Global Sodium Sulfide Market Size, Share, And Industry Analysis Report By Product Type (Anhydrous, Crystal, Low Ferric), By Application (Paper and Pulp, Water Treatment, Textile, Tanneries, Others), By Region, and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends, and Forecast 2025-2034

- Published date: February 2026

- Report ID: 177793

- Number of Pages: 231

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

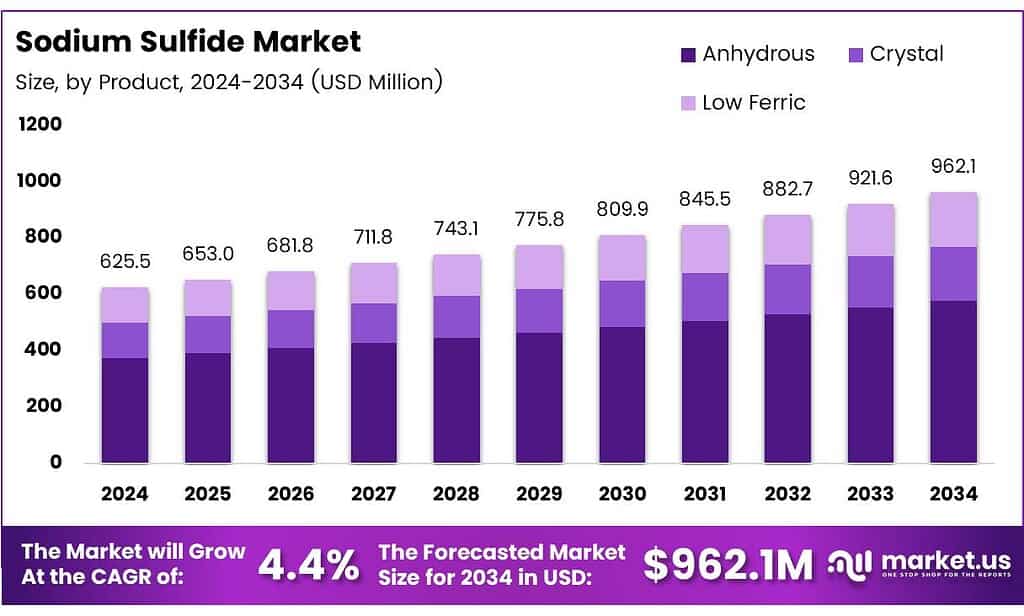

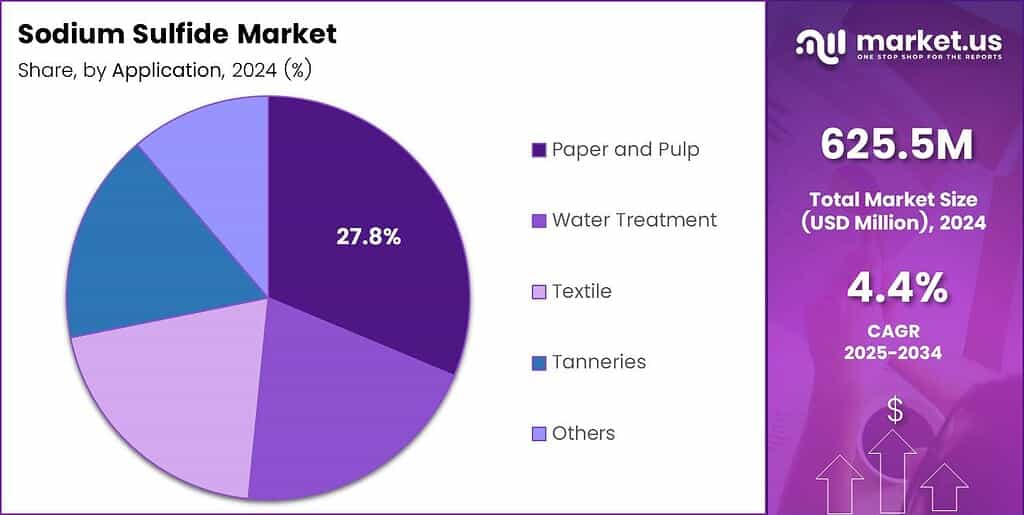

The Global Sodium Sulfide Market size is expected to be worth around USD 962.1 million by 2034 from USD 625.5 million in 2024, growing at a CAGR of 4.4% during the forecast period 2025 to 2034.

Sodium sulfide represents a critical inorganic compound used extensively across industrial chemical processes. Industries manufacture this yellow to red crystalline solid through carbothermic reduction of sodium sulfate using coal. The compound serves multiple sectors requiring sulfur-based chemical derivatives and processing agents.

Paper manufacturing consumes significant sodium sulfide volumes in kraft pulp recovery operations. Textile producers utilize the compound for sulfur dye production and fabric processing. Moreover, leather tanneries depend on sodium sulfide for hide treatment and hair removal processes.

- Sodium Sulphide solution is commonly supplied at 10–12% concentration in tanker loads for industrial applications such as rubber chemicals, sulfur dyes, ore flotation, oil recovery, and detergents. Manufacture and supply Sodium Sulfide 10% Solution across major Indian ports and cities, as well as the UAE, Oman, and Kenya, ensuring ready stock for both bulk and small orders at competitive prices.

Mining operations incorporate sodium sulfide in ore flotation and mineral extraction activities. Water treatment facilities use the compound for heavy metal precipitation and wastewater management. Additionally, chemical manufacturers employ it to produce rubber chemicals and various sulfur-based derivatives.

Industrial demand continues to expand as developing economies scale up leather processing capabilities. Manufacturing sectors in emerging markets drive consumption through increased textile dyeing and chemical production activities. Furthermore, mining operations require steady sodium sulfide supplies for efficient ore processing and metal recovery.

Key Takeaways

- The Global Sodium Sulfide Market is projected to grow from USD 625.5 million in 2024 to USD 962.1 million by 2034 at a CAGR of 4.4%.

- Anhydrous sodium sulfide leads the product segment with 49.6% market share.

- Paper and Pulp application holds 27.8% of the market, representing the largest application segment.

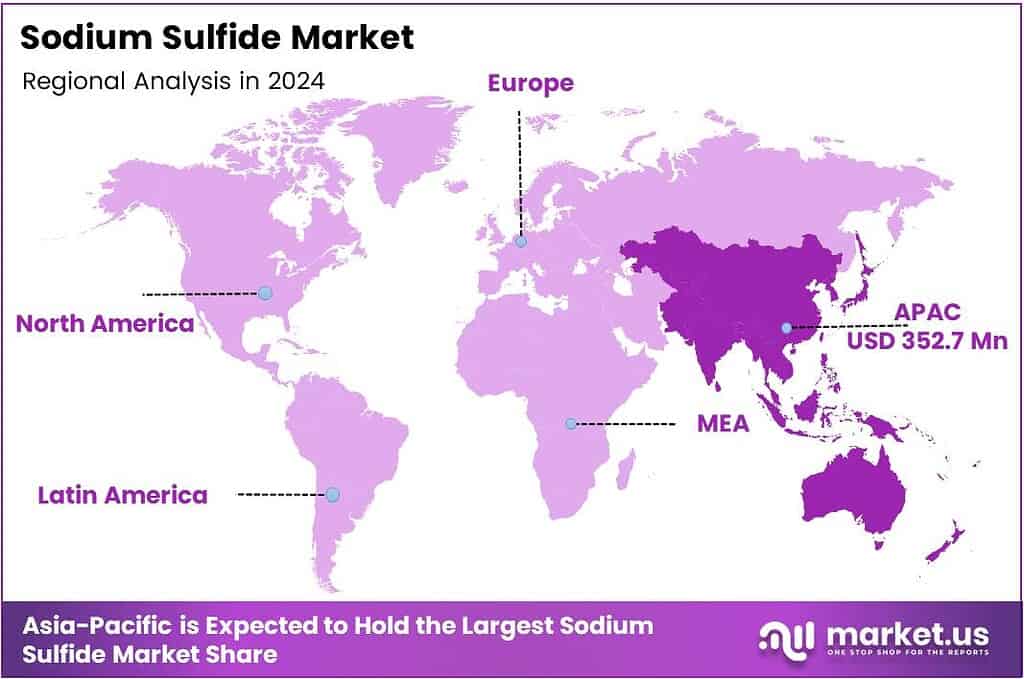

- Asia Pacific dominates the market with 56.4% share, valued at USD 352.7 million.

Product Type Analysis

Anhydrous sodium sulfide dominates with 49.6% due to superior purity levels and efficient handling characteristics.

In 2025, Anhydrous held a dominant market position in the By Product Type segment of the Sodium Sulfide Market, with a 49.6% share. Anhydrous sodium sulfide offers manufacturers higher concentration levels compared to hydrated forms. Industries prefer this variant for applications requiring precise chemical compositions and reduced water content. Consequently, paper mills and chemical producers specify anhydrous grades for kraft recovery and synthesis operations.

Crystal sodium sulfide serves specialized applications where controlled dissolution rates matter significantly. This crystalline form provides easier storage and transportation benefits compared to solution formats. Additionally, textile processors and smaller-scale operations favor crystal sodium sulfide for batch processing requirements. The stable crystal structure ensures a longer shelf life under proper storage conditions.

Low Ferric sodium sulfide meets stringent purity requirements for premium applications demanding minimal iron contamination. Specialty chemical manufacturers and pharmaceutical intermediates production utilize low ferric grades extensively. Moreover, high-value leather tanning operations specify low ferric content to prevent discoloration issues. This premium segment commands higher pricing due to additional purification processing steps.

Application Analysis

Paper and pulp dominate with 27.8% due to extensive usage in kraft recovery and pulping operations.

In 2025, Paper and Pulp held a dominant market position in the By Application segment of the Sodium Sulfide Market, with a 27.8% share. Paper manufacturers consume sodium sulfide primarily in kraft pulping processes for lignin removal. The compound enables efficient chemical recovery systems that recycle cooking liquor in pulp mills. Therefore, expanding paper production capacity directly correlates with increased sodium sulfide consumption patterns.

Water Treatment facilities utilize sodium sulfide for heavy metal precipitation and wastewater neutralization processes. Municipal treatment plants and industrial effluent systems require the compound to remove toxic metals. Additionally, mining operations employ sodium sulfide to treat process water before environmental discharge. Growing environmental regulations drive steady demand growth in this critical application segment.

Textile industries depend on sodium sulfide for sulfur dye production and fabric processing operations. Dyeing facilities use the compound to reduce vat dyes and create vibrant coloration. Moreover, textile manufacturers in developing regions increase sodium sulfide consumption as production scales. This application benefits from expanding garment manufacturing across cost-competitive Asian markets.

Tanneries consume sodium sulfide extensively for hide unhairing and leather processing operations worldwide. Leather manufacturers utilize the compound to remove hair and epidermis from animal hides efficiently. Furthermore, sodium sulfide enables proper hide swelling necessary for subsequent tanning chemical penetration. The growing leather goods market sustains consistent demand from tannery operations.

Key Market Segments

By Product Type

- Anhydrous

- Crystal

- Low Ferric

By Application

- Paper and Pulp

- Water Treatment

- Textile

- Tanneries

- Others

Drivers

Expanding Leather Processing Industry Across Emerging Economies Drives Market Growth

Leather manufacturing sectors in developing nations experience robust expansion driven by export-oriented production strategies. Countries across Asia and Latin America establish new tannery facilities to serve global footwear and accessories markets. Consequently, these operations require substantial sodium sulfide volumes for hide processing and hair removal applications. The compound remains essential for efficient leather production workflows.

- According to World Bank WITS data, Saudi Arabia’s sodium sulfide exports reached USD 27,053.29K and 46,715,600 Kg in 2024, reflecting Middle Eastern production growth. This substantial export volume demonstrates expanded regional manufacturing capacity serving global markets. Strategic investments in chemical production infrastructure enable Saudi producers to compete effectively internationally.

Rising demand from pulp and paper kraft recovery operations sustains steady sodium sulfide consumption patterns. Paper mills depend on the compound for efficient chemical recovery systems in kraft pulping processes. Additionally, textile dyeing facilities increase sodium sulfide usage as sulfur dye applications expand across developing markets. Mining operations similarly require consistent supplies for ore flotation and mineral separation activities.

Restraints

Stringent Environmental and Hazardous Waste Handling Regulations Limit Market Adoption

Governments worldwide implement strict controls governing sodium sulfide production, storage, and transportation activities. Regulatory agencies classify the compound as hazardous, requiring specialized handling procedures and safety equipment. Consequently, manufacturers face increased compliance costs for environmental protection systems and worker safety measures. These regulatory burdens particularly impact smaller producers lacking capital for infrastructure upgrades.

Raw material price volatility creates significant operational challenges for sodium sulfide manufacturers globally. Sulfur and caustic soda input costs fluctuate based on petroleum markets and industrial chemical supply-demand dynamics. Moreover, unpredictable pricing patterns reduce profit margins and complicate long-term supply contract negotiations. Producers struggle to maintain competitive pricing while managing variable production cost structures.

Environmental concerns regarding sulfide waste disposal limit market expansion in environmentally sensitive regions. Communities resist new sodium sulfide production facilities due to potential air and water contamination risks. Additionally, accidental releases can cause severe ecological damage requiring costly remediation efforts. These environmental challenges constrain capacity additions despite growing industrial demand for the compound.

Growth Factors

Rising Adoption in Wastewater Treatment and Heavy Metal Precipitation Accelerates Market Expansion

Municipal water authorities increasingly specify sodium sulfide for removing heavy metals from industrial wastewater streams. The compound effectively precipitates toxic metals, including chromium, lead, and mercury, into manageable solid forms. Therefore, expanding wastewater treatment infrastructure creates substantial new demand across developing urban centers.

- According to World Bank WITS data, Russia’s sodium sulfide exports totaled USD 24,581.84K and 30,999,700 Kg in 2024, indicating strong Eastern European production capacity. This export performance demonstrates Russia’s competitive position in serving European and Asian markets. Regional producers leverage proximity advantages and established distribution networks to capture growing demand.

Textile dyeing operations expand sodium sulfide consumption through increased sulfur dye applications worldwide. Manufacturers prefer sulfur dyes for their excellent wash fastness and economical production characteristics. Additionally, infrastructure development projects boost demand for process chemicals across construction-related industries. Technological advancements in safe handling systems reduce operational risks, encouraging broader industrial adoption.

Emerging Trends

Shift Toward Low-Iron and High-Purity Sodium Sulfide Grades Reshapes Market Landscape

Chemical manufacturers increasingly demand low-iron sodium sulfide grades for specialty applications requiring minimal contamination. Premium leather processors specify high-purity variants to prevent discoloration and quality defects in finished products. Consequently, producers invest in advanced purification technologies to meet stringent customer specifications. This quality upgrading trend supports premium pricing and improved profit margins for specialized producers.

Companies focus on sustainable sulfur recovery integration to reduce environmental footprint and production costs. Modern facilities implement closed-loop sulfur recovery systems, capturing emissions for sodium sulfide synthesis. Moreover, this approach reduces dependence on virgin sulfur inputs while improving environmental compliance. Sustainable production methods enhance corporate social responsibility profiles and regulatory standing.

Asia-Pacific chemical manufacturing hubs undergo significant capacity expansions to serve regional industrial growth. Chinese and Indian producers add production lines responding to domestic and export market opportunities. Additionally, strategic long-term supply agreements with mining companies provide stable revenue streams and demand visibility. These partnerships enable producers to optimize production planning and inventory management efficiently.

Regional Analysis

Asia Pacific Dominates the Sodium Sulfide Market with a Market Share of 56.4%, Valued at USD 352.7 Million

Asia Pacific commands the sodium sulfide market with a 56.4% share valued at USD 352.7 million, driven by extensive chemical manufacturing infrastructure. China leads regional production with large-scale facilities serving the domestic paper, textile, and leather industries. Moreover, India and Southeast Asian nations expand consumption through growing industrial activities. The region benefits from competitive production costs and proximity to end-user markets.

North America maintains a steady sodium sulfide demand driven by established paper manufacturing and mining operations. United States producers serve domestic pulp mills and water treatment facilities requiring consistent chemical supplies. Additionally, Canadian mining operations consume sodium sulfide for ore processing applications. The region emphasizes environmental compliance and safe handling practices across all production facilities.

Europe demonstrates moderate sodium sulfide consumption focused on specialty chemical applications and wastewater treatment. German and French manufacturers supply paper mills and textile processors with high-purity grades. Moreover, stringent environmental regulations drive demand for water treatment applications across municipal facilities. The region prioritizes sustainable production methods and reduced environmental impact.

Middle East & Africa experience growing sodium sulfide demand through expanding industrial chemical production capacity. Saudi Arabian producers leverage abundant sulfur resources to manufacture sodium sulfide for export markets. Additionally, South African mining operations consume the compound for ore flotation applications. Infrastructure development projects across the region support steady market growth.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Henan Province Nafine Chemical Industry Group Co., Ltd. operates as a major sodium sulfide producer serving Chinese domestic and international markets. The company maintains large-scale production facilities with integrated sulfur sourcing capabilities. Moreover, Nafine supplies paper mills, textile manufacturers, and leather processors across the Asia Pacific. Their vertical integration strategy enables competitive pricing and reliable supply chains for high-volume customers.

Ineos Calabrian represents a significant European sodium sulfide manufacturer with advanced production technologies. The company specializes in high-purity grades meeting stringent quality specifications for specialty chemical applications. Additionally, Ineos Calabrian serves the paper manufacturing and water treatment sectors across European markets. Their emphasis on environmental compliance and safety standards supports premium market positioning.

Chemical Products Corporation provides sodium sulfide solutions to North American industrial customers through established distribution networks. The company focuses on consistent quality and reliable delivery for mining and water treatment applications. Moreover, Chemical Products Corporation maintains technical support capabilities, assisting customers with process optimization. Their regional presence enables responsive customer service and rapid order fulfillment.

American Elements manufactures specialized sodium sulfide products for research and advanced industrial applications worldwide. The company offers high-purity and low-ferric grades serving pharmaceutical intermediates and specialty chemical synthesis. Additionally, American Elements provides custom formulations meeting specific customer requirements. Their technical expertise and quality focus attract customers requiring premium-grade sodium sulfide products.

Top Key Players in the Market

- Akshya Minerals and Chemicals

- American Elements

- Athiappa Chemicals

- Chemical Products Corporation

- Emco Dyestuff Pvt. Ltd

- Henan Province Nafine Chemical Industry Group Co., Ltd.

- Ineos Calabrian

- Innova Priority Solutions

- Kemcore

- Nanoshel

Recent Developments

- In 2025, American Elements will offer sodium sulfide in various forms, including high-purity, submicron, and nanopowder variants, primarily for industrial and research applications. They also provide sodium hydrogen sulfide in similar high-purity formats.

- In 2025, Athiappa Chemicals, established in 1986, manufactures sodium sulphide alongside barium carbonate and other chemicals. The company participated as a domestic producer in India’s Directorate General of Trade Remedies (DGTR) anti-dumping investigation on barium carbonate imports from China, where sodium sulphide is noted as a by-product in their production process.

Report Scope

Report Features Description Market Value (2024) USD 625.5 Million Forecast Revenue (2034) USD 962.1 Million CAGR (2025-2034) 4.4% Base Year for Estimation 2024 Historic Period 2020-2023 Forecast Period 2025-2034 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Product Type (Anhydrous, Crystal, Low Ferric), By Application (Paper and Pulp, Water Treatment, Textile, Tanneries, Others) Regional Analysis North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) Competitive Landscape Akshya Minerals and Chemicals, American Elements, Athiappa Chemicals, Chemical Products Corporation, Emco Dyestuff Pvt. Ltd, Henan Province Nafine Chemical Industry Group Co., Ltd., Ineos Calabrian, Innova Priority Solutions, Kemcore, Nanoshel Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF)

-

-

- Akshya Minerals and Chemicals

- American Elements

- Athiappa Chemicals

- Chemical Products Corporation

- Emco Dyestuff Pvt. Ltd

- Henan Province Nafine Chemical Industry Group Co., Ltd.

- Ineos Calabrian

- Innova Priority Solutions

- Kemcore

- Nanoshel

Our Clients

- 177793

- February 2026