Global Secondary Macronutrients Market Size, Share, And Enhanced Productivity By Nutrient (Calcium, Sulfur, Magnesium), By Form (Dry Form, Liquid Form), By Crop Type ((Cereals and Grains (Corn, Wheat, Rice, Others), Oilseeds and Pulses (Soybean, Sunflower, Others)), Fruits and Vegetables (Root and Tuber Vegetables, Leafy Vegetables, Pome Fruits, Berries, Citrus Fruits, Others), Others), By Application (Liquid Application (Fertigation, Foliar, Others), Solid Application (Broadcasting, Deep Tillage, Localized Placement)), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends, and Forecast 2026-2035

- Published date: March 2026

- Report ID: 181006

- Number of Pages: 289

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

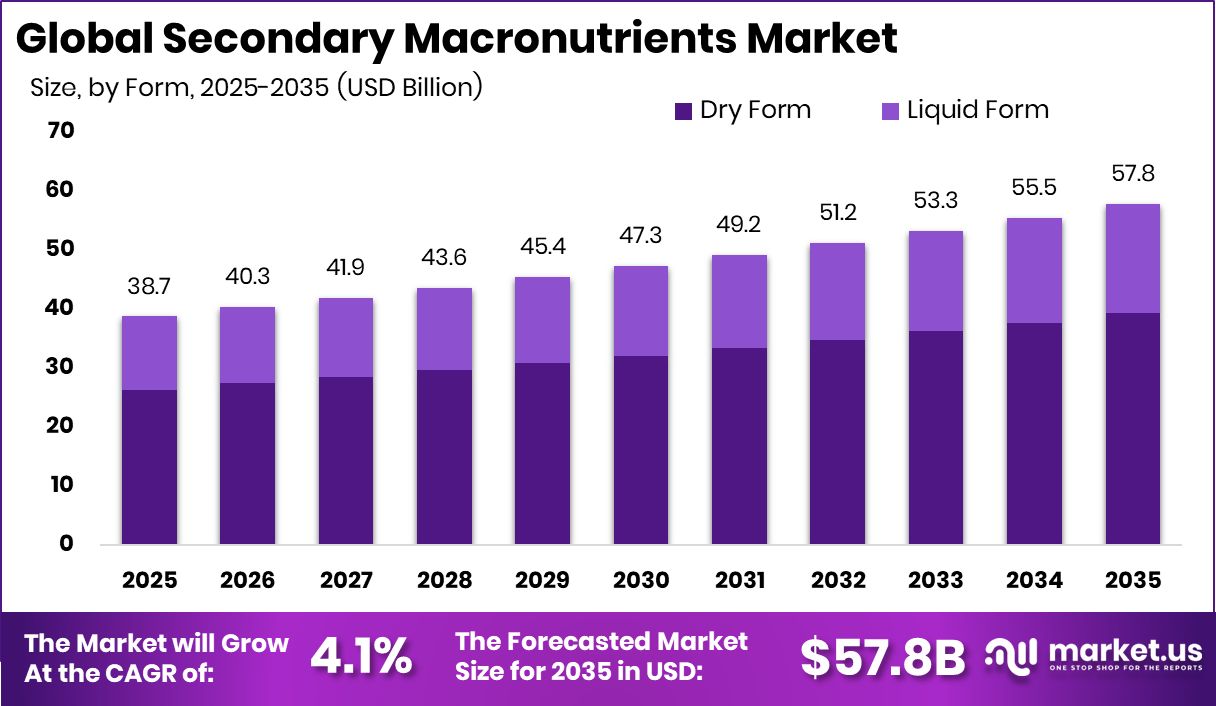

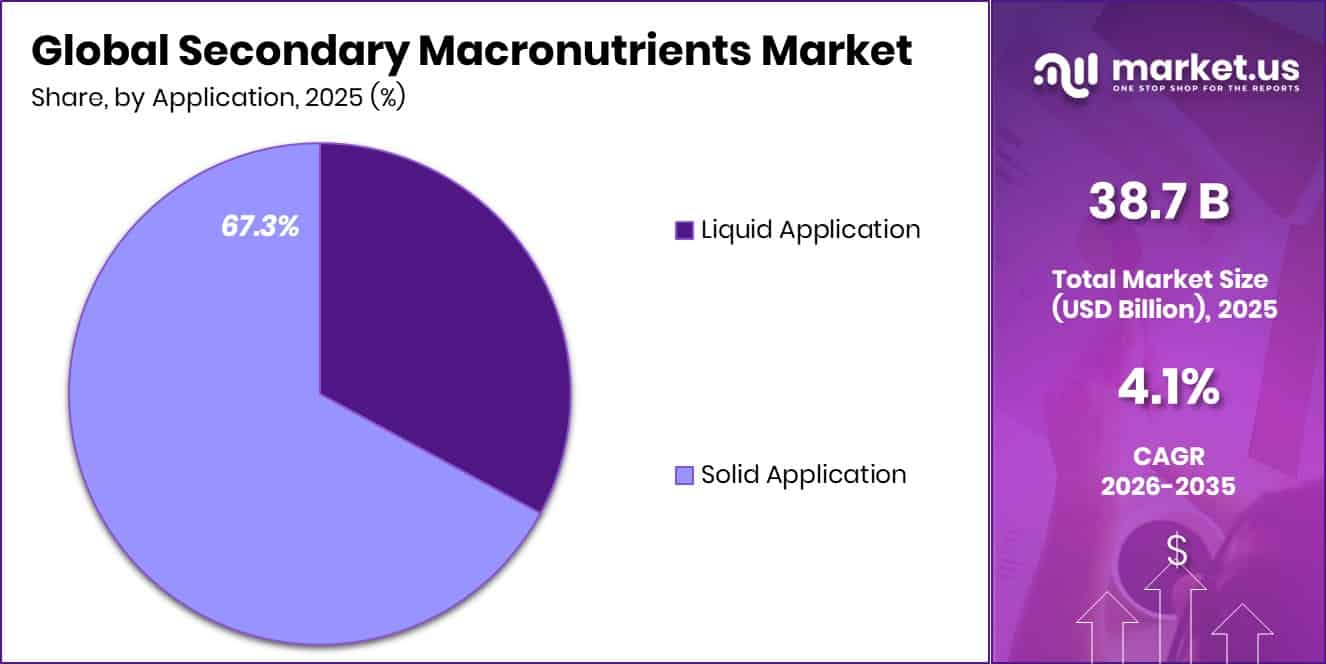

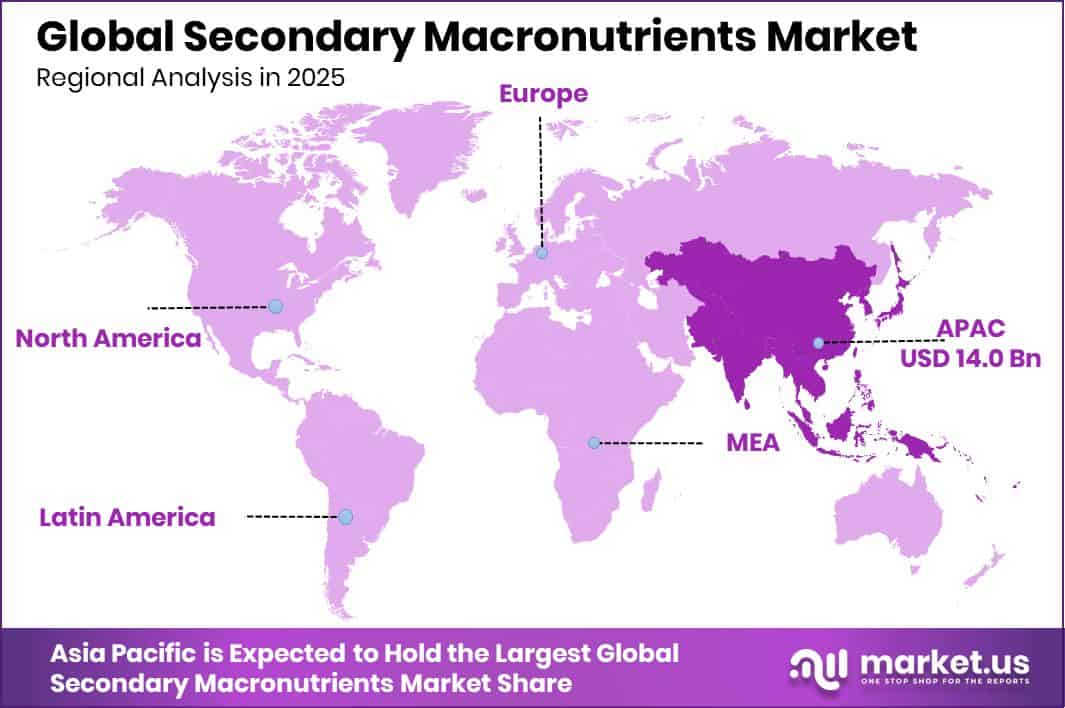

The Global Secondary Macronutrients Market is expected to be worth around USD 57.8 billion by 2035, up from USD 38.7 billion in 2025, and is projected to grow at a CAGR of 4.1% from 2026 to 2035. Secondary Macronutrients Market in Asia Pacific accounted for 36.4%, totaling nearly USD 14.0 Bn.

Secondary macronutrients are essential plant nutrients required in moderate amounts to support healthy crop growth and soil fertility. These nutrients mainly include calcium, sulfur, and magnesium, which play important roles in plant structure, enzyme activity, and nutrient absorption. Calcium helps strengthen plant cell walls, sulfur contributes to protein formation, and magnesium is a key component of chlorophyll used in photosynthesis. Farmers use fertilizers containing these nutrients to maintain soil balance and improve crop productivity. Proper management of secondary macronutrients helps crops grow stronger, enhances nutrient uptake from soil, and improves the overall quality of agricultural produce.

The Secondary Macronutrients Market refers to the supply and use of fertilizers that provide calcium, sulfur, and magnesium to crops. These products are available in dry and liquid forms and are widely applied across cereals and grains, oilseeds and pulses, fruits and vegetables, and other crops. Applications include liquid spraying and solid soil incorporation, depending on crop needs and farming practices. The market supports agricultural productivity by ensuring crops receive balanced nutrients required for growth and yield stability.

Growth in the market is mainly supported by increasing attention toward soil nutrient balance and long-term agricultural productivity. Continuous farming and intensive cultivation often reduce essential nutrients in soil, encouraging farmers to adopt fertilizers containing secondary macronutrients. Public investments and food system initiatives are also strengthening agricultural supply chains. For example, Apeel raised $250M in funding to accelerate fresh food supply chains, while Sufresca secured a $500k seed round for food coating innovations that help reduce food waste and maintain produce quality.

Demand for secondary macronutrients continues to rise as crop production expands and agricultural systems focus on improving yield quality. Support programs across the food and agriculture ecosystem also encourage better crop nutrition practices. The USDA has funded packaging innovations for the $143B specialty crop export industry, and food assistance programs remain important as Nevada may spend $7.3M to maintain food support for women and infants. These developments highlight the importance of maintaining a strong agricultural supply and crop quality.

Opportunities are also emerging through initiatives that promote fresh produce consumption and stronger distribution networks. For instance, Tesco extended its national Fruit & Veg for Schools programme with £4M in additional funding and plans to provide £4 million worth of fruits and vegetables to 400 schools this year. Such initiatives encourage higher fruit and vegetable production, which supports the need for balanced soil nutrients, including calcium, sulfur, and magnesium in agricultural cultivation.

Key Takeaways

- The Global Secondary Macronutrients Market is expected to be worth around USD 57.8 billion by 2035, up from USD 38.7 billion in 2025, and is projected to grow at a CAGR of 4.1% from 2026 to 2035.

- Sulfur dominates the Secondary Macronutrients Market, accounting for 45.8% due to its essential role in crop nutrition.

- Dry form leads the Secondary Macronutrients Market with 67.9%, favored for easier storage, transport, and application.

- Cereals and grains represent 39.6% of the Secondary Macronutrients Market, driven by global demand for staple crops.

- Solid application holds 67.3% share in the Secondary Macronutrients Market, ensuring efficient nutrient delivery and soil absorption.

- Asia Pacific dominated the Secondary Macronutrients Market with 36.4%, valued at around USD 14.0 Bn.

By Nutrient Analysis

Sulfur leads the Secondary Macronutrients Market with 45.8% nutrient share globally.

In 2025, sulfur accounted for 45.8% of the Secondary Macronutrients Market by nutrient type, reflecting its strong importance in modern agricultural practices. Sulfur plays a critical role in plant metabolism, protein synthesis, and chlorophyll formation, making it essential for improving crop quality and yield. Farmers are increasingly recognizing sulfur deficiency in soils due to reduced atmospheric sulfur deposition and intensive farming practices.

As a result, sulfur-based fertilizers are gaining wider adoption across different crop systems. The demand is particularly high in regions with sulfur-deficient soils where crop productivity depends heavily on balanced nutrient management. Additionally, the growing emphasis on sustainable agriculture and soil health management is supporting the steady expansion of sulfur-based secondary macronutrient products in the global agricultural input market.

By Form Analysis

Dry form dominates the Secondary Macronutrients Market, holding 67.9% share globally.

In 2025, dry form fertilizers held a 67.9% share of the Secondary Macronutrients Market by form, driven by their ease of storage, longer shelf life, and convenience in transportation. Dry fertilizers such as granules and powders are widely preferred by farmers because they can be applied through conventional fertilizer spreading equipment. Their compatibility with bulk blending techniques also allows manufacturers to create customized nutrient mixes tailored to specific soil and crop requirements.

Furthermore, dry formulations tend to be more cost-effective compared to liquid alternatives, making them suitable for large-scale farming operations. Many agricultural cooperatives and fertilizer distributors also favor dry products due to simplified logistics and reduced handling complexities. These factors collectively contribute to the continued dominance of dry form secondary macronutrient fertilizers in the agricultural sector.

By Crop Type Analysis

Cereals and grains dominate the Secondary Macronutrients Market with 39.6% demand.

In 2025, cereals and grains accounted for 39.6% of the Secondary Macronutrients Market by crop type, highlighting the strong demand for balanced nutrient management in staple crop production. Crops such as wheat, rice, maize, and barley require adequate levels of calcium, magnesium, and sulfur to support healthy plant development and optimal grain formation. The rising global population and increasing demand for staple foods have intensified efforts to improve crop productivity and soil fertility.

Secondary macronutrients help enhance nutrient uptake efficiency and improve crop resilience against environmental stress. In many regions, soil nutrient depletion caused by continuous cereal cultivation has further increased the need for secondary nutrient supplementation. Consequently, farmers are increasingly integrating these nutrients into fertilization programs to maintain consistent yields and improve crop quality.

By Application Analysis

Solid application leads the Secondary Macronutrients Market with 67.3% usage globally.

In 2025, solid application methods represented 67.3% of the Secondary Macronutrients Market by application, as they remain the most commonly used approach for delivering nutrients to crops. Solid fertilizers are typically applied through broadcasting, band placement, or incorporation into soil before planting. These methods allow nutrients such as calcium, magnesium, and sulfur to be distributed evenly across agricultural fields, ensuring consistent nutrient availability during plant growth.

Farmers often prefer solid applications because they are compatible with standard agricultural machinery and require minimal modification to existing farming practices. Additionally, solid fertilizers can provide gradual nutrient release, which supports sustained crop nutrition throughout the growing season. This practicality and reliability continue to drive the widespread adoption of solid application methods in agricultural nutrient management.

Key Market Segments

By Nutrient

- Calcium

- Sulfur

- Magnesium

By Form

- Dry Form

- Liquid Form

By Crop Type

- Cereals and Grains

- Corn

- Wheat

- Rice

- Others

- Oilseeds and Pulses

- Soybean

- Sunflower

- Others

- Fruits and Vegetables

- Root and Tuber Vegetables

- Leafy Vegetables

- Pome Fruits

- Berries

- Citrus Fruits

- Others

- Others

By Application

- Liquid Application

- Fertigation

- Foliar

- Others

- Solid Application

- Broadcasting

- Deep Tillage

- Localized Placement

Driving Factors

Rising demand for balanced crop nutrition

Balanced crop nutrition has become an important focus in modern agriculture as farmers seek to maintain soil productivity and improve crop quality. The Secondary Macronutrients Market is influenced by this shift, as nutrients such as calcium, sulfur, and magnesium help support plant growth and nutrient absorption. Farmers are increasingly applying these nutrients to maintain soil balance after repeated crop cultivation. Innovation in plant-based agricultural ingredients is also supporting this direction.

For example, Cano-ela raised €1.6M to extract innovative plant-based ingredients from oilseeds, highlighting growing investment in agricultural raw materials and nutrient-rich crops. Such developments encourage the cultivation of oilseeds and other nutrient-intensive crops, indirectly increasing the importance of secondary macronutrient inputs to maintain soil health and sustain long-term crop productivity.

Restraining Factors

High fertilizer production and transportation costs

The Secondary Macronutrients Market is also influenced by challenges related to fertilizer production and distribution costs. Manufacturing nutrient fertilizers requires energy, processing, and logistics infrastructure, which can increase overall costs for producers and farmers. Transportation and supply chain pressures can also limit the availability of fertilizers in certain regions. Broader developments across the agricultural investment landscape highlight these financial pressures.

In the agrifood sector, Paine Schwartz launched a $1.7bn agrifood fund, while Cricket One unveiled a new plant, demonstrating large capital requirements for food and agriculture infrastructure. At the same time, Infarm was declared bankrupt, showing the financial challenges faced by some agricultural technology ventures. These mixed developments illustrate how operational and financial constraints can affect investments across agricultural input and supply systems.

Growth Opportunity

Expanding fruit and vegetable cultivation globally

Expanding fruit and vegetable cultivation is creating new opportunities for the Secondary Macronutrients Market. Fruits, vegetables, and oilseed crops often require balanced soil nutrients to maintain plant health, yield stability, and produce quality. As cultivation areas expand to meet consumer demand for fresh food products, farmers increasingly focus on soil nutrient management. Infrastructure investments and research programs are also supporting agricultural development.

For instance, Moldova’s Trans-Oil Group received a EUR 24 million grant for an oilseed processing plant in Romania, strengthening regional oilseed supply chains. In addition, Michigan State University researchers are leading an $11 million study to deepen understanding of camelina, an oilseed crop used in various agricultural and industrial applications. These developments encourage crop production expansion, creating stronger demand for nutrient management inputs, including secondary macronutrients.

Latest Trends

Growing use of sulfur enriched fertilizers

One notable trend influencing the Secondary Macronutrients Market is the increasing use of sulfur-enriched fertilizers. Sulfur plays an important role in plant metabolism and protein formation, making it valuable for improving crop quality and supporting plant development. Farmers are increasingly recognizing sulfur deficiencies in soil and are adopting fertilizers containing this nutrient to maintain crop productivity.

Industry investments in oilseed processing and biofuel production are also shaping agricultural demand patterns. For example, GrainCorp placed a $500 million-plus price tag on an oilseed processing plant as part of the growing biofuels sector. Expansion in oilseed processing encourages the cultivation of crops that rely on balanced soil nutrients, indirectly supporting the need for fertilizers containing secondary macronutrients such as sulfur, calcium, and magnesium.

Regional Analysis

In the Secondary Macronutrients Market, Asia Pacific held 36.4% share, reaching USD 14.0 Bn.

The Secondary Macronutrients Market demonstrates varied growth patterns across North America, Europe, Asia Pacific, the Middle East & Africa, and Latin America, reflecting regional agricultural practices and soil nutrient requirements. Asia Pacific emerged as the dominating region, accounting for 36.4% of the market with a value of USD 14.0 Bn, supported by extensive agricultural activity and strong demand for crop nutrient management across major farming economies. The region’s large cultivation areas for cereals, grains, and other staple crops contribute significantly to the consistent consumption of secondary macronutrient fertilizers.

North America represents a mature agricultural market where the adoption of balanced fertilization practices supports steady demand for calcium, magnesium, and sulfur-based inputs. Europe also maintains a stable position in the market, driven by structured farming systems and the continuous focus on soil productivity and nutrient balance.

Meanwhile, the Middle East & Africa region reflects gradual market expansion as farmers increasingly adopt nutrient management practices to improve crop output under challenging soil conditions. Latin America also contributes to market development through expanding agricultural cultivation and fertilizer utilization across key crop-producing areas.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Nutrien Ltd. remains one of the most influential participants in the global Secondary Macronutrients Market due to its integrated fertilizer production and extensive agricultural supply network. The company’s operational structure allows it to support farmers through a broad portfolio of crop nutrients and agronomic solutions. Nutrien’s scale of operations and distribution capabilities enable consistent product availability across major agricultural regions. From an analyst perspective, the company’s strength lies in its ability to combine nutrient production with retail agricultural services, which helps maintain strong relationships with growers. This integrated approach supports stable participation in markets where secondary macronutrients such as sulfur, calcium, and magnesium play an important role in maintaining soil fertility and improving crop performance.

Yara is recognized for its strong position in crop nutrition and fertilizer solutions, which supports its involvement in the Secondary Macronutrients Market. The company focuses on nutrient efficiency and balanced fertilization practices that align with modern agricultural requirements. Analysts observe that Yara’s global operational presence and technical expertise in plant nutrition provide a competitive advantage in supplying nutrient solutions to different farming systems. Its focus on agronomic knowledge and product development contributes to the availability of fertilizers designed to improve soil nutrient balance and crop productivity.

The Mosaic Company also holds a notable position in the global fertilizer industry, contributing to the Secondary Macronutrients Market through its fertilizer production and supply capabilities. The company’s expertise in nutrient-based agricultural inputs allows it to support farmers with products that address soil nutrient deficiencies. Analysts note that Mosaic’s operational experience in fertilizer manufacturing and distribution strengthens its role in global agricultural input supply chains.

Top Key Players in the Market

- Nutrien Ltd.

- Yara

- The Mosaic Company

- Israel Chemicals Ltd.

- K+S Aktiengesellschaft

- Nufarm

- SPIC

- Koch Industries, INC.

- Coromandel International Ltd

- Deepak Fertilisers and Petrochemicals Corporation Ltd.

- Haifa Negev Technologies LTD

Recent Developments

- In September 2025, Nutrien Ltd., a global fertilizer producer supplying crop nutrients including secondary macronutrients, announced the sale of its 50% stake in Argentina-based nitrogen producer Profertil for about $600 million. The move supports Nutrien’s strategy to focus on core fertilizer assets and strengthen its crop nutrient business.

- In July 2024, Yara, a global company working in crop nutrition and fertilizer solutions, continued expanding its Yara Climate Choice fertilizers portfolio in 2024. These fertilizers are produced with new technologies that reduce carbon emissions during production while maintaining crop nutrition quality. The development supports farmers using balanced nutrients such as nitrogen and sulfur to improve crop growth.

Report Scope

Report Features Description Market Value (2025) USD 38.7 Billion Forecast Revenue (2035) USD 57.8 Billion CAGR (2026-2035) 4.1% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Nutrient (Calcium, Sulfur, Magnesium), By Form (Dry Form, Liquid Form), By Crop Type ((Cereals and Grains (Corn, Wheat, Rice, Others), Oilseeds and Pulses (Soybean, Sunflower, Others)), Fruits and Vegetables (Root and Tuber Vegetables, Leafy Vegetables, Pome Fruits, Berries, Citrus Fruits, Others), Others), By Application (Liquid Application (Fertigation, Foliar, Others), Solid Application (Broadcasting, Deep Tillage, Localized Placement)) Regional Analysis North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA Competitive Landscape Nutrien Ltd., Yara, The Mosaic Company, Israel Chemicals Ltd., K+S Aktiengesellschaft, Nufarm, SPIC, Koch Industries, INC., Coromandel International Ltd, Deepak Fertilisers and Petrochemicals Corporation Ltd., Haifa Negev Technologies LTD Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)  Secondary Macronutrients MarketPublished date: March 2026add_shopping_cartBuy Now get_appDownload Sample

Secondary Macronutrients MarketPublished date: March 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- Nutrien Ltd.

- Yara

- The Mosaic Company

- Israel Chemicals Ltd.

- K+S Aktiengesellschaft

- Nufarm

- SPIC

- Koch Industries, INC.

- Coromandel International Ltd

- Deepak Fertilisers and Petrochemicals Corporation Ltd.

- Haifa Negev Technologies LTD

Our Clients

- 181006

- March 2026