Quick Navigation

Report Overview

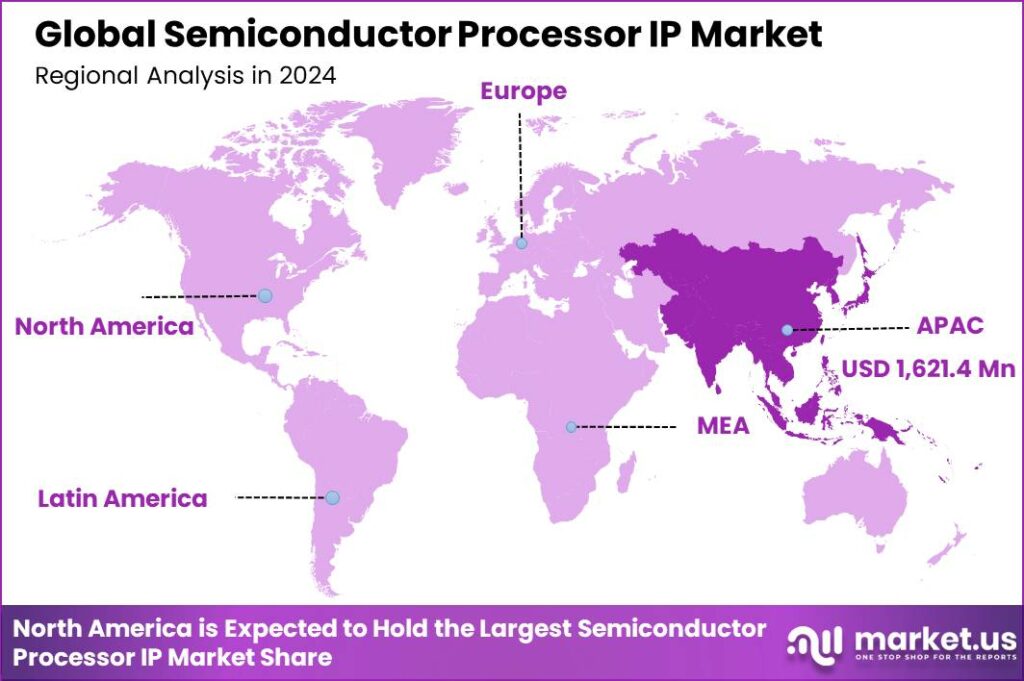

The Global Semiconductor Processor IP Market size is expected to be worth around USD 8,049.1 Million By 2034, from USD 4,053.7 Million in 2024, growing at a CAGR of 7.1% during the forecast period from 2025 to 2034. In 2024, Asia-pacific held a dominant market position, capturing more than a 40% share, holding USD 1,621.4 Million revenue.

Semiconductor Processor IP (Intellectual Property) refers to the reusable design components such as microprocessors, memory architectures, and other elements essential to the creation of integrated circuits. These IPs are developed to be licensed to others, allowing them to manufacture advanced chips without designing these complex parts from scratch. This enables more efficient, cost-effective production of electronic devices, ranging from mobile phones to automotive systems.

The market for semiconductor processor IP is driven by the increasing complexity of consumer electronics, the demand for more powerful and energy-efficient processors, and the continuous advancements in mobile and cloud computing technologies. This market is characterized by a robust ecosystem of developers and vendors who specialize in designing and licensing these IPs to manufacturers aiming to enhance their product offerings without investing heavily in new, costly development projects.

The growth of the Semiconductor Processor IP market is primarily fueled by the surge in demand for consumer electronics and the ongoing advancements in multi-core technology for System on Chip (SoC) designs. The trend towards connected devices and smart technologies, particularly in automotive and telecommunication sectors, has led to increased demand for sophisticated semiconductor IPs.

The demand in the semiconductor processor IP market is heavily influenced by the consumer electronics sector, particularly with the proliferation of smartphones, tablets, and wearables. Manufacturers are under constant pressure to upgrade their devices with higher computational power and improved battery life, driving the need for innovative processor IPs that can deliver these requirements efficiently.

According to Market.us, The global semiconductor intellectual property (IP) market is poised for significant growth, with its value expected to rise from USD 6.4 bn in 2023 to approximately USD 11.3 bn by 2033, reflecting a steady CAGR of 6.7%. In 2023, the Asia-Pacific (APAC) region led the market, contributing over 38% of the global share, equating to USD 1.9 billion in revenue.

Technological advancements are pivotal in shaping the Semiconductor Processor IP market. The rise of RISC-V processor technology, AI, IoT, and high-bandwidth memory (HBM) technologies are significant contributors. These advancements not only enhance the performance of electronic devices but also drive the demand for new, more advanced semiconductor IPs to support these technologies

Opportunities within the semiconductor processor IP market are abundant, particularly in the areas of AI and machine learning. As these technologies continue to evolve, there is a growing need for specialized processor IPs that can efficiently handle AI algorithms and processes. Furthermore, the expansion of the Internet of Things (IoT) creates additional demand for versatile and powerful semiconductor IPs that can be implemented across a variety of devices and platforms.

Key Takeaways

- The Global Semiconductor Processor IP Market is projected to grow significantly over the next decade, reaching an estimated value of USD 8,049.1 million by 2034. This represents a substantial increase from USD 4,053.7 million in 2024, driven by a compound annual growth rate (CAGR) of 7.1% during the forecast period from 2025 to 2034.

- In 2024, the Asia-Pacific region dominated the market, accounting for over 40% of the total revenue. This translated to a market value of approximately USD 1,621.4 million. The region’s leadership is attributed to robust manufacturing capabilities and strong demand for advanced processors.

- The CPU IP segment also held the leading position within the semiconductor processor IP market in 2024, capturing more than 54% of the total market share. This dominance highlights the critical role of central processing units in driving technological advancements across industries.

- Furthermore, the Integrated Device Manufacturer (IDM) segment emerged as a significant contributor in 2024, securing over 25% of the market share. IDMs continue to leverage their vertically integrated structures to enhance innovation and efficiency.

Type Analysis

In 2024, the CPU IP segment held a dominant market position, capturing more than a 54% share of the semiconductor processor IP market. This significant market share can be attributed to the extensive utilization of CPU IP cores across various high-demand industries, including consumer electronics, automotive, and telecommunications.

The fundamental role of CPU IP in enhancing processing capabilities and achieving higher efficiencies in complex computational tasks has driven its adoption. The leading status of the CPU IP segment is further reinforced by ongoing advancements in technology, such as the development of multicore processors for mobile devices and the increasing integration of AI capabilities directly into CPU IP.

These innovations have expanded the applications of CPU IP beyond traditional computing environments into areas requiring high-speed data processing and real-time analytics. Additionally, the push towards smart manufacturing and the IoT has escalated the need for more powerful and efficient processors, thus propelling the CPU IP market growth.

Moreover, strategic collaborations and IP licensing agreements among key players in the semiconductor industry have played a crucial role in fostering the growth of the CPU IP segment. Companies are increasingly investing in research and development to innovate and enhance CPU IP solutions, aiming to cater to the growing requirements for energy-efficient and high-performance processors.

This focus on continuous improvement has not only solidified the dominance of CPU IP in the market but also ensured its pivotal role in the future trajectory of semiconductor technologies. Conclusively, the predominance of the CPU IP segment in the semiconductor processor IP market is a result of its critical function in advancing computing power, coupled with technological progress and strategic industry initiatives.

Application Analysis

In 2024, the Integrated Device Manufacturer (IDM) segment held a dominant market position within the semiconductor processor IP market, capturing more than a 25% share. This leadership is largely due to IDMs’ comprehensive control over the entire production process, from design and fabrication to assembly and testing, which enables a high degree of product customization and quality assurance.

The IDM segment’s leading position is also bolstered by its capacity to invest significantly in research and development. This investment drives innovation in semiconductor processor IP, leading to the development of proprietary technologies that offer competitive advantages in terms of performance, power efficiency, and miniaturization.

Furthermore, IDMs are able to respond more swiftly to changes in market demand and technology trends, which is critical in sectors such as consumer electronics and automotive, where the lifecycle of products is becoming increasingly shorter.

Additionally, IDMs benefit from stronger customer relationships through their ability to provide end-to-end semiconductor solutions. This capability is particularly valued by large original equipment manufacturers (OEMs) that seek to reduce complexity and ensure supply chain security. The trust and reliance placed by these OEMs on IDMs contribute significantly to the sustained market dominance of this segment.

Overall, the IDM segment’s control over extensive semiconductor manufacturing processes, combined with its robust R&D capabilities and strong OEM partnerships, positions it as a leader in the semiconductor processor IP market. As technology continues to advance and integration needs grow, the role of IDMs is expected to become even more pivotal, potentially expanding their market share further.

Key Market Segments

By Type

- CPU IP

- GPU IP

- Others

By Application

- IDM (Integrated Device Manufacturer)

- Wafer Foundry

- Fabless

- OSAT (Outsourced Semiconductor Assembly and Test)

Driver

Increasing Demand for Advanced Electronics

The semiconductor Processor IP market is predominantly driven by the escalating demand for more sophisticated electronics, including laptops, smartphones, and tablets. This surge is coupled with the growth in consumer electronics and automotive systems, fueled by advanced technologies like 5G and AI that require robust semiconductor IPs to enhance their performance and functionality.

Innovations in IoT and the continuous adoption of SoC designs further augment this demand, making Processor IP a critical component in various digital applications. The push towards more capable devices, paired with advancements in technology that aim to reduce power consumption while maximizing performance, substantiates the increasing reliance on Processor IPs, ensuring sustained market growth.

Restraint

Intellectual Property Security Concerns

One of the significant restraints facing the semiconductor Processor IP market is the ongoing concern regarding intellectual property security. As the integration and complexity of semiconductor IPs evolve, so do the risks associated with IP theft and unauthorized usage, which can lead to substantial financial losses and reputational damage for companies.

These security challenges are compounded by the global nature of the semiconductor industry, where IPs are often developed, shared, and utilized across international borders, making enforcement of protections and legal recourse more complicated. This environment of heightened risk necessitates advanced security solutions and rigorous IP protection strategies to mitigate potential infringements.

Opportunity

Expansion in Emerging Markets

Emerging markets present a significant opportunity for the expansion of the semiconductor Processor IP sector. Countries like China and India are witnessing rapid technological advancements and significant investments in electronics manufacturing. Additionally, regions such as Latin America and the Middle East are experiencing growth in consumer electronics due to increasing disposable incomes and economic development.

These factors collectively create a fertile ground for the proliferation of semiconductor IPs, particularly as these regions continue to integrate more technology into everyday consumer products and industrial applications. The rising demand in these markets offers a lucrative opportunity for market players to introduce innovative products and expand their global footprint.

Challenge

Rapid Pace of Technological Change

The semiconductor Processor IP market faces the challenge of keeping pace with the rapid technological changes. The continuous evolution in the tech landscape demands constant innovation and frequent updates to semiconductor IPs to stay relevant and competitive.

This fast-paced environment can strain resources, as companies must invest heavily in research and development to keep up with the advancements in AI, machine learning, and other emerging technologies that reshape the semiconductor industry.

Additionally, the shift towards specialized architectures for new applications adds another layer of complexity, requiring tailored solutions that can quickly adapt to changing technological requirements and market demands.

Growth Factors

Robust Demand Across Diverse Applications

The semiconductor Processor IP market is experiencing significant growth, driven by a robust demand across various applications, including consumer electronics, automotive systems, and telecom & data centers. The integration of advanced technologies such as 5G, AI, and IoT into these sectors requires sophisticated semiconductor IPs that enhance device functionality and interconnectivity.

This trend is further bolstered by the increasing use of connected devices and the rise in consumer preference for high-performance electronics, which necessitate continual advancements in semiconductor technology. Additionally, the market is benefiting from reduced design and manufacturing costs, allowing for more widespread adoption and innovation in semiconductor IPs.

Emerging Trends

AI and Advanced Technologies

Artificial Intelligence (AI) is revolutionizing the semiconductor IP market by streamlining design processes, enhancing operational efficiency, and reducing time-to-market for new technologies. AI-driven tools are being increasingly employed to automate complex design tasks, optimize chip performance, and predict manufacturing issues, thus minimizing errors and production costs.

This incorporation of AI is not only improving the quality and efficiency of semiconductor manufacturing but is also fostering the development of new chip architectures tailored for AI applications, including those needed for deep learning and neural network processing. These advancements are setting the stage for next-generation semiconductor IPs that can handle increasingly complex computations required in modern digital applications.

Business Benefits

Strategic Market Advantages

The adoption of advanced semiconductor IPs offers significant business benefits, including enhanced product performance and competitive differentiation. Companies that integrate cutting-edge IPs into their product lines can achieve superior device functionality, which is critical for consumer electronics and automotive applications where performance and reliability are key.

Furthermore, the ability to rapidly deploy innovative products with advanced features allows companies to capture and retain market leadership in fast-evolving industries. By leveraging semiconductor IPs, businesses can not only enhance their product offerings but also streamline their development processes and reduce time-to-market, providing them with a strategic advantage in the global market.

Regional Analysis

In 2024, Asia-Pacific held a dominant market position in the Semiconductor Processor IP sector, capturing more than a 40% share with a revenue of USD 1,621.4 million. This region’s leadership in the market can be attributed to several compelling factors.

Firstly, rapid industrialization across major economies such as China, India, and South Korea has significantly boosted demand for semiconductor IPs. These countries have seen substantial investments in technology infrastructure, which in turn has spurred growth in sectors reliant on advanced semiconductor technologies.

Moreover, the Asia-Pacific region benefits from a strong foundation in electronics manufacturing. Countries like China and Japan are not only major producers but also large consumers of semiconductor IPs, driven by their robust consumer electronics and automotive industries. This internal ecosystem supports a continuous cycle of innovation and consumption, reinforcing the region’s market position.

Additionally, governmental policies and a favorable economic environment further enhance the region’s attractiveness to semiconductor companies. Initiatives aimed at boosting technological advancements have led to the development of integrated circuits and semiconductor devices that are crucial for modern electronics. This supportive regulatory framework helps maintain the region’s competitive edge in the global market.

The strategic collaborations and partnerships within the Asia-Pacific semiconductor industry also play a critical role. These alliances across companies streamline the integration of semiconductor IPs into various applications, ensuring compatibility, performance, and reliability. Such collaborations are vital for keeping up with the rapid pace of technological changes and market demands, making Asia-Pacific a pivotal area for growth in the semiconductor IP landscape.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

The semiconductor processor IP market is a dynamic sector characterized by rapid innovation and strategic maneuvers among key players.

ARM has been prominently featured in the semiconductor industry’s news due to its acquisition activities and strategic movements in the market. A key event was the attempted $40 billion acquisition by Nvidia, which would have been one of the largest deals in the semiconductor sector. This acquisition was scrutinized heavily by international regulators over concerns that it could lead to reduced competition and innovation.

Synopsys has made significant strides through acquisitions and new product launches, solidifying its position in the market. The company has expanded its IP portfolio by acquiring more niche technology providers, enhancing its capabilities in areas such as optical solutions and digital design.

Cadence has actively engaged in expanding its influence and capabilities in the semiconductor IP market through strategic acquisitions and the launch of innovative products. By integrating newly acquired technologies, Cadence has been able to offer comprehensive solutions that support the end-to-end design and analysis of semiconductor products.

Top Key Players in the Market

- ARM

- Synopsys

- Cadence

- Imagination

- CEVA

- Alphawave Semi

- Achronix

- Lattice Semiconductor

- VeriSilicon

- Faraday

- ASR Microelectronics

- Cambricon Technologies

- C*core Technology

- Huaxia Smart Photon Technology

- Nuclei System Technology

- StarFive

- Andes Technology

- Other Key Players

Recent Developments

- In January 2025, Faraday introduced an updated version of its LPDDR5X memory IP, which promises improved energy efficiency and higher speeds, targeting applications in mobile devices and high-performance computing.

- In March 2025, VeriSilicon unveiled a new line of custom SoCs optimized for automotive applications, focusing on safety and reliability standards necessary for autonomous driving technologies.

- In October 2024, Cadence launched a new suite of power-efficient IP solutions tailored for PCI Express 6.0, aimed at enhancing performance in hyper-scale computing environments. This launch reflects Cadence’s ongoing commitment to innovation in semiconductor design.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 4,053.7 Mn |

| Forecast Revenue (2034) | USD 8,049.1 Mn |

| CAGR (2025-2034) | 7.1% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments |

| Segments Covered | By Type (CPU IP, GPU IP, Others), By Application (IDM (Integrated Device Manufacturer), Wafer Foundry, Fabless, OSAT (Outsourced Semiconductor Assembly and Test)) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | ARM, Synopsys, Cadence, Imagination, CEVA, Alphawave Semi, Achronix, Lattice Semiconductor, VeriSilicon, Faraday, ASR Microelectronics, Cambricon Technologies, C*core Technology, Huaxia Smart Photon Technology, Nuclei System Technology, StarFive, Andes Technology, Other Key Players |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three license to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |