Global Synthetic Ester Lubricants Market Size, Share, And Industry Analysis Report By Product Type (Polyol Ester Lubricants, Diester Lubricants, Complex Ester Lubricants, Blended Synthetic Ester Formulations), By Application (Cooling Systems and Thermal Management, Base Station Equipment Lubrication, Power Backup Systems), By Equipment Type (Telecom Towers and Base Transceiver Stations, Data Centers and Network Switching Equipment, Optical Fiber and Cable Infrastructure, Power and Energy Storage Systems), By End-User (Telecom Network Operators, Data Center Operators, Telecom Equipment Manufacturers, Infrastructure Service Providers), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2026-2035

- Published date: March 2026

- Report ID: 180228

- Number of Pages: 350

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

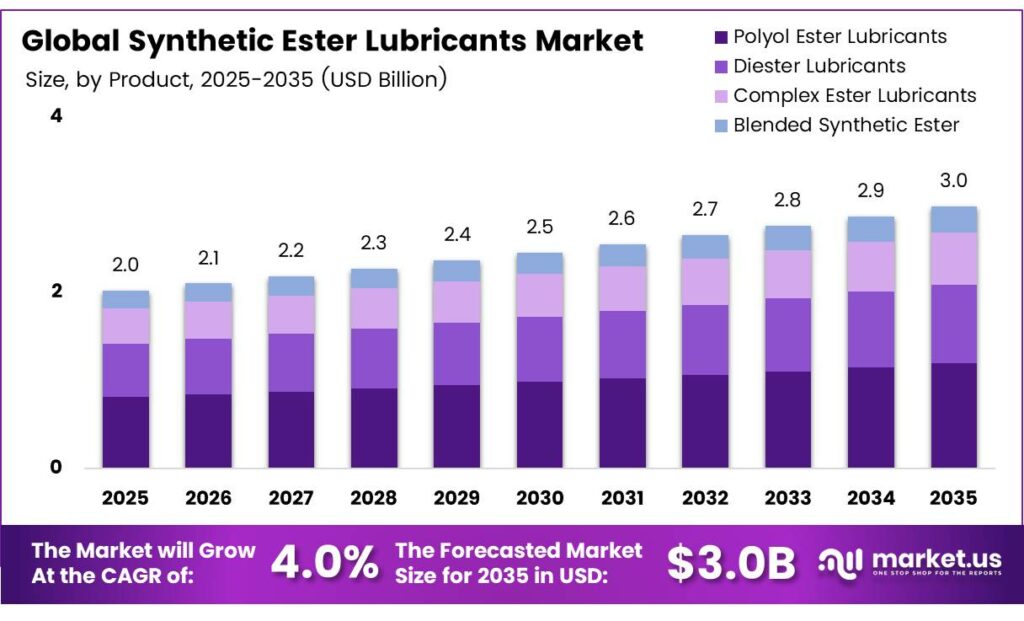

The Global Synthetic Ester Lubricants Market size is expected to be worth around USD 3.0 billion by 2035 from USD 2.0 billion in 2025, growing at a CAGR of 4.0% during the forecast period 2026 to 2035.

Synthetic ester lubricants are high-performance fluids derived from chemical reactions between alcohols and acids. These lubricants deliver superior thermal stability, biodegradability, and low-temperature fluidity. Industries such as aerospace, automotive, and industrial manufacturing actively adopt these solutions for demanding applications.

Ester-based lubricants outperform conventional mineral oils in extreme heat and pressure conditions. They reduce equipment wear, extend fluid change intervals, and lower maintenance costs. Consequently, sectors operating heavy machinery and precision equipment prefer synthetic ester formulations over traditional alternatives.

- Global lubricant demand reached approximately 38 million metric tons in 2024, reflecting total consumption across transportation, industrial, marine, and aviation sectors. This broad lubricant base creates a large addressable opportunity for synthetic esters as industries upgrade from mineral to high-performance fluids.

Environmental regulations push manufacturers and operators toward biodegradable lubricant solutions. Governments in Europe and North America enforce strict standards on lubricant disposal and ecological impact. Therefore, synthetic esters gain traction as a compliant and sustainable choice across marine, forestry, and industrial sectors.

- The global lubricant market revenue reached $63.9 billion in 2024, covering industrial, automotive, and specialty products, including synthetic ester formulations. This large revenue base highlights the commercial scale available to synthetic ester producers as sustainability mandates and performance requirements accelerate product substitution.

Electric vehicle production accelerates demand for specialized thermal management fluids. EV manufacturers require lubricants that handle high-voltage cooling systems safely and efficiently. Moreover, aerospace operators favor polyol and diester fluids for jet engine and turbine applications where performance under extreme conditions is critical.

Key Takeaways

- The Global Synthetic Ester Lubricants Market is valued at USD 2.0 billion in 2025 and is projected to reach USD 3.0 billion by 2035, at a CAGR of 4.0% during the forecast period 2026 to 2035.

- Polyol Ester Lubricants dominate with a 38.2% market share in 2025.

- Cooling Systems and Thermal Management holds the leading share at 34.7%.

- Telecom Towers and Base Transceiver Stations lead with a 34.1% share.

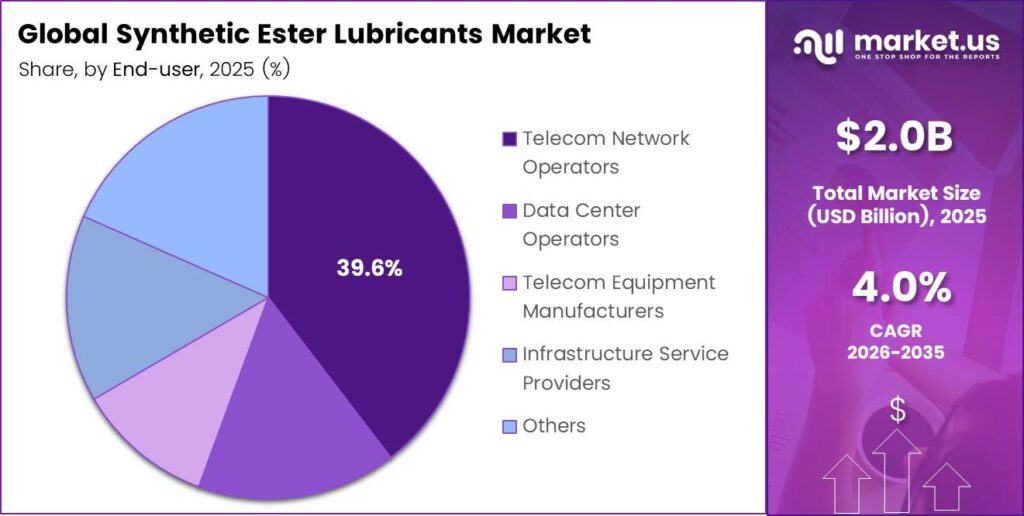

- Telecom Network Operators represent the largest segment at 39.6%.

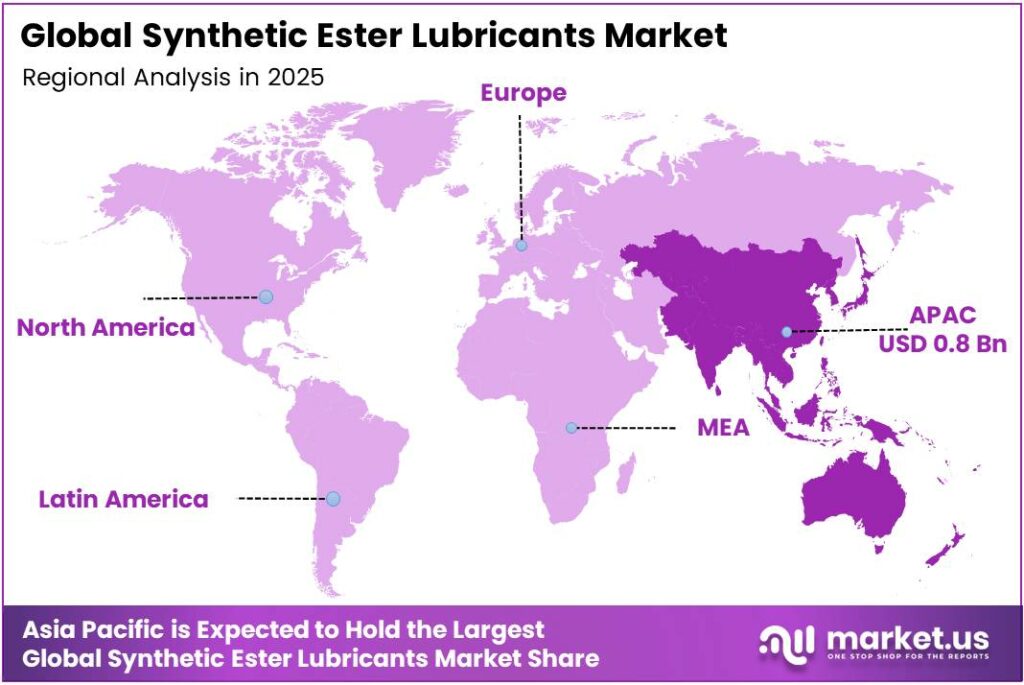

- Asia Pacific dominates the regional landscape with a 38.4% share, valued at USD 0.8 billion.

By Product Type Analysis

Polyol Ester Lubricants dominate with 38.2% due to superior thermal stability and wide use in aerospace and EV thermal fluids.

In 2025, Polyol Ester Lubricants held a dominant market position in the By Product Type segment of the Synthetic Ester Lubricants Market, with a 38.2% share. These esters deliver exceptional thermal and oxidative stability, making them the preferred choice for jet engines, turbines, and electric vehicle cooling circuits requiring reliable high-temperature performance.

Diester Lubricants serve as versatile base fluids across compressor, refrigeration, and general industrial applications. They offer good low-temperature flow and lubricity. Moreover, diesters blend well with additives, supporting formulators in developing cost-effective, high-performance finished lubricants for automotive and industrial markets.

Complex Ester Lubricants combine multiple alcohol and acid components to achieve tailored viscosity and load-carrying capacity. These advanced fluids address demanding metalworking, gear, and bearing applications. Consequently, equipment manufacturers in heavy industry and defense specify complex esters where standard formulations cannot meet performance thresholds.

Blended Synthetic Ester Formulations combine ester base stocks with other synthetics, such as PAO, to optimize cost and performance. These blends expand the accessible market by offering improved properties over mineral oils at lower prices than full-synthetic esters. Therefore, they attract cost-sensitive industrial users seeking performance upgrades on moderate budgets.

By Application Analysis

Cooling Systems and Thermal Management dominate with 34.7% due to rapid growth in EV and data center thermal fluid demand.

In 2025, Cooling Systems and Thermal Management held a dominant market position in the By Application segment of the Synthetic Ester Lubricants Market, with a 34.7% share. Electric vehicles, power electronics, and high-density data centers drive this segment as operators require thermally stable, dielectric fluids that manage heat efficiently while protecting sensitive components.

Base Station Equipment Lubrication covers the growing network of telecom towers and 5G base stations requiring reliable lubricants. These installations operate in harsh outdoor environments with wide temperature swings. Moreover, synthetic esters extend maintenance intervals and protect critical radio and antenna components from wear and corrosion.

Cable and Connector Protection uses synthetic ester fluids to prevent oxidation, moisture ingress, and mechanical wear in telecom infrastructure. High-performance ester compounds protect fiber optic connectors and high-voltage cable joints. Consequently, network operators reduce downtime and extend asset life across dense urban and remote deployment environments.

Power Backup Systems, including UPS units and generator sets, require lubricants that perform reliably during intermittent and emergency operation cycles. Synthetic esters maintain film strength across extended storage and sporadic load conditions. Therefore, data center operators and critical infrastructure providers increasingly specify ester-based fluids for backup power equipment.

By Equipment Type Analysis

Telecom Towers and Base Transceiver Stations dominate with 34.1% due to the global 5G rollout and tower infrastructure expansion.

In 2025, Telecom Towers and Base Transceiver Stations held a dominant market position in the By Equipment Type segment of the Synthetic Ester Lubricants Market, with a 34.1% share. The rapid global expansion of 5G networks and increasing tower density requires high-performance lubricants that protect mechanical components and antenna systems in varied climatic conditions.

Data Centers and Network Switching Equipment represent a fast-growing equipment category as cloud computing and digital services expand globally. These facilities rely on synthetic ester fluids for immersion cooling and precision lubrication of switching hardware. Additionally, rising server densities increase thermal loads, reinforcing demand for advanced ester-based cooling solutions.

Optical Fiber and cable infrastructure require protective lubricants during installation and long-term operation. Synthetic esters prevent surface degradation and maintain connector integrity in underground and submarine cable systems. Moreover, telecommunications expansion in the Asia-Pacific and Africa drives new cable deployments requiring compatible and environmentally safe ester fluids.

Power and Energy Storage Systems, including battery storage arrays and transformer equipment, benefit from synthetic ester dielectric fluids. These fluids offer fire-resistant and biodegradable properties compared to mineral transformer oils. Consequently, renewable energy developers and grid operators prefer synthetic esters for new transformer installations supporting solar and wind energy projects.

By End-User Analysis

Telecom Network Operators dominate with 39.6% due to large-scale infrastructure maintenance and 5G expansion programs.

In 2025, Telecom Network Operators held a dominant market position in the By End-User segment of the Synthetic Ester Lubricants Market, with a 39.6% share. These operators manage vast tower and cable networks requiring scheduled lubrication and thermal fluid management. Their large procurement volumes and stringent quality requirements drive consistent demand for premium synthetic ester products.

Data Center Operators represent a rapidly growing end-user group as hyperscale and enterprise data centers multiply worldwide. These facilities require large volumes of dielectric and cooling fluids. Moreover, data center operators increasingly adopt immersion cooling systems that rely exclusively on synthetic ester fluids for safe, efficient heat dissipation.

Telecom Equipment Manufacturers specify lubricants during product development and factory assembly of base stations, routers, and switching platforms. Their choices influence downstream maintenance lubricant decisions by network operators. Therefore, manufacturers who design equipment to use synthetic esters create a lasting demand channel throughout the product’s operational life.

Infrastructure Service Providers manage the installation, maintenance, and repair of telecom and energy networks for multiple clients. These firms purchase synthetic ester lubricants at scale for field operations. Additionally, Others including government agencies and utilities, contribute to market demand through infrastructure modernization and rural connectivity programs.

Key Market Segments

By Product Type

- Polyol Ester Lubricants

- Diester Lubricants

- Complex Ester Lubricants

- Blended Synthetic Ester Formulations

By Application

- Cooling Systems and Thermal Management

- Base Station Equipment Lubrication

- Cable and Connector Protection

- Power Backup Systems

By Equipment Type

- Telecom Towers and Base Transceiver Stations

- Data Centers and Network Switching Equipment

- Optical Fiber and Cable Infrastructure

- Power and Energy Storage Systems

By End-User

- Telecom Network Operators

- Data Center Operators

- Telecom Equipment Manufacturers

- Infrastructure Service Providers

- Others

Emerging Trends

Biosynthetic Formulations and EV Thermal Fluids Define Next-Generation Synthetic Ester Applications

Manufacturers actively develop 100% biosynthetic lubricants produced using solar-powered and low-carbon facilities. This shift combines sustainable raw material sourcing with green manufacturing processes. Consequently, environmentally responsible producers gain a competitive advantage as buyers in Europe and North America prioritize low-carbon supply chains for industrial lubricants.

- Polyol and aromatic esters increasingly dominate high-load and low-volatility applications in aerospace, defense, and heavy machinery. Global lubricant industry shipments totaled 198,188 lubricating oil shipments between June 2024 and May 2025 across 15,267 exporters and 16,808 buyers. This trade volume signals growing international demand for specialty ester fluids serving performance-critical applications.

Electric vehicle coolants and high-voltage thermal management systems drive rapid adoption of dielectric ester fluids. Innovations in low-GWP compatible esters also address energy-efficient HVAC and refrigeration systems. Moreover, refrigerant transitions away from high-GWP gases create new formulation opportunities for ester lubricants compatible with next-generation low-GWP refrigerants in commercial cooling equipment.

Drivers

Environmental Regulations, EV Growth, and Aerospace Demand Drive Synthetic Ester Lubricants Adoption

Stringent environmental regulations and maritime compliance requirements push industries toward biodegradable ester lubricants. Regulatory bodies in the EU and IMO enforce strict rules on lubricant discharge and ecological impact in marine environments. According to the U.S. Census Bureau, United States lubricant exports reached $6.98 billion in 2024, confirming strong global trade flows for high-performance synthetic lubricants.

- Explosive growth in electric vehicle manufacturing creates specialized demand for thermal management fluids. EV battery packs and power electronics require dielectric cooling solutions that ester lubricants uniquely provide. Furthermore, FUCHS SE’s free cash flow before acquisitions of €306 million in FY2024, reflecting the financial strength of leading lubricant producers investing in ester product development and capacity expansion.

The aerospace and aviation sector drives consistent adoption of synthetic esters due to superior performance at extreme temperatures. Jet engines and turbine systems require fluids that resist thermal degradation across wide operating ranges. Additionally, rapid industrialization in the Asia-Pacific region increases demand for high-efficiency lubricants in manufacturing, power generation, and heavy equipment maintenance applications.

Restraints

High Production Costs and Competing Alternatives Limit Synthetic Ester Lubricants Market Penetration

High manufacturing and raw material costs restrict synthetic ester adoption in cost-sensitive industrial segments. Ester base stocks require complex chemical synthesis from specialized fatty acids and alcohols, making them significantly more expensive than mineral oil alternatives. Consequently, small and mid-sized manufacturers in developing markets often continue using conventional lubricants to manage operational budgets.

Competing synthetic alternatives, such as polyalphaolefins and bio-lubricants, challenge the synthetic ester market share. PAO lubricants offer comparable thermal performance at lower costs in many applications. Moreover, bio-lubricants derived from vegetable oils attract environmentally conscious buyers who may perceive them as more natural alternatives, creating price and positioning competition for synthetic ester producers.

Technical compatibility limitations also restrain wider adoption. Some synthetic ester formulations are incompatible with specific seal materials, coatings, or legacy equipment designed for mineral oil use. Therefore, industrial operators face upgrade costs and engineering challenges when converting existing systems to synthetic ester lubricants, slowing replacement cycles in mature industrial markets.

Growth Factors

Renewable Energy Expansion, Food-Grade Demand, and Custom Formulations Fuel Synthetic Ester Market Growth

Renewable energy projects create substantial demand for durable wind turbine gear lubricants. Wind turbine gearboxes operate under high loads and variable speeds, requiring synthetic esters that resist oxidation and water contamination. China’s lubricating oil consumption reached around 8.2 million metric tons in 2024, driven by industrial machinery and manufacturing growth that supports ester lubricant demand.

- Rising demand for food-grade and pharmaceutical-grade ester lubricants creates premium growth segments. Regulatory bodies require incidental contact lubricants to meet NSF H1 and similar safety certifications. Moreover, Evonik Industries adjusted EBITDA of €2,065 million in FY2024, reflecting the profitability of specialty chemical producers whose ester-based product lines serve high-value food and pharmaceutical lubrication markets.

Government incentives and manufacturing investments in emerging markets support local synthetic ester production scaling. Partnerships for custom ester formulations in defense and high-performance industrial applications expand addressable revenue. Additionally, defense procurement programs in Asia-Pacific and the Middle East require specialized ester fluids for aircraft, armored vehicles, and naval applications that command premium prices.

Regional Analysis

Asia Pacific Dominates the Synthetic Ester Lubricants Market with a Market Share of 38.4%, Valued at USD 0.8 Billion

Asia Pacific leads the global synthetic ester lubricants market with a 38.4% share, valued at USD 0.8 billion in 2025. Rapid industrialization in China, India, and Southeast Asia drives strong demand for high-efficiency lubricants across manufacturing, automotive, and energy sectors. Moreover, China’s large base oil refining capacity and active 5G infrastructure rollout reinforce the region’s dominant position.

North America maintains a significant market position driven by aerospace, defense, and advanced manufacturing sectors. The United States leads regional consumption, supported by stringent environmental regulations that favor biodegradable synthetic esters. Additionally, strong domestic lubricant production infrastructure and high EV adoption rates sustain demand for specialized thermal management fluids across the region.

Europe represents a mature and regulation-driven market for synthetic ester lubricants. EU environmental directives enforce strict lubricant discharge and biodegradability standards across marine, forestry, and industrial applications. Consequently, European operators actively replace mineral oils with compliant ester formulations, while wind energy expansion in Germany, the UK, and Scandinavia creates growing turbine lubrication demand.

The Middle East and Africa market grows steadily as infrastructure investment expands across energy, telecom, and industrial sectors. Gulf states invest in downstream petrochemical refining that supports local lubricant production. Moreover, rising telecom network deployments across Africa increase demand for synthetic ester fluids used in base station and cable infrastructure maintenance applications.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Exxon Mobil Corporation holds a leading position in the synthetic ester lubricants market through its Mobil-branded product portfolio. The company serves aerospace, automotive, and industrial segments with high-performance ester and PAO-based formulations. Its extensive global distribution network and strong R&D investment enable consistent product innovation and customer retention across demanding end-use markets worldwide.

Royal Dutch Shell plc actively competes in the synthetic lubricants space through its Shell Lubricants division, offering ester-based products for industrial, marine, and energy sectors. Shell leverages its global refining and blending infrastructure to supply premium lubricant solutions. Moreover, its technical service capabilities help industrial clients optimize lubricant selection for specific equipment and operating conditions.

TotalEnergies SE supplies synthetic ester lubricants under its Total and ELF brand families, targeting aviation, automotive, and renewable energy applications. The company reflecting strong operating capacity to fund product development and international market expansion. TotalEnergies actively develops bio-based ester formulations aligned with global sustainability requirements.

Chevron Corporation competes in the synthetic lubricants market through its Chevron and Texaco product lines. The company focuses on high-performance industrial and transportation lubricants, including specialty ester-based fluids for compressors, turbines, and aviation equipment. Chevron’s technology centers drive the continuous development of next-generation lubricant formulations that meet evolving environmental and performance standards globally.

Top Key Players in the Market

- Exxon Mobil Corporation

- Royal Dutch Shell plc

- TotalEnergies SE

- Chevron Corporation

- BP p.l.c.

- Fuchs SE

- Sinopec Limited

- Valvoline Inc.

- AMSOIL Inc.

- Others

Recent Developments

- In 2025, Shell has made clear advances in synthetic ester-based fluids through its lubricants business. Shell U.K. Limited completed the acquisition of the MIDEL and MIVOLT product lines from M&I Materials Ltd. MIDEL products are synthetic (and natural) ester-based transformer insulating fluids used in power distribution, offshore wind, utilities, and traction systems.

- In 2025, Exxon Mobil Corporation maintains its established portfolio of synthetic lubricants, including ester-based aviation turbine oils under the Mobil brand. Still, no new product launches, expansions, or partnerships tied directly to synthetic esters appeared in official announcements.

Report Scope

Report Features Description Market Value (2025) USD 2.0 Billion Forecast Revenue (2035) USD 3.0 Billion CAGR (2026-2035) 4.0% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Product Type (Polyol Ester Lubricants, Diester Lubricants, Complex Ester Lubricants, Blended Synthetic Ester Formulations), By Application (Cooling Systems and Thermal Management, Base Station Equipment Lubrication, Cable and Connector Protection, Power Backup Systems), By Equipment Type (Telecom Towers and Base Transceiver Stations, Data Centers and Network Switching Equipment, Optical Fiber and Cable Infrastructure, Power and Energy Storage Systems), By End-User (Telecom Network Operators, Data Center Operators, Telecom Equipment Manufacturers, Infrastructure Service Providers, Others) Regional Analysis North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) Competitive Landscape Exxon Mobil Corporation, Royal Dutch Shell plc, TotalEnergies SE, Chevron Corporation, BP p.l.c., Fuchs SE, Sinopec Limited, Valvoline Inc., AMSOIL Inc., Others Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF)  Synthetic Ester Lubricants MarketPublished date: March 2026add_shopping_cartBuy Now get_appDownload Sample

Synthetic Ester Lubricants MarketPublished date: March 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- Exxon Mobil Corporation

- Royal Dutch Shell plc

- TotalEnergies SE

- Chevron Corporation

- BP p.l.c.

- Fuchs SE

- Sinopec Limited

- Valvoline Inc.

- AMSOIL Inc.

- Others

Our Clients

- 180228

- March 2026