Quick Navigation

Report Overview

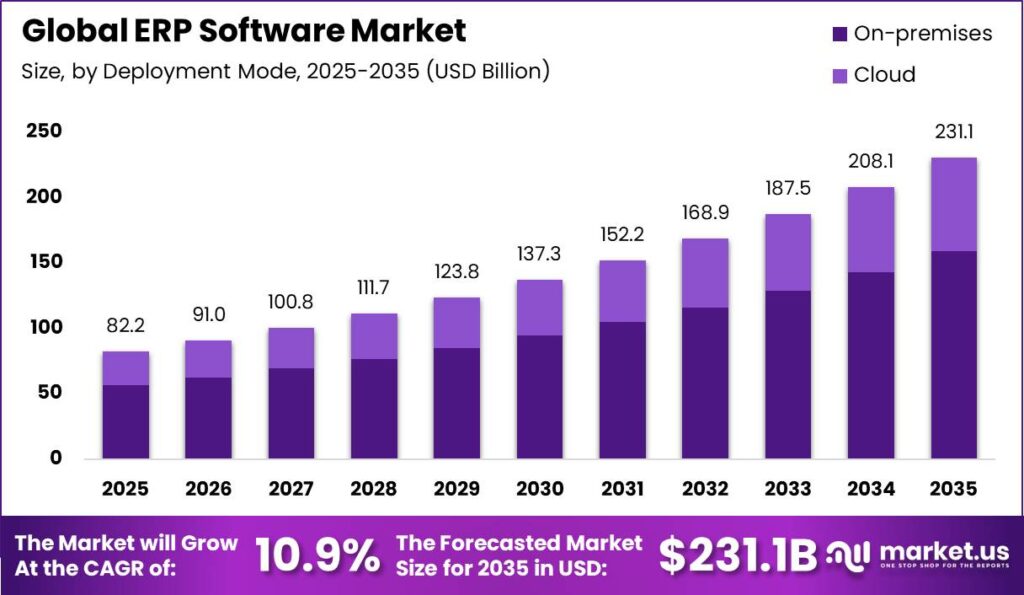

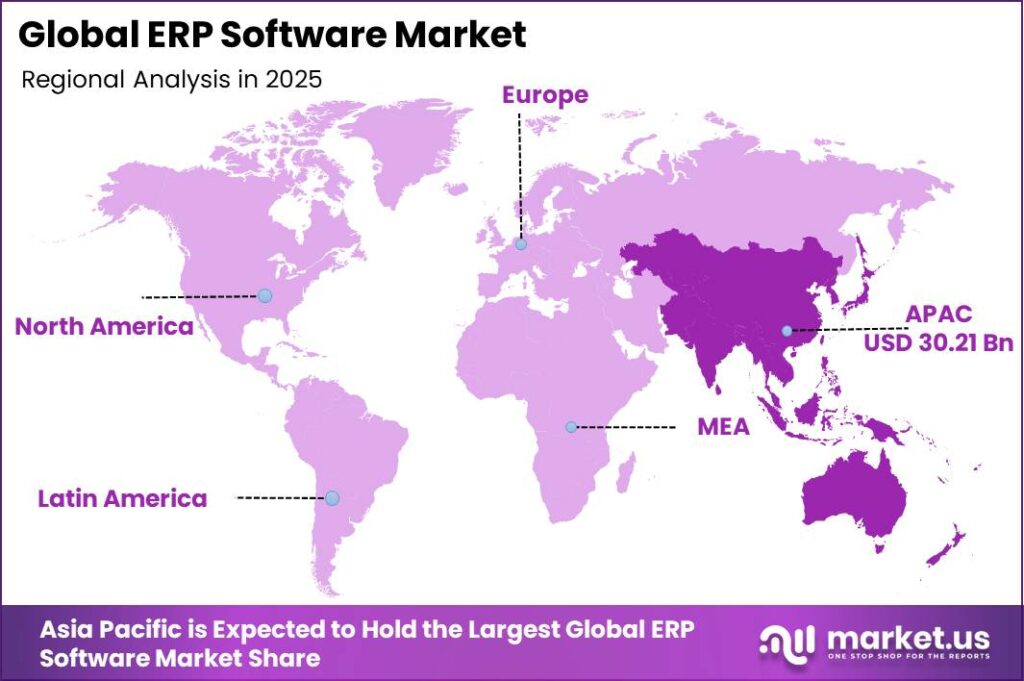

In 2025, the Global ERP software market was valued at USD 82.2 billion and is expected to grow at a CAGR of 10.9% from 2026 to 2035, reaching around USD 231.1 billion by 2035. The Asia-Pacific region holds a leading position, accounting for more than 36.78% of global ERP revenues, supported by rapid digital transformation, strong manufacturing and services industries, and increasing enterprise technology investments.

The expansion of the ERP market is closely connected with the global rise in software and digital technology spending. According to the World Intellectual Property Organization (WIPO), global software spending reached approximately USD 675 billion in 2024, increasing by nearly 50% from USD 454 billion in 2020. This growth reflects the shift of businesses from traditional processes toward software-based solutions that improve automation, efficiency, and decision-making.

As organizations allocate more budgets toward core business systems, ERP platforms are gaining importance because they integrate critical functions such as finance, supply chain, human resources, and customer operations into a unified system. This enables companies to improve productivity, access real-time data, and manage complex business processes more effectively.

Additionally, Asia-Pacific ICT spending is projected to reach around USD 1.4 trillion in 2025, showing strong investment in IT infrastructure and enterprise applications. As manufacturers automate operations, logistics companies implement real-time tracking, and governments modernize procurement and payroll systems, ERP adoption continues to rise, supporting steady market growth through 2035.

Key Takeaway

- The Global ERP Software Market was valued at USD 82.2 billion in 2025 and is projected to reach USD 231.1 billion by 2035, growing at a CAGR of 10.9% during 2026 to 2035.

- On-premises deployment dominates the market with a 68.78% share, driven by enterprise preference for control, security, and customized infrastructure.

- Finance function holds the largest share among ERP applications, accounting for 31.67% due to increasing demand for integrated financial management solutions.

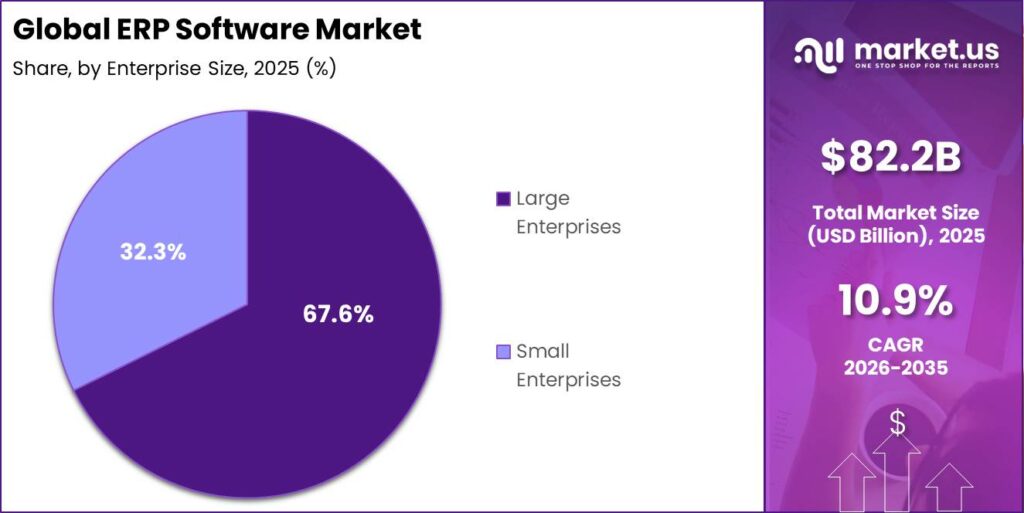

- Large enterprises represent the leading enterprise size segment with a 67.67% share, supported by complex operational requirements and higher technology investments.

- Retail vertical dominates ERP adoption with a 48.67% share, driven by the need for inventory management, supply chain optimization, and customer operations integration.

- Asia-Pacific leads the ERP Software Market with a 36.78% share, generating approximately USD 30.21 billion in market revenue.

Deployment Mode Analysis

The On-premises deployment mode, accounting for around 68.78% of ERP installations globally, remains dominant because it underpins the core systems of the world’s largest, asset-intensive industries. In 2024, global manufacturing value added reached about USD 16.8 trillion, representing a substantial share of world GDP and reflecting millions of factory-floor operations that depend on tightly coupled, low-latency ERP, MES, and production control systems hosted on local infrastructure for deterministic performance and uptime.

Medium- and high-tech manufacturing, including machinery and transport equipment, forms a large proportion of this value, further increasing reliance on highly customized, plant-specific ERP deployments. In parallel, banking institutions manage more than USD 180 trillion in assets worldwide, embedding ERP into highly regulated finance and risk platforms where data residency, encryption control, and audited change management favor in-house hosting.

Function Analysis

The Finance function segment, with a dominant 31.67% share of the ERP software market by function, leads adoption because it is directly tied to statutory financial reporting and tax compliance across virtually all formal enterprises worldwide.

Small and medium enterprises represent about 90% of all businesses and over 50% of employment globally, yet every one of these firms must maintain compliant accounts and file corporate taxes, which on average contribute 17.8% of total tax revenues across 131 jurisdictions according to OECD Corporate Tax Statistics 2025.

IFRS Accounting Standards are required or permitted in more than 140 jurisdictions, and IOSCO members regulate over 95% of the world’s securities markets, creating a unified global framework that demands granular, auditable financial data captured and consolidated through ERP finance modules.

Enterprise Size Analysis

Large Enterprises, which account for approximately 67.6% of ERP software revenues by enterprise size, dominate the market because they sit at the center of global value creation and trade. The world’s 500 largest corporations alone generated about 41 to 41.7 trillion USD in revenue in 2023 to 2024, equivalent to roughly one-third of global GDP and employing over 70 million people.

OECD and UNCTAD analyses show that multinational enterprises contribute around one-third of world output and GDP and about half of global exports, reflecting their outsized role in complex cross-border value chains. These firms orchestrate global production networks in which roughly 80% of world trade flows through value chains coordinated by transnational corporations.

Vertical Analysis

The Retail Vertical, accounting for 48.67% of ERP software demand, justifiably holds the dominant share of the ERP software market. Its scale alone creates a structural need for advanced ERP: the wholesale and retail trade sector employs about 420.5 million people worldwide, making it one of the largest global employers and a major generator of transactional and inventory data.

UNCTAD estimates total global e-commerce sales at roughly USD 26.7 trillion, with online retail sales growing three times faster than overall retail between 2017 and 2023, sharply increasing data, order, and fulfillment complexity for retailers.

ERP software directly addresses these pain points by consolidating point-of-sale, inventory, supply chain, and financials into a single, real-time system of record, which is economically critical in a low-margin sector where even a 1 to 2% productivity or shrinkage improvement materially lifts profit.

Key Market Segments

By Deployment Mode

- On-premises

- Cloud

By Function

- Finance

- HR

- Supply Chain

- Others

By Enterprise Size

- Large Enterprises

- Small Enterprises

By Vertical

- Retail

- Aerospace & Defense

- BFSI

- Manufacturing & Services

- Government

- Telecom

- Other Industry Verticals

Market Dynamics

Drivers

| Driver | (~) % Impact on CAGR | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cloud-First ERP Adoption & SaaS Model Proliferation | +2.8% | Global, led by North America, Western Europe, India, Southeast Asia | Short term (≤ 2 years) |

| Embedded AI, Predictive Analytics & Automation Integration | +2.2% | Global, with fastest uptake in North America, DACH, Japan | Short term (≤ 2 years) |

| Mandatory Government & Tax Compliance Digitization | +1.6% | India, EU, Latin America (Brazil, Mexico), Saudi Arabia | Short term (≤ 2 years) |

| Industry 4.0 & Smart Manufacturing Adoption | +1.2% | Germany, China, South Korea, United States, India | Medium term (2–4 years) |

| SME Digital Transformation & ERP Democratization | +1.0% | Asia-Pacific, Sub-Saharan Africa, Latin America, Eastern Europe | Medium term (2–4 years) |

| ESG Reporting & Sustainability Compliance Modules | +0.6% | EU, United Kingdom, Australia, Canada | Medium term (2–4 years) |

Cloud-First ERP Adoption & SaaS Model Proliferation

The shift from perpetual on-premise licensing to SaaS-based ERP delivery has become one of the most significant growth drivers in the ERP software market. Cloud ERP adoption is accelerating as organizations seek lower upfront costs, faster deployment, scalability, and reduced infrastructure requirements.

As of 2025, cloud ERP represents approximately 60–70% of new ERP deal activity globally, while India recorded 41% year-on-year growth in cloud ERP adoption. The global cloud ERP segment is expanding at nearly 20% annual growth, supported by increasing demand for subscription-based enterprise solutions.

For vendors, SaaS delivery improves revenue predictability through recurring ARR streams, higher upsell opportunities, and stronger customer retention. Cloud ERP implementations have become approximately 40% faster than traditional on-premise deployments, reducing adoption barriers for businesses.

Restraints

| Restraint | (~) % Impact on CAGR | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Total Cost of Ownership & Implementation Overruns | -1.8% | Global, most acute for SMEs in emerging markets | Short term (≤ 2 years) |

| Data Privacy Regulation & Cross-Border Data Sovereignty Constraints | -1.3% | EU (GDPR), India (DPDP Act 2025), China (PIPL), Brazil (LGPD) | Short term (≤ 2 years) |

| Enterprise Budget Freeze & Macro-Driven CapEx Austerity | -0.9% | North America, Western Europe, export-exposed Asia-Pacific economies | Short term (≤ 2 years) |

| Cybersecurity Breach Risk Blocking Cloud ERP Procurement | -0.8% | Global, heightened in BFSI, healthcare, government verticals | Medium term (2–4 years) |

| Concentration Risk from Oligopolistic Vendor Lock-In | -0.5% | Global, especially mid-market segments dominated by SAP, Oracle, Microsoft | Long term (≥ 4 years) |

High Total Cost of Ownership & Implementation Overruns

The high total cost of ownership (TCO) associated with ERP deployments remains a major barrier to adoption, especially among small and mid-sized enterprises that represent one of the fastest-growing demand segments. Although SaaS models have reduced upfront licensing costs, implementation expenses, customization requirements, and migration challenges continue to delay purchasing decisions.

A 2025 survey by an independent ERP advisory practice found that more than 50% of ERP implementations exceeded their original budgets, while over 60% surpassed planned go-live timelines. These delays can extend procurement cycles by approximately 6–18 months.

For SMEs operating with margins below 10–15%, unexpected implementation overruns can require additional approvals and delay ERP investments by a full fiscal year or longer. Vendors offering fixed-scope, fixed-fee deployment models within 90–120 days or outcome-based pricing are helping reduce this challenge, but these approaches are still not widely adopted across the ERP market.

Challenges

| Challenge | (~) % CAGR | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| Legacy System Integration Complexity | -1.5% | Global, concentrated in manufacturing-heavy economies (Germany, China, Japan, India) | Medium term (2–4 years) |

| ERP Talent & Implementation Skill Shortage | -1.1% | Global, most severe in US, UK, India, Southeast Asia | Long term (≥ 4 years) |

| Change Management & User Adoption Friction | -0.8% | Global, acute in large enterprises undergoing M&A or rapid growth | Medium term (2–4 years) |

| Multi-Vendor API & Ecosystem Interoperability | -0.6% | Global, particularly in heterogeneous IT stacks across retail, logistics, financial services | Medium term (2–4 years) |

| Data Quality & Master Data Governance Gaps | -0.5% | Global, heightened in rapidly scaling SMEs and post-merger integrations | Short term (≤ 2 years) |

| AI Governance & Hallucination Risk in Automated Workflows | -0.4% | Global, most acute in regulated verticals (BFSI, healthcare, public sector) | Long term (≥ 4 years) |

Legacy System Integration Complexity

The continued use of aging on-premise ERP systems and customized operational platforms across manufacturing, distribution, and process industries remains a major challenge for ERP market expansion. These legacy environments slow replacement decisions by increasing migration complexity, extending sales cycles, raising implementation costs, and creating higher post-deployment risks.

Legacy ERP systems often lack modern APIs, use outdated data structures, and contain extensive customizations that require significant re-engineering during migration. When organizations need to connect 5 or more legacy systems such as WMS, MES, payroll, CRM, and reporting tools, project timelines can increase by 30–50%, while data-cleaning activities may account for 15–25% of total implementation budgets.

For ERP vendors, complex migrations can extend deployment cycles to 9–18 months for mid-to-large enterprises, delaying revenue recognition and increasing implementation risks. Reducing this barrier requires investment in pre-built connectors and iPaaS-native adapters covering 40–60 common legacy ERP, WMS, and MES platforms, a capability expansion expected to require 2–4 years to significantly lower integration costs.

Opportunities

| Opportunity | (~) % Potential CAGR | Geographic Relevance | Execution Window |

|---|---|---|---|

| Vertical SaaS ERP for Untapped Industry Niches | +2.4% | Global, with concentrated opportunity in healthcare, agri-food, construction, education across Asia-Pacific & Latin America | Medium term (2–4 years) |

| Agentic AI & Autonomous Workflow Monetization Layer | +1.9% | Global, fastest uptake in North America, DACH, Singapore, UAE | Short term (≤ 2 years) |

| ERP Expansion into Emerging Market First-Time Buyers | +1.4% | South & Southeast Asia, Sub-Saharan Africa, MENA, Andean Latin America | Medium term (2–4 years) |

| Embedded Fintech & Payments Within ERP Ecosystems | +1.1% | India, Southeast Asia, Sub-Saharan Africa, Latin America | Medium term (2–4 years) |

| ERP-as-a-Platform for M&A Consolidation & Roll-Up Plays | +0.8% | North America, Western Europe, Australia | Long term (≥ 4 years) |

| Outcome-Based & Consumption Pricing Model Innovation | +0.6% | Global, most relevant for SME-focused vendors in price-sensitive markets | Short term (≤ 2 years) |

Vertical SaaS ERP for Untapped Industry Niches

The largest untapped opportunity in the ERP software market is the shift from generic horizontal ERP platforms toward purpose-built vertical SaaS ERP solutions. These platforms address industry-specific workflows that traditional ERP systems often fail to cover, especially in sectors still dependent on spreadsheets or fragmented point solutions.

In 2025, SMEs accounted for approximately 57–58% of vertical software market revenue, while adoption in sectors such as agri-food processing, construction, specialty healthcare, and education administration remained below 30% of the serviceable market. Vertical SaaS ERP solutions can achieve 20–35% higher gross margins than generic ERP platforms due to demand for industry-specific workflows, compliance, and reporting capabilities.

Vendors can capture this opportunity by developing industry-specific data models, compliance engines, and integrated ecosystems, including FSSAI traceability, NABH accreditation tracking, and RERA-linked project accounting. Companies establishing leadership in 2–3 vertical niches within 24–48 months could achieve higher retention rates, with vertical SaaS providers estimated to deliver 110–125% NRR compared with 95–105% for horizontal ERP platforms.

Geopolitical Impact Analysis

Geopolitical tensions are increasing ERP software deployment risks by disrupting global hardware, cloud infrastructure, and data centre supply chains. UNCTAD estimates that Suez Canal transits declined by 42% from peak levels, forcing longer shipping routes for ERP-related infrastructure components such as servers, storage, and networking equipment. These disruptions increased Asia-Europe shipping lead times by 10 to 14 days, delaying infrastructure expansion and large-scale ERP implementation projects.

The World Bank reported that the Drewry World Container Index remained 141% above pre-crisis levels in November 2024, while Red Sea-affected routes such as Shanghai-Rotterdam experienced freight rates around 230% higher than at the end of 2023.

These logistics cost increases raise the delivered cost of ERP-critical hardware, increasing capital expenditure for on-premises deployments and regional data centres supporting ERP SaaS platforms. IMF analysis further indicates that Suez trade volumes declined by approximately 50% year-on-year in early 2024, increasing the risk of delays in global ERP roll-outs.

Energy-related geopolitical risks are also affecting ERP cloud economics. The IEA estimates that data centres consumed around 415 TWh of electricity in 2024, representing 1.5% of global power demand, and expects consumption to more than double to 945 TWh by 2030 due to AI workloads and digital services. Rising energy demand increases exposure to power price volatility and can result in mid-single-digit increases in ERP cloud hosting operating costs in certain regions.

Regional Analysis

The Asia-Pacific ERP software market is experiencing strong growth, driven by rapid digital transformation across major economies, including China, India, Japan, and Southeast Asia. Increasing adoption of Industry 4.0, smart manufacturing, cloud technologies, and government-led digital initiatives is accelerating ERP implementation across industries.

The region accounts for approximately 36.78% of global ERP market revenues, with estimated revenues of around USD 30 to 33 billion. Supported by a high single-digit to low double-digit CAGR, Asia-Pacific remains the largest and one of the fastest-growing regional markets for ERP solutions.

Asia-Pacific’s leading position is supported by growing adoption of cloud and SaaS-based ERP platforms, particularly among SMEs in China and India. Rising automation across sectors such as retail, healthcare, and manufacturing is driving demand for integrated enterprise management solutions.

China contributes more than 30% of regional ERP revenues, while India is experiencing the fastest growth rate in the region, creating strong opportunities for both global ERP providers and local technology vendors. The market continues to evolve as organizations prioritize digital infrastructure, operational efficiency, and data-driven decision-making.

Key Regions and Countries

Asia-Pacific

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

The global ERP software market is highly competitive, with Tier-1 vendors such as Oracle, SAP, and Microsoft leading enterprise cloud ERP adoption, installed base, and revenue generation. Together, these companies capture a low-to-mid-teens share of the overall ERP software market, while the remaining market is distributed among specialized and regional providers.

Oracle remains one of the largest ERP vendors, supported by strong cloud ERP growth and enterprise adoption. In fiscal 2025, Oracle reported USD 57.4 billion in total revenue, including USD 44.0 billion from cloud services and license support. Its Fusion Cloud ERP and NetSuite Cloud ERP SaaS revenue each reached USD 1.0 billion in Q4 2025, growing 22% and 18% year over year, respectively.

Oracle’s cloud ERP business represents an estimated USD 8 to 9 billion annualized run rate, translating to approximately 6.5% to 6.6% share of global ERP software revenue. The company continues expanding its cloud ecosystem, with cloud revenue increasing 34% year over year to USD 8.0 billion in Q2 fiscal 2026, supported by OCI, multicloud capabilities, and AI-driven ERP solutions.

SAP continues to be a major ERP market leader, particularly among large enterprises through its S/4HANA Cloud platform. In FY 2025, SAP’s cloud revenue increased 23% year over year (26% in constant currency), while Cloud ERP Suite revenue grew 28% (32% in constant currency).

SAP reported EUR 5.13 billion in cloud revenue in Q2 2025, representing 24% year-over-year growth, while 86% of SAP income became predictable recurring revenue. The company is also expanding AI-based ERP capabilities, with Cloud ERP Suite and Business Technology Platform components growing 30% year over year, strengthening SAP’s position in intelligent enterprise applications.

Tier-2 players, including Workday, Infor, Epicor, and regional vendors such as Tally, Ramco, and Totvs, compete through industry-focused solutions, midmarket offerings, and localized capabilities. These companies generally hold low-single-digit global revenue shares but maintain stronger positions in specific segments such as HCM, manufacturing ERP, and emerging markets.

Top Key Players in the Market

- Epicor Software Corporation

- Hewlett-Packard Development Company, L.P.

- Infor Inc.

- IBM Corporation

- Microsoft

- NetSuite Inc.

- Oracle

- Sage Group, plc

- SAP SE

- Unit4

- Other Key Players

Recent Developments

- In March 2026, SAP SE signed a definitive agreement to acquire Reltio to strengthen AI-ready master data capabilities across SAP and non-SAP ERP environments. The acquisition is expected to close in Q2–Q3 2026. The integration of Reltio’s multi-domain master data management platform with SAP’s cloud ERP and data ecosystem will improve data quality, governance, and AI-driven enterprise use cases.

- In May 2026, SAP SE announced the acquisition of Prior Labs and committed more than EUR 1.0 billion over 4 years to establish a European frontier AI research lab focused on tabular foundation models for ERP and analytics workloads. Prior Labs will operate as an independent unit within SAP while aligning its research with SAP’s cloud ERP and data platforms. The investment is supported partly by SAP’s EUR 3.5 billion multi-tranche

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 82.2 Billion |

| Forecast Revenue (2035) | USD 231.1 Billion |

| CAGR (2026-2035) | 10.9% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Deployment (Cloud and On-premises), By Function (Finance, Supply Chain, HR, and Other Functions), By Enterprise Size (Small Enterprises, Medium Enterprises, and Large Enterprises), By Industry Verticals (Retail, Aerospace & Defense, BFSI, Manufacturing & Services, Government, Telecom, and Other Industry Verticals) |

| Regional Analysis | Asia-Pacific – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA |

| Competitive Landscape | Epicor Software Corporation, Hewlett-Packard Development Company, L.P., Infor Inc., IBM Corporation, Microsoft, NetSuite Inc., Oracle, Sage Group, plc, SAP SE, Unit4, Other Key Players |

| Customization Scope | Customization for segments and region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |