Quick Navigation

Report Overview

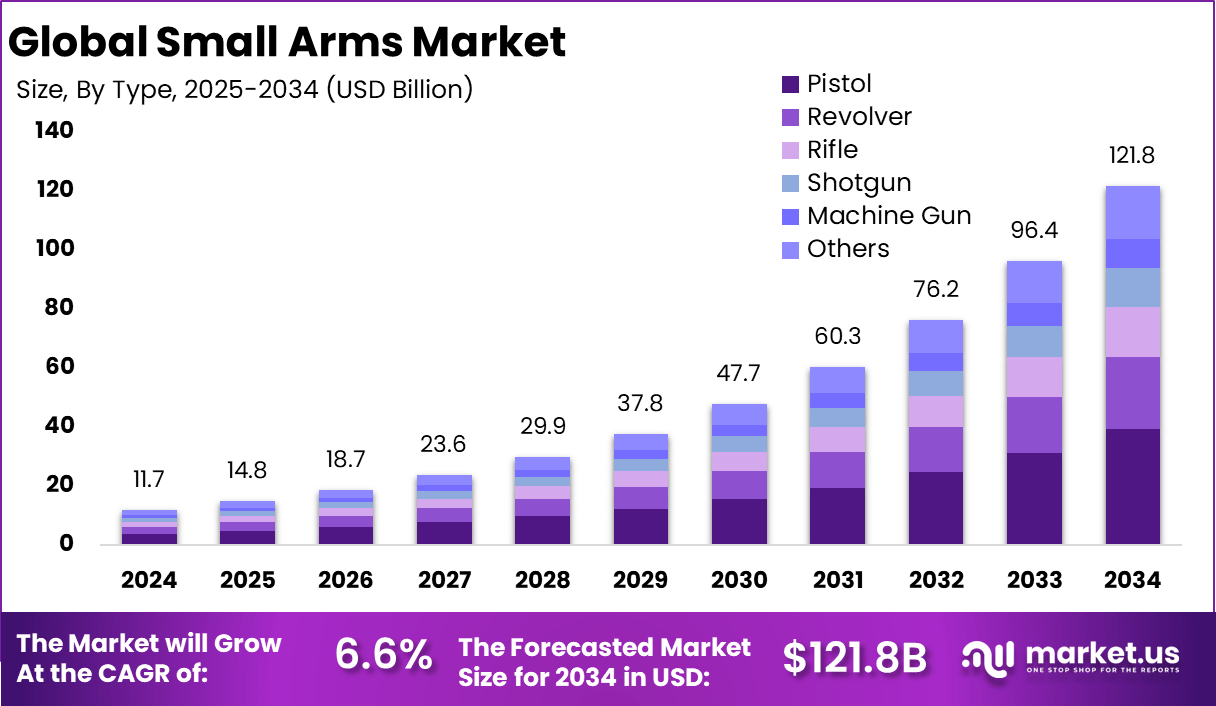

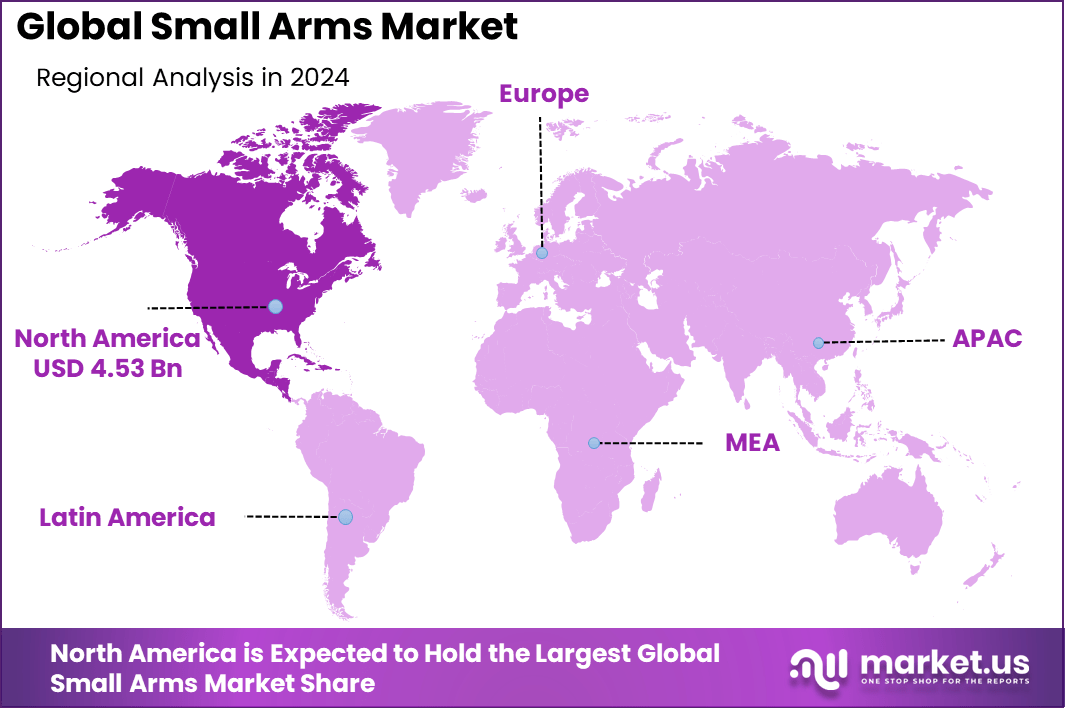

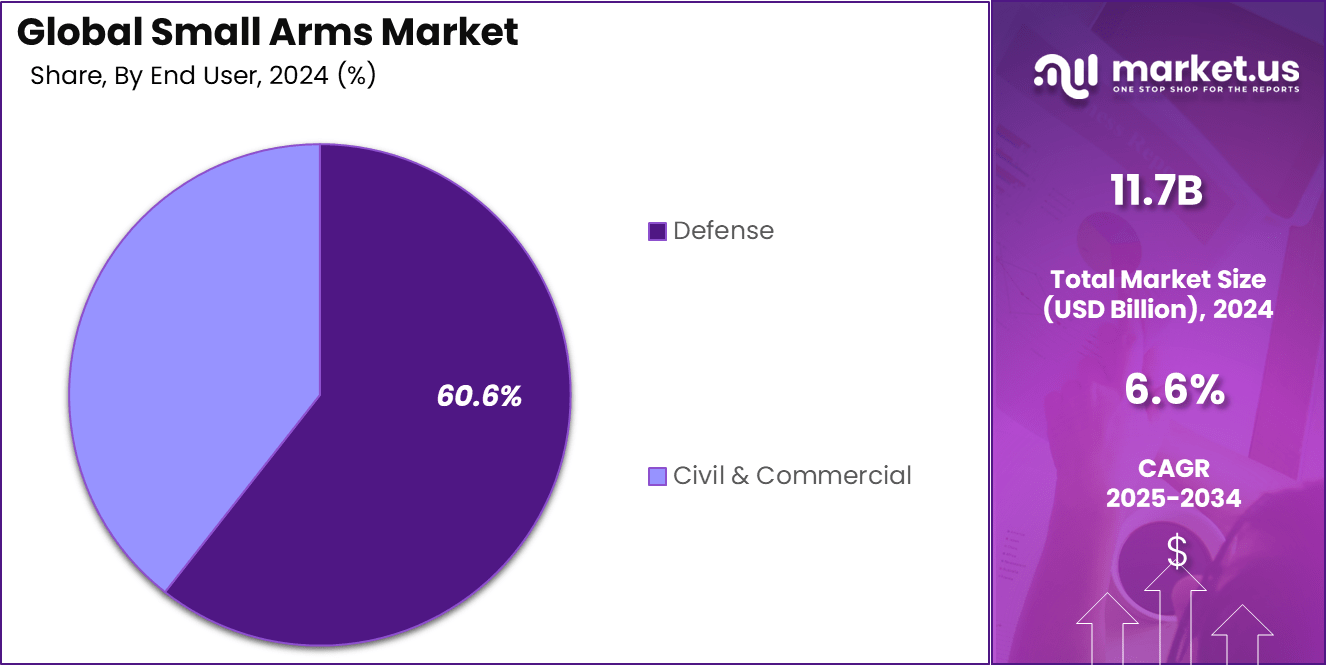

The Global Small Arms Market size is expected to be worth around USD 121.8 Billion By 2034, from USD 11.7 billion in 2024, growing at a CAGR of 6.6% during the forecast period from 2025 to 2034. In 2024, North America held a dominant market position, capturing more than a 38.2% share, holding USD 4.4 Billion revenue.

Small arms are lightweight, portable firearms designed for individual use. They include handguns like pistols and revolvers, as well as rifles, carbines, shotguns, and submachine guns. These weapons are commonly used by military personnel, law enforcement agencies, and civilians for purposes ranging from defense and law enforcement to hunting and sport shooting.

The global small arms market is experiencing steady growth, driven by various factors. Several key factors are propelling the expansion of the small arms market. Heightened geopolitical tensions and the ongoing modernization of military forces have led to increased procurement of advanced firearms. Simultaneously, the rise in civilian firearm ownership for personal defense and recreational purposes contributes significantly to market demand.

For instance, in November 2024, Sig Sauer partnered with India’s Nibe Group to manufacture advanced firearms domestically, supporting India’s military modernization and “Make in India” initiative. This collaboration aims to produce complete firearms for the Indian Ministry of Defence and Ministry of Home Affairs by 2025, reflecting rising defense spending and the push for locally produced, high-tech small arms.

Analyzing demand trends reveals a robust interest across various end-users. Military and law enforcement agencies are investing in modern, efficient weaponry to enhance operational capabilities. In the civilian sector, factors like increasing crime rates and a growing emphasis on personal safety have led to a surge in firearm purchases.

The adoption of emerging technologies is reshaping the small arms landscape. Innovations such as modular weapon systems, improved optics, and integration with digital technologies are enhancing firearm performance and user experience. These advancements not only improve accuracy and reliability but also offer customization options to meet specific operational requirements.

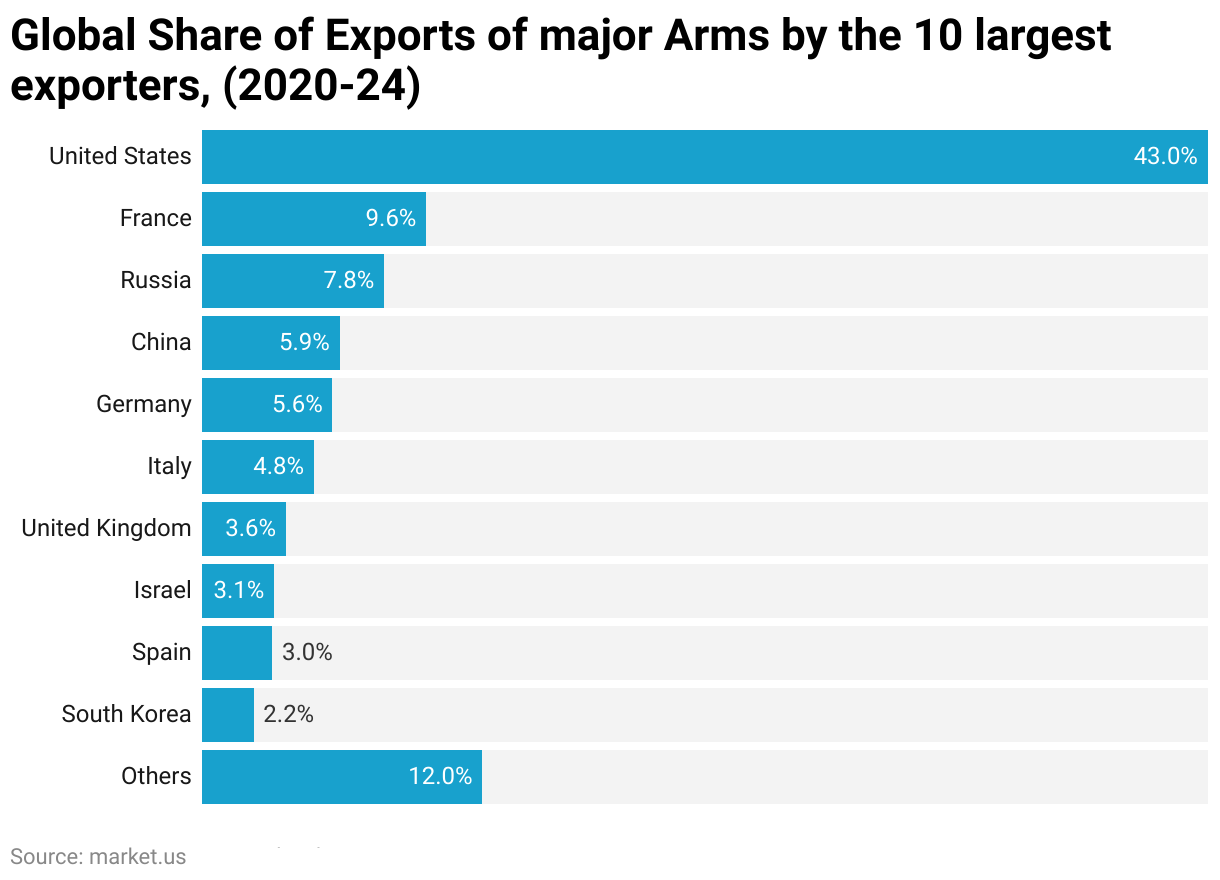

According to the Stockholm International Peace Research Institute (SIPRI), from 2020 to 2024, the United States solidified its position as the world’s leading arms exporter, accounting for 43% of global arms exports. This marks a significant increase from the 35% share recorded in the previous five-year period.

Key Takeaways

- The global small arms market is set to grow from USD 11.7 billion in 2024 to around USD 121.8 billion by 2034, registering a CAGR of 6.6%.

- North America is leading the global market in 2024 with a 38.2% share, contributing around USD 4.4 billion in revenue.

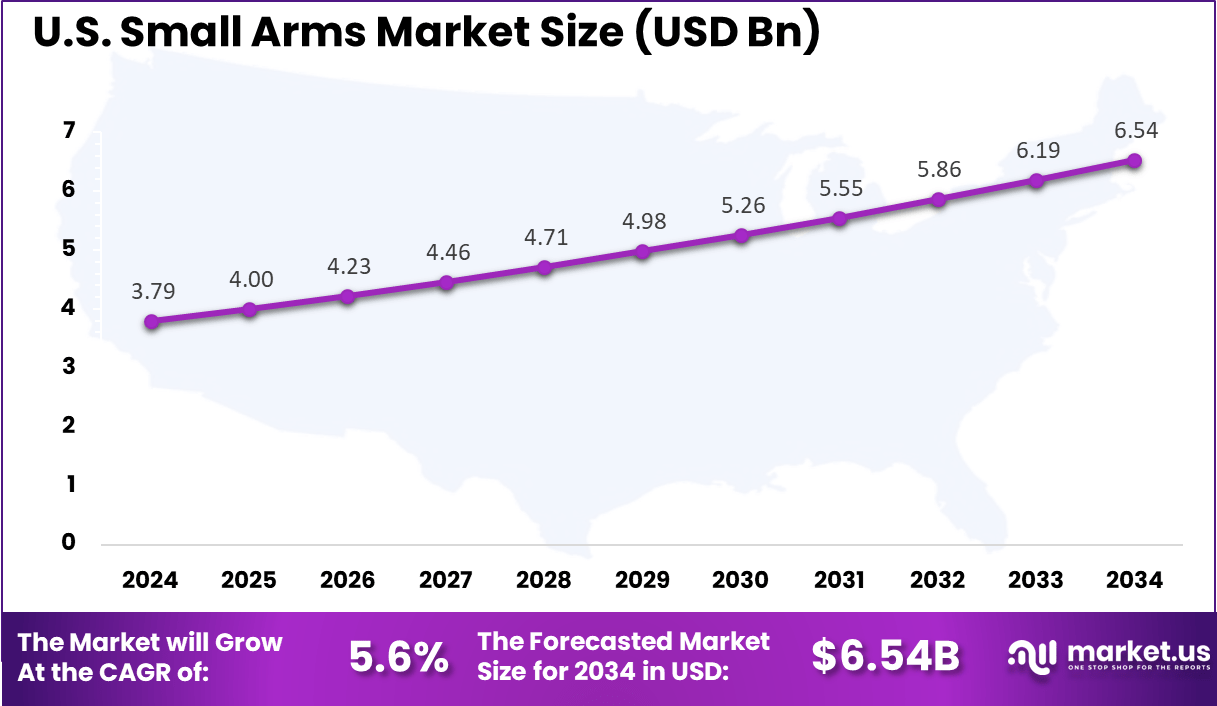

- The United States alone generated USD 3.79 billion in 2024, growing steadily at a 5.6% CAGR through the forecast period.

- Among product types, pistols are the most demanded, accounting for a significant 32.2% market share.

- In terms of operational preference, automatic small arms dominate, making up 55.8% of the total demand.

- The defense sector is the primary end user, representing a commanding 60.6% share in 2024.

Analysts’ Viewpoint

Investment opportunities in the small arms market are large, particularly in regions experiencing increased defense spending and civilian interest in firearms. Companies focusing on research and development of innovative technologies are well-positioned to capitalize on this growth. Emerging markets in Asia and the Middle East present significant potential due to their expanding defense budgets and evolving security needs.

Businesses operating in this sector can reap several benefits, including access to a growing customer base and the ability to diversify product offerings. By investing in cutting-edge technologies and responding to market trends, companies can enhance their competitiveness and establish a strong presence in both traditional and emerging markets.

The regulatory environment plays a crucial role in shaping the small arms market. Stringent laws and export controls can impact manufacturing and distribution, while changes in regulations may influence consumer behavior. Manufacturers must navigate complex legal frameworks to ensure compliance and maintain market access.

US Market Expansion

The market for Small Arms within the U.S. is growing tremendously and is currently valued at USD 3.79 billion. And the market has a projected CAGR of 5.6%. The market for small arms within the U.S. is growing tremendously due to a combination of factors, including heightened concerns over personal safety, a robust firearms culture, and increasing participation in recreational shooting and sporting activities.

Civilian demand for self-defense remains a primary driver, further fueled by rising disposable incomes and the expanding popularity of shooting sports. In addition to the relatively relaxed regulatory environment compared to other countries, the continuous innovation of the product and the simplicity of gun sales on the Internet also contribute to the expansion of the market.

For instance, In January 2025, the U.S. Army allocated a record budget for the Next Generation Squad Weapon (NGSW) program, underscoring its commitment to modernizing infantry capabilities. The budget includes $23.1 million for 1,772 units of the XM250 Automatic Rifle, $91.4 million for 18,019 units of the XM7 Rifle, and $252.7 million for 20,045 XM157 Fire Control Systems.

These investments aim to replace legacy systems like the M249 and M4, enhancing range, accuracy, and lethality with advanced features such as integrated fire control systems and reduced muzzle flash. The program is currently in the developmental and procurement stages, with increased production planned to meet deployment timelines.

North America Growth

In 2024, North America held a dominant market position in the global Small Arms Market, capturing more than a 38.2% share, holding USD 4.53 Billion in revenue. North America holds a dominant position in the small arms market due to its high defense spending, wide range of ownership of private firearms, and the constant modernization of military and law enforcement arsenals.

The United States continues to invest heavily in advanced small arms technology, fueled by a strong gun culture, steady demand for personal defense, and the popularity of shooting sports. Law enforcement agencies are actively modernizing their gear to tackle changing security threats.

Combined with the presence of top manufacturers and constant innovation, these factors firmly establish North America as a global leader in the small arms market. In April 2025, Taurus Armas, a leading Brazilian firearms maker, emphasized the value of its U.S. factory amid new U.S. tariffs on Brazilian exports.

CEO Salesio Nuhs stated that the U.S. facility produces 3,000 weapons daily, supporting Brazil’s 7,000 daily output – 85% of which are exported to the U.S. This highlights North America’s leading role in the small arms market, driven by strong domestic demand and high defense expenditure.

Type Analysis

In 2025, the pistol segment stood out prominently in the global small arms market, securing a commanding 32.2% share. This leadership stems from the pistol’s practical advantages – compactness, ease of handling, and effectiveness in close-range defense. Its broad appeal spans across civilians, law enforcement, and military users, making it one of the most versatile and in-demand weapon types.

In cities where crime rates and security concerns are rising, particularly in regions with less restrictive firearm regulations, civilian adoption of pistols has seen a notable increase. The segment’s steady momentum is further fueled by technological refinements like modular designs, ergonomic enhancements, and advanced safety features, which elevate both user confidence and functionality.

In a clear testament to this trend, May 2025 marked a notable wave of product innovation in the handgun market. Leading firearm makers rolled out next-generation models tailored for everyday use and performance shooting. Kahr’s introduction of the X9 Carry Comp exemplifies this shift. This micro-compact pistol includes a ported barrel to reduce recoil and supports interchangeable magazines compatible with widely-used models like the SIG P365 and Springfield Hellcat.

Mode of Operation Analysis

In 2025, the automatic segment dominated the global small arms market, capturing a commanding 55.8% share. This leadership is driven by the essential role automatic firearms play in military and law enforcement operations. Their rapid-fire capabilities make them critical for suppressive fire, quick threat response, and modern tactical engagement, especially in high-intensity environments.

As global defense strategies evolve, there’s been a noticeable surge in military modernization and increased defense budgets across NATO and allied countries. Automatic weapons, such as light machine guns and assault rifles, are at the core of this transition, making them indispensable assets on the battlefield.

The demand for advanced automatic firearms is also being shaped by breakthroughs in robotics, artificial intelligence, and modular weapons systems. These technologies are expanding the role of automatic arms beyond traditional use, opening doors to their integration in unmanned combat systems and next-generation battlefield automation. This shift is not only about firepower but about enhancing precision, efficiency, and adaptability in complex scenarios.

A compelling example came in April 2025, when FN Herstal – a renowned Belgian firearms manufacturer – noted a sharp rise in production of its FN Minimi light machine guns, increasing annual output from 3,000 to 4,500 units. This was largely driven by urgent demand from NATO and European countries amid the continuing conflict in Ukraine.

Interestingly, even with the incorporation of robotics in manufacturing, FN Herstal continues to rely on skilled craftsmanship for key components, highlighting the intricate precision required in producing reliable automatic weapons. The company is also exploring 3D printing technologies to support potential mass production of its ultralight FN Evolys machine gun – pending long-term procurement contracts.

End-user Analysis

In 2025, the defense segment led the global small arms market with a commanding 60.6% share, highlighting the critical role of military demand in driving industry growth. This dominance is closely tied to a global rise in defense budgets, ongoing geopolitical instability, and an urgent push for military modernization across key regions.

Nations facing persistent threats from terrorism, insurgency, and border conflicts are prioritizing the acquisition of next-generation small arms to bolster national security and maintain technological parity with adversaries. These investments are not just about quantity – they reflect a strategic shift toward precision, adaptability, and battlefield efficiency.

A strong example of this trend came in April 2025, when the Indian government moved to strengthen its domestic defense manufacturing capabilities. The Ministry of Science and Technology, through the Technology Development Board (TDB), provided financial backing to M/s dvipa Defence India Pvt. Ltd., Hyderabad, for the development and commercialization of the 7.62 mm x 51 mm UGRAM assault rifle.

This weapon is being tailored to meet the Indian Army’s General Staff Qualitative Requirements (GSQR), ensuring it meets stringent operational standards. This initiative is part of a broader effort to reduce import dependency, stimulate local defense innovation, and equip military personnel with cutting-edge, homegrown technology. As more nations adopt similar policies, the defense segment is set to remain a dominant force in the small arms market, fueled by both strategic necessity and national pride.

Key Market Segments

By Type

- Pistol

- Revolver

- Rifles

- Shotgun

- Machine Gun

- Others

By Mode of Operation

- Semi-automatic

- Automatic

By End-user

- Defense

- Military

- Law Enforcement

- Civil & Commercial

- Sporting

- Hunting

- Self-defense

- Others

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherlands

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Thailand

- Vietnam

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Driver

Rising Defense Spending and Military Modernization

Rising global tensions and growing security threats are pushing countries to boost their defense spending and modernize their armed forces. Across the world, military and law enforcement agencies are phasing out outdated weaponry in favor of more advanced small arms.

These newer firearms are designed to be lighter, more accurate, and easier to operate, often equipped with smart technology to enhance battlefield performance. This wave of modernization reflects a broader shift in defense strategy, with governments prioritizing the acquisition of high-performance and future-ready equipment.

Leading defense spenders like the United States, China, and India are at the forefront of this transformation, while even smaller nations are stepping up their investments to strengthen national security. The focus is not just on buying weapons, but on building technological capability and reducing dependence on foreign imports.

For instance, In February 2025, India announced a 9.53% hike in its defense budget, bringing the total to $78.3 billion. A large portion of this increase is aimed at modernizing the country’s armed forces, particularly through the procurement of next-generation small arms and ammunition. In a strong move toward self-reliance, 75% of the modernization budget has been allocated to domestic defense production.

Restraint

Stringent Regulations

Stringent government regulations remain a significant barrier for companies operating in the small arms industry. From manufacturing to sales and exports, firms must navigate complex legal frameworks that differ across borders. Governments impose these rules to reduce gun violence, prevent illegal weapon use, and protect national security.

However, for businesses, the process of obtaining licenses, meeting compliance standards, and managing long approval timelines can be slow, costly, and often unpredictable. These hurdles make it particularly challenging for manufacturers to expand internationally, as adapting to each country’s unique regulatory landscape requires substantial legal and operational effort.

For instance, in April 2024, the United States government introduced stricter export controls on small arms under the Biden administration. These measures were aimed at preventing U.S.-manufactured firearms from reaching unauthorized users and regions prone to conflict.

The new policy placed restrictions on exports to 36 countries considered high-risk for diversion, particularly limiting sales to non-governmental buyers. As a direct impact, analysts projected a potential decline of up to $40 million annually in firearms exports. Such regulatory changes, often driven by political or security concerns, can quickly shift market dynamics and force companies to adjust their strategies.

Opportunity

Technological Integration

Technology is rapidly reshaping how small arms are designed, produced, and used. Innovations such as biometric sensors, smart locks, and advanced aiming systems are making firearms safer, more accurate, and easier to handle.

These smart features are increasingly appealing not only to military and law enforcement but also to private security firms and civilian buyers who prioritize control and reliability. Such enhancements reduce accidental discharges and restrict unauthorized use, aligning safety with performance.

For companies, this opens up a strong opportunity to lead with innovation and differentiate their products in a competitive market. A prime example is from May 2025, when AimLock, a U.S.-based firm specializing in precision firearms, shifted focus towards autonomous counter-drone systems. At SOF Week 2025, CEO Bryan Bockmon stressed the importance of kinetic defense tools, especially in scenarios where electronic jamming fails.

Challenge

Illicit Trade and Black Market

One of the biggest problems in the small arms market is illegal transactions. Many weapons find themselves in the hands of criminals, gangs, or armed forces in the black market. This harms the legal company and damages the public’s trust. It also leads to violence and conflict in many regions.

The government is trying to stop illegal weapons transactions with more stringent laws and tracking systems, but the black market is still flourishing. Legal manufacturers and sellers have problems in ensuring the safety of suppliers and reputation chains. The fight against illegal trade is expensive and in progress, so it is a major obstacle to the industry.

For instance, in May 2025, a joint operation by the Border Security Force (BSF) and Amritsar Police successfully thwarted a significant cross-border smuggling attempt in Punjab. Utilizing a drone, smugglers attempted to transport arms and ammunition across the India-Pakistan border. Authorities recovered the drone along with the illicit cache near the border area.

Emerging Trends

The small arms industry is witnessing several emerging trends that are shaping its future. One notable trend is the integration of smart technologies into firearms, enhancing their functionality and appeal to modern consumers. Moreover, the use of lightweight materials and modular designs is becoming increasingly prevalent, allowing for greater customization and ease of use.

Another significant development is the growing emphasis on sustainable and energy-efficient manufacturing processes. Companies are focusing on reducing their environmental footprint by adopting eco-friendly practices in the production of small arms.

Business Benefits

The expansion of the small arms market offers several business benefits. Firstly, it creates numerous employment opportunities across various sectors, including manufacturing, distribution, and retail. This job creation contributes to economic growth and stability in regions where the industry is prominent.

Secondly, the industry’s growth stimulates innovation and technological advancement. Companies are investing in research and development to produce more advanced and efficient firearms, which can lead to increased competitiveness and profitability.

Key Player Analysis

The global small arms market includes well-established manufacturers known for their innovation and defense collaborations. Colt’s Manufacturing LLC, a legacy U.S. brand, continues to support law enforcement and military sectors globally with precision-grade rifles.

Sig Sauer remains a dominant player due to its diverse firearm lineup and contracts with the U.S. Army. Steyr Arms, based in Austria, is gaining momentum through export expansion and modular rifle platforms. These players focus heavily on product reliability and modernization to stay competitive in global tenders.

Remington Outdoor Company and Smith & Wesson play crucial roles in the North American market. Remington, despite past restructuring, maintains a strong presence in hunting and sporting rifles. Smith & Wesson has diversified into tactical weaponry, targeting both civilian and professional sectors.

Daniel Defense Inc. is noted for high-quality, customizable rifles, frequently used by special forces. These companies invest in lightweight materials, ergonomic designs, and improved recoil control to meet rising demand from defense agencies and enthusiasts.

Top Key Players Covered

- Colt’s Manufacturing LLC

- Sig Sauer

- Steyr Arms

- Remington Outdoor Company

- Smith & Wesson

- Daniel Defense Inc.

- Sturm, Ruger & Co., Inc.

- Israel Weapons Industry

- GLOCK Ges.m.b.H.

- Kalashnikov Group

- Èeská Zbrojovka a.s.

- Others

Recent Developments

- In May 2024, Colt CZ Group, the parent company of Colt’s Manufacturing, acquired Sellier & Bellot, a renowned ammunition producer. This strategic move significantly boosted Colt CZ’s revenue, which saw a 41.2% increase in the first half of 2024. The acquisition not only expanded their product portfolio but also strengthened their position in the ammunition market.

- In March 2024, SIG Sauer introduced the MCX-REGULATOR, a modern take on the classic ranch rifle, and the 1911-XSERIES, blending traditional design with contemporary features. These launches demonstrate SIG Sauer’s commitment to innovation and meeting diverse customer needs.

- On April 23, 2024, Czech investment group RSBC acquired 100% of Steyr Arms. This acquisition aims to leverage Steyr’s expertise in long guns for military and law enforcement, as well as hunting and sporting rifles, to expand RSBC’s footprint in the global arms market.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 11.7 Bn |

| Forecast Revenue (2034) | USD 12.8 Bn |

| CAGR (2025-2034) | 6.6% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue forecast, AI impact on market trends, Share Insights, Company ranking, competitive landscape, Recent Developments, Market Dynamics and Emerging Trends |

| Segments Covered | By Type (Pistol, Revolver, Rifles, Shotgun, Machine Gun, Others), By Mode of Operation (Semi-automatic, Automatic), By End-user (Defense (Military, Law Enforcement), Civil & Commercial (Sporting, Hunting, Self-defense, Others)), Leading Region (North America (38.2% Share)) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Colt’s Manufacturing LLC, Sig Sauer, Steyr Arms, Remington Outdoor Company, Smith & Wesson, Daniel Defense Inc., Sturm, Ruger & Co., Inc., Israel Weapons Industry, GLOCK Ges.m.b.H., Kalashnikov Group, Èeská Zbrojovka a.s., Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three license to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |