Quick Navigation

Report Overview

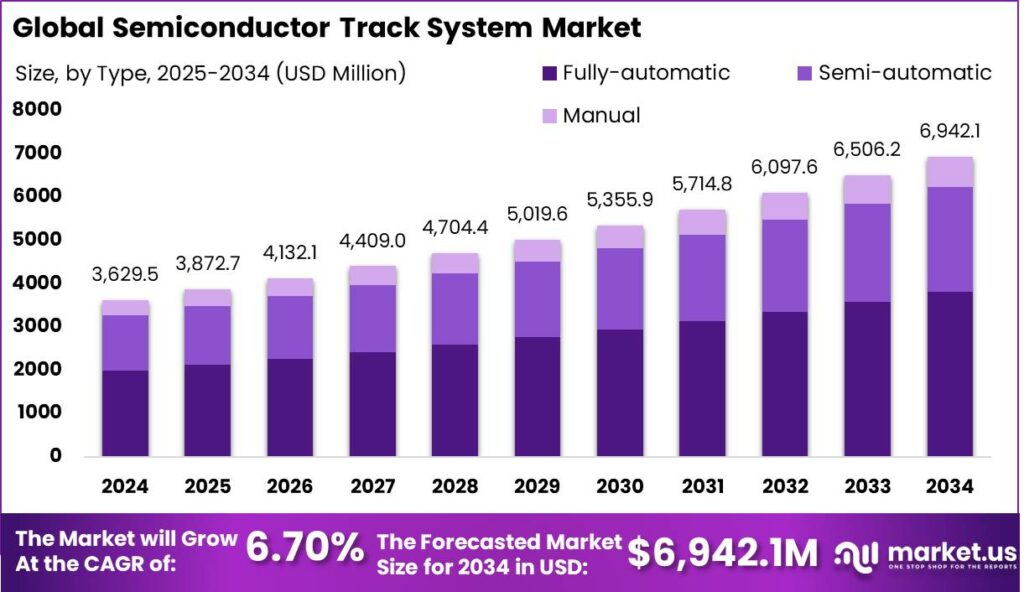

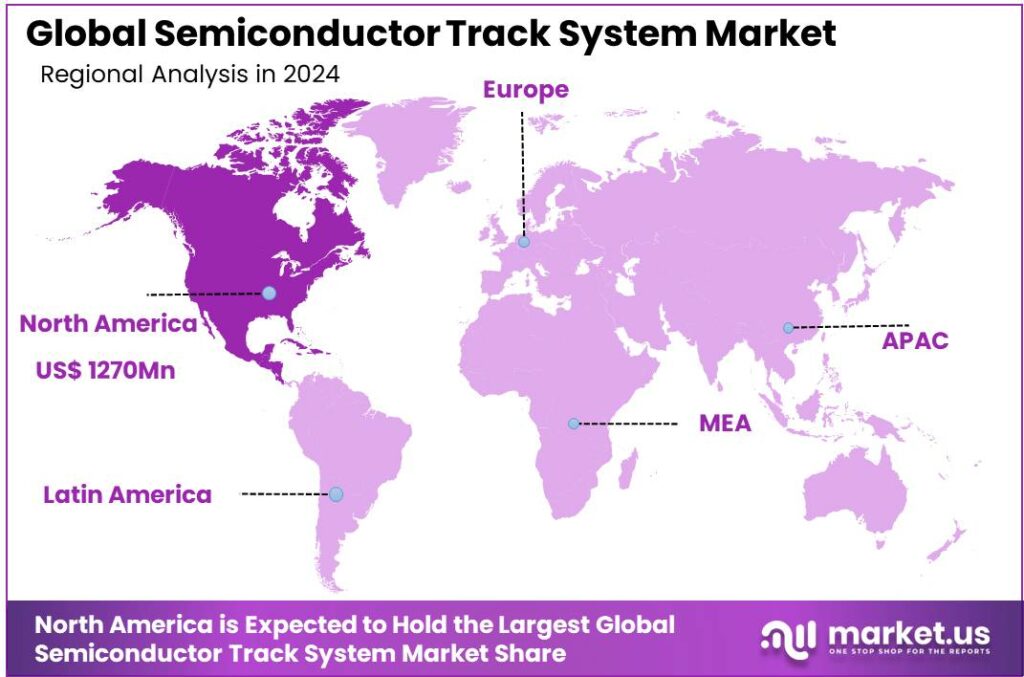

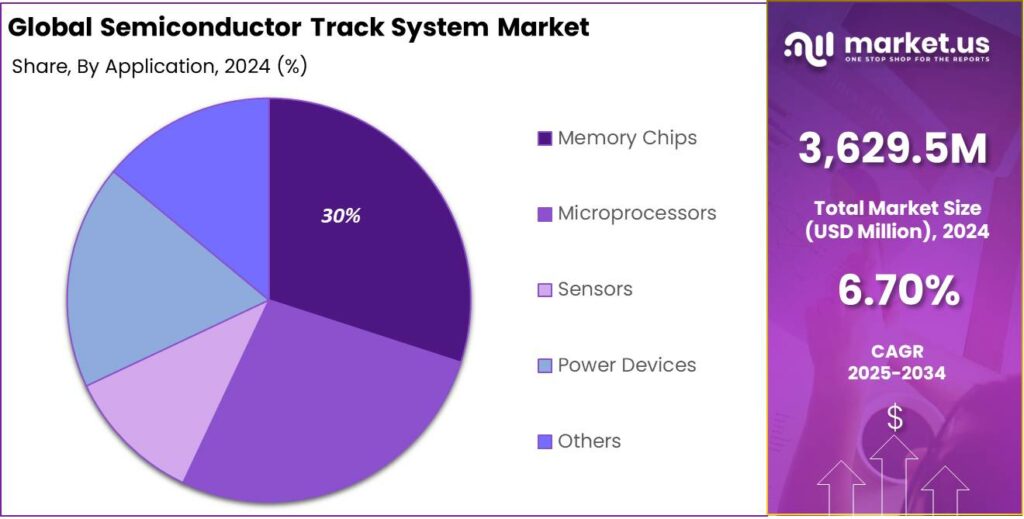

The Global Semiconductor Track System Market size is expected to be worth around USD 6,942.1 Million By 2034, from USD 3,629.5 Million in 2024, growing at a CAGR of 6.70% during the forecast period from 2025 to 2034. North America emerged as the leading regional market in 2024, holding more than 35% market share and generating USD 1,270 million in revenue.

A semiconductor track system is essential in semiconductor manufacturing, enabling the precise and controlled movement of silicon wafers through photolithography steps. It ensures accurate wafer positioning and smooth transfer between tools like coaters, developers, and etchers, supporting the high precision needed to form electronic circuits.

The growth of the semiconductor track system market is driven by the global expansion of electronic manufacturing, especially in developing regions, and the rising trend of automation in manufacturing. Increased investments in semiconductor production, including new fabs and technology upgrades, also contribute to market growth.

There is a strong market demand for semiconductor track systems, primarily fueled by the surge in consumer electronics, automotive electronics, and the Internet of Things (IoT). As electronic devices grow more complex and compact, the precision and efficiency of advanced track systems are essential for achieving production goals and upholding quality standards.

Artificial intelligence (AI) is transforming the semiconductor track system market by enabling smarter, more adaptive manufacturing processes. AI algorithms optimize track system logistics, reducing waste and boosting productivity. Predictive maintenance minimizes downtime by forecasting equipment failures, protecting the manufacturing process from disruptions.

This market has seen substantial growth due to the increasing demand for electronic devices, which require complex and miniaturized semiconductor components. The push towards smaller device geometries and more powerful integrated circuits drives the need for more precise and reliable track systems, thus bolstering the market growth.

The ongoing innovation in semiconductor technology, such as the development of smaller and more powerful chips, presents numerous opportunities for the market. The growth of semiconductor manufacturing in emerging markets drives demand for advanced track systems. Innovators in modular, scalable solutions are poised to gain market share.

Recent trends in the semiconductor track system market include the integration of IoT technologies for real-time tracking and management, increased automation, and the adoption of environmentally sustainable manufacturing practices. These trends are expected to continue as companies seek to improve operational efficiencies and reduce costs.

Key Takeaways

- The Global Semiconductor Track System Market is projected to reach USD 6,942.1 million by 2034, up from USD 3,629.5 million in 2024, growing at a CAGR of 6.70% during the forecast period 2025 to 2034.

- In 2024, the Fully-automatic segment dominated the Semiconductor Track System market, accounting for over 55% of the total market share.

- The Memory Chips segment also led the market in 2024, capturing more than 30% of the total share within the Semiconductor Track System Market.

- North America emerged as the leading regional market in 2024, holding more than 35% market share and generating USD 1,270 million in revenue.

Analyst’s Viewpoint

The semiconductor track system market is experiencing robust growth due to several emerging opportunities. The demand for energy-efficient semiconductor solutions is rising due to a global push for sustainability, supported by government incentives for green tech R&D. Additionally, the rollout of 5G technology creates significant market opportunities for advanced semiconductor components.

The market benefits from continuous innovations, particularly in AI and machine learning, which help mitigate high costs and shorten time-to-market for next-generation technologies. This integration not only streamlines operations but significantly improves the efficiency of the testing and design phases, thus enhancing overall productivity and market responsiveness

The global regulatory landscape heavily influences the semiconductor track system market. With countries like China and the USA tightening export controls and investment guidelines, companies must navigate these changes carefully. These geopolitical factors require strategic agility to maintain a competitive edge and ensure compliance with international standards.

US Tariff Impact Analysis

The US semiconductor industry is facing significant challenges due to the imposition of a 25% tariff on imported semiconductors, as announced by the Trump administration in 2025. This tariff predominantly targets advanced semiconductor chips from regions like Taiwan, South Korea, and China, which collectively contribute over 60% of the global semiconductor supply.

The tariffs have introduced increased costs and complexities within the semiconductor supply chains. Companies are expected to face heightened production costs, which may lead to reconsiderations of supply chain strategies and potentially encourage shifts towards domestic manufacturing. This strategic shift is crucial as it could alter operational approaches and capital allocation within companies.

From a market perspective, the broad application of these tariffs has created significant disruptions. Not only do they affect America’s trading partners, but they also impact global supply chains crucial for modern economies. This has led to increased geopolitical tensions and has heightened the costs of goods across various sectors.

Regional Analysis

In 2024, North America held a dominant market position in the semiconductor track system market, capturing more than a 35% share and generating revenue of USD 1270 million. This leading status can be attributed to several key factors.

North America, especially the United States, has a robust technological infrastructure which supports the extensive development and adoption of advanced semiconductor technologies. This region is home to some of the world’s leading semiconductor companies, such as Intel, AMD, and Qualcomm, which drive innovation and demand for sophisticated track systems.

The demand for semiconductor track systems in North America is also driven by the presence of significant end-user industries including automotive, consumer electronics, and telecommunications. These sectors require increasingly efficient and miniaturized semiconductors, fueling the need for advanced track systems that can enhance production capacities and operational efficiencies.

North America is a global leader in semiconductor R&D, driving growth in the semiconductor track system market through continuous innovation and advanced technologies. The U.S. government supports the industry with policies, funding, and initiatives like the CHIPS Act, aimed at enhancing domestic production and securing supply chains while fostering innovation.

Type Analysis

In 2024, the Fully-automatic segment held a dominant market position within the Semiconductor Track System market, capturing more than a 55% share. This leadership can be attributed to several key factors that align with the industry’s evolving demands for efficiency and precision.

The surge in semiconductor demand, fueled by the growth of consumer electronics, automotive electronics, and IoT devices, requires highly efficient production methods. Fully-automatic systems reduce human intervention, minimize errors, and enhance throughput. Automation of key processes like wafer handling and inspection ensures consistent product quality, which is essential in semiconductor manufacturing.

The adoption of fully-automatic systems is strengthened by integrating advanced technologies like AI and machine learning, which improve decision-making and enable predictive maintenance. This boosts production flow, reduces downtime, and increases the segment’s appeal to semiconductor manufacturers aiming to maximize ROI.

Furthermore, the push towards miniaturization of electronic components has made the manufacturing processes increasingly complex, necessitating the precise and repeatable operations provided by fully-automatic systems. The ability of these systems to accurately handle and process smaller wafers at high speeds without damage is a decisive factor driving their adoption.

Application Analysis

In 2024, the Memory Chips segment held a dominant market position within the Semiconductor Track System Market, capturing more than a 30% share. This leading stance can be attributed to several key factors,

The escalating need for larger data storage capacities due to the surge in data generation from various sources such as smartphones, IoT devices, and cloud computing has significantly driven the demand for memory chips. This trend has necessitated advancements in semiconductor track systems to efficiently handle the production complexities of high capacity memory chips.

Innovations in memory technologies, including the development of 3D NAND and DRAM, have fostered growth in the memory chips segment. These technologies require precise and reliable semiconductor track systems to manage the intricate processes involved in their fabrication, thereby reinforcing the segment’s growth.

The continuous expansion of the consumer electronics market, characterized by frequent upgrades in smartphones, laptops, and other gadgets, directly influences the demand for memory chips. As devices become more advanced, the integration of higher memory capacities becomes essential, further bolstering the segment’s dominance.

Key Market Segments

By Type

- Fully-automatic

- Semi-automatic

- Manual

By Application

- Memory Chips

- Microprocessors

- Sensors

- Power Devices

- Others

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Driver

Advancements in Lithography and Automation Technologies

The growth of the semiconductor track system market is significantly driven by advancements in lithography and automation technologies. The integration of Extreme Ultraviolet (EUV) lithography has necessitated the development of sophisticated track systems capable of handling complex processes with high precision.

Advanced track systems are critical to maintaining semiconductor production efficiency and integrity, especially as manufacturers pursue greater automation and higher yields. Growing demand in AI, 5G, and automotive electronics is driving the need for high-performance solutions, supporting ongoing market growth through efficient and sustainable wafer processing.

Restraint

Regulatory Compliance and Environmental Concerns

The semiconductor industry faces growing regulatory challenges, requiring companies to adapt to complex environmental and trade regulations while ensuring resilience. Compliance with stringent environmental standards necessitates significant investments in sustainable manufacturing practices and waste management systems.

Additionally, trade regulations and export controls can impact the global supply chain, leading to uncertainties in the availability of critical components and materials. Regulatory complexities limit the agility of semiconductor manufacturers, making it harder to quickly meet market demands. Navigating varying regional regulations adds operational strain, potentially slowing innovation and raising costs. As a result, compliance and environmental concerns serve as key restraints in the semiconductor track system market.

Opportunity

Expansion into Emerging Markets and Applications

The semiconductor track system market offers significant opportunities through growth in emerging markets and new applications. As advanced technologies gain traction in automotive, healthcare, and consumer electronics, demand for efficient track systems continues to rise.

Emerging economies, with their growing industrial base and supportive government policies, offer fertile ground for market expansion. Investments in infrastructure and the establishment of semiconductor manufacturing facilities in these regions can lead to increased demand for track systems.

The rise of innovative applications like wearable devices and smart home technologies opens new opportunities for semiconductor use. By exploring these emerging markets, companies can diversify their customer base and drive sustainable growth in the semiconductor track system market.

Challenge

Technological Complexity and High Capital Investment

The semiconductor track system market faces challenges due to growing technological complexity and high capital investment requirements. As semiconductor devices advance, manufacturing demands more sophisticated track systems for precise operations.

Developing and maintaining these systems requires significant R&D efforts, resulting in higher costs. Additionally, the rapid pace of technological advancements necessitates continuous upgrades and investments to stay competitive.

Small and medium-sized enterprises may find it particularly challenging to bear these costs, potentially limiting their participation in the market. Moreover, the integration of new technologies into existing manufacturing setups can be complex and time-consuming, affecting production timelines and efficiency.

Emerging Trends

Semiconductor track systems are evolving to meet the growing demand for precision, efficiency, and adaptability in fabrication. A key trend is the integration of advanced materials like gallium carbide (GaC), which offers better electronic and optical properties than traditional materials like gallium nitride (GaN). GaC’s larger band gaps in certain phases make it a promising candidate for next-generation semiconductors.

Emerging trends in semiconductor track systems include the adoption of advanced packaging techniques like 2.5D and 3D integration, improving performance and reducing power consumption. Additionally, RFID technology is gaining popularity for real-time asset and inventory tracking, boosting productivity and lowering operational costs.

Smart manufacturing practices, or “smart fabs,” are rising, digitally connecting the entire production lifecycle for improved cycle times, yield, and cost savings. The integration of AI and machine learning in semiconductor design and manufacturing enhances efficiency, accuracy, and enables predictive maintenance.

Business Benefits

Semiconductor track systems streamline the management of materials and carriers, leading to improved operational efficiency. By automating material tracking and handling, these systems reduce manual errors and accelerate processing times. This automation not only saves time but also minimizes production errors, contributing to cost-effective manufacturing processes.

Advanced track systems incorporate predictive analytics to monitor equipment performance in real-time. By analyzing data trends, these systems can forecast potential equipment failures, allowing for timely maintenance interventions. This proactive approach prevents unexpected downtime, ensuring continuous production and reducing maintenance costs.

Track systems offer real-time visibility into material and carrier statuses, enabling quick identification and resolution of issues. They maintain detailed logs of parameter changes, location updates, and lifecycle events, which are crucial for quality control and process optimization.

Key Player Analysis

The Semiconductor Track System market plays a crucial role in chip manufacturing by supporting photolithography and wafer processing.

Applied Materials, Inc. is one of the most well-known names in the semiconductor industry. The company’s strength lies in its ability to provide a complete set of solutions from deposition to etching and metrology, including track systems. Applied focuses on combining AI-driven automation and advanced materials engineering, making its track systems smarter and more efficient.

Tokyo Electron Limited (TEL), based in Japan, is a global leader in semiconductor production equipment, especially in coating and developing systems. TEL’s track systems are known for their precision, reliability, and high throughput. The company works closely with major chipmakers and has built long-term relationships with industry giants.

ASML Holding N.V. is primarily known for its EUV lithography machines, it also plays a part in the track system ecosystem through partnerships and integration efforts. ASML’s leadership in advanced photolithography drives track system performance. As lithography advances, the track system’s role becomes more critical.

Top Key Players in the Market

- Applied Materials, Inc.

- Tokyo Electron Limited (TEL)

- ASML Holding N.V.

- Lam Research Corporation

- KLA Corporation

- Nikon Corporation

- Veeco Instruments Inc.

- Hitachi High-Technologies Corporation

- Canon Inc.

- Cameca Instruments (AMETEK, Inc.)

- Other Key Players

Top Opportunities for Players

The Semiconductor Track System market is poised for growth, offering several lucrative opportunities for industry players and investors.

- Rise of AI and Cloud Computing: As artificial intelligence and cloud computing continue to drive demand for high-performance computing and data centers, semiconductor track systems that support AI accelerators and high-bandwidth memory (HBM) are expected to see significant growth.

- Sustainability and Green Technologies: There’s a growing focus on sustainability, prompting increased investments in energy-efficient semiconductor solutions. This trend is further supported by government incentives for research and development in energy-efficient technologies.

- Expansion of 5G Technology: The rollout of 5G technology, requiring advanced semiconductor components for enhanced data processing and communication capabilities, presents substantial opportunities. This sector is crucial for the continued evolution and deployment of 5G infrastructure.

- Geographical Expansion in Emerging Markets: Regions like Asia-Pacific are projected to dominate the market due to strong semiconductor manufacturing capabilities, particularly in countries like China, Japan, and South Korea. India is emerging as a significant player, offering new opportunities for material suppliers and manufacturers looking to establish a presence in new markets.

- Innovations in Semiconductor Manufacturing: The industry is witnessing innovations such as AI-integrated automated track systems, eco-friendly wafer processing, and advanced photolithography techniques. These technological advancements are set to open new avenues for growth and efficiency in semiconductor manufacturing.

Recent Developments

- In April 2025, Applied Materials acquired a 9% stake in BE Semiconductor Industries (BESI), becoming its largest shareholder. This strategic investment strengthens Applied Materials’ position in advanced chip packaging, particularly in hybrid bonding technologies crucial for stacking chips vertically.

- In year 2024, Tokyo Electron Limited (TEL) launched the Episode™ series of single-wafer deposition systems, designed to perform multiple processes without interruption, thereby improving productivity in semiconductor manufacturing.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 3,629.5 Mn |

| Forecast Revenue (2034) | USD 6,942.1 Mn |

| CAGR (2025-2034) | 6.70% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue forecast, AI impact on market trends, Share Insights, Company ranking, competitive landscape, Recent Developments, Market Dynamics and Emerging Trends |

| Segments Covered | By Type (Fully-automatic, Semi-automatic, Manual), By Application (Memory Chips, Microprocessors, Sensors, Power Devices, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Applied Materials, Inc., Tokyo Electron Limited (TEL), ASML Holding N.V., Lam Research Corporation, KLA Corporation, Nikon Corporation, Veeco Instruments Inc., Hitachi High-Technologies Corporation, Canon Inc., Cameca Instruments (AMETEK, Inc.), Other Key Players |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three license to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |