Skin Cancer Treatment Market By Type (Melanoma and Non-Melanoma), By Therapy (Targeted Therapy, Immunotherapy, and Chemotherapy), By Distribution Channel (Hospitals Pharmacies, Online Providers, and Retail Pharmacies), Region and Companies – Industry Segment Outlook, Market Assessment, Competition Scenario, Trends and Forecast 2025-2034

- Published date: July 2025

- Report ID: 152445

- Number of Pages: 307

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

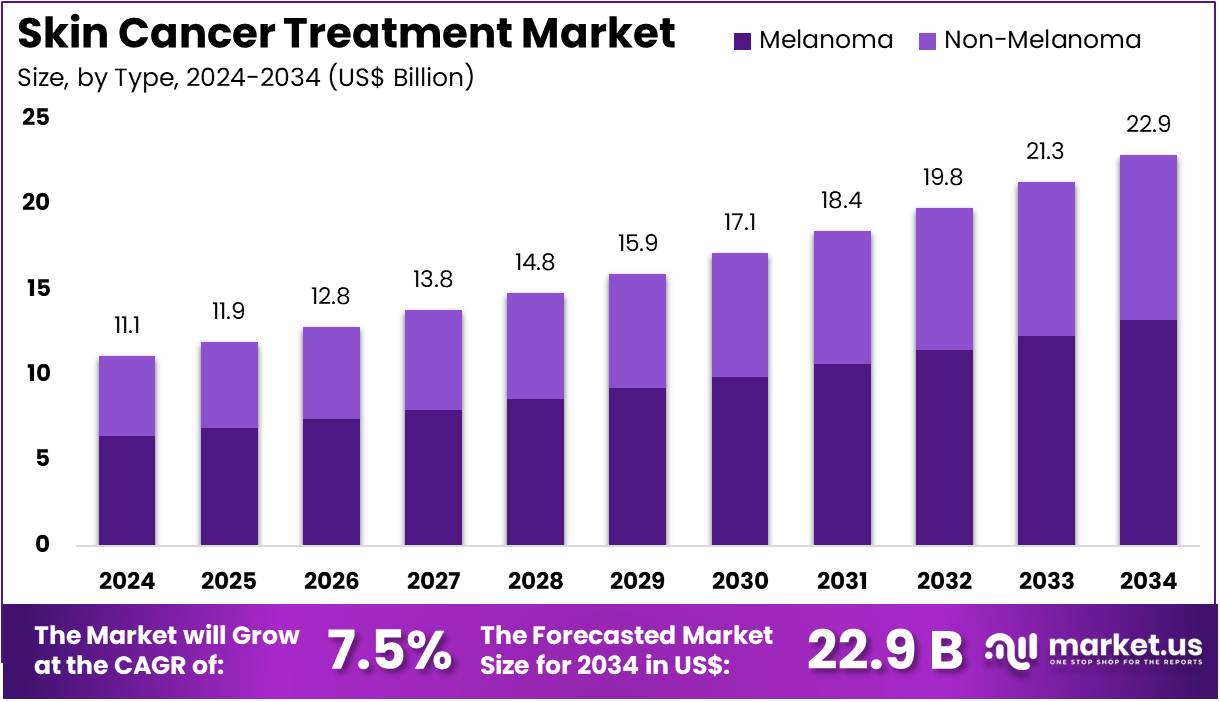

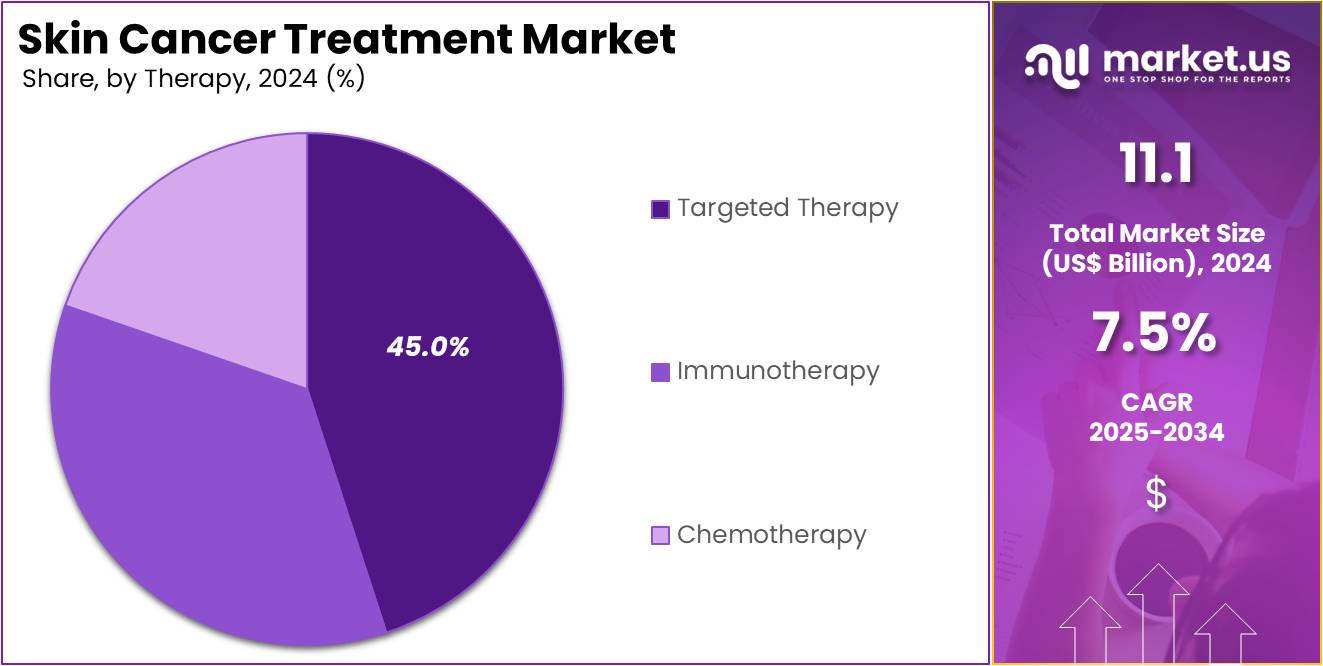

The Skin Cancer Treatment Market Size is expected to be worth around US$ 22.9 billion by 2034 from US$ 11.1 billion in 2024, growing at a CAGR of 7.5% during the forecast period 2025 to 2034.

Increasing rates of skin cancer diagnoses and growing awareness of early detection are driving the expansion of the skin cancer treatment market. Skin cancer, particularly basal cell carcinoma (BCC) and squamous cell carcinoma (SCC), has become one of the most common forms of cancer, with millions of cases diagnosed annually. The rise in skin cancer is closely linked to the increasing exposure to ultraviolet (UV) radiation from both natural and artificial sources, leading to more people seeking advanced treatment options.

Recent advancements in treatment techniques have improved patient outcomes, with innovative therapies such as immunotherapy, targeted therapy, and image-guided radiation therapies becoming increasingly popular. Treatments like immune checkpoint inhibitors and targeted therapies are showing promise in treating advanced skin cancers, particularly melanoma, which has a higher mortality rate. In July 2024, the Dermatology Association of Radiation Therapy (DART) published new clinical guidelines for BCC and SCC, recommending the use of image-guided superficial radiation therapy (IGSRT). This technique combines high-resolution ultrasound imaging with radiation, offering precise tumor targeting and demonstrating up to 99% effectiveness in treating skin cancer.

The market continues to benefit from the growing shift toward non-invasive treatments, such as topical therapies and photodynamic therapy, which reduce recovery time and side effects. Additionally, the increasing adoption of personalized medicine in skin cancer treatment, where therapies are tailored based on genetic and molecular profiles, is expanding treatment options and improving efficacy. As research continues and novel therapies are introduced, the skin cancer treatment market is poised for further growth, with more effective, less invasive solutions for patients.

Key Takeaways

- In 2024, the market for skin cancer treatment generated a revenue of US$ 11.1 billion, with a CAGR of 7.5%, and is expected to reach US$ 22.9 billion by the year 2034.

- The type segment is divided into melanoma and non-melanoma, with melanoma taking the lead in 2023 with a market share of 57.8%.

- Considering therapy, the market is divided into targeted therapy, immunotherapy, and chemotherapy. Among these, targeted therapy held a significant share of 45.0%.

- Furthermore, concerning the distribution channel segment, the market is segregated into hospitals pharmacies, online providers, and retail pharmacies. The hospitals pharmacies sector stands out as the dominant player, holding the largest revenue share of 56.4% in the skin cancer treatment market.

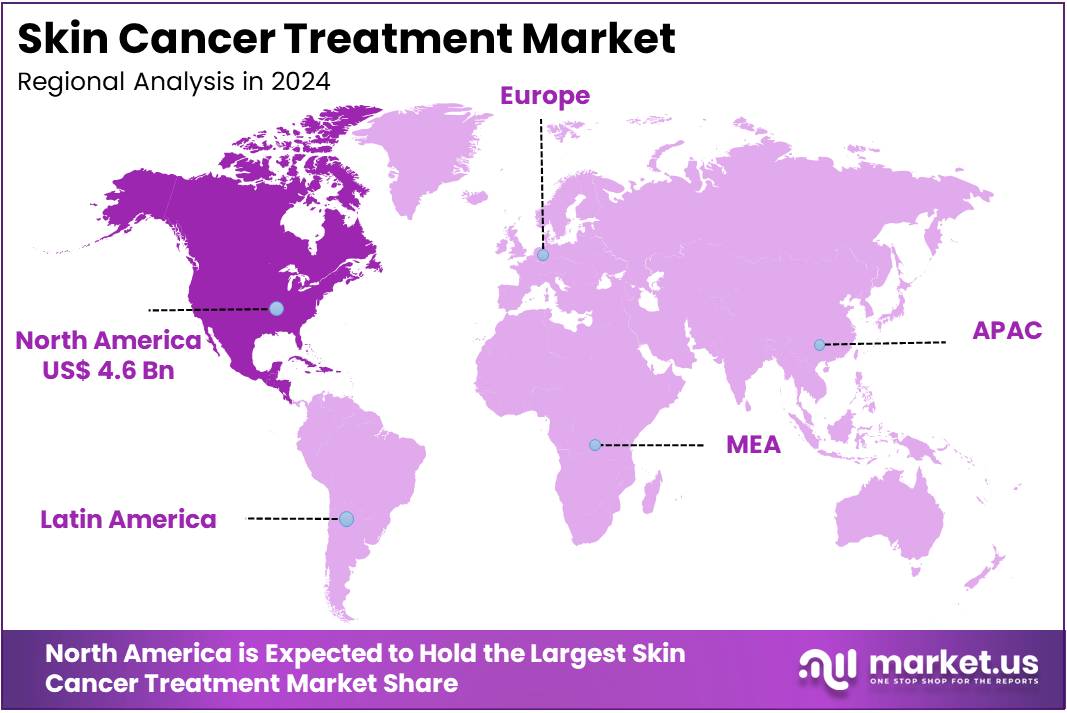

- North America led the market by securing a market share of 41.3% in 2023.

Type Analysis

Melanoma is expected to dominate the skin cancer treatment market, holding 57.8% of the market share. This segment’s growth is expected to be driven by the increasing prevalence of melanoma, one of the most aggressive forms of skin cancer. The rising rates of melanoma cases globally, particularly due to increased sun exposure and the rising awareness of skin cancer, are anticipated to contribute significantly to the demand for treatment.

Melanoma has seen substantial advancements in treatment options, particularly with the development of targeted therapies and immunotherapies that have improved survival rates for patients. These advancements are likely to further boost the melanoma treatment market as more patients opt for these specialized therapies. As the focus on early detection increases and new treatment options continue to emerge, the melanoma segment is projected to maintain its dominant position in the skin cancer treatment market.

Therapy Analysis

Targeted therapy is expected to be the dominant therapy type in the skin cancer treatment market, comprising 45.0% of the market share. This segment has experienced significant growth due to the ability of targeted therapies to directly affect cancer cells with minimal damage to surrounding healthy tissue. Targeted therapies have revolutionized the treatment of melanoma and non-melanoma skin cancers by offering more precise and effective options compared to traditional chemotherapy.

The increasing number of FDA-approved targeted therapies for skin cancer, particularly in melanoma, is anticipated to drive growth. Moreover, as more patients seek personalized treatment plans tailored to their specific cancer genetic profiles, targeted therapy will continue to be a preferred treatment option. The ongoing advancements in molecular biology and genomics are likely to further enhance the effectiveness of targeted therapies, contributing to continued market growth.

Distribution Channel Analysis

Hospital pharmacies are projected to remain the largest distribution channel in the skin cancer treatment market, holding 56.4% of the market share. Hospitals play a central role in providing specialized treatments for skin cancer, including surgery, targeted therapies, immunotherapies, and chemotherapy. The growth of this segment is expected to be driven by the increasing complexity of skin cancer treatment, which often requires highly specialized care and advanced medical equipment available in hospital settings.

Additionally, the growing number of cancer patients and the increasing adoption of combination therapies will contribute to the continued demand for hospital-based treatments. Hospital pharmacies are critical for managing and dispensing specialized cancer medications, ensuring proper patient monitoring and treatment management. As the global incidence of skin cancer rises, hospital pharmacies will continue to be a primary distribution channel for skin cancer treatments, driving the segment’s growth.

Key Market Segments

By Type

- Melanoma

- Non-Melanoma

By Therapy

- Targeted Therapy

- Immunotherapy

- Chemotherapy

By Distribution Channel

- Hospitals Pharmacies

- Online Providers

- Retail Pharmacies

Drivers

Increasing Global Incidence of Skin Cancer is Driving the Market

The escalating global incidence of skin cancer, particularly melanoma, is a primary driver for the skin cancer treatment market. As the number of diagnosed cases rises, the demand for both early-stage interventions and advanced systemic therapies for metastatic disease grows. Factors such as increased ultraviolet (UV) radiation exposure, a growing aging population, and heightened awareness leading to better screening contribute to the rising case numbers.

According to the International Agency for Research on Cancer (IARC), a part of the World Health Organization (WHO), there were an estimated 330,000 new cases of melanoma worldwide in 2022, and almost 60,000 deaths from the disease. IARC also reported that there were over 1.5 million new cases of non-melanoma skin cancers in 2022.

This significant disease burden necessitates continuous innovation in treatment options, from surgical and topical therapies for localized disease to systemic targeted and immunotherapies for advanced cases. The need to provide effective, long-term care for this expanding patient population creates a robust and expanding market for pharmaceutical companies, medical device manufacturers, and healthcare providers.

Restraints

High Cost of Advanced Systemic Therapies is Restraining the Market

A significant restraint on the skin cancer treatment market is the exceptionally high cost associated with advanced systemic therapies, especially immunotherapies and targeted therapies for melanoma. While these treatments have revolutionized the outlook for patients with advanced disease, their list prices can be substantial, leading to a phenomenon known as “financial toxicity” for patients and immense budget pressure on healthcare systems.

For example, some IV immunotherapies used to treat advanced melanoma have an average cash price of over US$ 22,000 per dose, leading to an annual cost that can exceed US$ 190,000 without insurance or discounts, as reported in publications that track drug pricing from sources like GoodRx. A 2025 study on the cost-effectiveness of immunotherapy combinations for advanced melanoma noted that drug acquisition and administration costs were the main cost drivers.

Even with insurance coverage, high copayments, deductibles, and out-of-pocket expenses can create a significant financial burden for patients. This economic barrier limits the accessibility of these life-saving drugs, particularly in regions with limited insurance coverage or in patients who cannot afford the financial strain, thereby restricting the market’s full growth potential.

Opportunities

The Development of Novel Combination Therapies Creates Growth Opportunities

The active development and clinical investigation of novel combination therapies represent a significant growth opportunity in the skin cancer treatment market. Clinicians and researchers are increasingly combining different therapeutic modalities, such as immunotherapy with targeted therapy, chemotherapy, or radiotherapy, to achieve synergistic effects that improve patient response rates and durability of response. This approach aims to overcome mechanisms of resistance to single-agent therapies and provide more comprehensive anti-tumor activity. The US Food and Drug Administration (FDA) has continued to approve new combination regimens.

For instance, in April 2025, the FDA approved nivolumab with ipilimumab for pediatric and adult patients 12 years of age and older with unresectable or metastatic microsatellite instability-high (MSI-H) or mismatch repair deficient (dMMR) tumors, including some melanomas, based on data from a trial showing improved patient outcomes.

Furthermore, the American Society of Clinical Oncology (ASCO) Annual Meeting in June 2025 featured clinical trial updates on combination strategies, including a study exploring a cancer vaccine in combination with standard immunotherapy for advanced melanoma. These ongoing efforts to design more effective multi-drug regimens are expanding the therapeutic arsenal and driving market growth.

Impact of Macroeconomic / Geopolitical Factors

Macroeconomic conditions strongly affect the skin cancer treatment market. Economic growth often leads to higher healthcare spending and better insurance coverage. This supports wider access to costly treatments like immunotherapy and targeted therapies. During stable periods, governments can allocate more funds to public health and research. However, in times of inflation or recession, healthcare budgets may shrink. This can delay the adoption of new treatments. It also places more financial burden on patients, which limits access to advanced care options and slows overall market progress.

The International Monetary Fund (IMF) in its April 2025 “World Economic Outlook” reported stable global growth. However, risks such as geopolitical fragmentation and high interest rates persist. These risks may indirectly affect pharmaceutical innovation and healthcare funding. When interest rates rise, it becomes more expensive for companies to borrow and invest in R&D. As a result, innovation may slow. At the same time, government budgets may face constraints. This can reduce support for new drug programs or delay regulatory approvals for skin cancer therapies.

Geopolitical factors also impact the skin cancer treatment market. Trade policies influence the import and export of drug ingredients and manufacturing tools. Political instability or trade conflicts can disrupt supply chains. This raises production costs and may lead to drug shortages. Public health crises can further strain global logistics. Despite these risks, the high public health burden of skin cancer ensures long-term investment. Governments and organizations remain committed to ensuring drug availability, supporting innovation, and promoting equitable access, which helps the market remain resilient.

Current US tariff policies may indirectly impact the skin cancer treatment market by raising the cost of imported active pharmaceutical ingredients (APIs), excipients, and manufacturing equipment. These elements are critical for producing biologics and advanced therapies. Despite its strength, the US pharmaceutical industry depends heavily on global supply chains. According to the US Census Bureau’s FT-900 report (Page 8, Exhibit 8), pharmaceutical imports reached US$246.849 billion in 2024. This high import volume highlights the industry’s reliance on international sourcing for essential medical products and components.

If new tariffs are placed on these raw materials or finished drugs, the cost of manufacturing in the US could rise. Companies may pass these increases on to patients and healthcare systems, resulting in higher drug prices. Alternatively, manufacturers might absorb the costs, which could reduce research and development budgets. This scenario may delay the introduction of innovative therapies and limit patient access. Thus, tariff changes pose financial challenges that can affect affordability, innovation, and the overall availability of skin cancer treatments.

However, these tariff policies could encourage pharmaceutical companies to shift toward domestic production. Localizing manufacturing for skin cancer therapies can reduce dependency on global supply chains. This shift also enhances national medical security by ensuring stable access to critical treatments. Though initial investments and regulatory compliance costs may be high, the long-term benefits include greater supply chain resilience. Overall, strategic domestic production may become a key focus area in response to evolving tariff policies and global trade uncertainties.

Latest Trends

Increased Adoption of Telehealth for Follow-up Care is a Recent Trend

A prominent recent trend in the skin cancer treatment market is the increasing adoption of telehealth and teledermatology for post-treatment follow-up and surveillance. After completing treatment, skin cancer patients, particularly those with melanoma, require frequent and long-term surveillance with a dermatologist to monitor for recurrence or new lesions.

Telehealth platforms allow patients to have virtual check-ups with their specialists, reducing the need for travel, saving time, and increasing convenience. The Centers for Medicare & Medicaid Services (CMS) has expanded reimbursement for telehealth services, including those for dermatology, facilitating its widespread use.

A study on the use of telehealth in the United States from February 2024 noted that the number of teledermatology visits increased significantly from 2021 to 2023. This increased adoption of remote monitoring and follow-up care is improving patient adherence to surveillance schedules and is particularly beneficial for patients in rural or underserved areas who lack local access to specialized dermatological care. This technological trend is streamlining post-treatment care and enhancing patient engagement in their long-term health management, which supports continued market stability and patient engagement.

Regional Analysis

North America is leading the Skin Cancer Treatment Market

North America led the skin cancer treatment market with a 41.3% revenue share. This dominance is due to the high rates of melanoma and non-melanoma skin cancers. In 2025, the United States is projected to report around 212,200 new melanoma cases. This includes 107,240 noninvasive and 104,960 invasive cases. Canada is also affected, with an estimated 11,300 new melanoma cases in 2024. These rising numbers show a significant patient burden across the region. Demand for innovative and effective treatment options continues to grow steadily.

The market is also supported by regulatory approvals of advanced therapies. The U.S. FDA plays a key role in this progress. In 2023, the FDA approved Zynyz (retifanlimab-dlwr) for treating metastatic or recurrent Merkel cell carcinoma. This is a rare but aggressive skin cancer. In 2024, the FDA approved lifileucel. It is a tumor-derived autologous T-cell therapy for unresectable or metastatic melanoma. This approval targets patients who have failed anti-PD-1 and BRAF inhibitor treatments. These approvals mark significant clinical advancements.

Pharmaceutical companies are seeing strong revenue from their oncology products. Merck’s Keytruda is a notable example in the immunotherapy space. It is widely used in melanoma treatment. In 2024, Keytruda generated US$29.48 billion in global sales. This marks an 18% increase from its 2023 revenue of US$25.01 billion. The strong sales reflect its expanded use across multiple cancer types, including skin cancer. Such growth highlights the rising importance of immunotherapy in the treatment landscape across North America.

The Asia Pacific region is expected to experience the highest CAGR during the forecast period

Asia Pacific is expected to grow with the fastest CAGR owing to increasing public awareness regarding sun exposure risks, improving diagnostic capabilities, and the growing availability of advanced therapeutic options. While specific regional incidence data for skin cancer can vary, the overall cancer burden in Asia remains high, with the World Health Organization (WHO) reporting nearly 1 million new breast cancer cases in Asia in 2022, indicating a large patient population susceptible to various cancer types, including skin malignancies.

Governments across the region are increasingly investing in cancer control programs and public health campaigns to promote early detection and prevention. For example, national health commissions in countries like China are enhancing their cancer screening and treatment infrastructure, which is likely to improve the diagnosis and management of skin cancers. Pharmaceutical companies are actively expanding their presence and product offerings in Asia Pacific.

Merck’s Keytruda, a key immunotherapy, has seen increasing adoption in Asian markets. Although precise regional sales figures for skin cancer treatments are often consolidated within broader oncology reports, the overall growth of these companies in the Asia Pacific region indicates a rising demand for advanced therapies. This combination of heightened awareness, improved diagnostics, and expanding treatment access is projected to drive robust growth for skin cancer management across Asia Pacific.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherland

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- New Zealand

- Singapore

- Thailand

- Vietnam

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

Key players in the skin cancer treatment market are actively using several strategies to boost growth. One major focus is the expansion of product portfolios. Companies are developing novel therapies and research tools that target various skin cancer types. They are also adopting automation and high-throughput technologies to improve efficiency. These efforts help increase the scalability and reproducibility of treatment processes. As demand rises, the use of technology and innovation is helping companies stay competitive in the global skin cancer treatment landscape.

Partnerships also play a crucial role in shaping the market. Leading firms collaborate with biotechnology companies, academic research institutions, and healthcare providers. These collaborations accelerate the development of new treatments and support faster clinical integration. Strategic alliances allow companies to access advanced scientific knowledge and shared resources. This approach ensures that new skin cancer therapies are backed by clinical evidence. As a result, companies can bring innovative products to market more quickly and meet rising patient needs effectively.

Amgen Inc. stands out as a key player in this market. Based in Thousand Oaks, California, Amgen is a biotechnology firm known for its innovative treatments. One of its leading products, Neulasta (pegfilgrastim), helps reduce infection risk in cancer patients receiving chemotherapy. Amgen is committed to research and development, focusing on therapies that meet critical medical needs. The company’s strong pipeline and ongoing collaborations help strengthen its market position. By investing in innovation and strategic partnerships, Amgen continues to drive advancements in skin cancer treatment solutions.

Top Key Players in the Skin Cancer Treatment Market

- Pfizer Inc

- Novartis AG

- Moderna

- Merck KGaA

- Iovance Biotherapeutics

- Glaxosmithkline plc

- Bristol-Myers Squibb

- Amgen Inc

Recent Developments

- In June 2024, Moderna and Merck announced positive three-year follow-up data for their individualized neoantigen therapy mRNA-4157 (V940) in combination with Keytruda for high-risk melanoma, showing a continued significant reduction in the risk of recurrence or death by 49% and distant metastasis or death by 62%.

- In February 2024, Iovance Biotherapeutics received accelerated approval from the US FDA for lifileucel (Amtagvi), making it the first cellular therapy approved for a solid tumor. This tumor-infiltrating lymphocyte (TIL) therapy is indicated for adult patients with unresectable or metastatic melanoma who have progressed on prior therapies.

Report Scope

Report Features Description Market Value (2024) US$ 11.1 billion Forecast Revenue (2034) US$ 22.9 billion CAGR (2025-2034) 7.5% Base Year for Estimation 2024 Historic Period 2020-2023 Forecast Period 2025-2034 Report Coverage Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments Segments Covered By Type (Melanoma and Non-Melanoma), By Therapy (Targeted Therapy, Immunotherapy, and Chemotherapy), By Distribution Channel (Hospitals Pharmacies, Online Providers, and Retail Pharmacies) Regional Analysis North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA Competitive Landscape Pfizer Inc, Novartis AG, Moderna, Merck KGaA, Iovance Biotherapeutics, Glaxosmithkline plc, Bristol-Myers Squibb, Amgen Inc. Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)  Skin Cancer Treatment MarketPublished date: July 2025add_shopping_cartBuy Now get_appDownload Sample

Skin Cancer Treatment MarketPublished date: July 2025add_shopping_cartBuy Now get_appDownload Sample -

-

- Pfizer Inc

- Novartis AG

- Moderna

- Merck KGaA

- Iovance Biotherapeutics

- Glaxosmithkline plc

- Bristol-Myers Squibb

- Amgen Inc

Our Clients

- 152445

- July 2025