Quick Navigation

Report Overview

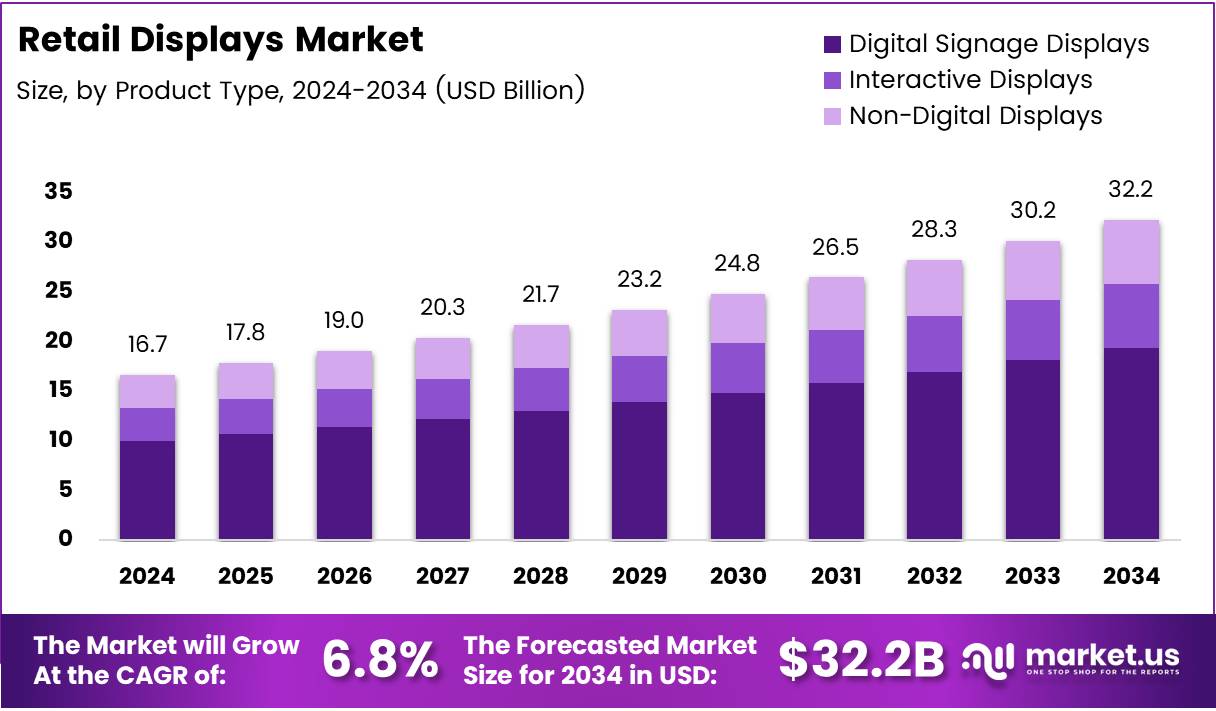

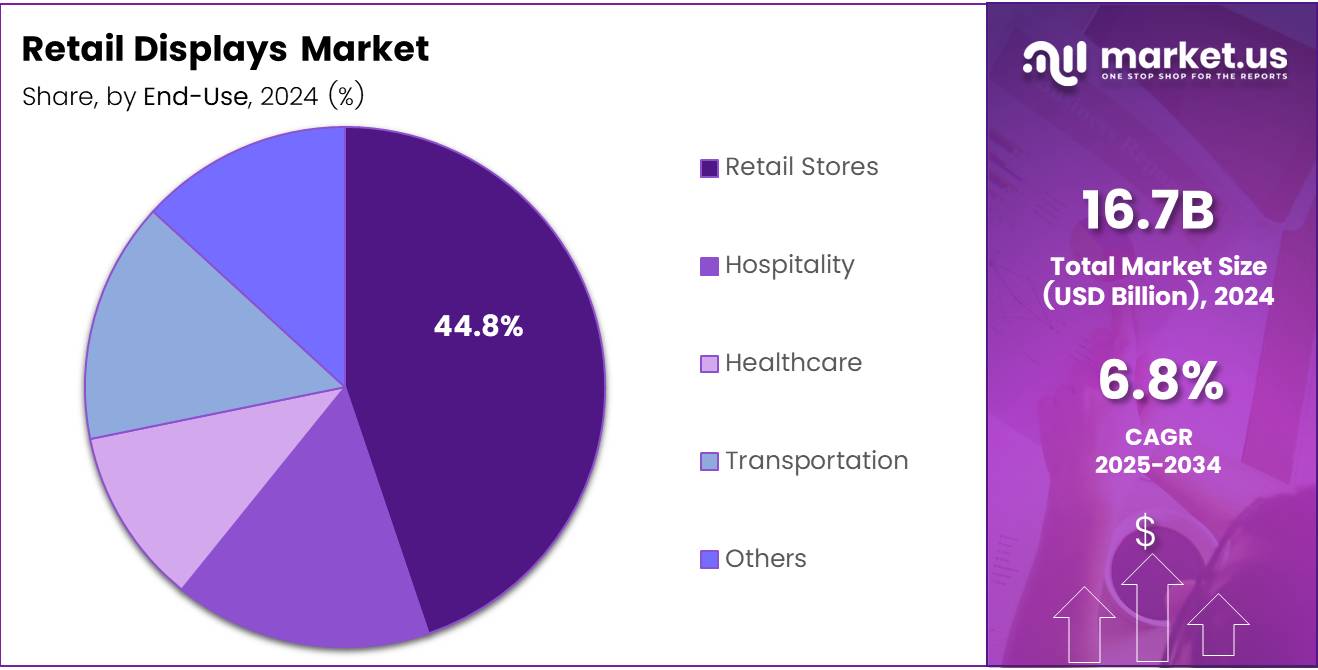

The Global Retail Displays Market size is expected to be worth around USD 32.2 Billion by 2034, from USD 16.7 Billion in 2024, growing at a CAGR of 6.8% during the forecast period from 2025 to 2034.

The Retail Displays Market represents a critical segment of the in-store marketing ecosystem, shaping how brands connect with shoppers at the point of purchase. It includes digital signage, shelf displays, POP stands, and interactive kiosks that influence buying behavior and strengthen brand visibility in competitive retail environments.

Moreover, as retail evolves, businesses are integrating smart and digital display technologies to create immersive consumer experiences. Retailers now focus on real-time engagement and adaptive content, allowing displays to react to customer data and demographics. This transformation is driving higher foot traffic, stronger conversions, and improved brand recall across retail chains globally.

Additionally, growing investments in digital transformation initiatives are accelerating market demand. Governments across regions are supporting smart retail infrastructure and local manufacturing of display technologies, particularly in Asia-Pacific and North America. These initiatives aim to boost innovation, sustainability, and energy-efficient display solutions across commercial and retail sectors.

Furthermore, sustainability remains a strong growth driver. Retailers increasingly adopt eco-friendly materials, modular display designs, and LED-based technologies to reduce carbon footprints. Manufacturers are responding with recyclable display solutions and energy-efficient screens that align with global green retail policies and environmental regulations, ensuring compliance and long-term operational efficiency.

According to industry reports, shoppers still expect 45% of purchases to come from physical stores in 2024, projected to decline to 41% by 2026. This trend is pushing retailers to enhance in-store experiences and invest in interactive displays that blend digital and physical shopping touchpoints.

Similarly, AI-influenced online sales reached $229 billion globally during the 2024 U.S. holiday season, while chatbot use rose 42% year over year, signaling a growing preference for dynamic, data-driven content on retail screens. This underscores a major opportunity for the Retail Displays Market to integrate AI-driven personalization, analytics, and immersive technologies, ensuring seamless omnichannel engagement and sustainable market expansion.

Key Takeaways

- The Global Retail Displays Market is projected to reach USD 32.2 Billion by 2034, growing from USD 16.7 Billion in 2024 at a CAGR of 6.8%.

- Digital Signage Displays dominated the Product Type segment in 2024 with a 49.3% share, driven by real-time content and interactive visual promotions.

- LCD technology led the Display Technology segment with a 39.4% share, favored for cost-efficiency, clarity, and energy savings.

- Point of Sale (POS) Displays captured 26.6% of the Application segment, capitalizing on impulse buying and promotional visibility.

- Retail Stores accounted for 44.8% of the End-Use segment, reflecting investments to enhance in-store visual merchandising and customer engagement.

- North America dominated the market with a 39.2% share, driven by advanced retail technologies, organized retail networks, and strong consumer spending.

By Product Type Analysis

Digital Signage Displays dominate with 49.3% due to their dynamic content delivery and enhanced visual appeal.

In 2024, Digital Signage Displays held a dominant market position in the By Product Type segment of the Retail Displays Market, with a 49.3% share. The growth is driven by the rapid adoption of digital signage in retail spaces to attract customers and promote real-time offers. Their ability to display customized content and interactive visuals enhances customer engagement and boosts sales performance.

Interactive Displays are gaining momentum as retailers increasingly focus on customer experience. These displays enable shoppers to explore product details, check availability, and make quick purchase decisions. The touch-based and sensor-integrated systems foster a personalized shopping journey, helping brands to connect better with tech-savvy customers.

Non-Digital Displays continue to remain relevant, especially among small and medium retailers with limited budgets. These displays, including posters, standees, and shelf talkers, offer a cost-effective means to highlight promotions. Although traditional, they still play a significant role in creating visual merchandising strategies that complement digital formats.

By Display Technology Analysis

LCD (Liquid Crystal Display) dominates with 39.4% due to its cost-efficiency and widespread availability.

In 2024, LCD (Liquid Crystal Display) technology held a dominant market position in the By Display Technology segment of the Retail Displays Market, with a 39.4% share. LCDs remain a preferred choice for retailers due to their affordability, energy efficiency, and high-definition visual output, making them ideal for large-scale installations.

LED (Light Emitting Diode) displays are rapidly expanding across modern retail environments. They offer superior brightness, vibrant colors, and long lifespan, which make them suitable for both indoor and outdoor applications. As costs decline, LED technology is becoming more accessible to small retailers.

OLED (Organic Light Emitting Diode) displays are emerging as premium options due to their ultra-thin profiles and flexible designs. Retailers adopt OLEDs to create immersive and futuristic display experiences, particularly in luxury retail segments.

E-paper Displays are gradually finding niche applications in shelf labeling and dynamic pricing systems. Their low power consumption and paper-like readability make them ideal for sustainable retail operations.

Projection technology continues to be used in experiential marketing and pop-up events. Retailers leverage projection for creating large visual narratives, brand storytelling, and immersive shopping experiences.

By Application Analysis

Point of Sale (POS) Displays dominate with 26.6% owing to their crucial role in influencing last-minute purchase decisions.

In 2024, Point of Sale (POS) Displays held a dominant market position in the By Application segment of the Retail Displays Market, with a 26.6% share. These displays are strategically placed near checkout counters to boost impulse buying and highlight promotional offers.

Point of Purchase (POP) Displays continue to play an integral role in capturing shopper attention at product shelves. Retailers use them to showcase new launches, attract walk-in customers, and reinforce brand recognition.

In-Store Marketing displays focus on promoting seasonal campaigns and exclusive deals. Retailers utilize both digital and non-digital media to create visually appealing store environments that drive engagement.

Interactive Advertising integrates technology such as motion sensors and touchscreens to deliver personalized experiences. These displays enhance consumer-brand interaction and support data-driven marketing strategies.

Customer Engagement displays are designed to strengthen loyalty by offering information, entertainment, and personalized recommendations. They create memorable brand interactions.

Product Information Displays serve as essential tools to educate consumers about features, usage, and benefits. They simplify decision-making and enhance transparency.

Others include event-specific or promotional display formats tailored for short-term campaigns and brand activations.

By End-Use Analysis

Retail Stores dominate with 44.8% as they remain the primary adopters of visual merchandising technologies.

In 2024, Retail Stores held a dominant market position in the By End-Use segment of the Retail Displays Market, with a 44.8% share. The demand is driven by increasing competition among retailers to improve in-store experiences and influence customer decisions through visually engaging displays.

Hospitality uses retail display solutions for menu boards, promotions, and guest information. Digital signage enhances the ambience and promotes special offers in restaurants, hotels, and entertainment venues.

Healthcare facilities implement displays to provide patient information, promote health awareness, and streamline navigation. The use of digital displays in pharmacies aids in highlighting wellness products.

Transportation sectors utilize displays for advertising, passenger guidance, and brand promotions across airports, metro stations, and bus terminals. Their high visibility makes them ideal for mass communication.

Others include corporate offices, educational institutions, and public venues that adopt display solutions for branding and information dissemination purposes, enhancing communication effectiveness.

Key Market Segments

By Product Type

- Digital Signage Displays

- Interactive Displays

- Non-Digital Displays

By Display Technology

- LCD (Liquid Crystal Display)

- LED (Light Emitting Diode)

- OLED (Organic Light Emitting Diode)

- E-paper Displays

- Projection

By Application

- Point of Sale (POS) Displays

- Point of Purchase (POP) Displays

- In-Store Marketing

- Interactive Advertising

- Customer Engagement

- Product Information Displays

- Others

By End-Use

- Retail Stores

- Hospitality

- Healthcare

- Transportation

- Others

Drivers

Increasing Adoption of Digital Signage and Interactive Retail Displays for Enhanced Customer Engagement

The retail displays market is witnessing strong growth due to the rising use of digital signage and interactive technologies. Retailers are increasingly turning to digital displays to create engaging in-store experiences that attract shoppers and encourage longer visits. Interactive displays, such as touchscreens and motion-based systems, help brands showcase products more dynamically while providing personalized recommendations.

Visually appealing displays have become a key sales tool as consumers prefer products presented in an attractive and informative manner. This has encouraged retailers to invest in innovative display formats that highlight brand identity and drive impulse purchases. As competition grows, the visual presentation of products now plays a crucial role in influencing buying decisions.

The global expansion of organized retail, including hypermarkets and shopping malls, is also fueling the demand for modern display systems. Retailers in emerging markets are adopting advanced display technologies to stay competitive and attract tech-savvy customers.

Moreover, the integration of AI and IoT is transforming retail displays into smart solutions capable of tracking shopper behavior and adjusting content in real time. This data-driven approach allows retailers to deliver targeted promotions, improving customer engagement and overall sales performance.

Restraints

Limited Space in Small Retail Outlets Restricting Large Display Installations

Despite strong market potential, the retail displays industry faces several challenges. One major restraint is the limited floor space available in small retail outlets. Many small and medium-sized stores struggle to install large or interactive display systems, which restricts the adoption of advanced visual merchandising solutions.

Environmental concerns are another growing issue. The increasing number of outdated electronic display systems contributes to electronic waste, raising sustainability challenges for both manufacturers and retailers. Disposal and recycling of these systems require additional costs and compliance with environmental regulations, which can limit their widespread use.

Furthermore, the rapid pace of technological change leads to short product life cycles. New display technologies frequently replace older models, making previous investments obsolete within a few years. This constant need for upgrades adds financial pressure on retailers, especially smaller ones with limited budgets.

Overall, space limitations, environmental issues, and quick obsolescence are significant barriers that slow down the full adoption of modern retail display technologies. Addressing these concerns through sustainable materials and scalable designs could help mitigate their impact.

Growth Factors

Expansion of Digital Retail Ecosystems Across Emerging Economies and Tier-2 Cities

The retail displays market holds significant growth opportunities, particularly in emerging economies and tier-2 cities. As digital retail ecosystems expand, more stores are incorporating advanced display technologies to attract younger, tech-driven consumers. This trend is expected to accelerate with the increasing digitalization of the retail sector.

The adoption of energy-efficient LED and OLED displays is another promising opportunity. These technologies not only reduce energy consumption but also offer brighter visuals and longer lifespans, making them a cost-effective investment for retailers aiming to enhance in-store experiences sustainably.

Growing investments in omnichannel retail strategies are also creating new possibilities. Retailers are blending physical and online experiences, using digital displays to provide consistent brand messaging and real-time updates across all channels. This integration helps in building stronger customer relationships and improving engagement.

Additionally, the development of customizable and modular display solutions enables retailers to design flexible layouts suited for different product categories. Such adaptability is especially beneficial for brands seeking to refresh store designs frequently without major infrastructure changes.

Emerging Trends

Shift Toward Sustainable and Recyclable Materials in Display Manufacturing

Sustainability has become a major trend shaping the future of the retail displays market. Manufacturers are increasingly adopting recyclable and eco-friendly materials to reduce the environmental footprint of display systems. Retailers are also favoring suppliers who align with green initiatives, reflecting the growing consumer demand for responsible business practices.

Another emerging trend is the use of immersive technologies such as Augmented Reality (AR) and Virtual Reality (VR) in retail displays. These advanced displays provide interactive and engaging shopping experiences, helping customers visualize products before purchase and enhancing brand recall.

Cloud-based display management systems are also gaining traction. They allow retailers to update display content in real time across multiple store locations, improving operational efficiency and ensuring consistent messaging.

Moreover, collaborations between display manufacturers and retail brands are becoming more common. Such partnerships enable the creation of personalized and data-driven visual merchandising strategies that resonate with target audiences. These collaborative and technology-driven approaches are expected to define the next phase of retail display innovation.

Regional Analysis

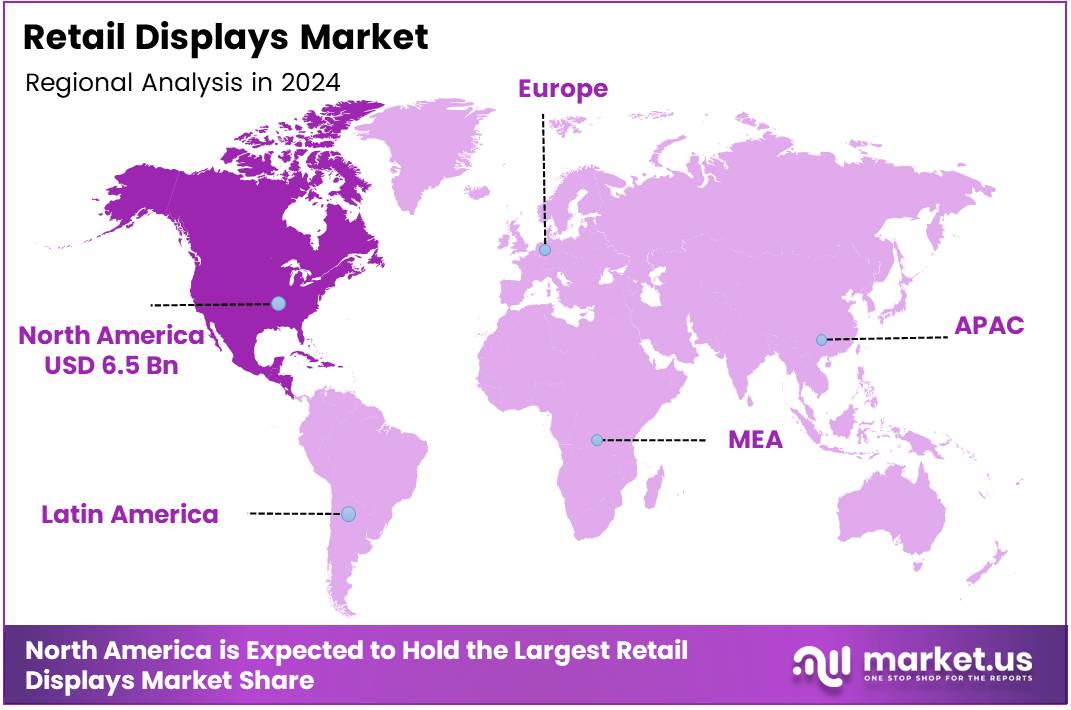

North America Dominates the Retail Displays Market with a Market Share of 39.2%, Valued at USD 6.5 Billion

In 2024, North America emerged as the leading region in the global Retail Displays Market, capturing 39.2% of the total share. The dominance is driven by the widespread presence of organized retail chains, advanced in-store marketing technologies, and strong consumer spending patterns. Retailers increasingly adopt digital and interactive displays to enhance shopper engagement and brand recall, fueling steady market expansion in the U.S. and Canada.

Europe Retail Displays Market Trends

Europe maintains a robust position in the Retail Displays Market, supported by a strong retail infrastructure and innovation in visual merchandising. The region witnesses rising adoption of energy-efficient and sustainable display materials, particularly in the U.K., Germany, and France. Retailers focus on eco-conscious designs and digital transformation to attract urban consumers and align with sustainability directives.

Asia Pacific Retail Displays Market Trends

The Asia Pacific region is experiencing rapid growth due to the expansion of modern retail formats and rising disposable incomes. Countries like China, Japan, and South Korea are investing in smart display systems to improve customer interaction and store aesthetics. Evolving shopping behaviors and digital retail integration make Asia Pacific a major growth frontier.

Middle East and Africa Retail Displays Market Trends

In the Middle East and Africa, the Retail Displays Market is growing steadily with the expansion of luxury malls and international retail chains. Increasing tourism and the development of new commercial complexes in the UAE and Saudi Arabia are key enablers. Retailers are embracing digital signage and experiential displays to attract premium shoppers.

Latin America Retail Displays Market Trends

Latin America’s Retail Displays Market is witnessing gradual growth, driven by retail modernization and the rising influence of global brands. Countries like Brazil and Mexico are investing in cost-effective and flexible display solutions. The region’s market is supported by the shift toward promotional in-store activities and increasing adoption of digital advertising displays.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Retail Displays Company Insights

In 2024, the global Retail Displays Market continues to evolve rapidly, driven by technological advancements, smart display integration, and growing demand for immersive consumer experiences.

Samsung Electronics Co., Ltd. remains a dominant player, leveraging its innovation in OLED and QLED technologies to provide energy-efficient, high-resolution retail displays. The company’s focus on smart signage and AI-driven visual solutions strengthens its leadership, especially in premium retail environments.

LG Display Co., Ltd. is making notable strides with its advancements in flexible OLED and transparent display technologies. The company emphasizes sustainability and next-generation visual performance, making it a preferred choice for luxury retail brands seeking both aesthetics and functionality. LG’s strategic partnerships with retail solution providers further enhance its global footprint.

Panasonic Corporation continues to expand its presence in the retail display segment through its emphasis on digital signage and durable commercial-grade LCDs. Known for reliability and innovation, Panasonic’s displays are widely adopted in large retail chains and shopping centers, offering seamless integration with interactive technologies.

Sharp Corporation maintains its competitive edge by focusing on ultra-high-definition display panels and energy-efficient solutions tailored for retail use. Its expertise in LCD technology and commitment to design innovation support the growing need for visually striking and cost-effective retail display systems.

Overall, the market in 2024 is characterized by a strong push toward smart, sustainable, and interactive display technologies. These key players continue to shape the competitive landscape through innovation, strategic collaborations, and customer-centric product portfolios.

Top Key Players in the Market

- Samsung Electronics Co., Ltd.

- LG Display Co., Ltd.

- Panasonic Corporation

- Sharp Corporation

- Sony Corporation

- NEC Display Solutions Ltd.

- Planar Systems, Inc.

Recent Developments

- In July 2025, TRG (The Royal Group) expanded its retail strategy through the acquisition of Trans World Marketing, a leading provider of in-store marketing and retail display solutions. This strategic move strengthens TRG’s capabilities in end-to-end retail experiences, enhancing its design-to-execution offerings across multiple consumer categories.

- In August 2025, Prometheus Retail Solutions acquired PackagingARTS, marking a pivotal step in transforming the luxury wine & spirits retail environment. The merger integrates creative packaging, design, and retail presentation expertise to deliver immersive, high-end consumer experiences in the premium beverage sector.

- In October 2024, DGS Retail completed the acquisition of SMS Display and announced the formation of the Agility Retail Group. This consolidation aims to unify retail display innovation, merchandising systems, and store fixture manufacturing under one agile, growth-focused entity.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 16.7 Billion |

| Forecast Revenue (2034) | USD 32.2 Billion |

| CAGR (2025-2034) | 6.8% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Product Type (Digital Signage Displays, Interactive Displays, Non-Digital Displays), By Display Technology (LCD, LED, OLED, E-paper Displays, Projection), By Application (POS Displays, POP Displays, In-Store Marketing, Interactive Advertising, Customer Engagement, Product Information Displays, Others), By End-Use (Retail Stores, Hospitality, Healthcare, Transportation, Others) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | Samsung Electronics Co., Ltd., LG Display Co., Ltd., Panasonic Corporation, Sharp Corporation, Sony Corporation, NEC Display Solutions Ltd., Planar Systems, Inc. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |