Quick Navigation

- Report Scope

- Key Takeaways

- Analysts’ Viewpoint

- Key Statistics

- Regional Analysis

- By Component

- By Application

- By Enterprise Size

- By End-User

- Key Market Segments

- Driving Factor

- Restraining Factor

- Growth Opportunity

- Challenging Factor

- Growth Factors

- Emerging Trends

- Business Benefits

- Key Player Analysis

- Recent Developments

- Report Scope

Report Scope

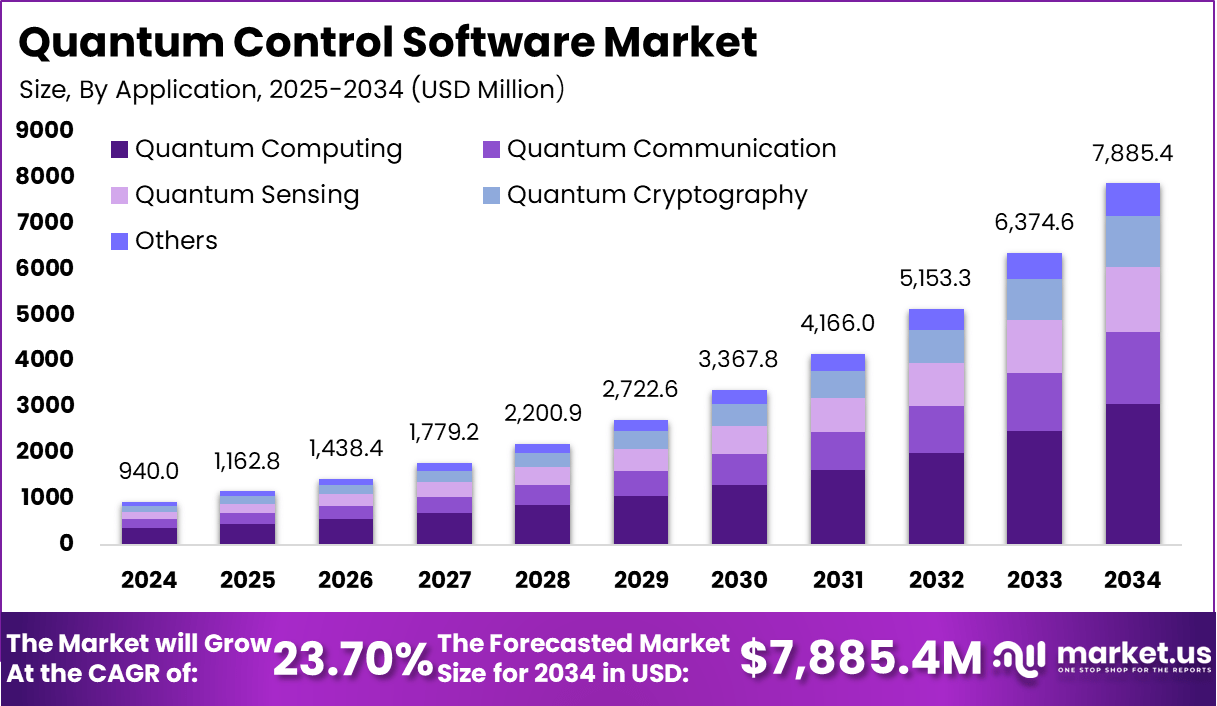

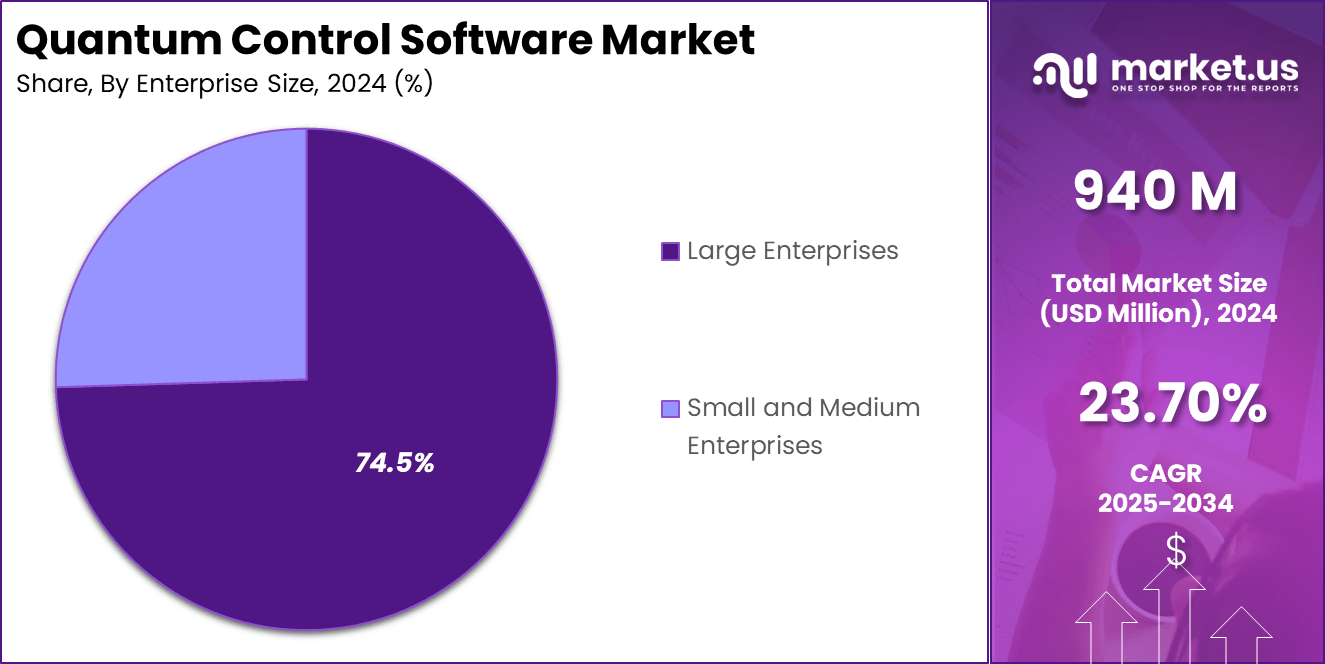

The Global Quantum Control Software Market is expected to be worth around USD 7885.4 Million by 2034, up from USD 940 Million in 2024. It is expected to grow at a CAGR of 23.70% from 2025 to 2034.

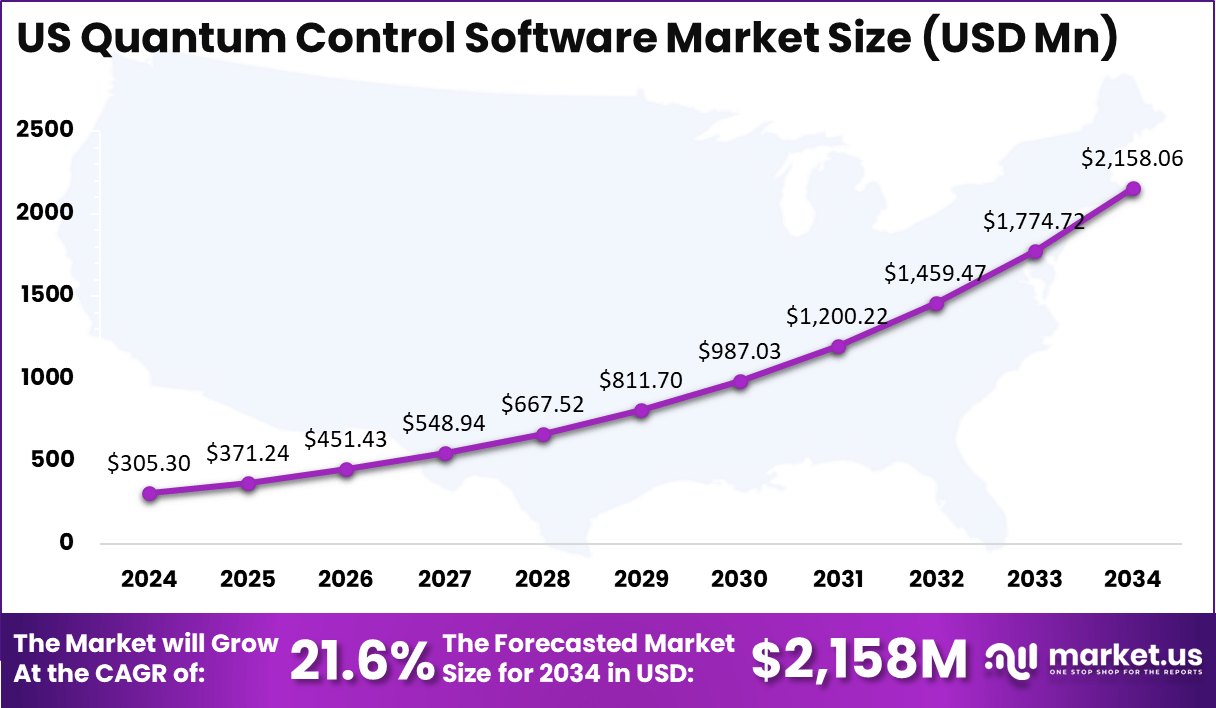

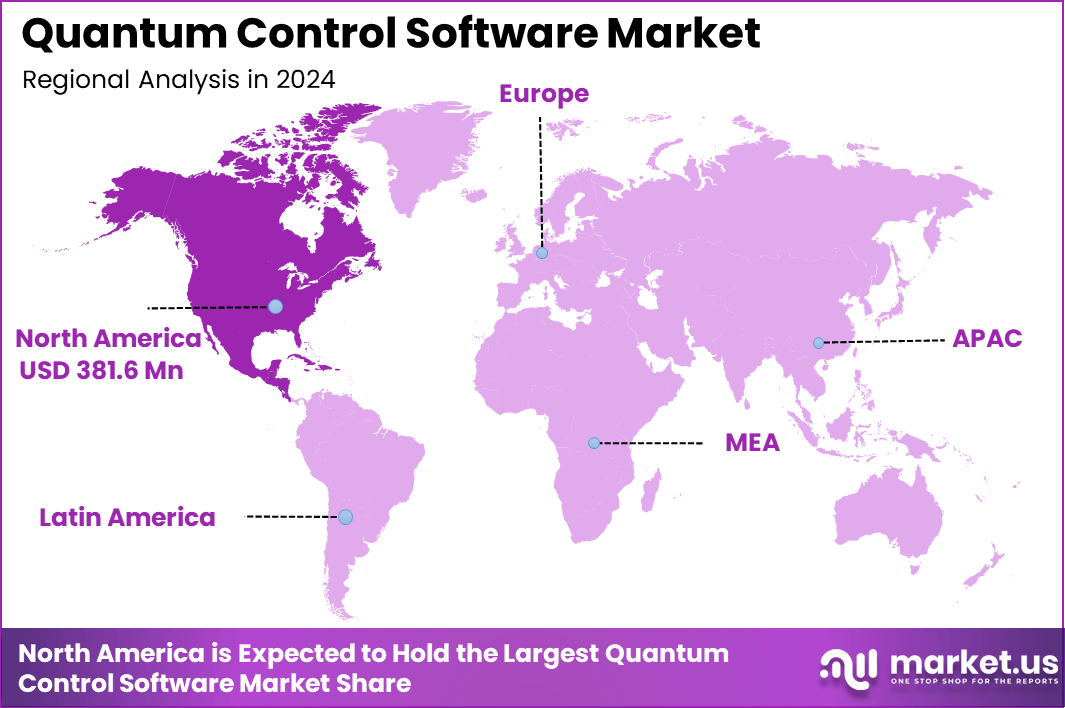

In 2024, North America held a dominant market position, capturing over a 40.6% share and earning USD 381.6 Million in revenue. Further, the United States dominates the market by USD 305.3 Million, steadily holding a strong position with a CAGR of 21.6%.

The quantum control software market is experiencing significant growth, driven by the increasing interest and investment in quantum technologies. Quantum control software is crucial in managing and manipulating quantum systems, which are fundamental to advancing quantum computing.

The primary factors fueling the growth of the quantum control software market include substantial investments in quantum research and development, advancements in quantum hardware, and the increasing recognition of quantum computing’s potential across various industries. Major technology companies such as IBM, Google, and Microsoft are actively developing quantum processors and software platforms, which in turn drive the demand for sophisticated quantum control solutions.

There is a growing demand for quantum control software from sectors like finance, pharmaceuticals, and materials science, where quantum computing holds promise for solving complex problems. For instance, IBM’s quantum systems are being utilized by clients like Wells Fargo to enhance AI capabilities, and by E.ON for weather risk management. This trend indicates a broadening application base and increasing interest in quantum solutions.

Key Takeaways

- Market Growth: The Quantum Control Software Market is expected to grow from USD 940 million in 2024 to USD 7.88 billion by 2034, at a CAGR of 23.70%.

- By Component: Software accounts for 64.3% of the market share in the Quantum Control Software Market.

- By Application: Quantum Computing represents 38.9% of the market demand in the Quantum Control Software Market.

- By Enterprise Size: Large Enterprises dominate the market, holding 74.5% of the market share in the Quantum Control Software Market.

- By End-User: The BFSI (Banking, Financial Services, and Insurance) sector is the largest end-user, contributing 32.7% to the Quantum Control Software Market.

- Geographic Insights: North America holds 40.6% of the global market share in the Quantum Control Software Market.

- U.S. Market: The U.S. market is valued at USD 305.3 million and is growing at a CAGR of 21.6% in the Quantum Control Software Market.

Analysts’ Viewpoint

The market presents numerous opportunities, particularly in developing software that can optimize quantum algorithms for specific applications. Companies like Quantinuum are offering platforms such as InQuanto for computational chemistry, demonstrating the potential of quantum software to revolutionize traditional processes. Additionally, the integration of quantum computing with artificial intelligence opens new avenues for data analysis and problem-solving across various domains.

Technological progress in quantum control software is pivotal for the scalability and reliability of quantum systems. Recent developments include modular software architectures that enhance real-time control and reduce execution overheads, as demonstrated by research in modular software for quantum control systems.

Moreover, advancements in noise suppression techniques are crucial for improving the performance of quantum computers, with software tools playing a vital role in mitigating errors and enhancing system stability. These advancements are essential for the practical deployment of quantum technologies in real-world applications.

Key Statistics

User Base

- Total Users: Over 22,000 users globally.

- Customer Base: Supports approximately 1,700 aviation companies.

- Active Users per Day: Around 15,000 users interact with the system daily.

Implementation and Support

- Technical Support: Offers 24/7 worldwide support for implementation, training, and technical issues.

- Service Maintenance Agreement (SMA): Required for accessing certain services like Data Services, with an average cost of $5,000 per year.

- Training Sessions: Conducts over 500 training sessions annually.

Data Management

- Import/Export Capabilities: Supports importing and exporting data using custom scripts for efficient data management.

- Data Services: Provides customized forms, reports, and data extracts for diverse needs such as IRS audits and custom reports.

- Data Volume: Handles over 10 million transactions per month.

Quantitative Data

- Revenue of Key Customers: Companies like Honeywell Aerospace have revenues of $35.50 billion.

- Employee Base of Key Customers: Companies like Honeywell Aerospace employ around 99,000 people.

- Average Customer Revenue: $10 million annually.

Regional Analysis

United States Market Size

In North America, the United States dominates the Quantum Control Software Market with a market size of USD 305.3 million, holding a strong position steadily with a strong CAGR of 21.6%. The United States has established itself as a leader in the quantum computing sector, owing to substantial investments in research and development and a thriving tech ecosystem.

With the presence of major technology companies and research institutions, the U.S. continues to drive innovation in quantum technologies, including quantum control software. The market is supported by increasing demand from industries such as finance, pharmaceuticals, and materials science, which are seeking quantum solutions to tackle complex computational challenges.

The U.S. market’s growth is fueled by the growing adoption of quantum computing applications and the need for efficient software solutions to control and manage quantum systems. As organizations look to leverage the potential of quantum computing, the demand for advanced quantum control software continues to rise, further solidifying the United States’ dominant role in the market.

Overall, the Quantum Control Software Market in North America, especially in the United States, remains robust, with strong growth prospects driven by technological advancements, industry demand, and continuous investments in quantum innovation.

North America Market Size

In 2024, North America held a dominant market position in the Quantum Control Software Market, capturing more than 40.6% of the global market share, amounting to USD 381.6 million in revenue. This region’s leadership can be attributed to its advanced technological infrastructure, strong investment in research and development, and the presence of leading companies in the quantum computing space.

The United States, in particular, plays a pivotal role, with major companies such as IBM, Google, and Microsoft driving innovation and investments in quantum technologies. The growing demand from various industries, including finance, healthcare, and manufacturing, for quantum solutions is further propelling the adoption of quantum control software in the region.

In Europe, the quantum control software market is experiencing significant growth, although it lags behind North America. The region is making substantial strides with increasing public and private sector investments aimed at developing quantum computing infrastructure. Key European countries, such as Germany, the United Kingdom, and France, are spearheading these advancements, supported by initiatives like the European Quantum Flagship Program. These efforts aim to boost quantum research and accelerate the commercialization of quantum technologies, driving demand for quantum control software.

In the Asia-Pacific (APAC) region, there is a growing emphasis on quantum computing, primarily driven by countries like China, Japan, and India. China, with its aggressive push toward becoming a global leader in quantum technologies, is expected to contribute significantly to the market’s expansion. The demand for quantum control software is expected to grow as these countries invest heavily in both research and commercializing quantum systems, attracting major international collaborations and partnerships.

Latin America, the Middle East, and Africa represent emerging markets in the quantum control software industry. While these regions currently hold a smaller share of the market, the growing interest in quantum computing is evident, with an increasing number of startups and research initiatives in countries such as Brazil and South Africa. As governments and industries in these regions begin to realize the potential of quantum technologies, the demand for quantum control software is expected to rise gradually, contributing to the overall market growth in the coming years.

By Component

In 2024, the Software segment held a dominant market position in the Quantum Control Software Market, capturing more than 64.3% of the total market share. This dominance is primarily due to the increasing adoption of quantum computing applications across various industries, where software solutions are critical in managing and controlling quantum systems.

Quantum control software enables the precise manipulation of quantum states, ensuring that quantum computers operate efficiently and accurately. As quantum computing technology continues to evolve, the need for sophisticated software platforms that can integrate seamlessly with quantum hardware is becoming more pronounced.

The growing focus on quantum applications in sectors like finance, healthcare, and materials science is fueling the demand for robust software solutions. Moreover, software solutions allow for greater scalability, flexibility, and efficiency in managing quantum systems compared to hardware components, which are still in their nascent stages.

With the increasing reliance on software to optimize quantum algorithms and manage complex quantum computations, the Software segment is expected to maintain its leadership position in the market in the coming years.

By Application

In 2024, the Quantum Computing segment held a dominant market position, capturing more than 38.9% of the total market share. This dominance is driven by the rapid advancements in quantum computing technologies and their increasing application across various industries.

Quantum computing has the potential to solve complex computational problems that classical computers struggle with, such as optimization, cryptography, and large-scale simulations. As industries like finance, healthcare, and pharmaceuticals begin to explore quantum solutions, the demand for quantum control software to manage and optimize quantum algorithms becomes essential.

The significant investment from major technology companies, research institutions, and government entities is further fueling the growth of the quantum computing segment. Quantum computers require precise control to maintain their quantum states and perform computations, which is where quantum control software plays a crucial role.

Given the broad application potential and the ongoing development of quantum hardware, the Quantum Computing segment is expected to continue leading the market in the coming years, outpacing other quantum technologies such as quantum communication and sensing.

By Enterprise Size

In 2024, the Large Enterprises segment held a dominant market position, capturing more than 74.5% of the total market share in the Quantum Control Software Market. This dominance is primarily due to the substantial resources and technological infrastructure that large enterprises can dedicate to adopting advanced quantum technologies.

These enterprises, particularly in industries such as finance, healthcare, and telecommunications, are increasingly exploring quantum computing and other quantum technologies to address complex challenges and gain a competitive edge.

Large enterprises are better equipped to invest in the expensive infrastructure needed for quantum systems and the associated software solutions. They also benefit from having dedicated research and development teams that can support the deployment and optimization of quantum control software.

The scalability, reliability, and integration capabilities required by large organizations to manage quantum systems further drive their preference for these software solutions. As quantum technologies continue to mature, large enterprises are expected to remain the primary drivers of growth in the quantum control software market, with their extensive adoption continuing to outpace smaller businesses in the coming years.

By End-User

In 2024, the BFSI (Banking, Financial Services, and Insurance) segment held a dominant market position, capturing more than 32.7% of the total market share in the Quantum Control Software Market. This dominance is primarily driven by the increasing demand for advanced computational capabilities in the BFSI sector.

Financial institutions are increasingly turning to quantum computing to solve complex financial models, optimize portfolios, and enhance risk management. The ability to perform ultra-fast calculations and process vast amounts of data in quantum systems makes quantum control software essential for managing these applications.

Moreover, the BFSI sector is highly competitive and risk-sensitive, which drives the need for innovative technologies like quantum computing to gain a strategic advantage. Quantum control software ensures that quantum systems perform reliably, supporting high-stakes financial transactions and secure data processing.

As more financial services companies explore the potential of quantum technologies for encryption and fraud detection, the demand for quantum control software within the BFSI sector is expected to continue to grow, maintaining its leadership in the market.

Key Market Segments

By Component

- Software

- Deployment Mode

- On-Premises

- Services

- Professional Services

- Managed Services

By Application

- Quantum Computing

- Quantum Communication

- Quantum Sensing

- Quantum Cryptography

- Others

By Enterprise Size

- Small and Medium Enterprises

- Large Enterprises

By End-User

- BFSI

- Healthcare

- IT and Telecommunications

- Government

- Aerospace and Defense

- Others

Driving Factor

Significant Investments in Quantum Computing Research and Development

A pivotal driver propelling the growth of the Quantum Control Software Market is the substantial investments channeled into quantum computing research and development (R&D). Both public and private sectors are recognizing the transformative potential of quantum technologies, leading to increased funding and strategic initiatives aimed at harnessing their capabilities.

Governments worldwide are actively investing in quantum technologies to secure a competitive edge and foster innovation. For instance, the Canadian government announced a CAD 40 million (approximately USD 32 million) investment to develop the world’s first photonic-based, fault-tolerant quantum computer. This initiative underscores the strategic importance attributed to quantum advancements and aims to position Canada as a leader in the quantum computing arena.

The private sector is equally proactive, with leading technology companies and startups allocating significant resources to quantum computing R&D. Companies like IBM, Google, and Microsoft are not only developing quantum hardware but are also investing in software solutions to control and optimize quantum systems. These investments are crucial for overcoming existing technological challenges and unlocking the practical applications of quantum computing.

Restraining Factor

High Development Costs and Technical Challenges

Despite the promising potential, the Quantum Control Software Market faces significant restraints, primarily stemming from high development costs and technical challenges associated with quantum computing. The complexity inherent in developing quantum technologies presents both financial and operational hurdles.

Developing quantum control software necessitates considerable investment in R&D to address the unique challenges posed by quantum systems. The intricate nature of quantum mechanics requires specialized expertise and resources, making it a costly endeavor. This financial barrier can limit the participation of smaller firms and startups, concentrating expertise and resources among a few large entities.

Quantum systems are highly sensitive to environmental factors, leading to issues like qubit instability and error rates. Developing software that can effectively manage and mitigate these challenges is technically demanding. The need for error correction and maintaining coherence in quantum states adds layers of complexity to software development, slowing progress and increasing costs.

Growth Opportunity

Emergence of Cloud-Based Quantum Computing Services

A significant growth opportunity in the Quantum Control Software Market lies in the emergence of cloud-based quantum computing services, which democratize access to quantum resources and foster broader adoption. This development is transforming how organizations and individuals engage with quantum technologies.

Cloud-based quantum computing platforms allow users to access quantum processors remotely, eliminating the need for substantial upfront investments in quantum hardware. This accessibility enables a wide range of users, from academic researchers to enterprises, to experiment with and develop quantum applications. Scalability is another advantage, as cloud platforms can adjust resources based on demand, accommodating varying workloads efficiently.

By leveraging cloud services, organizations can engage in quantum software development without bearing the high costs associated with maintaining on-premises quantum hardware. This cost-effective approach encourages innovation and experimentation, leading to the discovery of novel applications and solutions. It lowers the entry barrier for smaller enterprises and startups, fostering a more diverse and dynamic quantum ecosystem.

Challenging Factor

Ensuring Security Amidst Quantum Advancements

As quantum technologies advance, ensuring security becomes a paramount challenge, particularly concerning data protection and encryption. The potential of quantum computing to break current cryptographic systems necessitates urgent attention to developing quantum-resistant security measures.

Quantum computing poses a potential threat to existing cryptographic systems. Quantum algorithms, such as Shor’s algorithm, can efficiently factor large numbers, undermining the security of widely used encryption methods like RSA. This necessitates the development of quantum-resistant cryptographic techniques to safeguard sensitive information.

The ability of quantum systems to process vast amounts of data rapidly raises concerns about data privacy. Ensuring that quantum technologies do not inadvertently expose personal or confidential information is a critical challenge that requires robust security frameworks. Protecting data against quantum-enabled attacks is essential to maintain trust and integrity in digital systems. This transition is crucial to ensure the continued confidentiality and integrity of data in the quantum computing era.

Growth Factors

Strategic Investments and Technological Advancements

The Quantum Control Software Market is experiencing robust growth, propelled by strategic investments and significant technological advancements. Advancements in quantum algorithms and hardware are enhancing the capabilities of quantum control software.

The integration of machine learning and reinforcement learning techniques is revolutionizing the management of quantum systems, leading to more efficient and reliable operations. Both public and private sectors are heavily investing in quantum technologies. These investments are fueling the development of quantum control software, essential for managing and optimizing quantum systems.

Emerging Trends

Cloud-Based Quantum Services and Industry Adoption

Cloud platforms are democratizing access to quantum computing resources. This model allows users to leverage quantum capabilities without significant upfront investments in hardware, fostering broader experimentation and development. Major players are offering cloud-based quantum services, enhancing accessibility and scalability.

Industries such as finance, pharmaceuticals, and manufacturing are increasingly adopting quantum technologies to solve complex problems. For example, SAP is exploring quantum computing to enhance supply chain management, aiming to reduce simulation times from weeks to hours. This trend signifies a shift towards integrating quantum solutions for operational optimization.

Business Benefits

Enhanced Computational Capabilities and Competitive Advantage

Quantum computing enables the processing of complex calculations at unprecedented speeds. This capability is particularly beneficial in sectors like pharmaceuticals for drug discovery, where simulating molecular interactions can be computationally intensive. Quantum control software facilitates these complex simulations, accelerating research and development processes.

Early adoption of quantum technologies positions businesses as leaders in innovation. Companies investing in quantum solutions can tackle problems previously deemed intractable, opening new avenues for products and services. This proactive approach not only enhances operational efficiency but also establishes a strong market presence in emerging technological domains.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherlands

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Thailand

- Vietnam

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Player Analysis

IBM has significantly advanced its quantum computing capabilities through strategic product developments. In November 2024, the company unveiled IBM Quantum Heron, its most advanced quantum processor to date. This processor enhances the execution of complex quantum circuits, supporting up to 5,000 two-qubit gate operations. This advancement facilitates deeper exploration into quantum applications across various scientific domains, including materials science and chemistry.

Microsoft has actively expanded its quantum computing portfolio, notably through partnerships and product integrations. In March 2023, Microsoft added Pasqal’s neutral-atom processors to its Azure Quantum cloud computing platform, enhancing its quantum services offerings. Additionally, in December 2021, Microsoft integrated Rigetti Computing’s quantum technology into Azure Quantum, broadening its range of quantum solutions available to users.

Google has made significant strides in quantum computing with the introduction of its quantum chip, Willow. In December 2024, Google unveiled Willow, a chip capable of solving complex tasks in minutes, tasks that would take traditional supercomputers an impractical amount of time. This development marks a substantial advancement in quantum error correction and positions Google as a leader in the pursuit of practical quantum computing solutions.

Top Key Players in the Market

- IBM Corporation

- Microsoft Corporation

- Google LLC

- Rigetti Computing

- D-Wave Systems Inc.

- Honeywell International Inc.

- Intel Corporation

- Quantum Computing Inc.

- Atos SE

- Cambridge Quantum Computing Ltd.

- IonQ Inc.

- QC Ware Corp.

- Xanadu Quantum Technologies Inc.

- Zapata Computing Inc.

- 1QBit Information Technologies Inc.

- Q-CTRL Pty Ltd.

- ColdQuanta, Inc.

- Aliro Technologies, Inc.

- Quantum Machines

- Pasqal SAS

- Others

Recent Developments

- In 2024, IBM launched its Quantum Heron processor, enhancing the execution of complex quantum circuits and advancing quantum applications in various scientific domains.

- In 2024, Microsoft integrated Pasqal’s neutral-atom processors into its Azure Quantum platform, expanding its quantum computing capabilities for cloud-based services.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 940 Million |

| Forecast Revenue (2034) | USD 7885.4 Million |

| CAGR (2025-2034) | 23.70% |

| Largest Market | North America |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Component (Software, [Deployment Mode, On-Premises], Services [Professional Services, Managed Services]), By Application (Quantum Computing, Quantum Communication, Quantum Sensing, Quantum Cryptography, Others), By Enterprise Size (Small and Medium Enterprises, Large Enterprises), By End-User (BFSI, Healthcare, IT and Telecommunications, Government, Aerospace and Defense, Others) |

| Regional Analysis | North America (US, Canada), Europe (Germany, UK, Spain, Austria, Rest of Europe), Asia-Pacific (China, Japan, South Korea, India, Australia, Thailand, Rest of Asia-Pacific), Latin America (Brazil), Middle East & Africa(South Africa, Saudi Arabia, United Arab Emirates) |

| Competitive Landscape | IBM Corporation, Microsoft Corporation, Google LLC, Rigetti Computing, D-Wave Systems Inc., Honeywell International Inc., Intel Corporation, Quantum Computing Inc., Atos SE, Cambridge Quantum Computing Ltd., IonQ Inc., QC Ware Corp., Xanadu Quantum Technologies Inc., Zapata Computing Inc., 1QBit Information Technologies Inc., Q-CTRL Pty Ltd., ColdQuanta, Inc., Aliro Technologies, Inc., Quantum Machines, Pasqal SAS, Others |

| Customization Scope | We will provide customization for segments and at the region/country level. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |