Quick Navigation

Report Overview

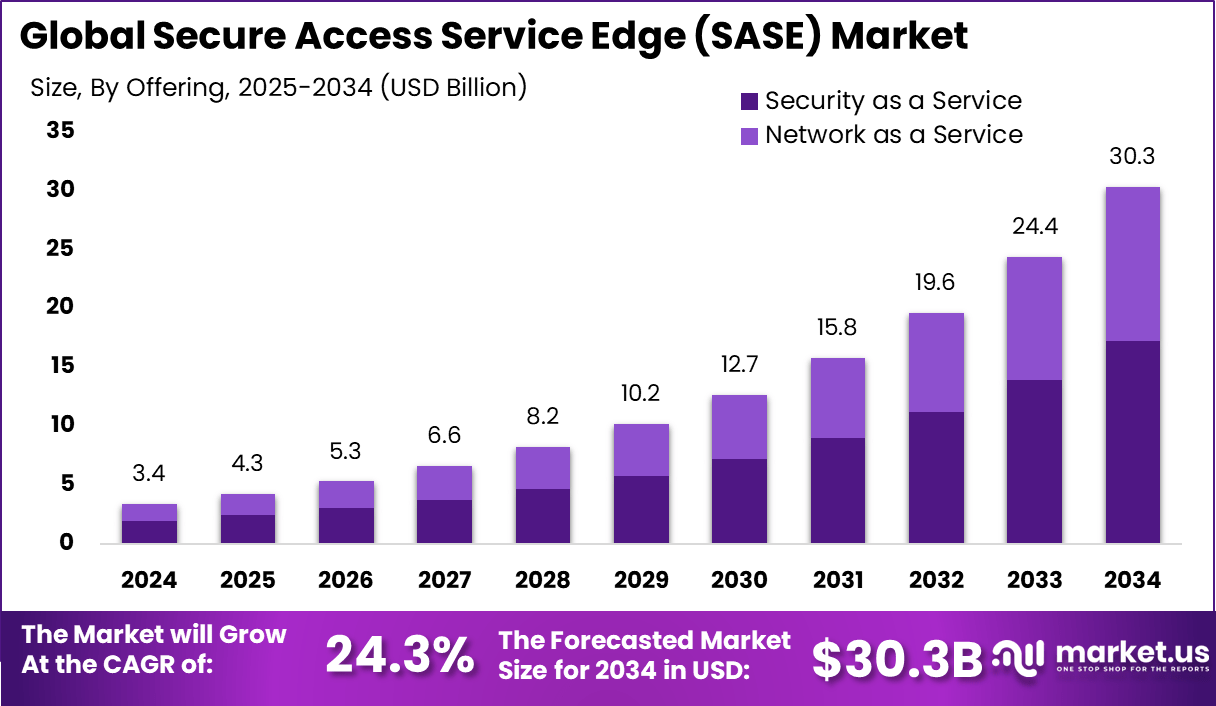

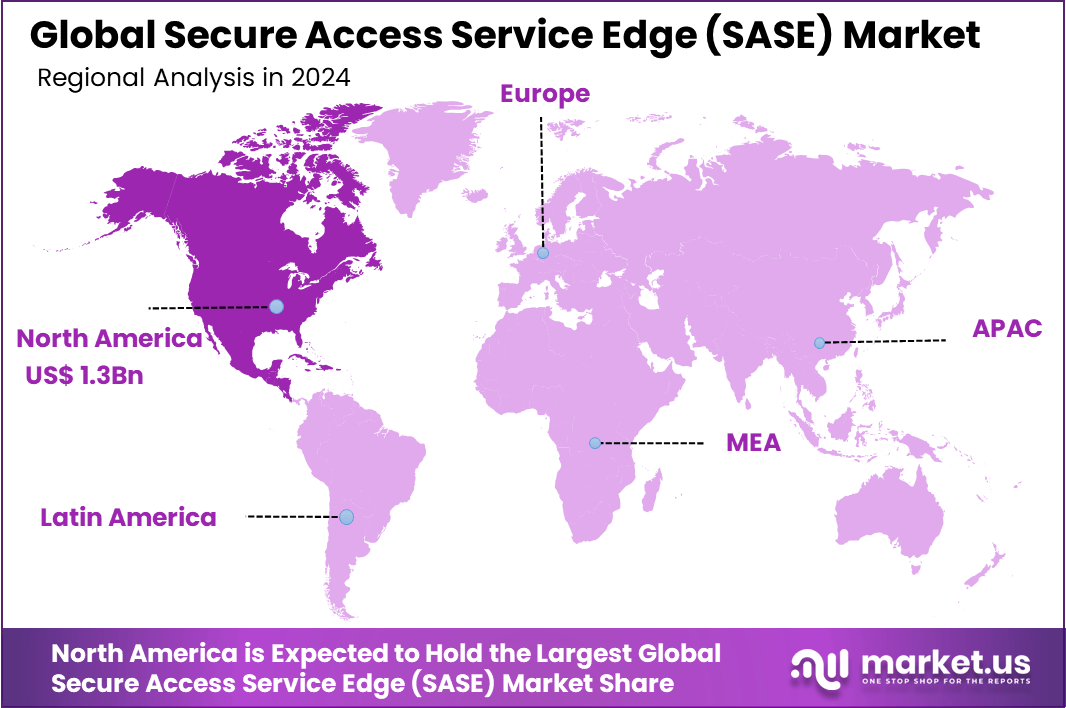

The Global Secure Access Service Edge Market size is expected to be worth around USD 30.3 Billion By 2034, from USD 3.4 billion in 2024, growing at a CAGR of 24.3% during the forecast period from 2025 to 2034. In 2024, North America held a dominant market position, capturing more than a 40% share, holding USD 1.3 Billion revenue.

The global secure access service edge market is being driven by the growing demand for secure data access and network protection. This growth is further supported by the increasing shift of large enterprises toward cloud-based solutions, rapid digitalization across industries, expanding internet penetration, and the rising adoption of edge computing. These factors collectively emphasize the need for integrated, cloud-native security frameworks, positioning SASE as a critical architecture for modern enterprise networks.

The primary drivers fuelling SASE market expansion include rapid adoption of remote and hybrid work models, digital transformation accelerating cloud service usage, and escalating cyber threats that expose the limitations of traditional security strategies. Enterprises transitioning from centralized data environments to dispersed cloud and edge infrastructures find SASE’s identity‑driven, zero‑trust security model essential for managing diverse endpoints and regulatory compliance.

The increasing adoption of enabling technologies such as SD‑WAN, cloud computing, and zero‑trust architectures is a critical enabler for SASE deployment. SD‑WAN provides scalable and dynamic connectivity, while CASB, ZTNA, SWG, and FWaaS offer layered security. These technologies support real‑time contextual access control and routing from distributed points of presence, reducing latency and providing a consistent user experience.

Enterprises are adopting SASE for several compelling reasons: to improve security posture with zero‑trust assurance; to unify management of networking and security under a cloud‑delivered model; to reduce both capital and operational expenses by eliminating fragmented point solutions; and to scale access efficiently for global workforces. Vendors report improved performance, lower latency, and simplified policy consistency across branches, remote users, and cloud applications.

Key Takeaways

- The Global Secure Access Service Edge (SASE) Market is projected to reach USD 30.3 Billion by 2034, rising from USD 3.4 Billion in 2024.

- A robust CAGR of 24.3% is expected during the forecast period from 2025 to 2034.

- In 2024, North America emerged as the dominant region, accounting for over 40% share, which translates to USD 1.3 Billion in revenue.

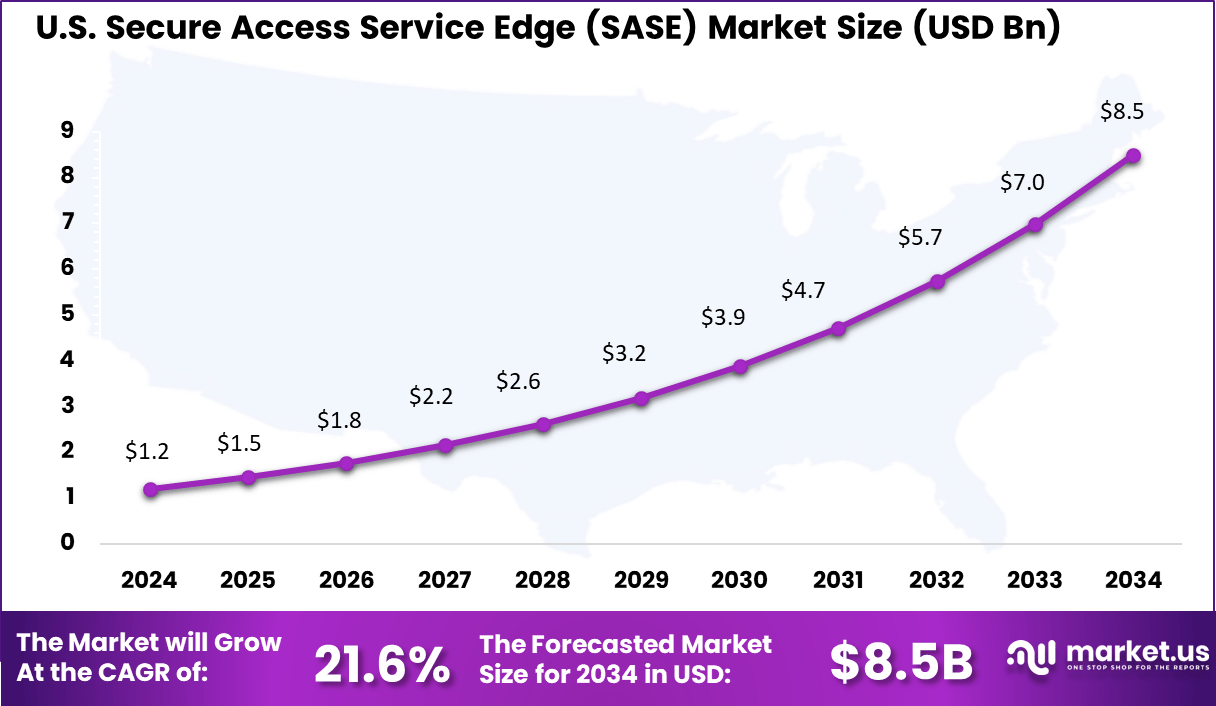

- The United States alone contributed USD 1.2 Billion, supported by a steady CAGR of 21.6%.

- Based on offering, Security as a Service (SECaaS) dominated the market with a 57% share in 2024.

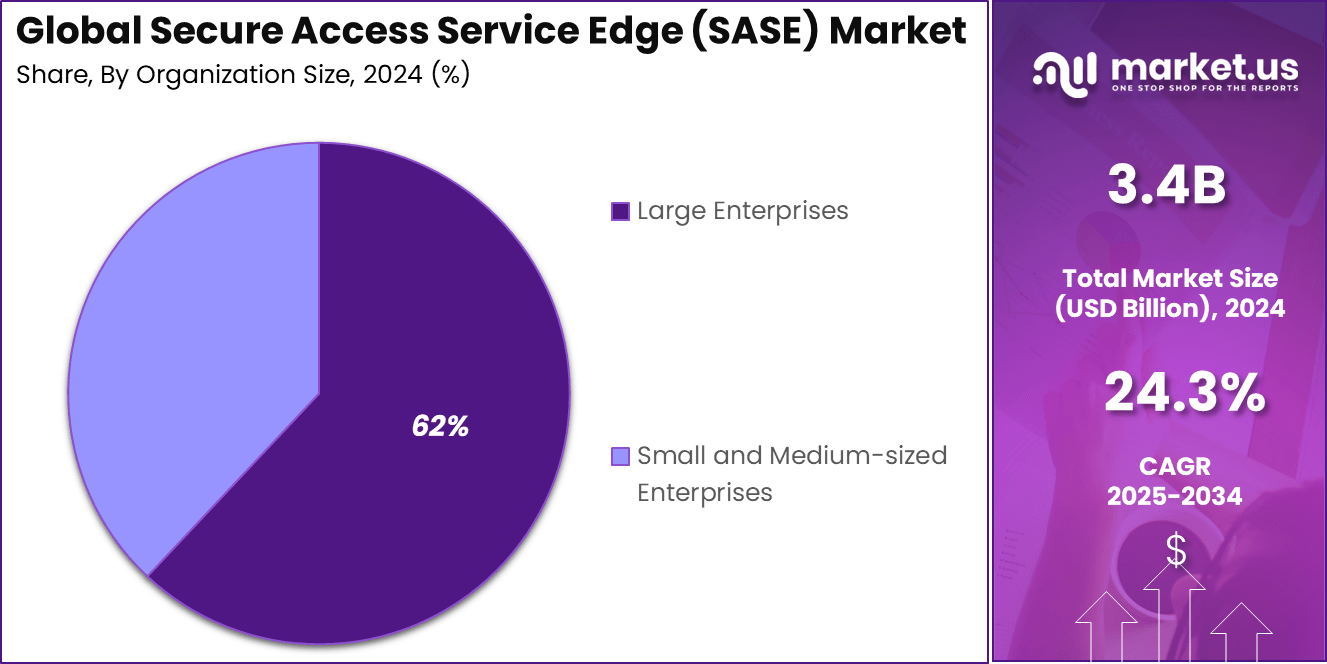

- By organization size, Large Enterprises held a clear lead, capturing 62% of the market share.

- In terms of verticals, the IT & Telecom sector accounted for the highest share at 25%, highlighting its critical need for secure, scalable access solutions.

US Market Expansion

The US Secure Access Service Edge (SASE) Market is valued at approximately USD 1.2 Billion in 2024 and is predicted to increase from USD 3.2 Billion in 2029 to approximately USD 8.5 Billion by 2034, projected at a CAGR of 21.6% from 2025 to 2034.

In 2024, North America held a dominant market position, capturing more than a 40% share, holding approximately USD 1.3 Billion in revenue in the global Secure Access Service Edge (SASE) market. This leadership can be attributed to the early adoption of cloud-native architectures and the region’s mature digital infrastructure.

Enterprises across the United States and Canada have accelerated the transition to remote and hybrid work models, creating urgent demand for integrated network and security frameworks such as SASE. The concentration of key technology vendors and cybersecurity innovators in North America has further enabled rapid deployment and continuous innovation in this space.

The dominance of North America has also been supported by increased investments from both public and private sectors in zero trust network access (ZTNA), secure web gateways, and cloud access security brokers. The region’s strict regulatory environment, particularly in sectors such as finance, healthcare, and defense, has pushed organizations to prioritize secure and scalable connectivity models.

For instance, In January 2024, Kyndryl partnered with Cisco to launch two new security edge services, aimed at improving threat response and strengthening security controls. Together with their SD-WAN solutions, these services support a smooth transition to secure access service edge (SASE) architecture for enterprises.

By Offering Analysis

In 2024, Security as a Service (SECaaS) segment held a dominant market position, capturing more than 57% share within the SASE ecosystem. This leading share can be attributed to its intrinsic alignment with modern enterprise requirements for scalable, subscription‑based security solutions that preclude the need for significant on‑premises infrastructure.

Moreover, the multitenant nature of SECaaS enabled faster deployment and continual updates, which are vital to counteract the rapidly evolving threat landscape-rendering it more attractive than Network‑as‑a‑Service offerings for hybrid and remote workforce scenarios. Furthermore, the resilience and agility delivered by SECaaS were decisive factors in its market leadership.

By anchoring security at the cloud edge, enterprises achieved consistent enforcement of security postures irrespective of user location, effectively simplifying compliance efforts amid tightening regulations such as GDPR, HIPAA, and ISO standards. The cloud‑native architecture also facilitated centralized visibility and analytics, enabling real‑time threat detection and automated remediation – capabilities that were highly valued in sectors like banking, healthcare, and IT services.

By Organization Size Analysis

In 2024, Large Enterprises segment held a dominant market position, capturing more than a 62% share of the Secure Access Service Edge (SASE) market. This leadership can be attributed to the complex and expansive IT environments typical of large organizations, which demand scalable, cloud-native networking and security frameworks.

Those enterprises oversee extensive branch offices, distributed workforces, and significant volumes of sensitive data – driving the need for integrated solutions that converge networking and security at scale. Their rigorous compliance mandates and global operations further necessitate robust zero‑trust architectures and comprehensive threat protection, both core tenets of SASE

Large enterprises possess the financial and operational resources to deploy full-suite SASE platforms, enabling centralized security policy enforcement across cloud, on‑premises, and edge environments. This capability supports seamless connectivity for remote and hybrid work models, reduces latency, and strengthens user application experience – factors that are vital for entities in heavily regulated sectors such as BFSI, healthcare, and government.

By Industry Vertical Analysis

In 2024, the IT & Telecom segment held a dominant market position in the Secure Access Service Edge (SASE) space, capturing more than a 25% share of total industry revenue. This commanding lead is attributed to the segment’s inherent requirement for expansive, secure, and high‑performance networking solutions capable of supporting large subscriber bases, 5G roll‑outs, and intricate multi‑cloud backbones.

Telecom carriers and IT service providers serve as both consumers and implementers of SASE, driving early adoption to modernize legacy infrastructure, package integrated security into network services, and support mobile and edge‑centric workflows at scale.

The segment’s status as a technology innovator and large‑scale network operator incentivizes investment in SASE platforms that blend SD‑WAN, zero‑trust access, and cloud‑native security. Ongoing 5G expansion and edge computing deployments have amplified the need for seamless, dynamic security enforcement across distributed points of presence.

Key Market Segments

By Offering

- Network as a Service

- Security as a Service

By Organization Size

- Small & Medium Enterprises

- Large Enterprises

By Industry Vertical

- Government

- BFSI

- Retail & Ecommerce

- IT & Telecom

- Healthcare

- Energy & Utilities

- Others

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherlands

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Thailand

- Vietnam

- Rest of Latin America

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Emerging Trends

AI-Driven Threat Detection

The integration of artificial intelligence (AI) into SASE solutions is becoming increasingly widespread. Providers are enhancing their platforms with AI and machine learning to enable real-time threat detection, automated policy adjustments, and intelligent traffic routing.

Enterprises are responding positively to these enhancements. AI-enabled SASE platforms are improving incident response times and reducing manual oversight, making them attractive to organizations managing complex, hybrid IT environments.

Driver

Escalating Cybercrime & Cloud‑Native Workforce

The frequency and severity of cyberattacks – such as ransomware, phishing, and data breaches – are rising sharply, exposing the limitations of perimeter-based security models. Traditional architectures struggle to protect remote, hybrid workforces and cloud-hosted assets. SASE addresses this gap through a cloud‑delivered, identity‑centric framework that secures every connection from any user, on any device, to any application.

Simultaneously, the widespread transition to cloud computing and remote work is fueling demand for flexible, secure, and efficient connectivity. SASE’s integration of SD‑WAN, secure web gateways, zero-trust network access (ZTNA), CASB, and firewall‑as‑a‑service (FWaaS) meets these needs. Organizations are choosing SASE to ensure secure, consistent access across geographically dispersed users and assets, aligning with evolving business practices and regulatory expectations.

Restraint

Implementation Complexity & Knowledge Gaps

Despite its benefits, SASE remains complex to adopt. Organizations – especially those with legacy infrastructure – often struggle with the integration of multiple components into a cohesive, cloud-native framework. This complexity introduces challenges related to design, configuration, interoperability, and migration.

In addition, many IT teams lack experience with cloud-based security architectures and SD-WAN strategies. As a result, misunderstandings, misconfigurations, and delays in deployment are common. This knowledge gap is a significant barrier that slows down meaningful SASE adoption.

Opportunity

AI‑Powered, Modular SASE Services

A key opportunity lies in the creation of modular, AI-enhanced SASE offerings tailored for mid‑market companies and global/regional compliance needs. Vendors that embed AI/ML for real-time policy automation and threat detection can win customers looking for smarter, self-optimizing security platforms.

Introducing modular structures and developer-friendly APIs enables integration with managed service providers (MSPs), fosters hybrid deployment, and reduces vendor lock‑in. This is especially appealing to enterprises in industries with strict data privacy laws, where local data handling and compliance are required.

Challenge

Vendor Lock‑In & Integration Frictions

One of the central challenges is avoiding dependence on single-vendor ecosystems, which often bundle SD-WAN, security, and management under one roof. Although this simplifies licensing and deployment, it can severely limit flexibility.

Organizations may find themselves locked into a single stack with minimal interoperability, making it difficult to adapt or mix-and-match best-in-class security components. Integration frictions with existing IT and networking infrastructure can impede modernization efforts.

Complex transition from MPLS to SD-WAN, merging legacy firewalls with cloud-native services, and extending zero-trust policies across multiple environments require careful planning. Insufficient architecture maturity or vendor flexibility can result in deployment delays, suboptimal performance, or security policy gaps.

Key Player Analysis

The secure access service edge (SASE) market is experiencing rapid growth, supported by innovation from key players. Barracuda Networks, Inc. focuses on strengthening cloud application security and remote access for dispersed workforces. Cato Networks delivers a unified SASE platform designed to streamline networking and security across cloud infrastructures.

Check Point Software Technologies Ltd. integrates SASE capabilities into its cybersecurity suite to safeguard data and applications from dynamic threats. Cisco Systems, Inc. leverages its broad portfolio to offer secure and scalable SASE solutions, enabling enterprises to transition effectively to cloud-centric operations.

Top Key Players Covered

- Cisco Systems Inc.

- Barracuda Networks Inc.

- Hewlett Packard Enterprise Development LP

- McAfee LLC

- Open Systems

- Broadcom

- VMWare Inc.

- Palo Alto Networks.

- Versa Networks Inc.

- Akamai Technologies Inc.

- Cato Networks

- Fortinet Inc.

- Check Point Software Technologies Ltd

- Cloudflare Inc.

- Forcepoint

- Others

Recent Developments

- In April 2025, ADAMnetworks was recognized in the 2025 Secure Access Service Edge Data Quadrant Report by Info-Tech Research, receiving high satisfaction scores for features like zero trust, ease of IT administration, and ongoing improvement – affirming its strength in zero trust security solutions.

- In February 2025, Versa introduced Versa Sovereign SASE™, enabling enterprises, governments, and service providers to deploy fully customized networking and security services directly from their own infrastructure using a flexible, do-it-yourself model.

- In June 2024, Tata Communications launched its Unified Hosted SASE solution, developed with Versa Networks, to offer global enterprises a platform that combines SSE and SD-WAN. This integrated solution enhances cloud performance, strengthens zero-trust security, and reduces operational costs.

- In November 2024, BT upgraded its managed secure SD-WAN service for UK public and business clients by integrating new SSE capabilities using Fortinet’s technology. This enhancement supports a seamless transition to SASE, ensuring secure cloud access and accelerating digital transformation.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 3.4 Bn |

| Forecast Revenue (2034) | USD 30.3 Bn |

| CAGR (2025-2034) | 24.3% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue forecast, AI impact on market trends, Share Insights, Company ranking, competitive landscape, Recent Developments, Market Dynamics and Emerging Trends |

| Segments Covered | By Offering (Network as a Service, Security as a Service), By Organization Size (Small & Medium Enterprises, Large Enterprises), By Industry Vertical (Government, BFSI, Retail & Ecommerce, IT & Telecom, Healthcare, Energy & Utilities, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Latin America; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Cisco Systems Inc., Barracuda Networks Inc., Hewlett Packard Enterprise Development LP, McAfee LLC, Open Systems, Broadcom, VMWare Inc., Palo Alto Networks, Versa Networks Inc., Akamai Technologies Inc., Cato Networks, Fortinet Inc., Check Point Software Technologies Ltd, Cloudflare Inc., Forcepoint, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three license to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |