Quick Navigation

Report Overview

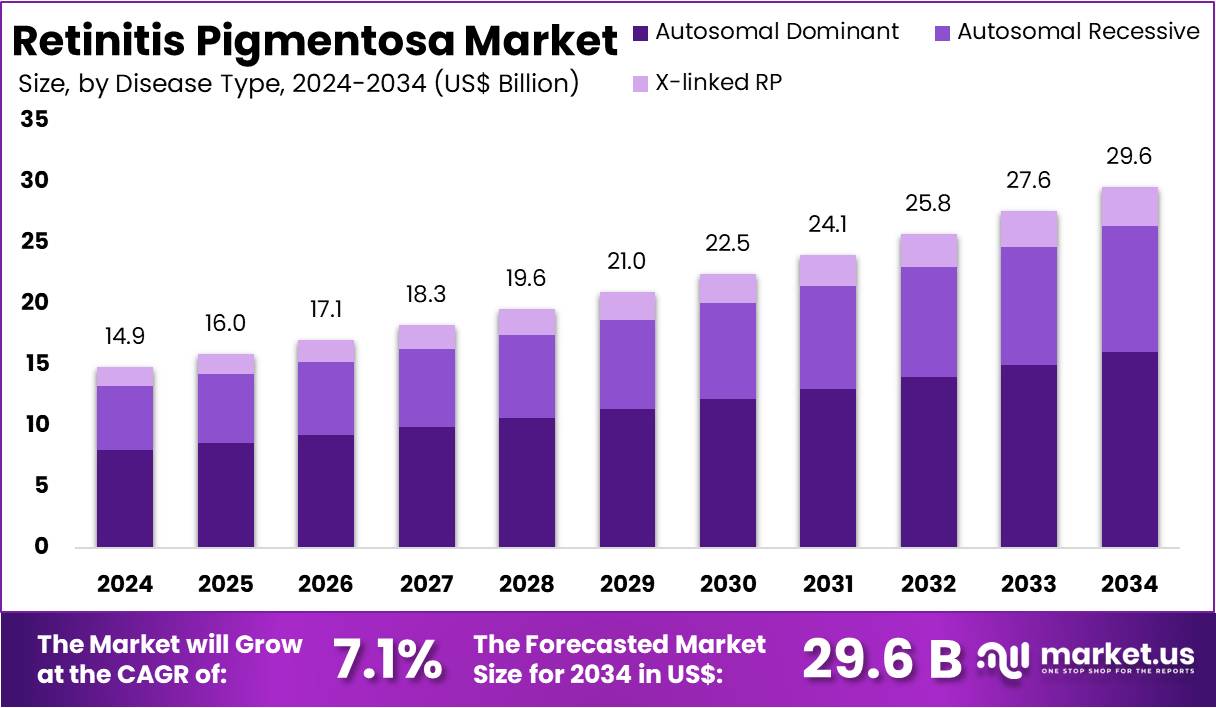

The Global Retinitis Pigmentosa Market Size is expected to be worth around US$ 29.9 Billion by 2034, from US$ 14.9 Billion in 2024, growing at a CAGR of 7.1% during the forecast period from 2025 to 2034.

Retinitis Pigmentosa (RP) refers to a group of inherited eye disorders that result in the gradual loss of vision. These conditions primarily damage the retina, which is the light-sensitive tissue at the back of the eye. Over time, individuals with RP may experience reduced night vision, peripheral vision loss, and eventually, complete blindness.

According to a study by the U.S. National Eye Institute, RP impacts approximately 1 in 4,000 individuals in the United States and around 1 in 5,000 people globally. The prevalence can vary across regions. For instance, studies conducted in India have reported higher rates, ranging between 0.13% and 0.17%. These elevated numbers may be linked to genetic diversity and consanguineous marriages, which increase the risk of hereditary disorders such as RP.

Advancements in genetic research have played a key role in the sector’s growth. More than 50 gene mutations have been identified as contributing factors to RP. This has paved the way for targeted treatments and personalized medicine. For example, voretigene neparvovec, a gene therapy approved by the U.S. FDA, treats patients with a specific mutation linked to RP. Such therapies are expanding treatment options and are contributing to the growth of the RP treatment landscape.

The socioeconomic burden of RP is also significant. Individuals often face high medical costs, including the use of assistive devices and modifications to their living environments. Furthermore, reduced employment opportunities due to vision impairment can lead to lower income. According to global health experts, these financial pressures highlight the need for cost-effective therapies and support services, which are increasingly becoming part of integrated RP care.

RP also severely impacts quality of life. The progressive loss of vision affects daily tasks, mobility, and social engagement. It can lead to psychological stress and a loss of independence. Therefore, there is a growing demand for comprehensive care strategies that include not only medical treatment but also psychological counseling, low vision rehabilitation, and community-based support systems.

Usher syndrome is a well-known condition associated with RP. It affects approximately 18% of all RP patients and is characterized by sensorineural hearing loss and balance issues. According to genetic studies, there are three main types of Usher syndrome, each varying in severity and underlying genetic causes. As awareness increases, early diagnosis and targeted management for syndromic RP are becoming more prevalent.

In recent years, research into innovative treatments such as stem cell therapy, retinal implants, and pharmacological agents has gained momentum. These approaches aim to preserve or restore vision. As these technologies advance and become more widely accessible, they are expected to further drive growth in the RP sector. The evolving therapeutic landscape presents new opportunities for patient care and industry expansion.

Key Takeaways

- In 2024, the global Retinitis Pigmentosa market was valued at US$ 14.9 Billion and is expected to reach US$ 29.9 Billion by 2034.

- The market is projected to grow at a CAGR of 7.1% from 2025 to 2034, driven by advancements in diagnostics and treatment approaches.

- The Autosomal Dominant disease type led the segment in 2024, accounting for over 54.3% of the total Retinitis Pigmentosa market share.

- Vitamin A Supplements dominated the treatment type category in 2024, securing more than 34.5% share due to their therapeutic benefits in slowing disease progression.

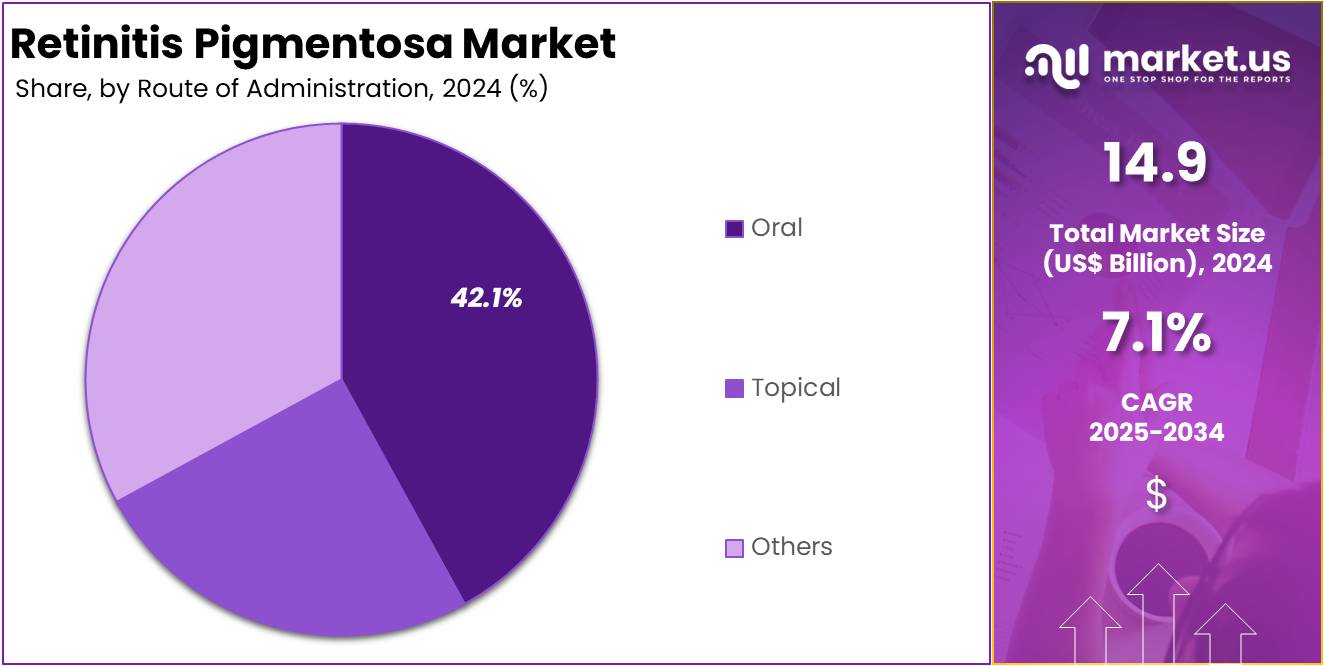

- The Oral route held the leading position in administration methods in 2024, capturing more than 42.1% of the overall segment share.

- Electroretinogram emerged as the top diagnostic method in 2024, with a market share exceeding 35.4%, due to its accuracy in detecting retinal abnormalities.

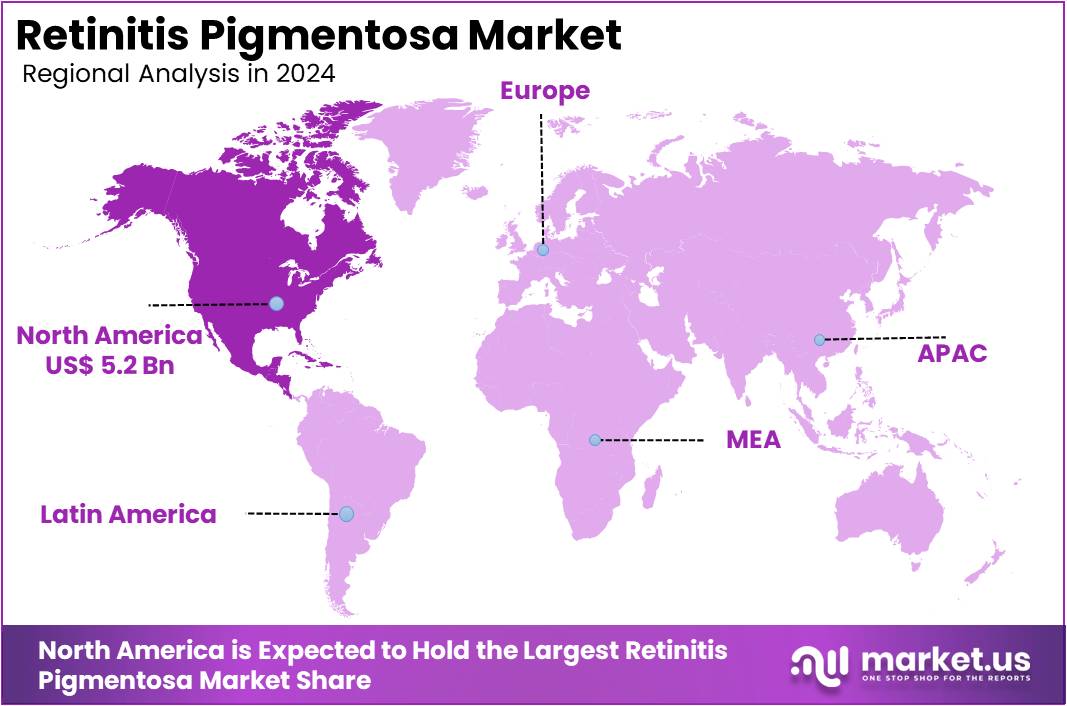

- North America led the global market in 2024, holding over 35.2% share and generating a regional value of US$ 5.2 Billion.

Disease Type Analysis

In 2024, the Autosomal Dominant section held a dominant market position in the disease type segment of the Retinitis Pigmentosa market, and captured more than a 54.3% share. This type of inheritance causes slower vision loss and usually affects both eyes equally. It is one of the most common forms of the disease. Increased access to genetic screening has helped detect cases earlier. These factors have contributed significantly to the large share held by this segment.

The Autosomal Recessive segment followed as the second-largest contributor to the market. This form of retinitis pigmentosa is usually more severe and tends to appear earlier in life. It is often found in regions with a higher rate of consanguinity. Advances in molecular testing have improved diagnosis in such populations. Clinical trials focusing on gene replacement therapies are also rising. These developments are supporting the gradual expansion of this segment in the overall market.

The X-linked Retinitis Pigmentosa segment remained the least common but most severe. It largely affects male patients and is associated with rapid vision decline at a young age. Despite the smaller affected population, research interest in this form is growing. Ongoing gene therapy studies are targeting mutations on the X chromosome. Early diagnosis through family history and genetic tests is improving. Future innovations may help address this unmet medical need.

Treatment Type Analysis

In 2024, the Vitamin A Supplements Section held a dominant market position in the Treatment Type Segment of Retinitis Pigmentosa Market, and captured more than a 34.5% share. This dominance can be linked to the long-standing use of Vitamin A palmitate in slowing retinal degeneration. Its low cost and easy availability have supported its widespread use. Many healthcare professionals still recommend Vitamin A as a first-line approach for early-stage patients, contributing to its sustained market presence.

Gene therapy is emerging as a powerful alternative in the treatment landscape. It targets genetic mutations responsible for inherited retinal disorders. This approach has shown encouraging results in clinical trials. Although its market share is currently smaller, gene therapy is expanding quickly. The growth is being supported by regulatory approvals and advancements in genetic science. It holds strong potential, especially for younger patients with specific genetic markers. Continued innovation is likely to drive future adoption.

Retinal implants are also gaining attention as a treatment option. These are primarily used in patients with late-stage disease. The technology helps restore limited vision by stimulating the retina. However, high costs and the need for surgical procedures have slowed adoption. Other treatments, such as Docosahexaenoic acid (DHA) and calcium channel blockers, are mainly used as complementary therapies. Their clinical impact remains limited compared to leading treatment types.

Route of Administration Analysis

In 2024, the Oral Section held a dominant market position in the Route of Administration Segment of Retinitis Pigmentosa Market, and captured more than a 42.1% share. Oral therapies are widely preferred due to their ease of use and better patient compliance. These treatments are generally used in long-term care. They act systemically and often target genetic or metabolic pathways linked to retinal degeneration. Their non-invasive nature continues to make them the first choice for patients and healthcare providers alike.

Topical treatments are also being used, although they hold a smaller share. These formulations, like eye drops and gels, aim to deliver medicine directly to the retina. They reduce systemic side effects but face challenges such as low bioavailability. Innovations in drug delivery systems are helping improve this method. Research in sustained-release drops and nano-formulations may support the future growth of topical options in treating retinitis pigmentosa effectively and safely.

The Others category includes advanced options such as intravitreal injections and implantable devices. These methods offer precise drug delivery and are often used in severe cases or clinical trials. Although their current usage is limited, their market potential is rising. Ongoing developments in gene and cell therapy are expected to drive interest in these routes over the coming years.

Diagnosis Analysis

In 2024, the Electroretinogram Section held a dominant market position in the Diagnosis Segment of Retinitis Pigmentosa Market, and captured more than a 35.4% share. This diagnostic method is widely preferred due to its accuracy in measuring retinal electrical responses. It helps in identifying functional abnormalities even before structural damage is visible. Electroretinograms are highly valuable in early-stage diagnosis, particularly among individuals with a family history of retinal diseases.

Optical Coherence Tomography (OCT) is another important diagnostic approach in the market. This imaging tool allows detailed visualization of retinal layers. OCT is commonly used for monitoring disease progression and treatment response. It is non-invasive, quick, and widely available in ophthalmology settings. Though it holds a smaller share than electroretinograms, its adoption is increasing due to improvements in imaging resolution and accessibility.

Other diagnostic options include fundus photography and genetic testing. Fundus images help in tracking pigment deposits and retinal thinning, supporting clinical decisions. Genetic testing is crucial for identifying specific mutations linked to inherited forms of retinitis pigmentosa. Though less frequently used, these methods complement primary diagnostic tools and contribute to a comprehensive assessment of the disease. Broader access to these technologies is expected to improve diagnostic accuracy in the coming years.

Key Market Segments

By Disease Type

- Autosomal Dominant

- Autosomal Recessive

- X-linked RP

By Treatment Type

- Vitamin A Supplements

- Docosahexaenoic acid (DHA)

- Calcium channel blockers

- Gene Therapy

- Retinal Implants

- Others

By Route of Administration

- Oral

- Topical

- Others

By Diagnosis

- Electroretinogram

- Visual Field Testing

- Genetic Testing

- Others

Drivers

Advancements In Gene Therapy

In recent years, the Retinitis Pigmentosa (RP) market has been significantly driven by breakthroughs in gene therapy. One of the most prominent examples is Luxturna (voretigene neparvovec), the first FDA-approved gene therapy for inherited retinal disease. This approval has opened new possibilities for addressing RP at its genetic root. By targeting specific mutations, gene therapy offers the potential to restore vision or slow degeneration, especially in patients with confirmed biallelic RPE65 mutation–associated retinal dystrophy.

These advancements have spurred increased investment and research interest across pharmaceutical and biotechnology companies. The success of Luxturna has served as proof of concept, encouraging further clinical trials for other gene-targeted therapies. New pipeline developments are actively exploring other gene defects responsible for RP. This innovation wave is supported by favorable regulatory frameworks that prioritize orphan drug designations and fast-track approvals, boosting the confidence of stakeholders in gene therapy as a viable commercial treatment path.

Furthermore, gene therapy is gaining support from public health institutions and patient advocacy groups. These stakeholders are driving awareness and funding, which contributes to the growth of the RP treatment ecosystem. As more data becomes available on long-term outcomes, the adoption of gene therapy is expected to expand. The increasing clinical success is laying the foundation for personalized treatment approaches in the RP market.

Restraints

High Cost of Treatment and Limited Accessibility

The high cost of treatment remains a major barrier in the Retinitis Pigmentosa market. Advanced therapies such as gene therapy and stem cell interventions involve complex research and manufacturing processes, which significantly increase their pricing. These treatments often require personalized solutions, further adding to the financial burden. As a result, many patients—especially those in uninsured or underinsured populations—find it challenging to afford long-term care, limiting overall patient access and adoption across the globe.

In low- and middle-income regions, accessibility is further restricted by limited healthcare infrastructure. The availability of specialized ophthalmologists, diagnostic centers, and treatment facilities is significantly lower in these areas. In addition, the lack of reimbursement programs and government funding makes it difficult for public healthcare systems to support costly interventions. Consequently, most patients in these regions are left with minimal or no access to advanced therapeutic options, worsening health disparities in inherited retinal disorders.

Moreover, even in high-income countries, insurance coverage for novel treatments like gene therapy is inconsistent. Regulatory uncertainties, delayed approvals, and restricted treatment slots in clinical programs contribute to delayed adoption. Many patients are added to waitlists or excluded due to financial limitations. This restraint continues to challenge the scalability of cutting-edge innovations and slows down the market’s broader penetration and equitable distribution of care.

Opportunities

Stem Cell Therapies in Retinitis Pigmentosa Market

Stem cell therapy presents a transformative opportunity for the Retinitis Pigmentosa (RP) market. Research into retinal regeneration using stem cells is advancing steadily, with promising results from preclinical and clinical trials. These therapies aim to replace or repair damaged photoreceptor cells, which are progressively lost in RP patients. This approach offers the potential to partially or fully restore visual function. As a result, stem cell-based treatments could emerge as a breakthrough in addressing the unmet needs of patients suffering from inherited retinal degeneration.

Several academic institutions and biotech firms are focusing on developing stem cell therapies for RP. For instance, studies using induced pluripotent stem cells (iPSCs) and embryonic stem cells have shown the ability to differentiate into retinal cells. These cells can be transplanted into the subretinal space to regenerate photoreceptors. Such advancements highlight the therapeutic potential of regenerative medicine in ophthalmology. The expanding clinical pipeline reinforces the role of stem cells in reshaping the treatment landscape for RP.

Moreover, increasing regulatory support and funding for stem cell research further enhance the market opportunity. The U.S. FDA and other health authorities have granted designations such as Orphan Drug and Regenerative Medicine Advanced Therapy (RMAT) to various stem cell candidates. This accelerates development timelines and promotes investor confidence. As technological barriers decline, stem cell therapies are expected to play a critical role in the future growth of the RP treatment market.

Trends

Growing Collaborations and Strategic Alliances in the Retinitis Pigmentosa Market

Collaborations between biotechnology firms and academic research institutions are gaining momentum in the Retinitis Pigmentosa (RP) market. These partnerships are aimed at leveraging advanced genetic insights and laboratory innovations. Research universities often provide access to preclinical models and expertise in gene therapy. Meanwhile, biotech firms contribute specialized technologies and development platforms. This synergy enables faster discovery and validation of potential treatment pathways. Such collaborations are playing a critical role in accelerating the pipeline for new therapies in inherited retinal disorders like RP.

Pharmaceutical companies are increasingly forming strategic alliances with startups and gene therapy firms to strengthen their RP treatment portfolios. These alliances often involve co-development agreements, licensing deals, and investment in early-stage clinical trials. Through such collaborations, larger firms gain access to niche technologies, while smaller players benefit from broader commercialization capabilities. These partnerships help overcome financial and technical barriers, fostering innovation in RP drug development. The result is an enhanced pace of research and reduced time-to-market for promising therapies.

Additionally, international public-private partnerships are supporting cross-border research initiatives in the RP market. Organizations such as the Foundation Fighting Blindness and government-funded bodies are backing joint ventures with global pharmaceutical companies. These alliances are facilitating multicenter clinical trials and expanding global access to investigational therapies. By combining funding, infrastructure, and scientific expertise, these collaborations are expected to drive significant advancements in the diagnosis and treatment of Retinitis Pigmentosa.

Regional Analysis

In 2024, North America held a dominant market position, capturing more than a 35.2% share and holds US$ 5.2 Billion market value for the year. The region’s leadership is driven by strong healthcare infrastructure and early diagnosis practices. Increased public awareness of genetic retinal disorders and access to advanced diagnostic technologies have contributed significantly to market expansion. Furthermore, ongoing support from research institutions and federal health programs plays a key role in driving therapeutic developments.

The presence of leading academic centers and patient advocacy organizations has encouraged clinical research and gene therapy trials across the United States and Canada. North America also benefits from higher rates of insurance coverage and better access to orphan drugs. These factors have helped improve patient outcomes and stimulate demand for innovative treatments. The availability of FDA-approved retinal implants and visual aid devices also supports the market’s growth.

Additionally, government initiatives promoting rare disease research, such as funding from the National Eye Institute (NEI), have further strengthened the regional outlook. Collaborative efforts between biotechnology firms and regulatory agencies are creating a favorable environment for treatment innovation. As a result, North America is expected to remain the primary revenue contributor to the global Retinitis Pigmentosa market during the forecast period.

The Asia Pacific region is emerging as a promising growth area in the global Retinitis Pigmentosa market. Several countries in this region, including China, Japan, India, and South Korea, are witnessing increased efforts in early diagnosis and public health awareness related to inherited retinal diseases. Government-funded eye health programs and improved access to ophthalmic care in urban and semi-urban areas are supporting the market’s expansion.

Rising healthcare expenditure and the growing prevalence of genetic eye disorders are encouraging investments in diagnostic imaging and genetic testing. Countries like Japan are at the forefront of clinical research, particularly in regenerative therapies and retinal implants. Additionally, increasing collaboration between research institutions and biotech firms is driving the development of novel therapies, including gene and stem cell-based treatments.

The expansion of medical tourism and the availability of low-cost treatment options also make Asia Pacific an attractive destination for ophthalmic care. With rising disposable incomes and an expanding middle-class population, the demand for advanced vision care is expected to grow. As infrastructure improves and regional governments continue to invest in rare disease research, Asia Pacific is likely to play a critical role in the global advancement of Retinitis Pigmentosa treatment solutions.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherland

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- New Zealand

- Singapore

- Thailand

- Vietnam

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

The global Retinitis Pigmentosa market is shaped by the strategic initiatives of leading pharmaceutical firms. These companies focus on research, treatment innovation, and broader global reach. Bausch Health contributes significantly through its investments in retinal disease therapies. The company’s focus on gene therapy development and partnerships in eye care help advance the treatment landscape. Its strong distribution network supports access to vision care products across developed and emerging markets, reinforcing its presence in the global ophthalmology segment.

Novartis AG remains a key player, particularly in gene and cell therapy for inherited retinal diseases. Its investment in Luxturna™, a leading gene therapy, highlights its leadership in treating rare genetic eye disorders. Novartis’ ophthalmology division is centered on precision treatments for progressive vision loss, including Retinitis Pigmentosa. The company also explores long-term regenerative therapies, showcasing its dedication to innovative approaches. Its efforts strengthen the pipeline for targeted therapies in inherited retinal conditions.

Sun Pharmaceutical Industries Ltd. is expanding its reach in rare ophthalmic diseases by offering both generic and specialty treatments. Its focus is on improving access to retinal therapies, particularly in low- and middle-income countries. By addressing cost and availability barriers, Sun Pharma aims to enhance care for Retinitis Pigmentosa patients. The company’s emphasis on therapeutic affordability aligns with growing demand in emerging regions. This approach positions it as a major contributor to the retinal treatment segment.

Allergan, now under AbbVie, and Astellas Pharma are also important contributors. Allergan has a well-established presence in eye care and supports research in neuroprotective and long-acting delivery systems. Astellas has strengthened its position in gene therapy through the acquisition of Audentes Therapeutics. It is actively pursuing AAV-based treatments for inherited retinal disorders. In addition, several biotechnology startups and academic institutions are advancing CRISPR, stem cell, and neuroprotective therapies, further driving innovation in this orphan disease segment.

Market Key Players

- Bausch Health Companies Inc.

- Novartis AG

- Sun Pharmaceutical Industries Ltd.

- Allergan

- Astellas Pharma Inc.

- AstraZeneca

- Johnson & Johnson Private Limited

- Orphagen Pharmaceuticals Inc.

- Clino Corporation

- Spark Therapeutics Inc.

- Caladrius Biosciences Inc.

- Genethon

Recent Developments

- In December 2024: Bausch + Lomb, a subsidiary of Bausch Health, acquired Elios Vision Inc., the developer of the ELIOS system a minimally invasive glaucoma surgery (MIGS) procedure utilizing an excimer laser. This acquisition underscores Bausch + Lomb’s commitment to providing advanced solutions for glaucoma treatment, enhancing care for patients worldwide.

- In May 2024: Johnson & Johnson introduced the EYE-RD Global Registry at the Association for Research in Vision and Ophthalmology (ARVO) Annual Meeting. This first-of-its-kind, non-interventional global registry aims to collect longitudinal clinical data on patients with inherited retinal diseases (IRDs), including X-linked retinitis pigmentosa (XLRP). The registry is designed to bridge knowledge gaps by providing real-world insights into disease progression and patient experiences, thereby supporting research, diagnosis, and treatment strategies for IRDs.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | US$ 14.9 Billion |

| Forecast Revenue (2034) | US$ 29.6 Billion |

| CAGR (2025-2034) | 7.1% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments |

| Segments Covered | By Disease Type (Autosomal Dominant, Autosomal Recessive, X-linked RP), By Treatment Type (Vitamin A Supplements, Docosahexaenoic acid (DHA), Calcium channel blockers, Gene Therapy, Retinal Implants, Others), By Route of Administration (Oral, Topical, Others), By Diagnosis (Electroretinogram, Visual Field Testing, Genetic Testing, Others) |

| Regional Analysis | North America – The US, Canada, & Mexico; Western Europe – Germany, France, The UK, Spain, Italy, Portugal, Ireland, Austria, Switzerland, Benelux, Nordic, & Rest of Western Europe; Eastern Europe – Russia, Poland, The Czech Republic, Greece, & Rest of Eastern Europe; APAC – China, Japan, South Korea, India, Australia & New Zealand, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, & Rest of APAC; Latin America – Brazil, Colombia, Chile, Argentina, Costa Rica, & Rest of Latin America; Middle East & Africa – Algeria, Egypt, Israel, Kuwait, Nigeria, Saudi Arabia, South Africa, Turkey, United Arab Emirates, & Rest of MEA |

| Competitive Landscape | Bausch Health Companies Inc., Novartis AG, Sun Pharmaceutical Industries Ltd., Allergan, Astellas Pharma Inc., AstraZeneca, Johnson & Johnson Private Limited, Orphagen Pharmaceuticals Inc., Clino Corporation, Spark Therapeutics Inc., Caladrius Biosciences Inc., Genethon |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |