Quick Navigation

Report Overview

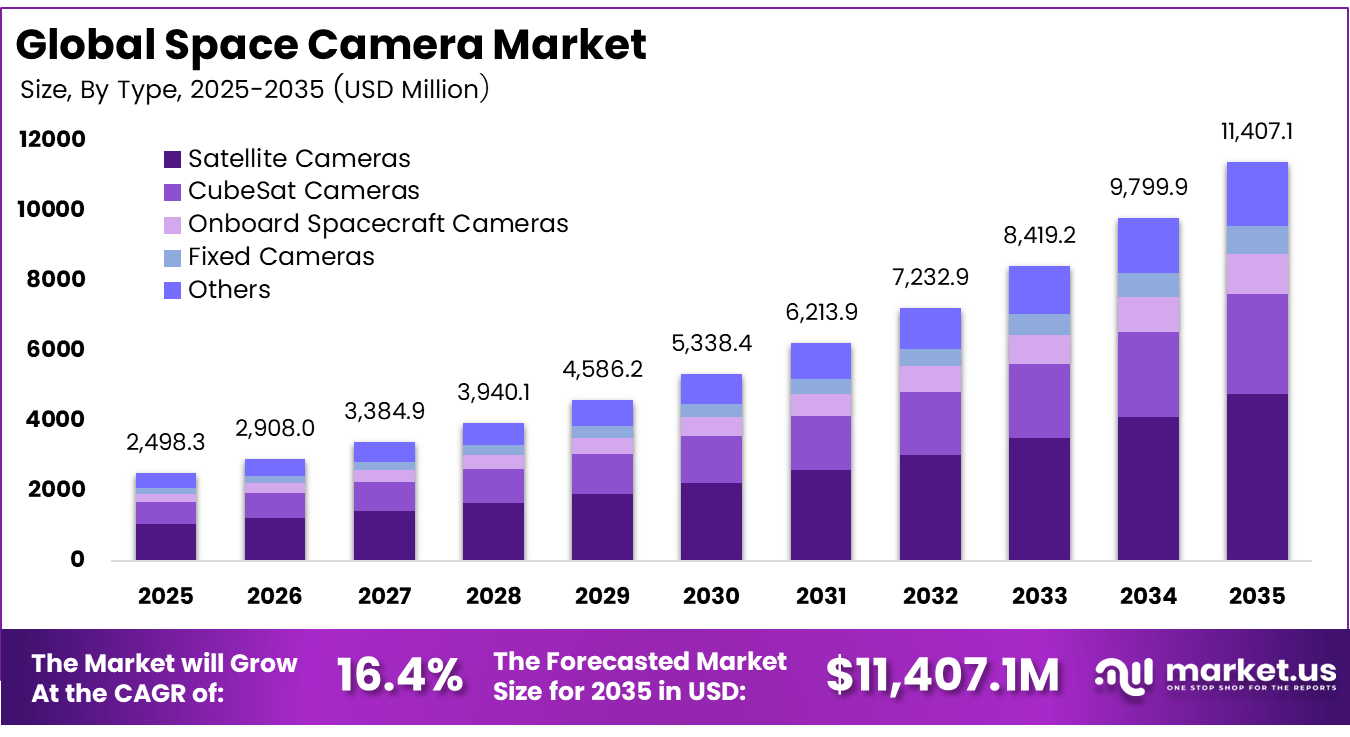

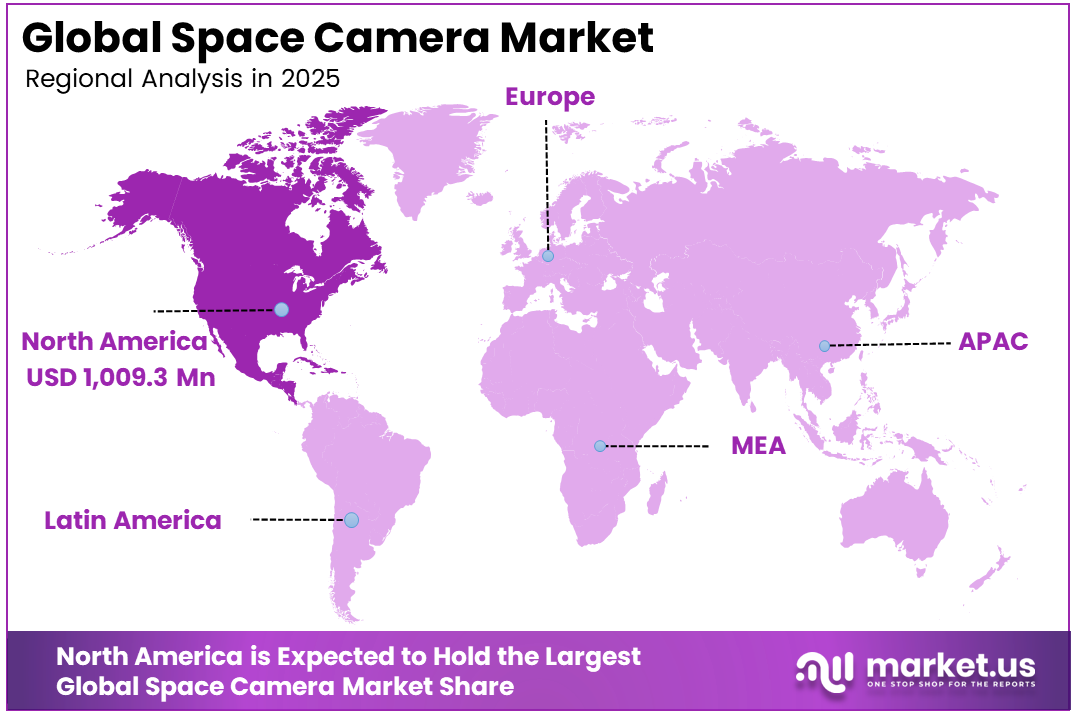

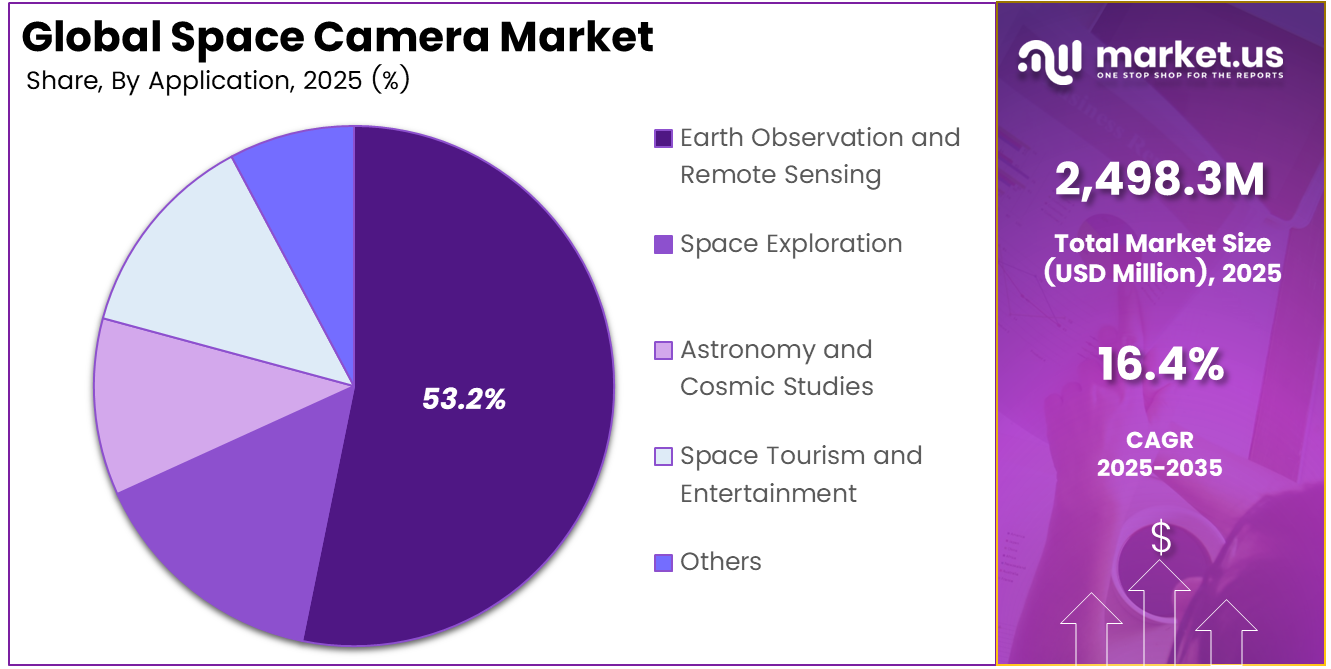

The Global Space Camera Market size is expected to be worth around USD 11,407.1 million by 2035, from USD 2,498.3 million in 2025, growing at a CAGR of 16.4% during the forecast period from 2025 to 2035. North America held a dominant market position, capturing more than a 40.4% share, holding USD 1,009.3 million in revenue.

Space Camera refers to a specialized imaging system designed to capture images and data from space environments. It is used on satellites and spacecraft to observe Earth, planets, and deep space. These cameras are built to withstand radiation, vacuum, and extreme temperatures while delivering clear and reliable images for scientific and operational purposes.

The growth of the space camera market is supported by a sharp rise in satellite launches and expanding planetary missions. In several launch cycles, more than 2,000 satellites are deployed globally, creating strong demand for compact and durable imaging systems that can operate reliably in harsh space environments such as radiation and vacuum.

The market for space cameras is driven by the rising need for accurate satellite imagery across climate monitoring, agriculture, defense, and disaster management. Increasing satellite deployments and demand for frequent Earth observation are supporting growth. Advances in imaging sensors and onboard processing are also enabling better image quality, making space cameras more useful for real-time analysis and long-term monitoring.

Demand is increasing as governments depend on orbital imagery for climate monitoring and disaster response activities. At the same time, commercial users require frequent imaging, with certain locations revisited several dozen times daily. This enables near real-time tracking of agriculture, shipping activity, and urban expansion across multiple global regions.

For instance, in March 2024, Hamamatsu expanded its space-grade image sensor line, promoting radiation-tolerant CCD and CMOS devices for deep-space and high-energy missions in U.S., European, and Japanese programs. By tightening links with satellite primes, the company is positioning its sensors at the core of next-generation astronomy and planetary-probe cameras.

Key Takeaway

- In 2025, the Satellite Cameras segment held a dominant market position, capturing a 41.8% share of the Global Space Camera Market.

- In 2025, the Earth Observation and Remote Sensing segment held a dominant market position, capturing a 53.2% share of the Global Space Camera Market.

- In 2025, the Electro-Optical (EO) Cameras segment held a dominant market position, capturing a 47.6% share of the Global Space Camera Market.

- In 2025, the Government and Military segment held a dominant market position, capturing a 34.9% share of the Global Space Camera Market.

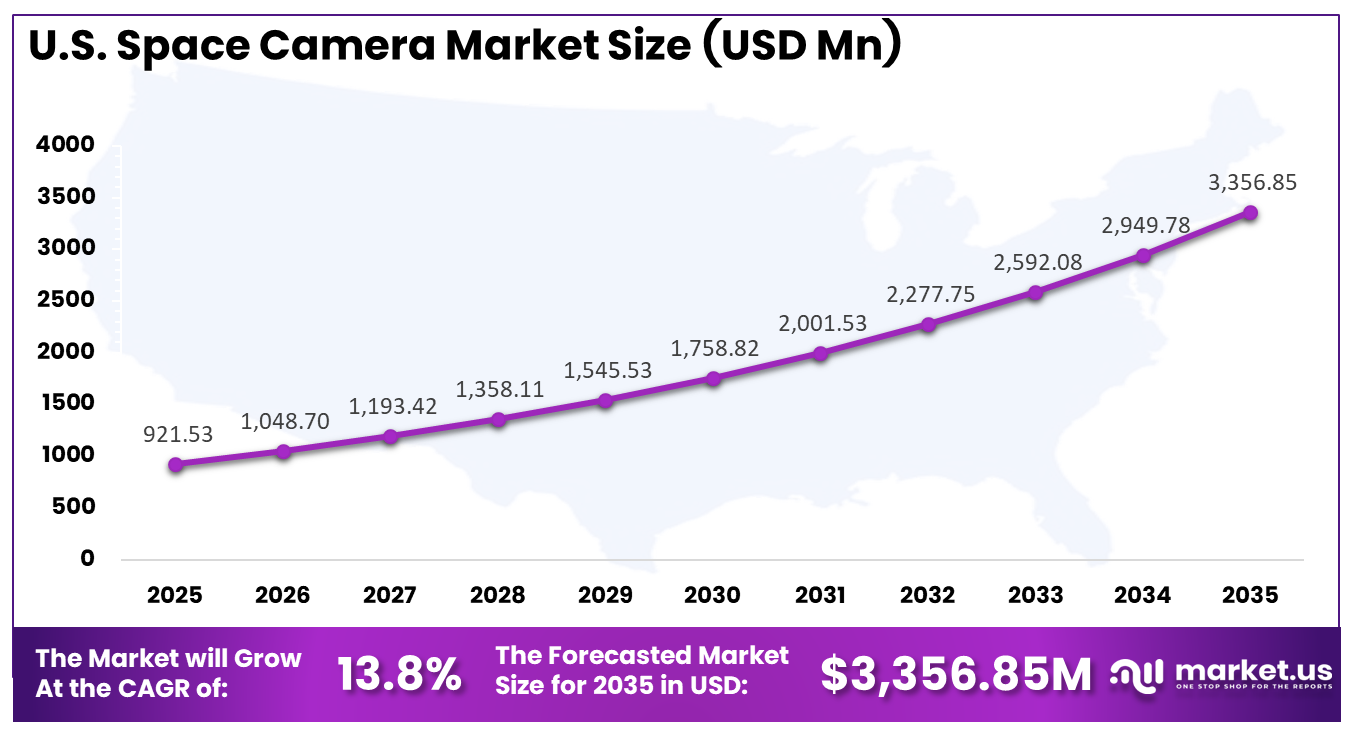

- The U.S. Space Camera Market was valued at USD 921.53 Million in 2025, with a robust CAGR of 13.8%.

- In 2025, North America held a dominant market position in the Global Space Camera Market, capturing more than a 40.4% share.

Role of Generative AI

Generative AI is becoming part of the space imaging workflow by improving image quality before data is transmitted to Earth. It helps clean noisy, low-light, and radiation-affected frames, allowing more usable visual information to be preserved. Some test campaigns have shown usable data rates rising by well over 30%.

Generative models are also helping mission teams test camera systems in virtual environments before final hardware decisions are made. This supports better design validation under difficult space conditions. NASA’s report that 88% of the Perseverance rover driving is autonomous shows how onboard AI is advancing toward camera control and event-based imaging.

Investment and Business Benefits

Investment activity is being directed toward small satellite constellations and AI-enabled onboard analytics. Opportunities are also emerging in radiation-hardened optics and electronics. In addition, downstream analytics platforms are gaining attention as they convert millions of daily images into actionable datasets for sectors such as agriculture, insurance, and infrastructure monitoring.

Operational benefits include faster situational awareness during floods and wildfires, along with accurate tracking of construction progress. Space cameras also enable the precise counting of ships and vehicles. Over time, continuous imaging builds multi-year datasets, generating millions of observations for each region and supporting long-term planning and decision-making.

Regional Analysis

In 2025, North America held a dominant market position in the Global Space Camera Market, capturing more than a 40.4% share, holding USD 1,009.3 million in revenue. This dominance is due to North America’s strong space infrastructure, high satellite deployment activity, and deep investment in defense, Earth observation, and scientific missions. The region benefits from advanced imaging technology development, established launch capabilities, and strong demand for real-time geospatial data. It also has a mature ecosystem of aerospace firms, research institutions, and government agencies, which supports faster innovation, wider adoption of space cameras, and steady commercial expansion across multiple applications.

For instance, in May 2024, Raytheon, an RTX business, launched two next-generation commercial satellite imagers on Maxar’s WorldView Legion satellites, delivering the highest commercially available Earth-observation resolution with frequent revisits over populated regions. These U.S.-built optical systems bolster North American dominance in premium commercial space imaging services.

U.S. Space Camera Market Size

The market for Space Cameras within the U.S. is growing tremendously and is currently valued at USD 921.53 million; the market has a projected CAGR of 13.8%. The market is growing due to rising satellite launches, strong government support for space and defense programs, and increasing use of Earth observation data across agriculture, climate monitoring, and security. Demand is also supported by rapid progress in imaging sensors, onboard processing, and small satellite platforms. In addition, the presence of advanced aerospace infrastructure and continued investment in domestic space technology are helping expand adoption across commercial and public missions.

For instance, in February 2024, BAE Systems finalized its acquisition of Ball Aerospace, integrating a U.S. leader in spacecraft, optical payloads, and imaging instruments into its new Space & Mission Systems sector. With Ball’s long heritage on missions like Landsat imagers and other optical systems, the deal strengthens North America’s industrial base for high-end space cameras.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherlands

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Thailand

- Vietnam

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Type Analysis

In 2025, the Satellite Cameras segment held a dominant market position, capturing a 41.8% share of the Global Space Camera Market. This dominance is due to the growing reliance on satellite-based imaging for continuous global monitoring and mission support. Satellite cameras are designed to operate in extreme space conditions, making them essential for capturing stable and repeatable imagery across long durations in orbit for multiple scientific and security applications.

Their widespread use is also linked to increasing satellite launches and multi-mission deployments. These cameras support diverse functions such as environmental tracking, mapping, and surveillance. Their ability to deliver consistent image quality from orbit ensures they remain a preferred choice across both civil and defense-related space programs globally.

For instance, in March 2026, Surrey Satellite Technology announced its collaboration with the Eric and Wendy Schmidt Observatory System’s Lazuli program, developing the spacecraft platform for one of the most ambitious privately funded space telescopes. The company is creating a platform that will carry the Lazuli space observatory far beyond Earth orbit into deep space, demonstrating SSTL’s expanding capabilities beyond traditional low Earth orbit satellite camera applications.

Application Analysis

In 2025, the Earth Observation and Remote Sensing segment held a dominant market position, capturing a 53.2% share of the Global Space Camera Market. This dominance is due to the strong need for continuous monitoring of Earth systems across land, oceans, and atmosphere. Earth observation applications rely on satellite imagery to track environmental changes, manage natural resources, and support timely responses during disasters and climate-related events across different regions.

The application is further strengthened by growing demand from agriculture, urban planning, and infrastructure monitoring. Remote sensing enables accurate data collection without physical presence, making it highly efficient for large-scale analysis. This supports better planning, policy making, and operational decisions across industries and government agencies worldwide.

For instance, in January 2026, Raytheon Technologies was selected by NASA to build a series of Landsat Next instruments, continuing the company’s heritage in advanced Earth observation systems. This contract follows the successful deployment of imaging instruments for Maxar’s WorldView Legion satellites, which feature innovative telescope designs using novel optical materials that are stronger and lighter than previous generations.

Technology Analysis

In 2025, the Electro-Optical (EO) Cameras segment held a dominant market position, capturing a 47.6% share of the Global Space Camera Market. This dominance is due to the strong capability of electro-optical cameras to capture clear and detailed images in visible and infrared ranges. These systems are widely used where accurate visual interpretation is required, supporting applications such as mapping, surveillance, and environmental observation from space platforms.

Their continued adoption is supported by improvements in sensor performance and image clarity. Electro-optical cameras provide reliable outputs for both scientific and operational missions. Their flexibility in different lighting conditions and compatibility with advanced processing systems make them suitable for a wide range of imaging requirements.

For instance, in March 2026, Dragonfly Aerospace announced a strategic Compatibility Agreement with Unibap Space Solutions, enabling seamless integration between its electro-optical imaging payloads and Unibap’s high-performance edge-computing platforms. This partnership moves the industry beyond image capture to real-time insight through onboard AI capabilities that transform satellite imaging into intelligent decision-making tools.

End-Use Analysis

In 2025, the Government and Military segment held a dominant market position, capturing a 34.9% share of the Global Space Camera Market. This dominance is due to the critical need for secure and reliable imaging for national security and public safety operations. Government and military organizations depend on space-based cameras for surveillance, border monitoring, and strategic planning, ensuring timely and accurate situational awareness across regions.

Their use is also driven by increasing focus on disaster management and environmental monitoring. Space cameras help authorities assess damage, track changes, and respond quickly to emergencies. This supports informed decision-making while improving coordination across defense and civil agencies at national and global levels.

For instance, in April 2026, Lockheed Martin outlined its strategic space technology roadmap, highlighting active manufacturing of 18 Tranche 2 Tracking Layer satellites featuring advanced infrared sensors designed to detect and track hypersonic missile threats. The company successfully launched GPS III SV09 in January 2026, the first in the constellation to host a laser retroreflector array for improved coordinate system measurements.

Key Market Segments

By Type

- Satellite Cameras

- CubeSat Cameras

- Onboard Spacecraft Cameras

- Fixed Cameras

- Others

By Application

- Earth Observation and Remote Sensing

- Space Exploration

- Astronomy and Cosmic Studies

- Space Tourism and Entertainment

- Others

By Technology

- Electro-Optical (EO) Cameras

- Infrared (IR) Cameras

- Multispectral Cameras

- Hyperspectral Cameras

- Others

By End-Use

- Government and Military

- Commercial Enterprises

- Space Agencies

- Research Institutions

Emerging Trends

A major trend is the move from sending all raw images to sending only selected information based on onboard AI filtering. This approach allows cameras to identify meaningful frames before transmission. For large satellite constellations, internal assessments indicate that downlink volume can be reduced by 40–60% without losing analytical usefulness.

Another strong trend is the growing use of compact and modular cameras in CubeSats and nanosatellites. These systems are increasingly built with integrated AI accelerators and software-defined features. Over the last decade, the share of small satellites in total launches has moved well beyond 70%, driving demand for lighter imaging payloads.

Growth Factors

Rising demand for high-resolution Earth observation is a major factor shaping the space camera market. Defense, agriculture, climate monitoring, and insurance are all increasing their dependence on orbital imagery. In several national EO programs, imaging missions already represent more than 50% of operational satellites, showing the strength of this demand.

Technological progress is also supporting faster market growth. Improvements in CMOS sensors, radiation-hardened materials, and onboard processing are reducing the mass and power required per useful pixel. This makes advanced cameras more practical for small satellites and deep space probes, while standard camera bus reuse is increasing year after year.

Market Dynamics

Drivers - Rising Demand for High-Resolution Earth Observation

The market is driven by the increasing need for clear and detailed satellite images across sectors such as agriculture, climate monitoring, and security. High-resolution imagery supports better tracking of land use, weather patterns, and environmental changes, helping organizations make informed and timely decisions at both regional and global levels.

Growing dependence on satellite data for planning and monitoring is further strengthening demand. Governments and businesses require frequent and precise imaging to manage resources, track infrastructure, and respond to emergencies. This consistent need for reliable data is supporting wider adoption of advanced space camera systems across various applications.

For instance, in June 2024, Raytheon Technologies secured a contract worth USD 506 million from NASA to design the Landsat Next Instrument Suite. The next-generation instruments will deliver up to 3 times the spatial, temporal, and spectral resolution of previous versions. Enhanced data collection will improve awareness of water quality, crop production, soil conservation, forest management, and climate change impacts.

Restraint - High Launch Costs

High launch costs remain a key restraint for the space camera market. Sending payloads into orbit requires significant investment in launch services, integration, and testing. These costs can limit the number of missions, especially for smaller organizations or research groups with limited financial resources and budget constraints.

In addition, the cost pressure extends beyond launch to include insurance, mission planning, and maintenance. This creates a barrier to frequent upgrades or replacements of camera systems. As a result, some users delay adoption or rely on shared satellite services instead of investing in dedicated imaging payloads.

For instance, in May 2024, NanoAvionics announced full standardization of all its nano and microsatellite buses, significantly reducing lead times to just 4 months for bus manufacturing. The standardization lowers costs and improves reliability compared to custom-built solutions. This development addresses the challenge of high development expenses by enabling faster and more cost-effective mission launches than ever before.

Opportunities - AI Enhanced Imaging and Analytics

AI-based imaging and analytics present strong growth opportunities in the market. Advanced algorithms can process images directly in orbit, improving clarity and extracting useful insights before data is transmitted to Earth. This helps reduce delays and supports faster decision-making across sectors that depend on timely satellite information.

The integration of AI also enables automated detection of patterns such as crop health, urban expansion, and environmental risks. This creates new value for industries that rely on continuous monitoring. As demand for real-time insights grows, AI-driven imaging solutions are expected to play an important role in expanding market capabilities.

For instance, in January 2025, NanoAvionics partnered with Absolut Sensing to build a demonstration satellite featuring onboard artificial intelligence for autonomous greenhouse gas emission detection. The satellite will enable near-real-time emission detection using cutting-edge AI to process measurements autonomously in orbit. This capability will support a planned 24-satellite constellation for sophisticated local greenhouse gas measurement.

Challenges - Harsh Space Environment

The space environment presents a major challenge for camera systems due to exposure to radiation, vacuum, and extreme temperature variations. These conditions can damage sensitive components and affect image quality over time. Ensuring long-term reliability requires careful design, testing, and use of specialized materials and protective technologies.

Maintaining performance in such conditions also increases complexity in system development. Engineers must balance durability with the size and weight limits of satellites. This makes it difficult to design compact yet robust cameras, especially for smaller missions that require efficient and reliable imaging systems in demanding space conditions.

For instance, in February 2024, Redwire announced its flight-proven Sentinel camera technology would launch aboard Intuitive Machines’ Nova-C lunar lander on the IM-2 mission. The company delivered Terrain Relative Navigation and Hazard Detection cameras designed to withstand the demanding lunar environment. These cameras form part of a technology suite supporting navigation and landing in extreme temperature and radiation conditions.

Key Players Analysis

One of the leading players in October 2024, L3Harris Technologies Inc., won a USD 90 million contract from the U.S. Space Force to deliver next-generation multi-sensor payloads for persistent surveillance. These payloads integrate advanced imaging cameras with other sensors, underlining L3Harris’s importance in high-end defense and intelligence imaging from orbit.

Top Key Players in the Market

- Teledyne Technologies Incorporated

- Hamamatsu Photonics K.K.

- Canon Inc.

- L3Harris Technologies Inc.

- Raytheon Technologies Corporation

- Surrey Satellite Technology Ltd.

- OHB SE

- GOMSpace A/S

- NanoAvionics UAB

- Dragonfly Aerospace (Pty) Ltd.

- Redwire Corporation

- Leonardo S.p.A.

- Thales Alenia Space S.A.S.

- IMENCO AS

- Xinrui Optoelectronics Technology Co., Ltd.

- Pixelteq (Ocean Insight)

- Stemmer Imaging AG

- Quantum Spatial Inc.

- Lockheed Martin Corporation

- Ball Aerospace And Technologies Corp.

- Others

Recent Developments

- In January 2025, Canon Inc. signed an agreement with a European launch provider to supply modular cameras optimized for lunar surface logistics missions. By adapting its sensors for dusty, thermally harsh environments, Canon is positioning its space cameras for upcoming lunar infrastructure projects and commercial cargo services.

- In March 2024, Teledyne Space Imaging introduced upscreened industrial CMOS sensors qualified for orbit, supporting resolutions up to 67 megapixels for Earth-observation, star-tracker, and rover cameras. This move deepens Teledyne’s grip on high-end detectors for Western science, defense, and commercial constellations.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 2,498.3 Million |

| Forecast Revenue (2035) | USD 11,407.1 Million |

| CAGR (2026-2035) | 16.4% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Type (Satellite Cameras, CubeSat Cameras, Onboard Spacecraft Cameras, Fixed Cameras, Others), By Application (Space Exploration, Earth Observation and Remote Sensing, Astronomy and Cosmic Studies, Space Tourism and Entertainment, Others), By Technology (Electro-Optical (EO) Cameras, Infrared (IR) Cameras, Multispectral Cameras, Hyperspectral Cameras, Others), By End-Use (Government and Military, Commercial Enterprises, Space Agencies, Research Institutions) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | Teledyne Technologies Incorporated, Hamamatsu Photonics K.K., Canon Inc., L3Harris Technologies Inc., Raytheon Technologies Corporation, Surrey Satellite Technology Ltd., OHB SE, GOMSpace A/S, NanoAvionics UAB, Dragonfly Aerospace (Pty) Ltd., Redwire Corporation, Leonardo S.p.A., Thales Alenia Space S.A.S., IMENCO AS, Xinrui Optoelectronics Technology Co., Ltd., Pixelteq (Ocean Insight), Stemmer Imaging AG, Quantum Spatial Inc., Lockheed Martin Corporation, Ball Aerospace And Technologies Corp., Others |

| Customization Scope | Customization at the segment and region/country levels will be provided. Moreover, customization can be tailored to the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |