Quick Navigation

- Report Overview

- Key Takeaway

- Role of Generative AI

- Investment and Business Benefits

- Regional Analysis

- Deployment Mode Analysis

- Organization Size Analysis

- Application Analysis

- End-User Industry Analysis

- Key Market Segments

- Emerging Trends

- Growth Factors

- Market Dynamics

- Key Players Analysis

- Recent Developments

- Report Scope

Report Overview

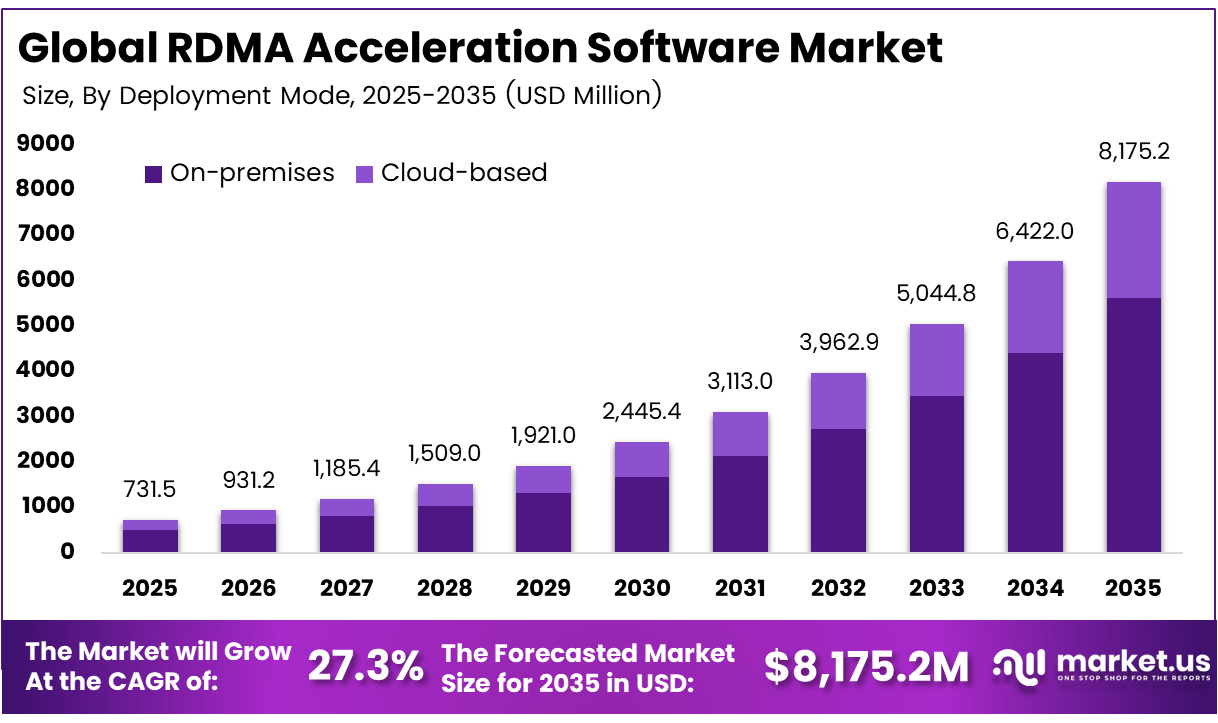

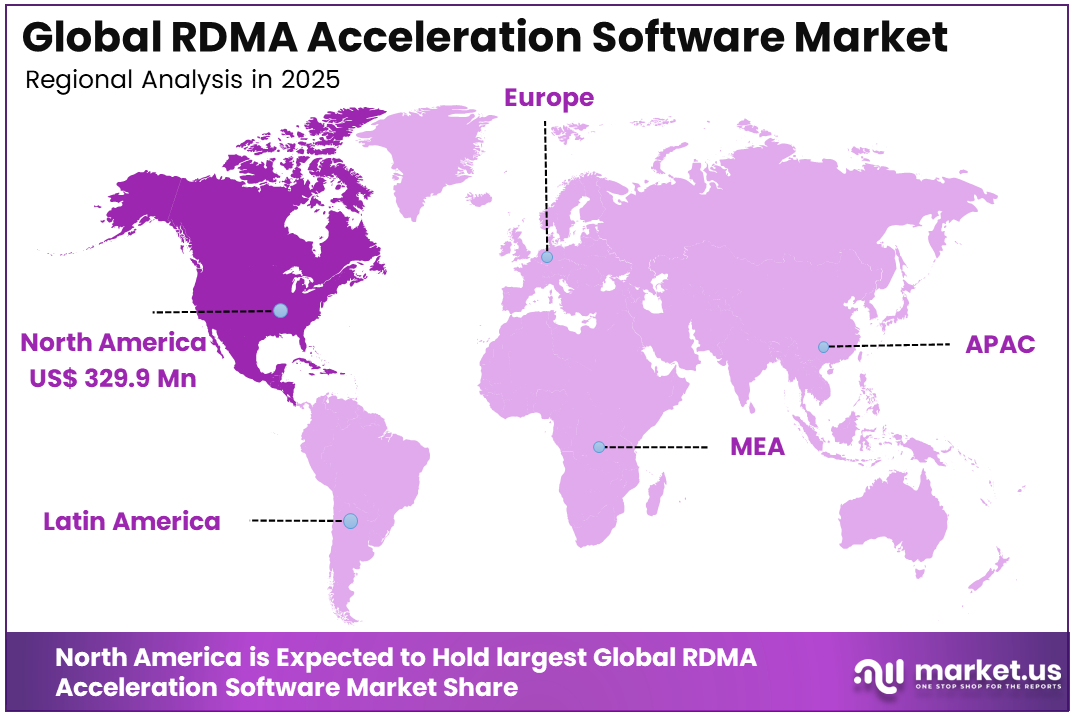

The Global RDMA Acceleration Software Market size is expected to be worth around USD 8,175.2 million by 2035, from USD 731.5 million in 2025, growing at a CAGR of 27.3% during the forecast period from 2025 to 2035. North America held a dominant market position, capturing more than 45.1% share and generating USD 329.9 million in revenue.

RDMA Acceleration Software refers to tools that improve data transfer between servers by allowing direct memory access with less CPU involvement. It is used in data centers, AI clusters, storage systems, and high-speed networks where low latency and stable performance are important. It helps applications move large amounts of data faster and more efficiently.

The market is supported by the rising use of AI training clusters, in-memory databases, and distributed analytics platforms. These workloads need microsecond-level latency and stable bandwidth for large data movement. Many operators report CPU usage drops from around 50% to under 10% in some RDMA-enabled pipelines, encouraging faster upgrades across data centers and edge nodes.

The market for RDMA Acceleration Software is driven by the growing need for faster data movement across AI clusters, cloud data centers, storage systems, and real-time analytics platforms. Enterprises are using it to reduce network delay, lower CPU involvement, and improve workload performance. Its value is rising as distributed applications require stable bandwidth and faster communication between connected servers.

Demand is increasing across finance, healthcare, telecom, and machine vision, where frequent small messages and parallel data streams often create network bottlenecks. Adoption is stronger in environments already using high-speed Ethernet or InfiniBand. These networks can support RDMA more effectively through tuned firmware, optimized transport layers, and better handling of low-latency workloads.

For instance, in April 2026, IBM advanced its hybrid-cloud and AI data-center strategy by promoting high-performance fabrics for Red Hat OpenShift and IBM Cloud. The company increasingly positions RDMA support as a way for enterprises to accelerate databases, analytics, and AI workloads, with RDMA acceleration software orchestrating low-latency data paths across on-prem and cloud clusters.

Key Takeaway

- In 2025, the On-premises segment held a dominant market position, capturing a 68.7% share of the Global RDMA Acceleration Software Market.

- In 2025, the Large Enterprises segment held a dominant market position, capturing a 78.6% share of the Global RDMA Acceleration Software Market.

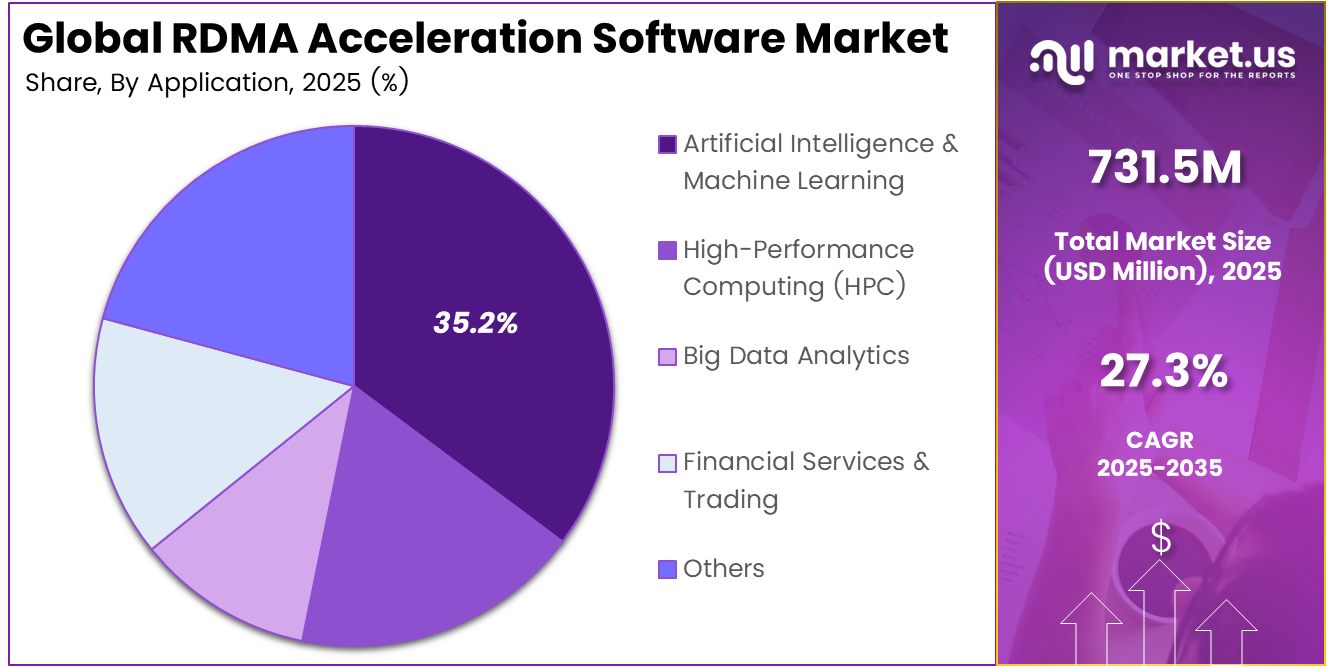

- In 2025, the Artificial Intelligence & Machine Learning segment held a dominant market position, capturing a 35.2% share of the Global RDMA Acceleration Software Market.

- In 2025, the IT & Telecommunications segment held a dominant market position, capturing a 47.3% share of the Global RDMA Acceleration Software Market.

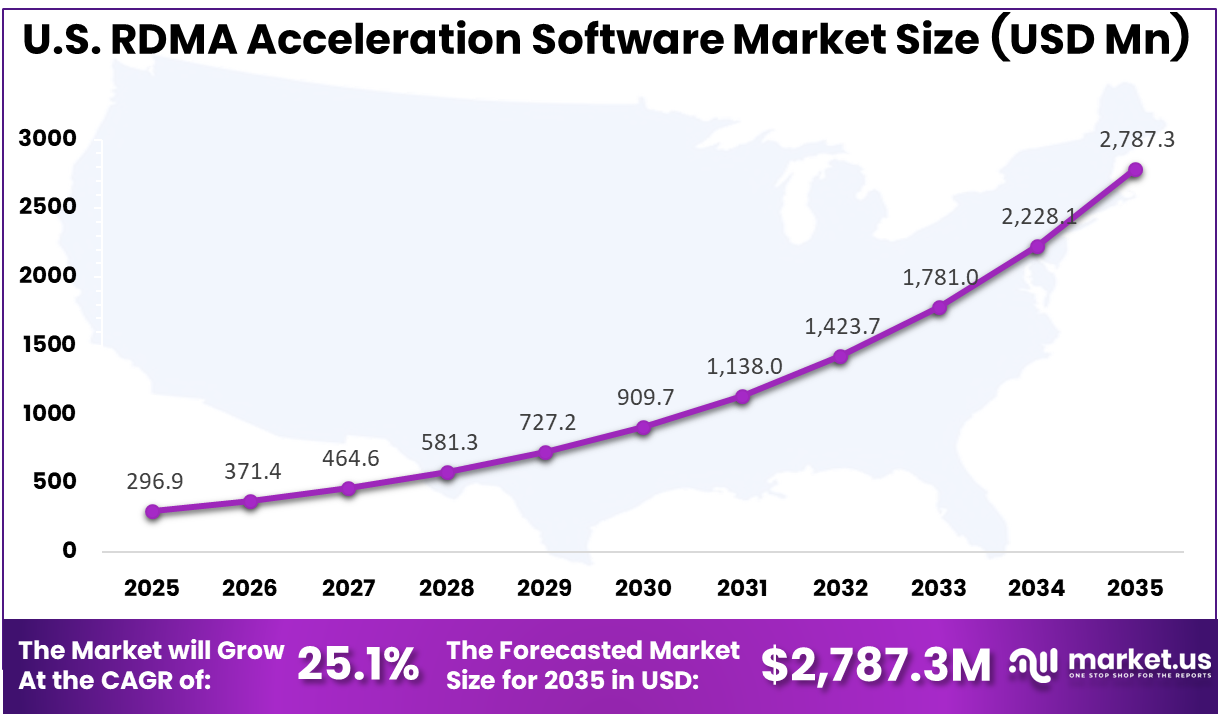

- The U.S. RDMA Acceleration Software Market was valued at USD 296.9 Million in 2025, with a robust CAGR of 25.1%.

- In 2025, North America held a dominant market position in the Global RDMA Acceleration Software Market, capturing more than a 45.1% share.

Role of Generative AI

Generative AI training depends on large GPU clusters that need fast data movement between nodes. RDMA helps reduce idle time by offloading network tasks from CPUs. One major provider reported roughly 70% of internal storage traffic on Ethernet-based RDMA instead of TCP, showing its growing role in AI infrastructure.

As models move toward trillions of parameters, training jobs often use thousands of GPUs and push networks near full capacity. RDMA acceleration software improves flow control, congestion handling, and CPU bypass. This supports better job completion, steadier scaling, and faster access to object storage adapted for AI training workloads.

Investment and Business Benefits

Investment opportunities are emerging in software-defined RDMA control planes, virtualization-aware frameworks, and tools that manage congestion, fairness, and multi-tenant isolation at scale. Growth potential is also seen in acceleration software for AI training fabrics, content delivery, remote storage, and long-distance RDMA, where optimization beyond 100 kilometers is now actively studied.

Business benefits include higher application throughput, shorter batch windows, and more predictable service quality for mission-critical workloads. RDMA helps reduce networking overhead by freeing CPU cycles, allowing organizations to consolidate servers or delay hardware refresh cycles. This supports long-term operating cost control and can lower power use per transaction in demanding digital infrastructure.

Regional Analysis

In 2025, North America held a dominant market position in the Global RDMA Acceleration Software Market, capturing more than 45.1% share and generating USD 329.9 million in revenue. This dominance is due to the strong presence of hyperscale data centers, cloud service providers, AI infrastructure, and advanced telecom networks across North America. Enterprises in the region are adopting RDMA acceleration software to reduce latency, improve data transfer, and support high-performance workloads. Strong investment in AI training clusters, distributed storage, financial trading systems, and edge computing also supports wider adoption across mission-critical digital infrastructure.

For instance, in November 2025, NVIDIA showcased RDMA-accelerated S3-compatible AI storage, optimized with its networking and GPU platforms, enabling low-latency, high-throughput data access for large-scale training workloads in North American hyperscale data centers. This reinforces NVIDIA’s central role in RDMA acceleration software stacks used for AI and HPC clusters across the region.

U.S. RDMA Acceleration Software Market Size

The market for RDMA Acceleration Software within the U.S. is growing tremendously and is currently valued at USD 296.9 million; the market has a projected CAGR of 25.1%. The market is growing due to the rapid expansion of AI data centers, cloud infrastructure, high-performance computing, and low-latency enterprise applications in the U.S. Strong demand from hyperscale operators, financial services, healthcare data platforms, and telecom networks is increasing the use of RDMA acceleration software. Its ability to reduce CPU load, improve data movement, and support faster distributed workloads is making it important for modern digital infrastructure.

For instance, in April 2026, IBM advanced its hybrid-cloud and AI data-center strategy by promoting high-performance fabrics for Red Hat OpenShift and IBM Cloud. The company increasingly positions RDMA support as a way for enterprises to accelerate databases, analytics, and AI workloads, with RDMA acceleration software orchestrating low-latency data paths across on-prem and cloud clusters.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherlands

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Thailand

- Vietnam

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Deployment Mode Analysis

In 2025, the On-premises segment held a dominant market position, capturing a 68.7% share of the Global RDMA Acceleration Software Market. This dominance is due to the strong need for direct control over data center networking, latency settings, and workload security. On-premises deployment allows enterprises to tune RDMA software with servers, network cards, storage systems, and applications under one controlled infrastructure.

It is also preferred where critical workloads cannot depend fully on external cloud environments. Financial systems, AI clusters, storage platforms, and analytics engines benefit from closer hardware control, stable bandwidth, and lower CPU overhead, making on-premises deployment more suitable for performance-sensitive operations.

For instance, in July 2025, NVIDIA expanded its GPUDirect RDMA guides for Grace Blackwell platforms, helping data center teams wire GPUs, NICs, and switches for ultra-low latency inside their own racks. The updated documentation focuses on tuning on-premises clusters, making it easier for operators to roll out RDMA acceleration software in tightly controlled environments.

Organization Size Analysis

In 2025, the Large Enterprises segment held a dominant market position, capturing a 78.6% share of the Global RDMA Acceleration Software Market. This dominance is due to the larger scale of infrastructure operated by big organizations. Large enterprises manage complex databases, cloud platforms, AI workloads, and distributed storage systems that need fast communication between servers with minimum delay and predictable performance.

These organizations also have stronger budgets and technical teams to deploy RDMA acceleration software correctly. Their ability to invest in advanced network adapters, tuned Ethernet fabrics, and skilled support makes adoption easier across high-volume workloads and mission-critical applications.

For instance, in November 2025, at Ignite 2025, Microsoft highlighted RDMA-based connectivity inside Azure for demanding applications, showing live demos that linked regions with low-latency paths. Large enterprises running global services saw how RDMA can sustain performance across big, distributed systems, pushing them to adopt similar acceleration approaches in their own estates.

Application Analysis

In 2025, the Artificial Intelligence & Machine Learning segment held a dominant market position, capturing a 35.2% share of the Global RDMA Acceleration Software Market. This dominance is due to the rising use of AI training clusters that depend on the fast movement of data between GPUs, storage, and compute nodes. RDMA acceleration software helps reduce CPU involvement and supports smoother data transfer across distributed AI workloads.

AI and machine learning systems also require stable throughput during model training and inference. As workloads become more distributed, network delays can slow processing and reduce hardware efficiency. RDMA helps improve communication between nodes, making it valuable for large AI pipelines.

For instance, in January 2026, AWS release notes for Elastic Fabric Adapter detailed updates to libfabric, RDMA core, and NCCL integrations to support GPU-intensive training jobs. These improvements help customers run distributed AI workloads more efficiently on EC2, demonstrating how tightly tuned RDMA acceleration software can directly improve training times and cluster utilization.

End-User Industry Analysis

In 2025, the IT & Telecommunications segment held a dominant market position, capturing a 47.3% share of the Global RDMA Acceleration Software Market. This dominance is due to the heavy use of low-latency infrastructure in IT and telecom environments. Cloud platforms, data centers, telecom networks, and managed service providers rely on fast data movement to support storage, databases, virtual machines, and real-time applications.

The segment also benefits from continuous demand for reliable digital services. Telecom and IT operators need stronger network performance, better server utilization, and stable service quality. RDMA acceleration software supports these needs by reducing networking overhead and improving data flow across critical infrastructure.

For instance, in March 2025, Intel’s announcements at MWC 2025 emphasized platforms for network and edge use, aligning with virtual RAN and cloud native telecom deployments that often lean on RDMA-capable fabrics. This strengthens adoption among communication service providers that need consistent low latency at a large scale.

Key Market Segments

By Deployment Mode

- On-premises

- Cloud-based

By Organization Size

- Large Enterprises

- Small and Medium-sized Enterprises (SMEs)

By Application

- High-Performance Computing (HPC)

- Artificial Intelligence & Machine Learning

- Big Data Analytics

- Financial Services & Trading

- Others

By End-User Industry

- IT & Telecommunications

- Banking, Financial Services, and Insurance (BFSI)

- Healthcare & Life Sciences

- Government & Defense

- Others

Emerging Trends

RDMA is expanding from high-performance computing into mainstream Ethernet environments through RoCEv2 and software-defined control planes. Large cloud operators are using RoCEv2 for storage traffic at scale, while hyperscalers are standardizing RDMA for AI and storage backends to support lower latency and more efficient data movement.

Long-distance RDMA acceleration is gaining attention, with specialized frameworks showing more than 30 times improvement for small message transfers over wide area networks compared with standard RDMA. Research is also exploring RDMA designs for machine learning, where controlled data loss or reordering may improve throughput in tolerant workloads.

Growth Factors

Growth is supported by disaggregated and cloud native architectures, where storage, memory, and compute are separated across networks. RDMA acceleration software is becoming important as enterprise data traffic rises and cloud data centers expand. Its role is also increasing in analytics, trading, and real-time decision systems.

The next stage of growth is linked to AI and edge computing. Demand is being supported by larger AI workloads, hyperscale data center expansion, real-time analytics, and edge infrastructure deployment. These use cases need ultra-low latency transport and CPU bypass, making RDMA-aware software more important across modern digital systems.

Market Dynamics

Drivers - Rising Low Latency Workloads

The market is driven by the rising need for faster data movement across AI clusters, distributed databases, storage platforms, and real-time analytics systems. RDMA acceleration software reduces network delay by allowing direct memory access between servers, which supports smoother workload performance.

Enterprises are adopting this software to improve throughput and reduce CPU involvement in data transfer. It is becoming important in workloads where even small delays can affect processing speed, service quality, or user experience across modern data centers.

For instance, in April 2025, NVIDIA highlighted GPUDirect RDMA support on Red Hat OpenShift AI to cut communication delays in distributed model training. By letting GPUs move data directly over InfiniBand or Ethernet without extra CPU hops, the stack helps AI teams handle latency-sensitive training workloads more efficiently inside large clusters.

Restraint - Integration Complexity

Integration complexity remains a key restraint because RDMA requires proper alignment between software, network cards, switches, firmware, and application layers. Many organizations operate mixed infrastructure, which makes deployment more difficult and increases the need for skilled technical teams.

RDMA also needs careful tuning for traffic control, packet handling, and workload compatibility. If the network is not configured correctly, performance gains may remain limited. This can slow adoption among enterprises with legacy systems or limited networking expertise.

For instance, in November 2025, the InfiniBand Trade Association released specification updates that expand features for InfiniBand and RoCE-based RDMA fabrics. While these enhancements improve performance and interoperability, they also show how quickly RDMA standards evolve, which can make integration and long-term maintenance challenging for operators without strong in-house networking skills.

Opportunities - Expansion in AI, Cloud, and Edge Workloads

Strong opportunities are emerging as AI, cloud, and edge workloads continue to expand. These environments depend on fast communication between compute, storage, and memory resources. RDMA acceleration software can support better workload movement, lower latency, and improved infrastructure efficiency.

Cloud providers and enterprises are also moving toward distributed and disaggregated architectures. This creates demand for software that can manage RDMA traffic across many nodes and locations. Edge workloads further increase the need for reliable low-latency data transfer.

For instance, in March 2025, Google Cloud introduced RoCEv2-capable compute instances such as A3 Ultra and A4, where each node has multiple RDMA-capable NICs for GPU-to-GPU traffic. These services target AI and ML jobs that need fast, lossless communication, creating more room for RDMA acceleration software in managed clouds.

Challenges - Data Privacy Concerns

Data privacy concerns remain a challenge as RDMA enables direct memory access across connected systems. While this improves performance, it also requires strict access controls, secure configuration, and strong monitoring to prevent unauthorized data exposure in shared or multi-tenant environments.

Enterprises must ensure that RDMA acceleration software works within internal security policies and compliance rules. Privacy risks may increase when sensitive workloads move across distributed infrastructure. This makes encryption, isolation, and governance important for wider adoption.

For instance, in October 2025, EFA release notes mention improvements in error handling, resource cleanup, and verification of queue pair numbers, reflecting AWS efforts to harden RDMA communication paths against subtle failures that could affect data integrity.

Key Players Analysis

One of the leading players in April 2026, AWS expanded its AI and HPC portfolio with new instances connected via ultra-low-latency fabrics to support large-scale model training. RDMA-style offload is central to these designs, allowing RDMA acceleration software stacks to move data directly between memory domains and improve utilisation of GPUs and custom accelerators in hyperscale environments.

Top Key Players in the Market

- NVIDIA Corporation

- Intel Corporation

- Microsoft Corporation

- Amazon Web Services, Inc.

- Google LLC

- IBM Corporation

- Hewlett Packard Enterprise Company (HPE)

- Dell Technologies, Inc.

- Broadcom, Inc.

- Cisco Systems, Inc.

- Fujitsu, Ltd.

- Huawei Technologies Co., Ltd.

- AMD (Advanced Micro Devices, Inc.)

- Lenovo Group, Ltd.

- Micron Technology, Inc.

- Others

Recent Developments

- In February 2026, NVIDIA deepened its data-center dominance as partners showcased GPUDirect RDMA-enabled AI storage and networking stacks optimised for Blackwell and Rubin GPUs. This ecosystem push focuses on ultra-low-latency access between GPUs and storage, a critical foundation for RDMA acceleration software layers that tune AI training and inference throughput at hyperscale.

- In April 2026, AWS expanded its AI and HPC portfolio with new instances connected via ultra-low-latency fabrics to support large-scale model training. RDMA-style offload is central to these designs, allowing RDMA acceleration software stacks to move data directly between memory domains and improve utilisation of GPUs and custom accelerators in hyperscale environments.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 731.5 Million |

| Forecast Revenue (2035) | USD 8,175.2 Million |

| CAGR (2026-2035) | 27.3% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Deployment Mode (On-premises, Cloud-based), By Organization Size (Large Enterprises, Small and Medium-sized Enterprises (SMEs)), By Application (High-Performance Computing (HPC), Artificial Intelligence & Machine Learning, Big Data Analytics, Financial Services & Trading, Others), By End-User Industry (IT & Telecommunications, Banking, Financial Services, and Insurance (BFSI), Healthcare & Life Sciences, Government & Defense, Others) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | NVIDIA Corporation, Intel Corporation, Microsoft Corporation, Amazon Web Services, Inc., Google LLC, IBM Corporation, Hewlett Packard Enterprise Company (HPE), Dell Technologies, Inc., Broadcom, Inc., Cisco Systems, Inc., Fujitsu, Ltd., Huawei Technologies Co., Ltd., AMD (Advanced Micro Devices, Inc.), Lenovo Group, Ltd., Micron Technology, Inc., Others |

| Customization Scope | Customization at the segment and region/country levels will be provided. Moreover, customization can be tailored to the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |