Quick Navigation

- Report Overview

- Key Takeaways

- Business Benefits of Smart Energy

- By Product Analysis

- By Component Solution Analysis

- By Application Analysis

- By End-user Analysis

- Key Market Segments

- Driving Factors

- Restraining Factors

- Growth Opportunity

- Latest Trends

- Regional Analysis

- Key Players Analysis

- Recent Developments

- Report Scope

Report Overview

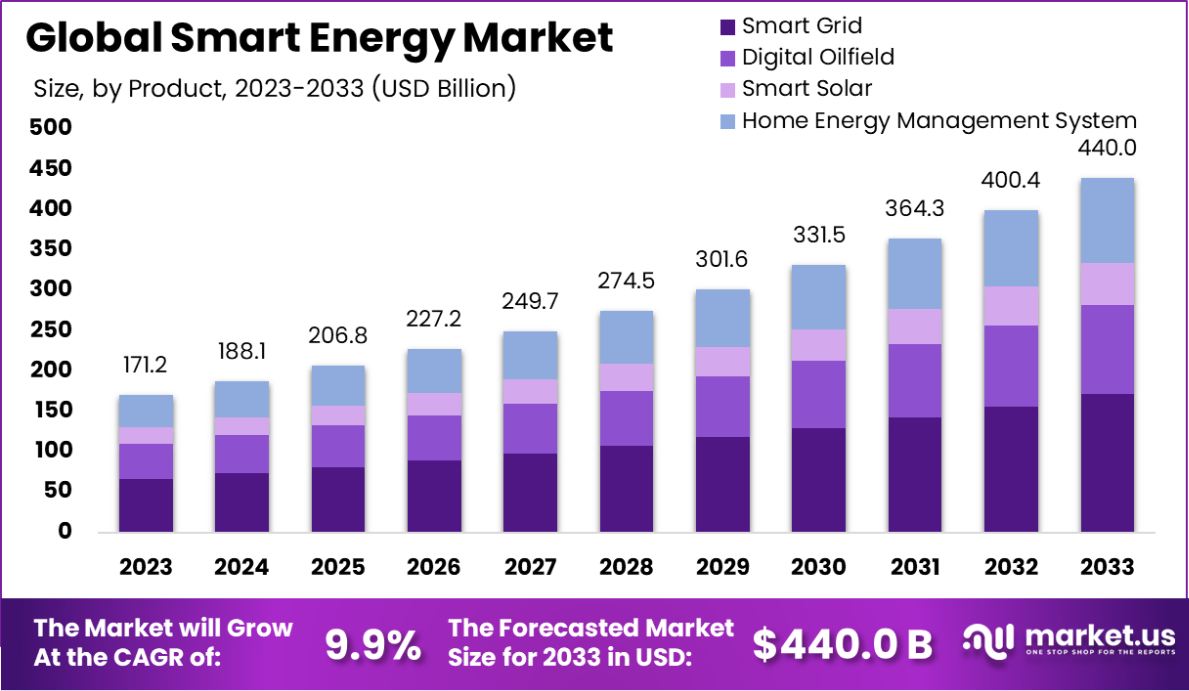

The Global Smart Energy Market is expected to be worth around USD 440.0 Billion by 2033, up from USD 171.2 Billion in 2023, and grow at a CAGR of 9.9% from 2024 to 2033. North America holds 41.6% of the Smart Energy Market, USD 71.2 Bn.

Smart Energy refers to the use of digital technology to optimize the production and distribution of energy. It involves integrating smart grids, renewable energy sources, and energy-efficient technologies to enhance the efficiency of energy systems, reduce costs, and minimize environmental impacts. Smart energy systems can adapt to changes in energy demand and supply, improve grid reliability, and facilitate real-time energy management.

Smart Energy Market encompasses the technologies and services that support the development and deployment of smart energy systems. This market includes smart meters, smart appliances, renewable energy technologies, energy management systems, and services that enhance energy efficiency and grid management.

As countries prioritize sustainable energy solutions, this market is poised for significant growth driven by government regulations, technological advancements, and increasing environmental awareness.

The smart energy market is expanding due to advancements in IoT and AI technologies, which enhance grid management and energy efficiency. Additionally, global efforts to reduce carbon emissions are boosting the adoption of smart energy solutions.

Increasing energy consumption and the need for sustainable energy practices are driving demand for smart energy technologies. Urbanization and industrialization, especially in developing regions, further escalate this demand.

There is substantial opportunity to develop integrated systems that combine renewable energy sources with smart grids. Also, evolving consumer preferences towards sustainable and energy-efficient products present a lucrative market for smart energy innovations.

The Smart Energy Market, particularly advanced metering infrastructure (AMI), continues to show robust growth, reflecting an increasing commitment to modernizing energy distribution and enhancing consumer engagement.

In 2022, U.S. electric utilities reported approximately 119 million AMI installations, which account for about 72% of all electric meters. This widespread adoption underscores the utility sector’s strategic shift towards more efficient grid management and responsive energy usage monitoring.

Residential consumers represent the lion’s share of this adoption, with 88% of all AMI installations geared towards this segment. This indicates a significant penetration of smart technologies in the domestic sphere, involving around 73% of all residential electric meters.

The transition to AMI systems is a critical step in achieving enhanced energy efficiency and reliability, providing utilities and consumers alike with real-time data to better manage consumption and reduce energy wastage.

This integration of smart technologies is not only pivotal for advancing grid modernization but also plays a crucial role in supporting the shift toward renewable energy sources. By enabling more precise demand response and load management, AMI systems are foundational in the push toward a more sustainable and resilient energy ecosystem.

The continued growth in AMI installations is expected to further catalyze innovations in smart grid technologies, driving both market expansion and environmental benefits.

Key Takeaways

- The Global Smart Energy Market is expected to be worth around USD 440.0 Billion by 2033, up from USD 171.2 Billion in 2023, and grow at a CAGR of 9.9% from 2024 to 2033.

- Smart grids dominate the Smart Energy Market with a substantial 39.1% share.

- Component solutions hold a significant 67.4% of the Smart Energy Market.

- Energy generation accounts for 29.4% of the market, emphasizing its pivotal role.

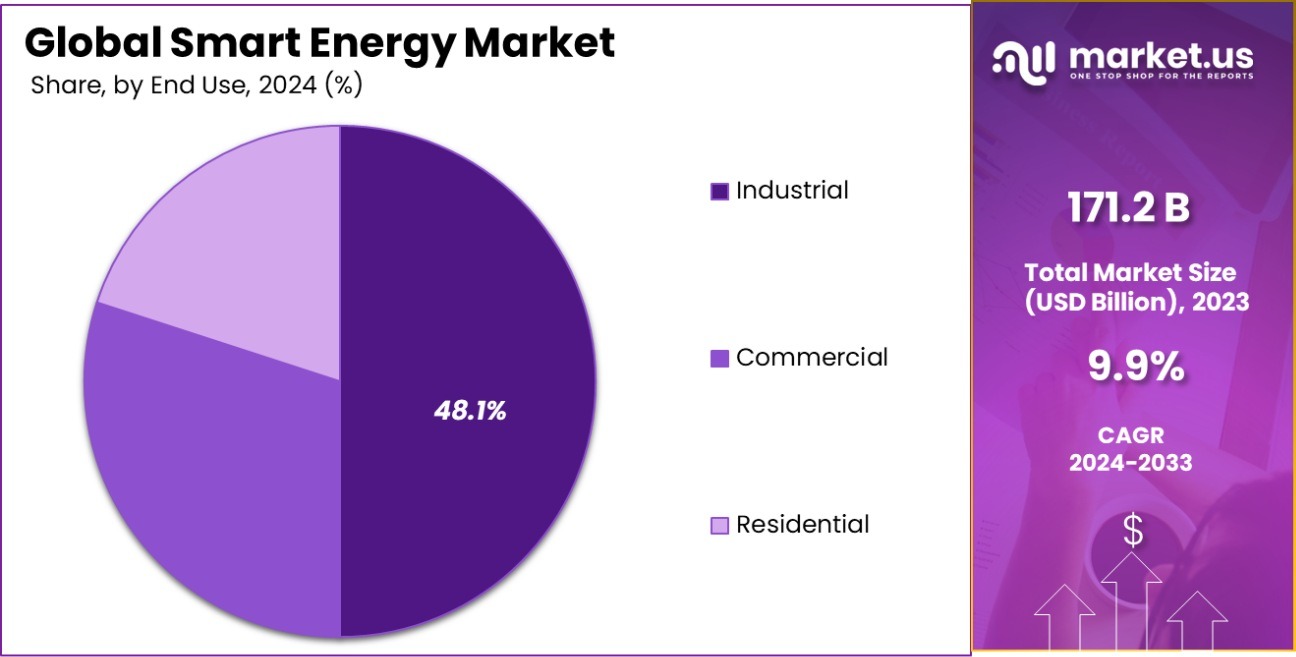

- Industrial users lead, occupying 48.1% of the Smart Energy Market.

- In 2023, North America held 41.6% of the Smart Energy Market, totaling USD 71.2 billion.

Business Benefits of Smart Energy

The adoption of smart energy systems offers substantial business benefits, pivotal in driving operational efficiency and sustainability. Firstly, smart energy solutions facilitate significant cost reductions through optimized energy consumption. By utilizing intelligent algorithms and IoT devices, these systems can analyze usage patterns and adjust energy outputs accordingly, minimizing waste and reducing utility expenses.

Additionally, smart energy technologies enhance reliability and energy supply quality. They are capable of identifying and rectifying inefficiencies and potential faults in real-time, thereby reducing downtime and maintenance costs. This proactive approach to energy management not only extends the lifespan of equipment but also ensures consistent operational conditions.

Environmental sustainability is another critical advantage. Businesses employing smart energy solutions contribute to reducing carbon footprints by optimizing energy use and integrating renewable energy sources. This alignment with global sustainability goals not only enhances corporate reputation but also complies with increasing regulatory demands on energy efficiency and environmental responsibility.

Furthermore, smart energy systems provide data-driven insights that enable businesses to make informed decisions regarding energy management and future investments. This strategic capability can be instrumental in gaining competitive advantages, as it allows companies to anticipate market trends and adapt swiftly to changing energy landscapes.

By Product Analysis

Smart Grid dominates the Smart Energy Market with a significant 39.1% share.

In 2023, Smart Grid held a dominant market position in the By Product segment of the Smart Energy Market, with a 39.1% share. This technology has been pivotal in transforming how energy is distributed and managed, leveraging advanced metering infrastructure, grid automation, and real-time data analytics to enhance efficiency and reliability.

Following closely, Digital Oilfield technology accounted for 25.2% of the market, integrating IoT and AI to optimize oil production and reduce environmental impact.

Smart Solar emerged as another significant segment, capturing 18.9% of the market. This sector focuses on using advanced photovoltaic systems that incorporate smart meters and grid-integrated technologies to maximize the efficiency of solar energy production and distribution.

Lastly, the Home Energy Management Systems (HEMS) held a 16.8% share, reflecting a growing consumer interest in managing energy consumption through intelligent devices that monitor and control energy use in real time. This segment is expected to grow as consumers become more aware of their energy consumption patterns and seek solutions that offer cost savings and sustainability.

By Component Solution Analysis

Component Solutions lead market components, capturing a dominant 67.4% of the sector.

In 2023, Solution held a dominant market position in the “By Component” segment of the Smart Energy Market, with a 67.4% share. This significant market control underscores Solution’s pivotal role in the deployment and management of smart energy technologies.

Following the Solution, Smart Meters emerged as a crucial component, enabling real-time data collection and enhanced energy distribution efficiency. Smart Meters accounted for a substantial market share, reflecting the growing adoption of automated meter reading and management systems across residential, commercial, and industrial sectors.

Data and Device Management systems also captured a notable segment of the market, driven by the need for sophisticated data analytics tools to optimize energy consumption and manage network operations effectively. Similarly, PV Monitoring systems have been integral in boosting the performance and reliability of photovoltaic installations, contributing positively to the market growth.

Smart Energy Storage solutions, recognized for their ability to stabilize grids and manage energy loads, have seen increasing investments, which is indicative of a shift towards more sustainable energy solutions.

The “Others” category, comprising various emerging technologies and innovations, along with Services, which include installation, maintenance, and consulting, round out the remaining market segments, each playing a vital role in the evolving landscape of the smart energy sector.

By Application Analysis

In applications, Energy Generation holds a 29.4% stake in the Smart Energy Market.

In 2023, Energy Generation held a dominant market position in the “By Application” segment of the Smart Energy Market, with a 29.4% share. This sector’s prominence is underscored by the escalating demand for renewable and sustainable power sources, which are integral to modern energy policies worldwide.

Following closely, Energy Consumption accounted for a 25.1% market share, driven by the increasing adoption of smart devices and IoT technologies that optimize energy use in residential and commercial settings.

Energy Transmission and Energy Distribution also played critical roles, capturing 19.6% and 15.2% of the market, respectively. These segments are pivotal in enhancing grid efficiency and reliability through advanced technologies like smart grids and real-time data monitoring.

Lastly, Energy Storage, which secured a 10.7% share, has been gaining traction due to its importance in balancing supply and demand, stabilizing renewable energy outputs, and improving overall energy management systems. Together, these segments underline a shifting landscape in the Smart Energy Market, focusing on efficiency and sustainability.

By End-user Analysis

Industrial end-users lead in Smart Energy usage, accounting for 48.1% of the market.

In 2023, Industrial held a dominant market position in the End-user segment of the Smart Energy Market, with a 48.1% share. This segment’s robust performance is driven by the widespread adoption of smart technologies aimed at enhancing efficiency and reducing operational costs in manufacturing and production facilities.

As industries increasingly focus on sustainable practices, the integration of smart energy solutions has become crucial, further propelling this segment’s growth.

The Commercial segment also showed significant activity, accounting for 29.6% of the market. The adoption in this segment is fueled by the growing need for energy management solutions in office buildings, retail spaces, and other commercial establishments. These solutions not only help in controlling energy consumption but also in adhering to regulatory standards and achieving environmental sustainability goals.

Lastly, the Residential segment captured 22.3% of the market. Homeowners are turning towards smart energy systems to reduce bills and increase energy independence. This trend is supported by the rising availability of user-friendly technologies that allow for more efficient management of home energy usage, such as smart thermostats and renewable energy systems.

Each segment’s growth is influenced by consumer awareness and technological advancements, which are expected to drive further market expansion.

Key Market Segments

By Product

- Smart Grid

- Digital Oilfield

- Smart Solar

- Home Energy Management System

By Component

- Solution

- Smart Meters

- Data And Device Management

- PV Monitoring

- Smart Energy Storage

- Others

- Services

By Application

- Energy Generation

- Energy Transmission

- Energy Distribution

- Energy Consumption

- Energy Storage

- Others

By End-user

- Industrial

- Commercial

- Residential

Driving Factors

Increased Demand for Renewable Energy Sources

As global awareness of environmental issues rises, the demand for renewable energy sources has surged, making it a primary driving factor in the Smart Energy Market. Consumers and corporations alike are shifting towards sustainable energy solutions, including smart solar and wind power, which are complemented by smart energy systems that optimize usage and distribution.

This shift not only helps reduce carbon footprints but also decreases dependence on non-renewable energy sources, thereby fueling the growth of the smart energy sector.

Advancements in IoT and Connectivity Technology

The integration of Internet of Things (IoT) technology in energy management systems is revolutionizing the Smart Energy Market. IoT devices enable real-time monitoring and management of energy usage, making systems more efficient and responsive.

This technological advancement allows for the automation of energy-saving tasks and improves the accuracy of data collection and analysis, leading to more informed decisions on energy use. As connectivity technology continues to evolve, the potential for smarter energy solutions grows, driving further market expansion.

Government Policies and Incentives for Energy Efficiency

Governmental regulations and incentives play a crucial role in driving the adoption of smart energy solutions. Policies aimed at reducing energy consumption and minimizing environmental impact encourage both businesses and private consumers to invest in smart energy technologies.

These incentives often come in the form of tax rebates, grants, or subsidies, which lower the cost barrier for new technology adoption. Such governmental support not only promotes wider usage of smart energy systems but also stimulates technological innovations within the market.

Restraining Factors

High Initial Costs of Smart Energy Systems

One of the significant restraining factors for the Smart Energy Market is the high initial investment required for implementing smart energy solutions. The cost of advanced technologies, including smart meters, sensors, and energy management software, can be prohibitively expensive for small businesses and residential users.

This financial barrier often delays or prevents the adoption of these technologies, limiting market growth. Despite the long-term savings these systems can offer, the upfront costs remain a major hurdle for many potential users.

Complexity of Installation and Integration

The integration and installation of smart energy systems pose another challenge. These systems often require significant changes to existing infrastructure, which can be complex and disruptive. The need for specialized skills and knowledge for installation and maintenance further complicates the process, deterring many from upgrading to smart systems.

This complexity not only affects the adoption rate among new users but also limits the expansion of smart energy technologies in areas with older infrastructure or less technical expertise.

Data Security and Privacy Concerns

Data security and privacy issues are critical concerns in the Smart Energy Market. Smart energy solutions involve the collection and analysis of large amounts of data, which can include sensitive information about user behavior and energy usage.

The potential for data breaches or unauthorized access raises significant privacy concerns, making consumers hesitant to adopt these technologies. Ensuring robust cybersecurity measures and transparent data handling practices is essential to alleviate these fears and foster greater trust in smart energy technologies.

Growth Opportunity

Expansion into Emerging Markets with Rising Energy Needs

Emerging markets present a significant growth opportunity for the Smart Energy Market. These regions often experience rapid urbanization and industrialization, leading to increased energy demands. By introducing smart energy solutions, companies can help these areas optimize energy usage and support sustainable development.

The potential for growth in these markets is enhanced by the lack of entrenched, outdated infrastructure, which allows for the direct implementation of advanced technologies, bypassing traditional systems and potentially leapfrogging to more efficient energy management practices.

Development of Consumer-Friendly Energy Management Tools

There is a growing opportunity in the development and distribution of consumer-friendly energy management tools. As more individuals become conscious of their energy consumption and its impact, the demand for easy-to-use technologies that help manage and reduce personal energy use rises.

Innovations such as smartphone apps that provide real-time energy consumption data or allow for remote control of home energy systems can tap into the consumer market more effectively. These tools not only enhance consumer engagement but also drive the adoption of smart energy solutions at the residential level.

Partnerships between Technology and Energy Companies

Forging partnerships between technology companies and traditional energy providers is a burgeoning opportunity that can drive the growth of the Smart Energy Market. These collaborations can harness the technological expertise of tech companies with the infrastructure and consumer base of energy firms, leading to innovative solutions that enhance energy efficiency and integration.

Such partnerships can also facilitate the sharing of resources, reduce costs, and speed up the deployment of smart energy technologies across different regions and consumer bases. This cooperative approach can significantly amplify market reach and impact.

Latest Trends

Integration of Artificial Intelligence in Energy Systems

The integration of artificial intelligence (AI) into energy systems is a leading trend in the Smart Energy Market. AI enhances the ability to analyze energy usage patterns and optimize power distribution, which can significantly reduce waste and improve efficiency.

This technology allows for predictive maintenance and automated adjustments based on real-time data, leading to more reliable and efficient energy management. As AI technology evolves, its application in smart energy systems is expected to become more widespread, driving further innovations and efficiencies in this sector.

Rise of Distributed Energy Resources (DERs)

The adoption of distributed energy resources (DERs) like solar panels, wind turbines, and battery storage systems is rapidly becoming a trend. These resources allow consumers and businesses to produce their own energy, reducing reliance on traditional power grids and fostering greater energy independence.

The integration of DERs with smart energy systems facilitates better energy management and distribution, aligning with the growing preference for decentralized and sustainable energy solutions. This trend is particularly pronounced in areas with high electricity costs or unreliable grid infrastructure.

Growth of Electric Vehicle (EV) Integration with Smart Grids

Electric vehicles (EVs) are increasingly being integrated with smart grid technology, a trend that’s shaping the future of the Smart Energy Market. Smart grids are capable of supporting the high power demands of EV charging while managing the load to prevent grid overloads.

This integration also paves the way for innovations like vehicle-to-grid (V2G) systems, where EVs can return energy to the grid during peak times. As the adoption of EVs continues to grow, their integration with smart energy systems is expected to become more critical, opening new avenues for energy management and efficiency.

Regional Analysis

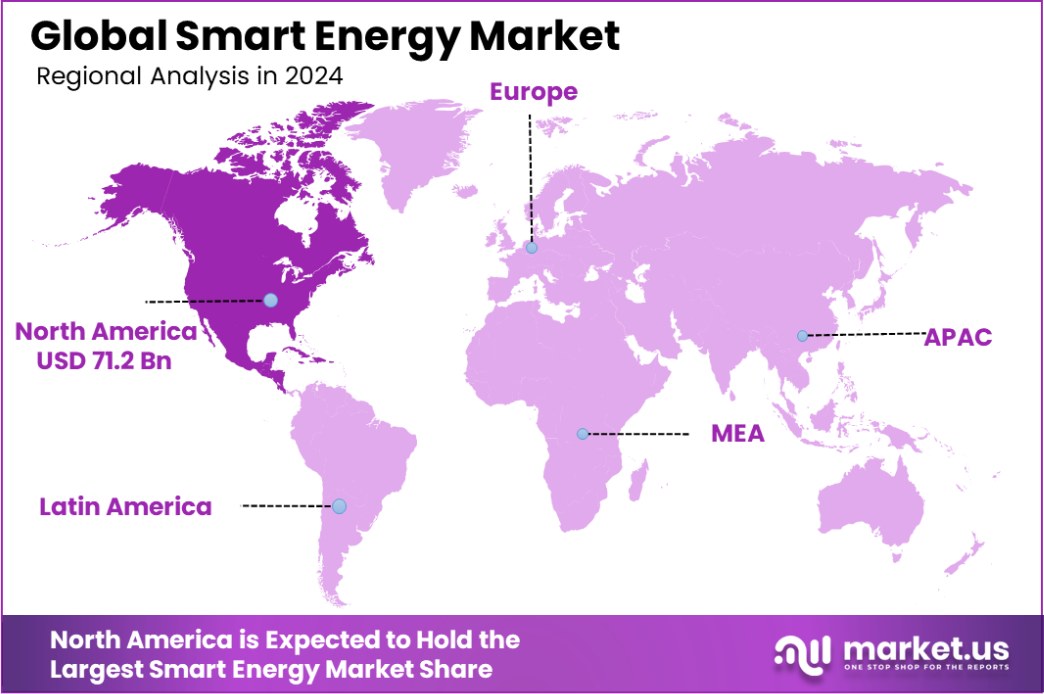

In 2023, North America held 41.6% of the Smart Energy Market, valued at USD 71.2 billion.

In the Smart Energy Market, North America emerges as the dominant region, commanding a 41.6% share with a market value of USD 71.2 billion. This leadership stems from robust investments in smart grid technology and a high adoption rate of smart meters and renewable energy sources across the U.S. and Canada.

Europe follows, driven by stringent environmental regulations and government initiatives promoting energy efficiency. The region has rapidly adopted smart energy solutions to meet its ambitious sustainability goals, further supported by substantial technological advancements in countries like Germany and the UK.

Asia Pacific is witnessing the fastest growth in the Smart Energy Market, thanks to increasing energy demand fueled by rapid urbanization and industrialization, particularly in China and India. These economies are investing heavily in smart infrastructure to manage energy consumption efficiently and sustain economic growth.

Meanwhile, the Middle East & Africa, and Latin America are gradually embracing smart energy technologies. In these regions, growth is spurred by the need to modernize aging energy infrastructure and increase energy access in remote areas, although market penetration remains lower compared to other global regions.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

The global Smart Energy Market in 2023 is characterized by intense competition and significant innovation driven by a mix of established conglomerates and emerging technology-focused companies. Industry leaders like Schneider Electric, Siemens AG, and ABB Ltd. dominate the market with their advanced energy management solutions and extensive global presence.

Schneider Electric continues to push the boundaries of energy efficiency with its EcoStruxure platform, while Siemens’ digital grid technologies and ABB’s automation expertise maintain their competitive edge.

General Electric (GE) and Honeywell International Inc. remain pivotal in integrating renewable energy and smart grid technologies, leveraging their deep expertise in industrial systems. Meanwhile, Eaton Corporation, Itron Inc., and Landis+Gyr are spearheading innovation in smart metering and grid infrastructure. Their solutions cater to increasing demands for real-time energy monitoring and efficiency.

Tech giants like Oracle Corporation, Cisco Systems, and IBM bring cutting-edge software, IoT, and data analytics capabilities into the smart energy space. IBM’s AI-driven energy solutions and Cisco’s IoT connectivity play pivotal roles in enabling energy optimization at scale.

Emerging players such as Grid4C, BuildingIQ, and Watty are disrupting the market with AI-powered predictive energy analytics and user-friendly energy management tools. On the other hand, renewable energy leaders like NextEra Energy, Enel X, and Octopus Energy Group drive market growth through innovative approaches to energy distribution and storage.

Lastly, Japanese giants Toshiba and Mitsubishi Electric Corporation strengthen their positions by focusing on advanced technologies for grid modernization and renewable integration, especially in Asia. The competitive landscape remains vibrant, underscoring the market’s dynamic nature.

Top Key Players in the Market

- Schneider Electric

- Siemens AG

- ABB Ltd.

- General Electric (GE)

- Honeywell International Inc.

- Eaton Corporation

- Itron Inc.

- Landis+Gyr

- Oracle Corporation

- Cisco Systems

- IBM

- Grid4C

- Enel X (Enel Group)

- Octopus Energy Group

- NextEra Energy

- BuildingIQ

- Watty

- Capgemini

- Toshiba

- Mitsubishi Electric Corporation

Recent Developments

- In 2023, Schneider Electric emphasized the rapid deployment of smart grids to enhance energy efficiency and integrate renewable energy. Innovations unveiled at Enlit Europe 2023, like the RM AirSeT and EcoStruxure Microgrid Flex, are key to their strategy for modernizing grid infrastructure and promoting sustainable energy transitions

- In 2023, Siemens AG’s Smart Infrastructure division achieved significant growth and profitability in the smart energy sector. Throughout the fiscal year, the division experienced an 11% increase in revenue, totaling €77.8 billion, with the profit margin for its industrial business climbing to 15.4%. Siemens AG focused on enhancing its digital business, which grew by 12% to €7.3 billion, surpassing its annual growth target.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2023) | USD 171.2 Billion |

| Forecast Revenue (2033) | USD 440.0 Billion |

| CAGR (2024-2033) | 9.9% |

| Base Year for Estimation | 2023 |

| Historic Period | 2019-2022 |

| Forecast Period | 2024-2033 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Product (Smart Grid, Digital Oilfield, Smart Solar, Home Energy Management System), By Component (Solution (Smart Meters, Data And Device Management, PV Monitoring, Smart Energy Storage, Others), Services), By Application (Energy Generation, Energy Transmission, Energy Distribution, Energy Consumption, Energy Storage, Others), By End-user (Industrial, Commercial, Residential) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Schneider Electric, Siemens AG, ABB Ltd., General Electric (GE), Honeywell International Inc., Eaton Corporation, Itron Inc., Landis+Gyr, Oracle Corporation, Cisco Systems, IBM, Grid4C, Enel X (Enel Group), Octopus Energy Group, NextEra Energy, BuildingIQ, Watty, Capgemini, Toshiba, Mitsubishi Electric Corporation |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |