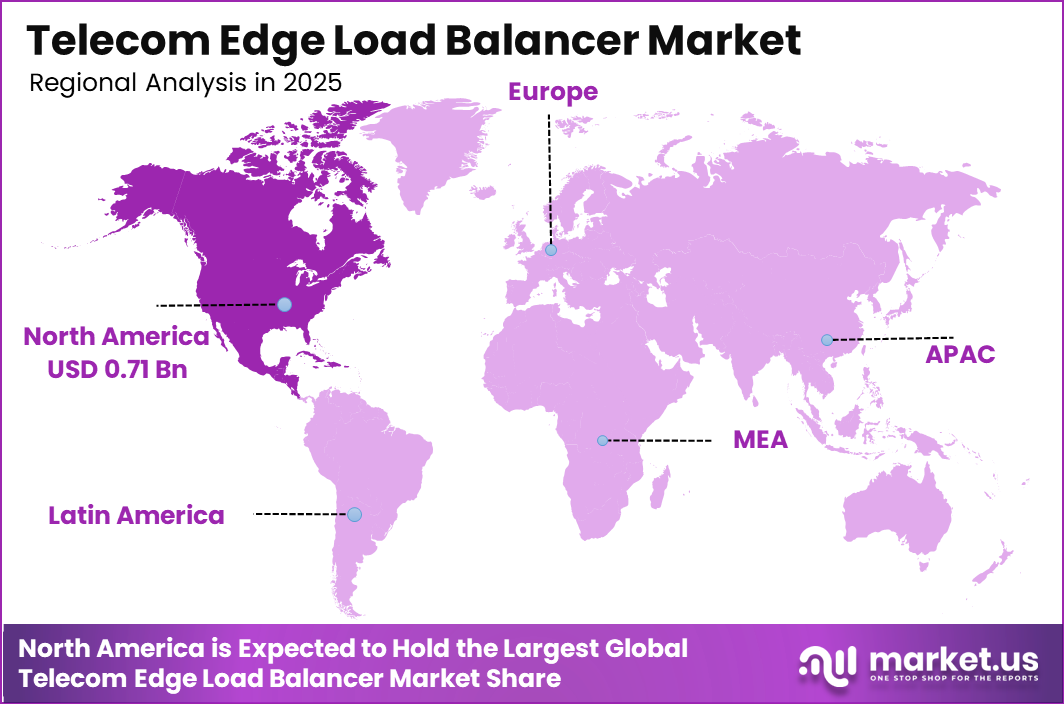

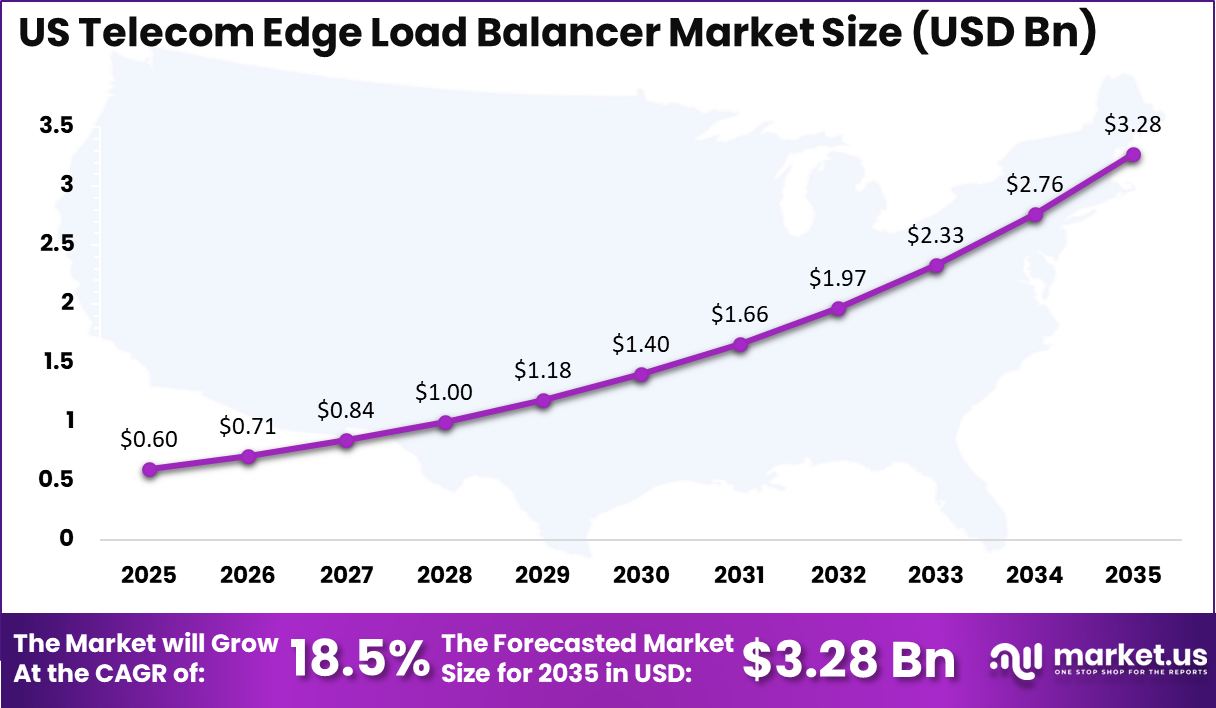

North America leads the market with a share of 38.1%, generating about USD 0.71 billion in revenue in 2025. The United States accounts for approximately USD 0.60 billion of this value, supported by advanced telecom infrastructure and early adoption of next-generation network technologies. The US market is projected to grow at a CAGR of 18.5% during the forecast period, driven by continuous investments in 5G expansion, cloud integration, and edge network optimization.

The growth of telecom edge load balancing solutions is closely linked to the rapid expansion of mobile data traffic and edge computing adoption. According to Ericsson, global mobile data traffic exceeded 130 exabytes per month in 2023 and is expected to continue increasing as video streaming, cloud gaming, and real-time applications gain popularity.

This surge in data requires efficient traffic distribution at the network edge to reduce congestion and latency. At the same time, the number of connected IoT devices is rising significantly, with estimates from the International Telecommunication Union indicating that there are more than 15 billion connected devices worldwide, many of which rely on low-latency edge networks.

The rollout of 5G networks is another major factor supporting demand. The GSM Association reported that global 5G connections surpassed 1.5 billion in 2023, with continued expansion expected across regions. These networks require advanced load balancing to manage high volumes of simultaneous connections.

In addition, Cisco has projected that more than 75% of data will be processed outside traditional centralized data centers, highlighting the shift toward edge computing. This trend is increasing the need for telecom edge load balancers to ensure efficient data routing, improve network reliability, and support real-time digital services.

Core Key Insights

- The Telecom Edge Load Balancer Market reached a value of USD 1.87 billion in 2025, reflecting strong demand for low-latency network traffic management.

- The market is projected to grow at a CAGR of 21.00% during the forecast period.

- By 2035, the global market value is expected to reach USD 12.58 billion.

- North America accounted for the leading regional share of 38.1% in 2025.

- The North American market size reached approximately USD 0.71 billion in 2025.

- The United States generated around USD 0.60 billion in revenue in 2025.

- The US market is expected to grow at a CAGR of 18.5% during the forecast period.

- By component, hardware solutions held a dominant share of 52.6%.

- By deployment mode, on-premises solutions accounted for 55.8% of the market.

- By application, network function virtualization represented 40.7% of the market demand.

- By end user, telecom operators led with a share of 57.8% due to high network traffic management needs.

Market Outlook

The outlook for the Telecom Edge Load Balancer Market remains highly positive as telecom networks continue to evolve toward low-latency, high-performance architectures. With the rapid expansion of 5G networks and the increasing demand for real-time applications such as video streaming, online gaming, and IoT services, telecom operators are focusing on improving traffic distribution at the edge of the network.

Edge load balancers play a key role in managing data flow efficiently, reducing latency, and ensuring uninterrupted service delivery across distributed network environments. The growing adoption of edge computing is another important factor shaping the market outlook. As data processing shifts closer to end users, telecom providers require advanced load balancing solutions to handle dynamic traffic patterns and support decentralized infrastructure.

This is particularly important for applications that require immediate response times, such as autonomous systems, smart cities, and industrial automation. Edge load balancers help maintain network reliability by distributing workloads across multiple edge nodes.

In addition, telecom operators are investing in network virtualization and cloud integration to enhance flexibility and scalability. These developments are increasing the demand for load balancing solutions that can operate across hybrid and multi-cloud environments. As data traffic continues to grow and network complexity increases, the adoption of telecom edge load balancers is expected to remain strong across global markets.

Future Predictions

The future of the Telecom Edge Load Balancer Market is expected to be shaped by the rapid expansion of edge computing and next-generation telecom networks. As data consumption continues to rise, telecom operators are increasingly shifting processing closer to end users to reduce latency and improve service performance.

It is estimated that a significant share of network traffic will be handled at the edge in the coming years, driven by applications such as real-time video streaming, cloud gaming, and connected devices. This shift will require advanced load-balancing solutions capable of managing distributed traffic efficiently across multiple edge nodes.

The continued rollout of 5G networks is also expected to accelerate demand for edge load balancers. With billions of connected devices and increasing network complexity, telecom providers will require intelligent traffic management systems to ensure stable and reliable connections. Artificial intelligence and automation are likely to play a key role in optimizing load balancing processes, enabling systems to adjust traffic flow dynamically based on real-time conditions.

In addition, the growth of smart cities, autonomous systems, and industrial IoT applications will further increase the need for low-latency network performance. As these technologies expand, telecom edge load balancers are expected to become a critical component of modern network infrastructure, supporting efficient data distribution and enhanced user experience.

Key Market Segments

The Telecom Edge Load Balancer Market is segmented by component, deployment mode, application, and end user, each reflecting how telecom networks manage increasing data traffic and distributed infrastructure. These segments highlight the growing importance of efficient traffic distribution and network optimization in modern telecom environments.

By component, hardware holds the largest share at 52.6%. Hardware-based load balancers are widely used in telecom networks due to their ability to handle high volumes of data traffic with low latency. These solutions are designed for performance-intensive environments and are commonly deployed in edge locations where speed and reliability are critical.

By deployment mode, on-premises solutions account for 55.8% of the market. Telecom operators often prefer on-premises deployment to maintain control over network infrastructure, ensure data security, and support high-performance requirements.

By application, network function virtualization holds 40.7%, as telecom providers increasingly virtualize network functions to improve scalability and flexibility. By end user, telecom operators dominate with 57.8%, as they rely heavily on edge load balancing solutions to manage network traffic, enhance service delivery, and support the growing demand for real-time applications.

Research-Based Segments

By Component

- Hardware

- Software

- Services

By Deployment Mode

- On-Premises

- Cloud

- Hybrid

By Application

- Network Function Virtualization

- Content Delivery Networks

- IoT

- 5G Networks

- Others

By End-User

- Telecom Operators

- Enterprises

- Data Centers

- Others

By Component

The component segment of the Telecom Edge Load Balancer Market includes hardware, software, and services, with hardware holding the leading share at 52.6%. Hardware-based load balancers dominate due to their ability to process large volumes of network traffic with high speed and low latency. These solutions are widely deployed in telecom edge environments where performance, reliability, and real-time data handling are critical.

Telecom operators use dedicated hardware appliances to ensure efficient traffic distribution across edge nodes, especially in high-demand scenarios such as 5G networks, video streaming, and IoT connectivity. Hardware solutions also provide strong stability and are preferred for mission-critical network operations.

Software-based load balancers are gaining traction as telecom networks move toward virtualization and cloud native architectures. These solutions offer flexibility, scalability, and easier integration with virtual network functions.

Services play a supporting role in the market, including consulting, integration, and maintenance. Service providers help telecom companies deploy and manage load-balancing systems effectively. As telecom networks become more complex, both software and services are expected to grow, although hardware remains the dominant component due to its performance advantages in edge environments.

By Deployment Mode

The deployment mode segment of the Telecom Edge Load Balancer Market includes on-premises, cloud, and hybrid solutions, with on-premises holding the dominant share at 55.8%. Telecom operators prefer on premises deployment because it provides greater control over network infrastructure, performance, and security.

Edge environments require ultra-low latency and high reliability, which are often better supported by locally deployed hardware and systems. On-premises solutions allow operators to manage traffic distribution directly within their networks, ensuring faster response times and minimizing dependency on external systems. This approach is especially important for mission-critical telecom operations and high traffic applications such as 5G services and real-time communication.

Cloud-based deployment is gaining adoption as telecom companies increasingly integrate cloud infrastructure into their networks. Cloud solutions offer scalability, flexibility, and the ability to manage traffic across distributed environments. Hybrid deployment models are also emerging, combining the strengths of on-premises and cloud systems.

These setups allow telecom operators to handle sensitive or latency-critical workloads locally while using cloud platforms for scalability and broader network management. As telecom networks continue to evolve, hybrid models are expected to grow, although on-premises deployment remains dominant due to its performance and control advantages.

By Application

The application segment of the Telecom Edge Load Balancer Market includes network function virtualization, content delivery networks, IoT, 5G networks, and other use cases, with network function virtualization holding the leading share at 40.7%. Telecom operators are increasingly virtualizing core network functions to improve scalability, flexibility, and cost efficiency.

Edge load balancers play a critical role in distributing traffic across virtualized network functions, ensuring smooth performance and efficient resource utilization. This approach allows telecom providers to manage dynamic workloads and adapt quickly to changing network demands.

Content delivery networks are another key application, where load balancers help distribute content efficiently across edge servers to reduce latency and improve user experience, especially for video streaming and digital media services. In IoT environments, load balancing solutions manage traffic from a large number of connected devices, ensuring stable and reliable communication.

The rollout of 5G networks is also driving demand, as these networks require advanced traffic management to handle high data volumes and low latency requirements. Other applications include enterprise edge computing and cloud-based telecom services. As network complexity increases, adoption across these application areas is expected to grow steadily.

By End-User

The end user segment of the Telecom Edge Load Balancer Market includes telecom operators, enterprises, data centers, and other users, with telecom operators holding the dominant share at 57.8%. Telecom operators rely heavily on edge load balancing solutions to manage large volumes of network traffic and ensure smooth service delivery.

With the expansion of 5G networks and increasing data consumption, operators need efficient traffic distribution systems to reduce latency and maintain network performance. Edge load balancers help optimize data flow across distributed network nodes, supporting real-time applications and improving user experience.

Enterprises are also adopting these solutions to support edge computing environments and enhance application performance across multiple locations. Data centers play a crucial role as well, using load balancing systems to manage traffic across servers and ensure high availability of services.

These solutions help data centers handle increasing workloads and maintain operational efficiency. Other users include service providers and organizations deploying edge infrastructure for specialized applications. As demand for low-latency services and high-speed connectivity continues to grow, adoption across all end-user segments is expected to increase steadily.

Regional Analysis

North America holds a leading position in the Telecom Edge Load Balancer Market, accounting for approximately 38.1% of the global share. The regional market reached around USD 0.71 billion in 2025, reflecting strong demand for advanced network infrastructure and low-latency solutions.

Telecom operators in the region are rapidly expanding 5G networks and edge computing capabilities, which increases the need for efficient traffic management systems. Edge load balancers play a critical role in ensuring smooth data distribution across decentralized network environments, supporting real-time applications and high-speed connectivity.

The presence of major technology companies, cloud service providers, and telecom operators supports market growth in North America. These organizations are investing heavily in network virtualization, cloud integration, and edge infrastructure to improve performance and scalability. Industries such as media streaming, online gaming, and IoT services are driving demand for low-latency communication, further increasing the adoption of edge load-balancing solutions.

In addition, strong digital infrastructure and high data consumption levels in the region contribute to market expansion. As network complexity continues to grow and demand for real-time services increases, North America is expected to remain a key market for telecom edge load balancer solutions.

US Market Size

The United States Telecom Edge Load Balancer Market generated approximately USD 0.60 billion in revenue and represents the largest share within North America. The market is expanding as telecom operators invest in advanced network infrastructure to support rising data traffic and low-latency applications.

With the rapid rollout of 5G networks and increasing adoption of edge computing, there is a growing need for efficient traffic distribution across decentralized network environments. Edge load balancers help telecom providers manage network congestion, improve service reliability, and deliver faster response times for applications such as video streaming, online gaming, and IoT services.

The US market is expected to grow at a strong CAGR of 18.5% during the forecast period, reflecting continuous investments in next-generation telecom technologies. Telecom operators and cloud service providers are focusing on network virtualization and edge infrastructure to enhance scalability and performance. Enterprises are also adopting edge solutions to improve application delivery and user experience.

In addition, the increasing demand for real-time data processing and high-speed connectivity is driving the adoption of telecom edge load balancing solutions. As digital services continue to expand and network complexity increases, the US market is expected to witness strong and sustained growth over the coming years.

Regional Analysis and Coverage

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherlands

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Thailand

- Vietnam

- Rest of Latin America

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Driving Factors

The Telecom Edge Load Balancer Market is driven by the rapid growth of data traffic and the expansion of 5G networks. Telecom operators are handling increasing volumes of real-time data from applications such as video streaming, online gaming, and IoT devices. This creates a strong need for efficient traffic distribution at the network edge to reduce latency and improve performance. Edge load balancers help manage this complexity by optimizing data flow across distributed nodes.

The shift toward edge computing is another major driver, as organizations move data processing closer to end users. In addition, telecom companies are investing in network virtualization and cloud integration to improve flexibility and scalability. These developments are increasing the demand for advanced load balancing solutions that can support dynamic and high-speed network environments.

Restraint Factors

One of the key restraints in the Telecom Edge Load Balancer Market is the high cost associated with deploying and maintaining advanced edge infrastructure. Hardware-based load balancers and edge systems require significant capital investment, which can be challenging for smaller telecom operators. Integration complexity is another issue, as edge load balancing solutions must work seamlessly with existing network architectures, including legacy systems.

This can increase deployment time and require specialized expertise. In addition, concerns related to data security and network reliability can slow adoption, especially in highly regulated industries. Managing distributed edge environments also adds operational complexity, which may limit adoption in regions with limited technical resources or infrastructure capabilities.

Growth Opportunities

The market offers strong growth opportunities with the increasing adoption of edge computing and 5G technologies. Telecom operators are expanding edge networks to support real-time applications, creating demand for advanced load balancing solutions. The integration of artificial intelligence and machine learning into load balancing systems presents new opportunities for intelligent traffic management and predictive optimization.

Enterprises are also investing in edge infrastructure to improve application performance and user experience, further driving demand. In addition, the growth of smart cities, autonomous systems, and industrial IoT is expected to create new use cases for edge load balancing. As digital transformation accelerates across industries, the need for efficient and scalable network solutions is expected to increase significantly.

Trending Factors

Several trends are shaping the Telecom Edge Load Balancer Market as network architectures evolve. One major trend is the shift toward software-defined networking and network function virtualization, which allows telecom operators to manage networks more flexibly. Another trend is the increasing adoption of cloud native load balancing solutions that support hybrid and multi-cloud environments.

Artificial intelligence is also being integrated into load balancing systems to enable real-time traffic optimization and automated decision-making. Additionally, there is a growing focus on energy-efficient and scalable solutions to support expanding edge networks. The rise of decentralized computing and edge data centers is further influencing the market, as organizations seek to improve performance and reduce latency for critical applications.

Competitive Analysis

The competitive landscape of the Telecom Edge Load Balancer Market is moderately consolidated, with a mix of global networking giants, cloud infrastructure providers, and specialized load balancing vendors competing on performance, scalability, and innovation.

Key players such as Amazon Web Services, F5, Cloudflare, Akamai Technologies, and A10 Networks focus on delivering high-performance edge traffic management solutions integrated with cloud and content delivery ecosystems. These companies leverage large-scale infrastructure and global edge networks to provide low-latency services, which strengthens their competitive positioning.

Technology-driven competition is increasing as vendors invest in software-defined networking, network function virtualization, and AI-based traffic optimization. For instance, the broader load balancer market is expanding from over USD 7 billion in 2025 toward nearly USD 19 billion by the early 2030s, indicating strong demand for advanced traffic management solutions. Additionally, the telecom edge load balancer segment itself continues to grow steadily, supported by the rapid deployment of 5G and edge computing infrastructure.

New entrants and niche providers such as HAProxy Technologies, Radware, and Fastly are focusing on software-based and cloud native solutions to compete with established players. Competition is driven by the ability to handle high traffic volumes, support multi-cloud environments, and deliver real-time analytics. As telecom networks become more distributed, vendors that offer integrated, scalable, and intelligent load balancing solutions are expected to gain a competitive advantage.

Top Key Players in the Market

- A10 Networks

- Akamai Technologies

- Array Networks

- Barracuda Networks

- Broadcom (F5 Networks)

- Citrix Systems

- Cisco Systems

- Cloudflare

- Edgecast (Verizon Media)

- Fortinet

- Hewlett Packard Enterprise (HPE)

- Imperva

- Juniper Networks

- Kemp Technologies (Progress Software)

- Microsoft Azure

- NGINX (F5 Networks)

- Radware

- Sangfor Technologies

- Zscaler

- Zeus Technology (Riverbed Technology)

- Others

Recent Developments

- In 2025, telecom operators accelerated edge infrastructure deployment as 5G adoption reached nearly 28% of mobile broadband subscriptions across OECD countries, increasing the need for efficient edge load balancing systems.

- In 2025, telecom operators accelerated edge infrastructure deployment as 5G adoption reached nearly 28% of mobile broadband subscriptions across OECD countries, increasing the need for efficient edge load balancing systems.

- In 2026, telecom networks began integrating agentic AI for automated traffic management, enabling predictive load balancing and real-time network optimization at the edge.

Report Scope

Report Features Description Market Value (2025) USD 1.87 Billion Forecast Revenue (2035) USD 12.58 Billion CAGR(2025-2035) 21.00% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue forecast, AI impact on Market trends, Share Insights, Company ranking, competitive landscape, Recent Developments, Market Dynamics, and Emerging Trends Segments Covered By Component (Hardware, Software, Services), By Deployment Mode (On-Premises, Cloud, Hybrid), By Application (Network Function Virtualization, Content Delivery Networks, IoT, 5G Networks, Others), By End-User (Telecom Operators, Enterprises, Data Centers, Others) Regional Analysis North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Latin America; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA Competitive Landscape A10 Networks, Akamai Technologies, Array Networks, Barracuda Networks, Broadcom (F5 Networks), Citrix Systems, Cisco Systems, Cloudflare, Edgecast (Verizon Media), Fortinet, Hewlett Packard Enterprise (HPE), Imperva, Juniper Networks, Kemp Technologies (Progress Software), Microsoft Azure, NGINX (F5 Networks), Radware, Sangfor Technologies, Zscaler, Zeus Technology (Riverbed Technology), Others Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF)  Telecom Edge Load Balancer MarketPublished date: Mar 2026add_shopping_cartBuy Now get_appDownload Sample

Telecom Edge Load Balancer MarketPublished date: Mar 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- A10 Networks

- Akamai Technologies

- Array Networks

- Barracuda Networks

- Broadcom (F5 Networks)

- Citrix Systems

- Cisco Systems

- Cloudflare

- Edgecast (Verizon Media)

- Fortinet

- Hewlett Packard Enterprise (HPE)

- Imperva

- Juniper Networks

- Kemp Technologies (Progress Software)

- Microsoft Azure

- NGINX (F5 Networks)

- Radware

- Sangfor Technologies

- Zscaler

- Zeus Technology (Riverbed Technology)

- Others

Our Clients

- 181859

- Mar 2026