Global Satcom Terminal Market Size, Share, Growth Analysis By Type (C Band, X Band, S Band, Ku Band, Ka Band), By Terminal Type (Fixed, Mobile), By Application (Civil Use, Military Use), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2026-2035

- Published date: Apr 2026

- Report ID: 183663

- Number of Pages: 333

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

Global Satcom Terminal Market size is expected to be worth around USD 15.2 Billion by 2035 from USD 7.6 Billion in 2025, growing at a CAGR of 7.1% during the forecast period 2026 to 2035.

Satellite communication terminals serve as the ground-side hardware that connects users to orbiting satellite networks. These systems enable voice, data, and broadband transmission across fixed and mobile platforms. Defense agencies, maritime operators, aviation providers, and remote industrial sites all depend on satcom terminals for mission-critical connectivity where terrestrial networks cannot reach.

The satcom terminal market spans multiple frequency bands, including C, X, S, Ku, and Ka band systems, each serving distinct operational needs. Ku band terminals lead commercial deployments for broadband services, while X band terminals serve defense-grade applications. This frequency diversity means that vendors targeting multiple verticals must manage different hardware architectures and regulatory frameworks simultaneously.

Fixed terminals currently anchor the market, holding a 59.2% share, largely because enterprise and government buyers prioritize throughput and stability over portability. However, mobile terminals are gaining ground as military, maritime, and emergency-response buyers demand connectivity on the move. This structural shift is already reshaping product roadmaps across the supply chain.

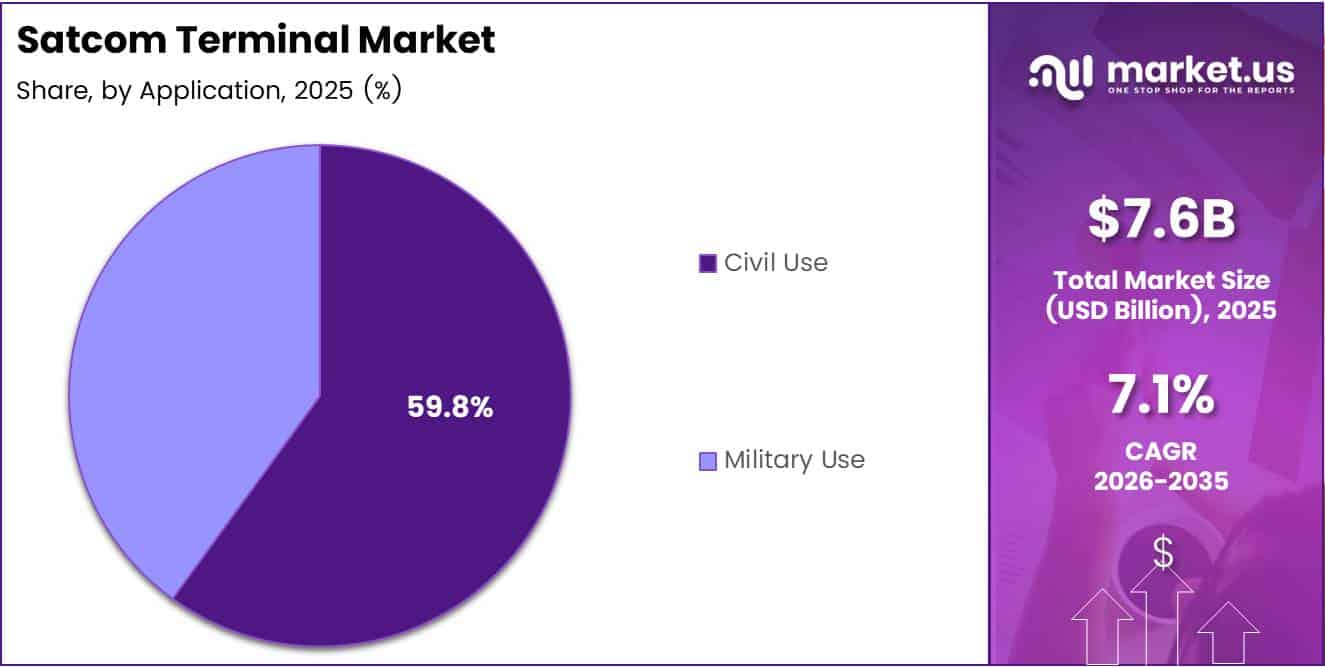

Civil applications account for 59.8% of total demand, driven by commercial aviation, maritime, and enterprise broadband deployments. Military use comprises the remaining share but commands higher per-unit contract values. In April 2025, Trace Systems won a $352 million U.S. Army VSAT IV contract for terminal modernization, illustrating how defense procurement alone can reshape competitive dynamics in a single quarter.

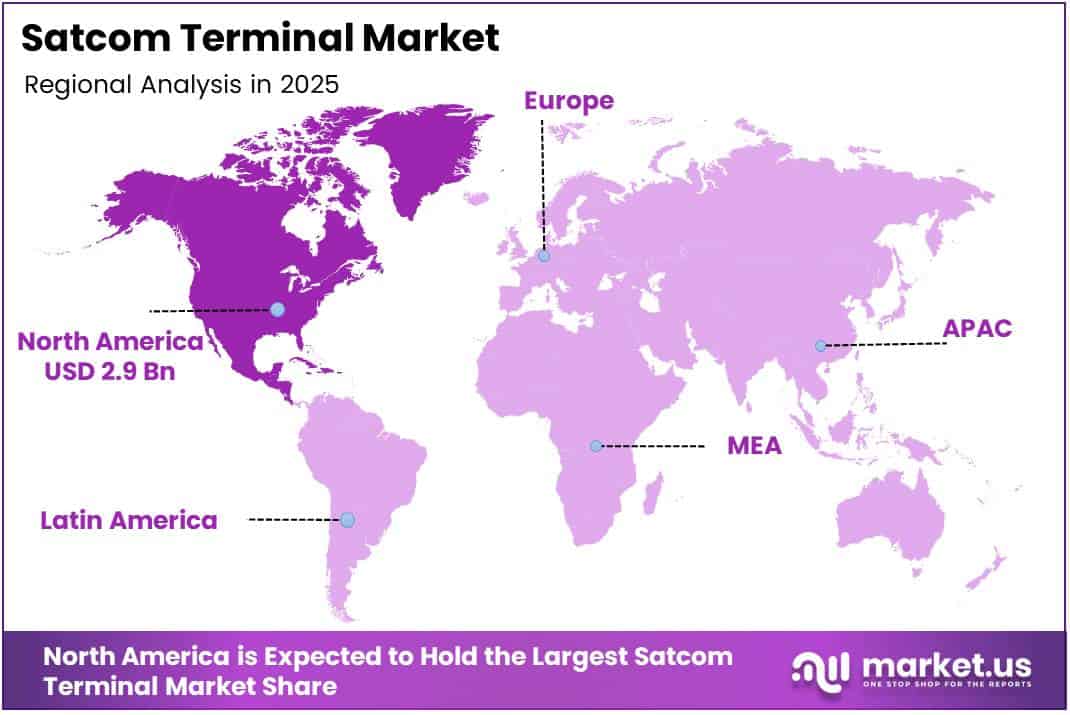

North America leads the global market with a 38.5% share, valued at approximately USD 2.9 billion. This dominance reflects sustained defense spending, mature commercial satellite infrastructure, and early adoption of high-throughput Ka-band networks. The region sets procurement standards that other markets often replicate with a one-to-two-year lag.

According to a 2025 study published in ScienceDirect, a traffic-aware beam-assignment and power-allocation scheme for LEO satellite communications selectively switches off satellites and beams while meeting user traffic demands, reducing total constellation power consumption versus always-on approaches. This finding signals that energy efficiency is becoming an engineering priority, which will influence next-generation terminal design requirements and procurement specifications for both civil and defense buyers.

The doubling of market value over the forecast decade — from USD 7.6 billion to USD 15.2 billion — reflects sustained capital commitment from both government and commercial operators. Multi-orbit satellite expansion, electronically steered antenna adoption, and software-defined platform upgrades each create distinct hardware replacement cycles, giving terminal vendors multiple parallel revenue opportunities through 2035.

Key Takeaways

- The global Satcom Terminal Market is valued at USD 7.6 Billion in 2025 and is forecast to reach USD 15.2 Billion by 2035.

- The market advances at a CAGR of 7.1% during the forecast period 2026 to 2035.

- By Type, Ku Band terminals hold the leading share at 43.6% of the market.

- By Terminal Type, Fixed terminals dominate with a 59.2% share due to higher throughput requirements.

- By Application, Civil Use leads with a 59.8% share across aviation, maritime, and enterprise deployments.

- North America holds the largest regional share at 38.5%, valued at approximately USD 2.9 Billion.

- Key players include Hughes Network Systems, Viasat, Inmarsat, Thales Group, SES S.A., Intelsat, Iridium Communications, and Comtech Telecommunications Corp.

Type Analysis

Ku Band dominates with 43.6% due to mature commercial broadband infrastructure.

In 2025, Ku Band held a dominant market position in the By Type segment of the Satcom Terminal Market, with a 43.6% share. This frequency band’s dominance reflects decades of commercial satellite infrastructure built around Ku, making it the path of least resistance for maritime, aviation, and enterprise broadband buyers seeking proven, cost-effective connectivity solutions.

Ka Band carries the highest throughput capacity within the frequency band segment. Ka-band terminals enable high-speed data transfer at lower cost-per-bit than Ku, making them the preferred choice for high-demand applications such as in-flight broadband and high-density maritime routes. However, rain-fade sensitivity limits deployment in tropical and high-precipitation regions.

C Band serves as the entry point for large-aperture, long-range communication links. Its lower frequency enables stronger signal penetration and resistance to atmospheric interference, making it indispensable for broadcast, government, and remote-location applications where link reliability outweighs bandwidth considerations.

X Band differentiates through its exclusive positioning as the primary frequency for military and government satellite communication. Defense agencies rely on X band terminals because dedicated military satellites in this band provide interference-resilient, secure channels unavailable on commercial frequency allocations.

S Band serves niche roles in weather monitoring, mobile satellite services, and LEO constellation communications. Its relatively narrow commercial market limits terminal volumes, but growing LEO deployments are expanding S-band terminal demand as new satellite operators build out multi-service constellations.

Terminal Type Analysis

Fixed terminals dominate with 59.2% due to enterprise and government throughput requirements.

In 2025, Fixed terminals held a dominant market position in the By Terminal Type segment of the Satcom Terminal Market, with a 59.2% share. Enterprise buyers, utility operators, and government facilities prioritize fixed installations because stationary dishes deliver higher sustained throughput and more predictable link budgets than mobile alternatives — a fundamental engineering advantage that buyer procurement criteria consistently reward.

Mobile terminals differentiate through their ability to maintain satellite links while in motion. Defense forces, maritime vessels, and aviation platforms require SATCOM-on-the-move capability that fixed installations cannot provide. In April 2025, Orbit Communication Systems showcased its MPT30Ka and MPT46Ka rapid-deployable terminals for unmanned surface vessels and special operations forces, reflecting how military buyers are actively driving mobile terminal innovation toward smaller form factors and faster deployment cycles.

Application Analysis

Civil Use dominates with 59.8% due to commercial aviation, maritime, and enterprise broadband scale.

In 2025, Civil Use held a dominant market position in the By Application segment of the Satcom Terminal Market, with a 59.8% share. Commercial aviation connectivity, maritime vessel tracking, enterprise remote-site broadband, and disaster-response networks collectively generate a broader and more geographically distributed demand base than defense channels, driving this segment’s majority position.

Military Use represents the remaining share but consistently commands the highest per-unit contract values and longest procurement timelines in the market. Defense buyers demand ruggedized hardware, secure frequency operations, and multi-orbit compatibility. These requirements push military terminal development costs well above commercial equivalents, which is why even a minority application share generates disproportionate revenue and margin for specialized vendors.

Key Market Segments

By Type

- C Band

- X Band

- S Band

- Ku Band

- Ka Band

By Terminal Type

- Fixed

- Mobile

By Application

- Civil Use

- Military Use

Drivers

Defense Procurement and Broadband Connectivity Mandates Accelerate Satcom Terminal Demand

Defense agencies and maritime operators require satellite communication terminals that function where terrestrial networks fail entirely. Military forces depend on secure, jam-resistant links for command and control, while naval vessels need broadband at sea for both operational and crew welfare purposes. These requirements produce sustained, non-discretionary procurement cycles that stabilize terminal demand regardless of broader economic conditions.

According to a 2025 IJSRA study, deploying VSAT links enabled connectivity for 10 remote utility sites within 72 hours of a disruptive event and maintained more than 99% link availability, contributing to an estimated 30–40% reduction in power-outage duration compared with historical performance without satellite backup. This measurable operational improvement demonstrates why utility operators and emergency managers increasingly specify satellite communication terminals as mandatory infrastructure rather than optional backup.

Broadband satellite network expansion compounds this demand by creating new addressable markets for terminal vendors. Aviation connectivity mandates, maritime regulatory requirements, and enterprise remote-site broadband programs each generate large-volume terminal procurement programs. In March 2024, L3Harris received a $60 million U.S. Army contract to deliver Hawkeye III Lite VSAT SATCOM terminals, illustrating how a single defense program can represent a meaningful share of annual terminal revenue for a leading vendor.

Restraints

High Terminal Costs and Integration Complexity Constrain Adoption Among Budget-Sensitive Buyers

Advanced satcom terminals carry substantial upfront hardware and installation costs that create a genuine barrier for smaller operators, emerging-economy buyers, and cost-constrained government agencies. High-throughput Ka-band terminals, electronically steered antennas, and ruggedized military units each carry price points that require multi-year budget justifications before procurement decisions can move forward.

According to the IJSRA 2025 smart-grid study, Ku-band VSAT TDMA links operating at 128 kbps across 15 remote substations recorded round-trip latency of 600–750 ms. While the study also found the satellite solution delivered approximately 65% lower total cost than microwave alternatives, the latency figure highlights a technical limitation that constrains satcom terminal adoption in latency-sensitive applications such as real-time industrial control and financial transaction processing.

Integration with existing communication infrastructure adds further friction. Organizations operating legacy terrestrial networks, proprietary SCADA systems, or multi-vendor communication stacks face significant engineering effort to incorporate satellite terminals without disrupting current operations. This complexity extends procurement timelines and increases total deployment cost beyond the terminal hardware price, particularly for mid-sized industrial and utility buyers.

Growth Factors

Portable Terminal Demand, Remote Industrial Connectivity, and Emerging Economy Expansion Create New Revenue Channels

Portable and compact satcom terminals open markets that fixed installations cannot address. Field operations, humanitarian missions, and rapid-deployment defense units require terminals light enough for individual carry yet capable enough to sustain broadband links. This form factor shift forces vendors to develop new product lines, creating replacement cycle revenue distinct from traditional fixed-terminal procurement.

Remote industrial operations — oil and gas, mining, and utility infrastructure — represent a structurally underserved segment where terrestrial connectivity is unavailable and operational downtime is commercially costly. According to the IJSRA 2025 study, a satellite VSAT solution delivered approximately 65% lower total cost than a comparable microwave deployment while sustaining utility SCADA operations across remote substations. This cost advantage makes satellite terminals the economically rational choice for remote industrial buyers, not just a technical fallback.

Emerging economies present a parallel expansion channel. In July 2025, Get SAT and Rangsons secured a multi-million-dollar contract to deliver over 100 Micro SAT compact mobile SATCOM-on-the-move terminals for a defense program in South Asia, integrated with India’s ISRO satellite constellation under the Make in India initiative. This transaction signals that emerging-market defense modernization programs are becoming material revenue sources for terminal vendors — a trend that will intensify as regional space programs expand satellite coverage.

Emerging Trends

Electronically Steered Antennas, Software-Defined Platforms, and Multi-Orbit Terminals Redefine the Satcom Terminal Product Architecture

Electronically steered antenna technology eliminates mechanical dish movement, enabling faster beam acquisition, lower profile hardware, and reliable operation on moving platforms. This capability directly addresses the mobility requirements of aviation, maritime, and ground-vehicle applications. Vendors that commercialize electronically steered antennas at competitive price points gain access to mobile terminal segments currently constrained by mechanical antenna limitations.

Software-defined satellite communication systems allow operators to update terminal parameters, frequency plans, and waveform configurations remotely — without hardware replacement. In February 2025, Comtech unveiled ELEVATE 2.0, a software-defined multi-orbit VSAT platform offering low SWaP terminals with real-time upgrade capability. This approach shifts terminal value from hardware specification to software flexibility, changing how buyers evaluate and compare competing terminal solutions.

Multi-orbit terminal solutions that operate across LEO, MEO, and GEO constellations simultaneously give operators resilience and latency options unavailable from single-orbit hardware. Flat panel antenna designs further enable this capability by supporting multiple simultaneous satellite links in a compact form. Together, these developments reposition satcom terminals from single-purpose hardware into programmable connectivity platforms — a shift that expands terminal addressable markets and raises the competitive stakes for vendors unable to support multi-orbit architectures.

Regional Analysis

North America Dominates the Satcom Terminal Market with a Market Share of 38.5%, Valued at USD 2.9 Billion

North America holds a 38.5% share of the global satcom terminal market, valued at USD 2.9 billion. This position reflects sustained U.S. defense satellite communication spending, mature commercial broadband satellite infrastructure, and early enterprise adoption of high-throughput Ka-band networks. Procurement programs at the U.S. Army, Navy, and Air Force alone generate multi-hundred-million-dollar terminal contract flows each year.

Europe Satcom Terminal Market Trends

Europe maintains a significant satcom terminal position driven by NATO defense interoperability requirements, offshore maritime broadband mandates, and government-backed satellite broadband programs targeting rural connectivity gaps. European defense agencies increasingly specify multi-orbit terminal compatibility to align with allied force requirements, which is accelerating procurement of next-generation terminal hardware across the region.

Asia Pacific Satcom Terminal Market Trends

Asia Pacific represents the fastest-expanding regional market, driven by defense modernization across India, Australia, Japan, and South Korea, alongside large-scale commercial maritime and aviation connectivity deployments. National satellite programs — particularly India’s ISRO-backed initiatives — are creating localized terminal supply chains and procurement ecosystems that reduce dependence on Western hardware suppliers.

Middle East and Africa Satcom Terminal Market Trends

Middle East and Africa demand for satcom terminals centers on military and government applications, where terrestrial infrastructure remains limited across large geographic areas. Gulf Cooperation Council defense programs and African utility and humanitarian organizations drive terminal procurement, with portable and rapid-deployable solutions carrying particular relevance for disaster-response and remote-site connectivity use cases.

Latin America Satcom Terminal Market Trends

Latin America’s satcom terminal market develops around remote industrial connectivity in oil and gas, mining, and agricultural sectors, where terrestrial broadband is absent. Brazil and Mexico lead regional adoption, supported by national satellite programs and growing enterprise demand for reliable connectivity across inland and offshore operations where terrestrial infrastructure cannot be deployed economically.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

Hughes Network Systems anchors its competitive position in high-throughput Ka-band broadband, serving enterprise, government, and consumer segments across the Americas and internationally. Its deep integration with EchoStar’s satellite fleet creates a vertically aligned supply chain that competitors relying on third-party satellite capacity cannot easily replicate. This vertical structure gives Hughes a structural cost advantage in high-volume commercial broadband terminal deployments.

Viasat differentiates through its simultaneous operation as a satellite operator and terminal manufacturer, allowing it to optimize terminal hardware specifically for its own high-throughput satellite fleet. This dual-role positioning enables Viasat to deliver end-to-end service level agreements that pure terminal vendors cannot offer. Its expansion into in-flight connectivity and defense communication terminals positions it across both the highest-margin commercial and government segments.

Inmarsat builds its competitive advantage around global maritime and aviation L-band and Ka-band coverage, serving sectors where connectivity gaps represent regulatory compliance risks rather than just operational inconvenience. Maritime operators in particular rely on Inmarsat’s Fleet Xpress platform for GMDSS safety communication requirements. This regulatory dependency creates a captive installation base that generates recurring terminal upgrade and service revenue independent of market pricing pressure.

Thales Group targets the defense and government satcom terminal segment with a portfolio of ruggedized, multi-band, and cyber-hardened communication systems. Its strategic value comes from deep integration with NATO and European defense procurement channels, where security certification requirements effectively exclude commercially-oriented terminal suppliers. Thales’s position as both a systems integrator and terminal manufacturer gives it influence over program specifications that shapes competitive terms for other vendors.

Key Players

- Hughes Network Systems

- Viasat

- Inmarsat

- Thales Group

- SES S.A.

- Intelsat

- Iridium Communications

- Comtech Telecommunications Corp.

Recent Developments

- July/August 2025 — ALL.SPACE announced the Hydra MAX, described as the world’s first dual-beam, full-duplex 500MHz Ka-band terminal supporting multi-orbit operations. The system incorporates military-grade ruggedness, targeting defense and government operators requiring simultaneous multi-orbit satellite access.

- October 2025 — Gilat DataPath received over $7 million in orders to supply DKET 3421 transportable SATCOM terminals and associated support services to the U.S. DoD and U.S. Army. The award reflects continued U.S. military investment in rapidly deployable satellite ground terminal infrastructure.

- October 2025 — L3Harris completed the Critical Design Review for the U.S. Army’s Large Wideband Satellite Communications Terminal (LWST) program. Completion clears the path for 2025 testing and integration into the Wideband Global SATCOM (WGS) network.

- April 2025 — Trace Systems was awarded a $352 million U.S. Army contract under the VSAT IV program. The award covers modernization and maintenance of SNAP terminals and related communication technologies across Army installations.

Report Scope

Report Features Description Market Value (2025) USD 7.6 Billion Forecast Revenue (2035) USD 15.2 Billion CAGR (2026-2035) 7.1% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Type (C Band, X Band, S Band, Ku Band, Ka Band), By Terminal Type (Fixed, Mobile), By Application (Civil Use, Military Use) Regional Analysis North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) Competitive Landscape Hughes Network Systems, Viasat, Inmarsat, Thales Group, SES S.A., Intelsat, Iridium Communications, Comtech Telecommunications Corp. Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)

-

-

- Hughes Network Systems

- Viasat

- Inmarsat

- Thales Group

- SES S.A.

- Intelsat

- Iridium Communications

- Comtech Telecommunications Corp.

Our Clients

- 183663

- Apr 2026