Quick Navigation

Report Overview

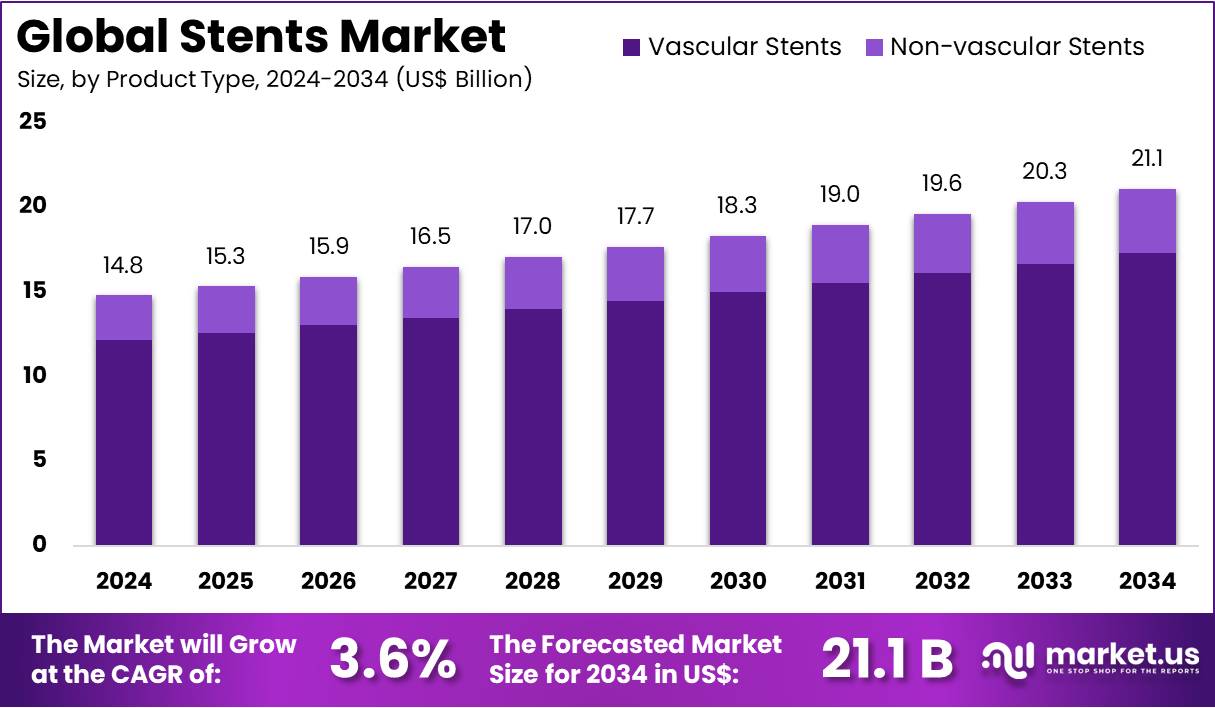

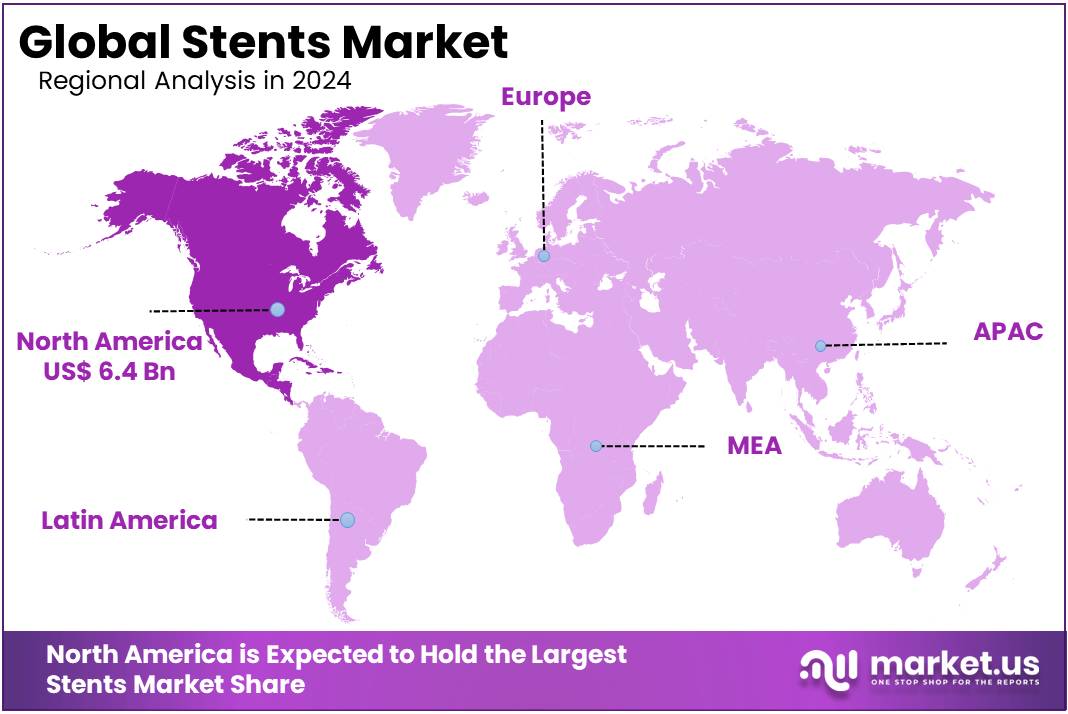

The Stents Market size is expected to be worth around US$ 21.1 billion by 2034 from US$ 14.8 billion in 2024, growing at a CAGR of 3.6% during the forecast period 2025 to 2034. North America held a dominant market position, capturing more than a 43.5% share and holds US$ 6.4 Billion market value for the year.

Growing demand for effective treatments for cardiovascular diseases has driven the expansion of the stents market. Stents, primarily used in coronary artery disease treatments, help maintain arterial patency and prevent blockages after angioplasty. The increasing incidence of lifestyle-related diseases, including hypertension, diabetes, and obesity, significantly contributes to the rise in cardiovascular procedures requiring stents.

Technological advancements in stent materials, such as drug-eluting stents and bioresorbable stents, have created opportunities for more effective, long-term treatments with fewer complications. The adoption of minimally invasive procedures has also facilitated market growth, as these procedures reduce recovery times and hospital stays.

In July 2024, Shanghai MicroPort Medical (Group) Co., Ltd. received approval from China’s NMPA for its innovative Firesorb stent, a fully bioresorbable cardiac stent. This next-generation stent has shown comparable performance to conventional drug-eluting stents in clinical trials, excelling in key metrics like lumen loss and procedural success rates. These innovations offer significant opportunities for continued market growth and improved patient outcomes.

Key Takeaways

- In 2024, the market for Stents generated a revenue of US$ 14.8 billion, with a CAGR of 3.6%, and is expected to reach US$ 21.1 billion by the year 2034.

- The product type segment is divided into vascular stents and non-vascular stents, with vascular stents taking the lead in 2024 with a market share of 82.0%.

- Considering material, the market is divided into metallic stents and non-metallic stents. Among these, metallic stents held a significant share of 78.5%.

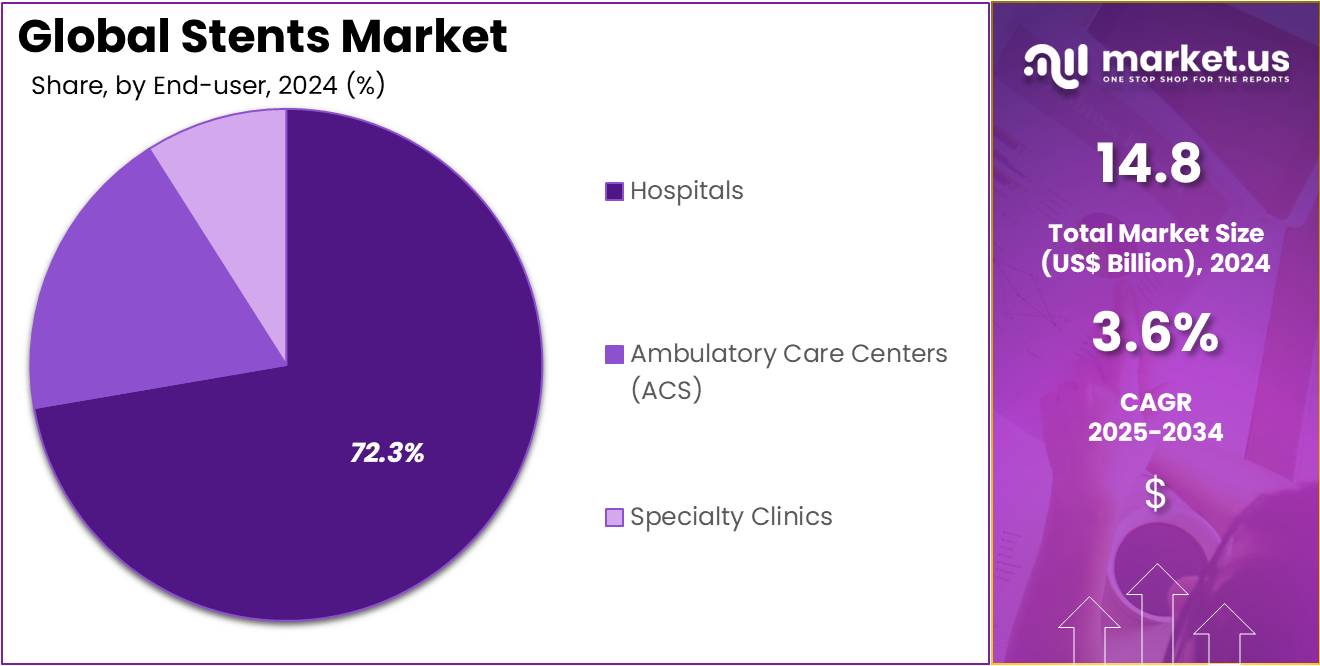

- Furthermore, concerning the end-user segment, the market is segregated into hospitals, ambulatory care centers (ACS), and specialty clinics. The hospitals sector stands out as the dominant player, holding the largest revenue share of 72.3% in the Stents market.

- North America led the market by securing a market share of 43.5% in 2024.

Product Type Analysis

The vascular stents segment led in 2024, claiming a market share of 82.0% owing to the increasing prevalence of vascular diseases, such as coronary artery disease, peripheral artery disease, and carotid artery disease. Vascular stents are projected to remain the primary solution for managing these conditions, as they help prevent vessel restenosis and maintain proper blood flow. The growing aging population, coupled with lifestyle factors such as smoking, obesity, and diabetes, is anticipated to drive the demand for vascular stents.

Additionally, advancements in stent designs, such as drug-eluting stents and bioresorbable stents, are likely to contribute to the segment’s expansion by offering improved outcomes and reduced complications. As healthcare systems continue to prioritize minimally invasive procedures, the vascular stents segment is expected to see sustained growth.

Material Analysis

The metallic stents held a significant share of 78.5% due to the proven effectiveness, strength, and durability of metallic stents, particularly in cardiovascular procedures. Metallic stents, made from materials such as stainless steel and cobalt-chromium alloys, offer superior flexibility and strength, which is critical for maintaining vessel patency. The demand for metallic stents is expected to rise as cardiovascular diseases become more prevalent, particularly in aging populations.

The increasing use of drug-eluting metallic stents, which release medication to prevent restenosis, is likely to further drive this segment’s growth. Moreover, technological advancements in metallic stent designs, including improved coatings and bioactive properties, are projected to enhance patient outcomes, contributing to the continued demand for metallic stents in the market.

End-user Analysis

The hospitals segment has experienced remarkable growth, accounting for a significant 72.3% revenue share. This growth is attributed to the critical role hospitals play in treating vascular diseases. Hospitals remain the primary end-users of stents, providing comprehensive care for patients requiring stent implantation in coronary, peripheral, and other vascular procedures. The rising prevalence of cardiovascular diseases and the increasing number of angioplasty procedures are key factors driving stent demand in hospital settings. This trend highlights hospitals’ essential role in vascular healthcare.

Hospitals are expected to continue adopting advanced stent technologies, such as drug-eluting stents, to enhance patient outcomes. These innovations help reduce restenosis rates, improving the success of minimally invasive treatments. As healthcare systems prioritize effective care solutions, hospitals are increasingly focusing on advanced treatment options. This trend is expected to sustain steady growth in the hospitals segment within the stents market in the coming years.

Key Market Segments

By Product Type

- Vascular Stents

- Coronary Stents

- Peripheral Stents

- Iliac Artery Stents

- Renal Artery Stents

- Femoral Artery Stents

- Carotid Artery Stents

- Other Peripheral Stents

- Neurovascular Stents

- Intracranial Stents

- Flow Diverters

- Non-vascular Stents

- Gastrointestinal Stents

- Biliary

- Pancreatic

- Esophageal Stents

- Duodenal

- Colonic

- Pulmonary (Airway) Stents

- Silicone Airway

- Metallic Airway

- Urological Stents

- Others

- Gastrointestinal Stents

By Material

- Metallic Stents

- Non-metallic Stents

By End-user

- Hospitals

- Ambulatory Care Centers (ACS)

- Specialty Clinics

Drivers

Increasing Prevalence of Cardiovascular Diseases is Driving the Market

The rising incidence of cardiovascular diseases (CVDs) significantly propels the stents market. CVDs, including coronary artery disease and peripheral artery disease, are leading causes of morbidity and mortality worldwide. In 2022, coronary heart disease accounted for 371,506 deaths in the US, making it the primary cause of death. This high prevalence necessitates effective interventions such as stenting procedures to restore proper blood flow.

The demand for stents as essential tools in managing and treating CVDs continues to increase. Healthcare providers are increasingly adopting stents to address the challenges of arterial blockages. Furthermore, improved access to healthcare and better diagnostic techniques are leading to earlier detection and treatment. As awareness of cardiovascular health rises and more patients seek medical interventions, the stents market is expected to continue expanding.

Restraints

High Costs and Procedural Risks are Restraining the Market

Despite their effectiveness, the adoption of stents faces challenges due to high costs and associated procedural risks. The expenses include the stents themselves, catheterization procedures, and post-operative care, which can be prohibitive, especially in low-resource settings. Additionally, although stenting is generally safe, risks such as thrombosis, restenosis, and allergic reactions to contrast materials exist. These complications can increase treatment costs and prolong recovery, deterring patients from opting for stent implantation.

The high financial burden also affects healthcare institutions, limiting their ability to invest in these advanced procedures. Moreover, in some regions, limited insurance coverage for stenting procedures further exacerbates the issue. To overcome these challenges, ongoing research is focused on enhancing stent technology to reduce procedural risks and lower overall costs. Without addressing these concerns effectively, the widespread adoption of stents may remain restricted.

Opportunities

Technological Advancements in Stent Design are Creating Growth Opportunities

Technological advancements in stent design present significant growth opportunities in the market. The development of drug-eluting stents (DES) has significantly improved patient outcomes by releasing medication to prevent restenosis. These innovations are enhancing the effectiveness of stenting procedures, leading to better long-term results.

Additionally, bioresorbable stents, designed to dissolve over time, offer further promise by reducing long-term complications associated with permanent implants. These advances cater to the growing demand for minimally invasive procedures that offer reduced recovery times and lower complication rates. As stent technology continues to improve, the market is witnessing an increase in the range of stent options available to patients and healthcare providers.

Ongoing research is focusing on improving the biocompatibility and drug-delivery capabilities of stents, which will likely lead to even better patient outcomes. The continued development of these innovative stent designs is expected to contribute to sustained growth in the market.

Impact of Macroeconomic / Geopolitical Factors

Macroeconomic and geopolitical factors significantly influence the stents market. Economic downturns can lead to reduced healthcare budgets, limiting access to advanced stenting procedures and treatments. Financial constraints within healthcare systems can slow down the adoption of innovative stent technologies, making it harder for healthcare providers to offer the latest options.

On the other hand, economic growth often results in increased healthcare spending, which can facilitate broader adoption of stents and other medical devices. Geopolitical tensions can disrupt global supply chains, affecting the availability of essential stents and related medical supplies. These disruptions can cause delays in the delivery of stents, hindering timely procedures for patients in need.

Additionally, variations in healthcare policies and reimbursement structures across regions can impact the affordability and adoption of stenting procedures. Despite these challenges, ongoing technological advancements and a global focus on improving cardiovascular health are expected to drive the market positively. Stable geopolitical environments and supportive economic conditions will create a conducive environment for the stents market to thrive.

Latest Trends

Integration of Nanotechnology and Biodegradable Materials is a Recent Trend

A notable recent trend in the stents market is the integration of nanotechnology and biodegradable materials into stent design. Nanotechnology allows for the development of stents with enhanced drug-delivery capabilities, improving the efficacy of treatment and reducing the risk of restenosis. These stents are more effective in preventing the re-blockage of arteries and reducing complications associated with traditional stents. Biodegradable stents, which dissolve after serving their purpose, minimize long-term complications and eliminate the need for surgical removal.

These innovations are aligned with the broader shift toward personalized medicine and minimally invasive procedures, offering patients a better treatment experience. Research is actively exploring the potential of combining these technologies to create stents that are more efficient, safer, and more comfortable for patients. This trend in stent technology reflects the overall move towards improving patient outcomes with less invasive and more targeted treatments. The continued development of these cutting-edge stents is expected to drive growth in the market.

Regional Analysis

North America is leading the Stents Market

North America dominated the market with the highest revenue share of 43.5% owing to several key factors. A major contributor was the increasing prevalence of cardiovascular diseases, leading to a higher demand for interventional procedures. Technological advancements also played a crucial role; the introduction of drug-eluting stents (DES) and bioresorbable vascular scaffolds (BVS) enhanced treatment efficacy and patient outcomes. In 2024, DES emerged as the largest revenue-generating product segment in the coronary stents market. Moreover, the presence of leading medical device companies, such as Abbott Laboratories and Medtronic, fostered innovation and expanded the availability of advanced stent technologies.

Regulatory support and improved reimbursement policies further facilitated market growth, making stent procedures more accessible to patients. Additionally, the shift towards minimally invasive procedures, which offer shorter recovery times and reduced complications, contributed to the increased adoption of stents in clinical practice. The growing demand for stents can also be attributed to the increasing focus on preventive healthcare and early disease detection, further driving the market expansion.

The Asia Pacific region is expected to experience the highest CAGR during the forecast period

Asia Pacific is expected to grow with the fastest CAGR owing to the rising burden of cardiovascular diseases, particularly in countries like China and India, which have large patient populations. For example, China accounted for a significant portion of the global coronary stents market revenue in 2024, highlighting its substantial market share. The demand for advanced stent technologies is expected to increase with the aging population and the adoption of Western lifestyles.

Healthcare infrastructure improvements and increased healthcare spending are likely to facilitate the adoption of sophisticated stent technologies. Government initiatives aimed at enhancing healthcare access and quality are projected to support market expansion. Collaborations between international medical device manufacturers and local healthcare providers are expected to introduce innovative stent solutions tailored to the regional market. Additionally, the growing focus on preventive healthcare and early disease detection is likely to drive the demand for stent procedures, further contributing to market growth in the Asia-Pacific region.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherland

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- New Zealand

- Singapore

- Thailand

- Vietnam

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

Key players in the stent market focus on product innovation, strategic partnerships, and expanding their geographic presence to drive growth. They invest heavily in research and development to improve stent design, material quality, and long-term outcomes for patients. Companies collaborate with hospitals and healthcare providers to improve adoption rates and enhance procedural efficacy.

Additionally, they target emerging markets, where rising healthcare infrastructure and awareness increase demand for advanced medical devices. Regulatory approvals and compliance with international standards ensure the continuous advancement and market acceptance of their stent technologies.

Abbott Laboratories, based in Abbott Park, Illinois, is a global healthcare company known for its leadership in medical devices, diagnostics, and pharmaceuticals. The company’s vascular division offers a range of stents, including coronary and peripheral options, aimed at improving patient outcomes.

Abbott is a key player in the stent market, focusing on innovation with devices like the Xience stent, which incorporates cutting-edge technology to enhance safety and effectiveness. Abbott continues to expand its global footprint through strategic acquisitions and partnerships with healthcare institutions, positioning itself as a leader in the cardiovascular space.

Top Key Players in the Stents Market

- Translumina Therapeutics

- Meril Life Science

- Medtronic Plc

- Elixir Medical Corporation

- Boston Scientific Corporation

- Biosensors International Group, Ltd.

- Braun Melsungen AG

- Abbott

Recent Developments

- In September 2024, Translumina Therapeutics entered into a strategic alliance with the renowned German Heart Centre, marking its expansion into the UAE. This partnership focused on creating cutting-edge drug-eluting stents, including a globally recognized stent backed by extensive research and over ten years of clinical validation, ensuring both safety and effectiveness.

- In May 2024, Abbott launched its state-of-the-art coronary stent, the XIENCE Sierra, in India. Engineered to address complex arterial blockages, this stent is designed to improve the safety and efficacy of angioplasty, offering better outcomes for patients requiring artery revascularization.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | US$ 14.8 billion |

| Forecast Revenue (2034) | US$ 21.1 billion |

| CAGR (2025-2034) | 3.6% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments |

| Segments Covered | By Product Type (Vascular Stents (Coronary Stents, Peripheral Stents (Iliac Artery Stents, Renal Artery Stents, Femoral Artery Stents, Carotid Artery Stents, and Other Peripheral Stents), Neurovascular Stents (Intracranial Stents and Flow Diverters))), Non-vascular Stents (Gastrointestinal Stents (Biliary, Pancreatic, Esophageal Stents, Duodenal, and Colonic), Pulmonary (Airway) Stents (Silicone Airway and Metallic Airway), Urological Stents, and Others)), By Material (Metallic Stents and Non-metallic Stents), By End-user (Hospitals, Ambulatory Care Centers (ACS), and Specialty Clinics) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Translumina Therapeutics, Meril Life Science, Medtronic Plc, Elixir Medical Corporation, Boston Scientific Corporation, Biosensors International Group, Ltd., B. Braun Melsungen AG, and Abbott. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |