Quick Navigation

Report Overview

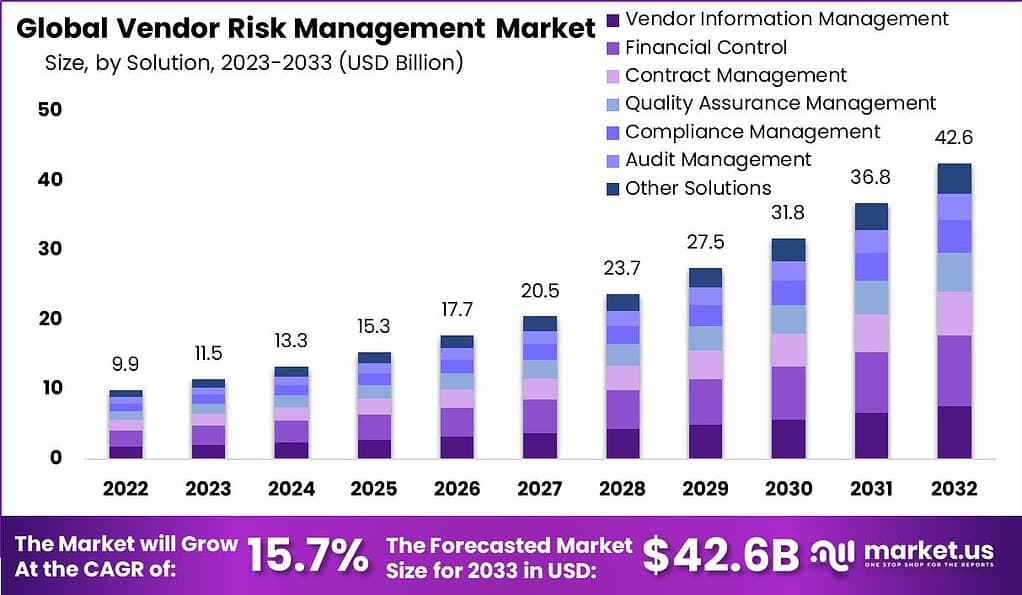

The Global Vendor Risk Management Market size is expected to be worth around USD 42.6 Billion By 2032, from USD 11.5 Billion in 2023, growing at a CAGR of 15.7% during the forecast period from 2024 to 2033.

Vendor Risk Management (VRM) is a crucial process that organizations employ to assess and mitigate risks associated with their third-party vendors and suppliers. In today’s interconnected business landscape, companies often rely on a network of vendors to deliver products, services, and critical support. However, this dependence on external parties exposes organizations to various risks, such as data breaches, compliance issues, operational disruptions, and reputational damage.

The VRM market has experienced significant growth in recent years due to several key factors. Firstly, the increasing complexity and interdependence of business ecosystems have amplified the need for robust risk management practices. As organizations expand their operations and engage with numerous vendors, the potential risks and vulnerabilities multiply. Consequently, companies recognize the importance of implementing effective VRM solutions to safeguard their operations and protect sensitive information.

Secondly, the escalating frequency and severity of cyber threats have propelled the demand for comprehensive VRM solutions. With the rise of sophisticated hacking techniques and data breaches, organizations must ensure that their vendors maintain adequate security measures to protect shared data and systems. Integrating VRM into the vendor selection and monitoring processes helps identify potential vulnerabilities and enforce necessary security controls.

Furthermore, regulatory compliance requirements have become more stringent, compelling organizations to establish rigorous risk management frameworks. Compliance standards, such as the General Data Protection Regulation (GDPR) and the California Consumer Privacy Act (CCPA), impose legal obligations on organizations to ensure that their vendors adhere to specific data protection and privacy requirements. VRM enables companies to assess vendor compliance and mitigate the risk of non-compliance penalties and legal repercussions.

Despite the growth opportunities, the VRM market also faces challenges. One significant obstacle is the lack of standardized frameworks and methodologies for assessing vendor risk. Each organization may have unique risk criteria and evaluation processes, making it difficult to establish consistent benchmarks. Additionally, the dynamic nature of vendor relationships and the evolving risk landscape require continuous monitoring and updating of risk profiles, which can be resource-intensive and time-consuming.

However, these challenges present opportunities for innovation and advancement in the VRM market. Technology solutions, such as artificial intelligence and machine learning, can automate and streamline the vendor risk assessment process, enabling organizations to scale their VRM efforts effectively. The emergence of specialized VRM platforms and tools provides organizations with comprehensive risk visibility, enabling them to make informed decisions about vendor selection, contract negotiation, and ongoing monitoring.

For instance, In July 2023, AuditBoard launched AuditBoard ITRM, a new IT risk management solution tailored for CISOs and their teams. Designed to enhance collaboration across organizational functions, it streamlines the identification and classification of IT systems, expedites business impact assessments, and aids in the remediation of issues. This launch highlights AuditBoard’s focus on advancing IT security and risk management processes.

Key Takeaways

- The Global Vendor Risk Management Market is projected to reach approximately USD 42.6 Billion by 2032, up from USD 11.5 Billion in 2023, with a compound annual growth rate (CAGR) of 15.7% during the forecast period from 2024 to 2033.

- In 2022, the Financial Control segment established a leading role in the Vendor Risk Management market, holding a significant market share of 23.7%.

- The Cloud-Based deployment option dominated the Vendor Risk Management Market in 2022, securing over 88.2% of the market share.

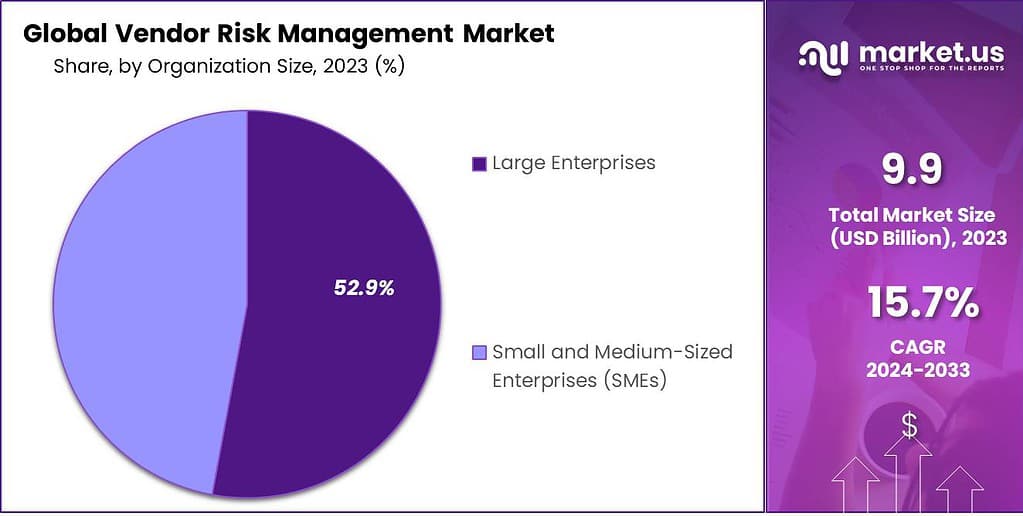

- Regarding enterprise size, Large Enterprises maintained a dominant position in the Vendor Risk Management Market in 2022, comprising more than 52.9% of the market.

- In the industry segmentation, the Manufacturing sector achieved a leading position in the Vendor Risk Management Market in 2022, with a market share exceeding 22.5%.

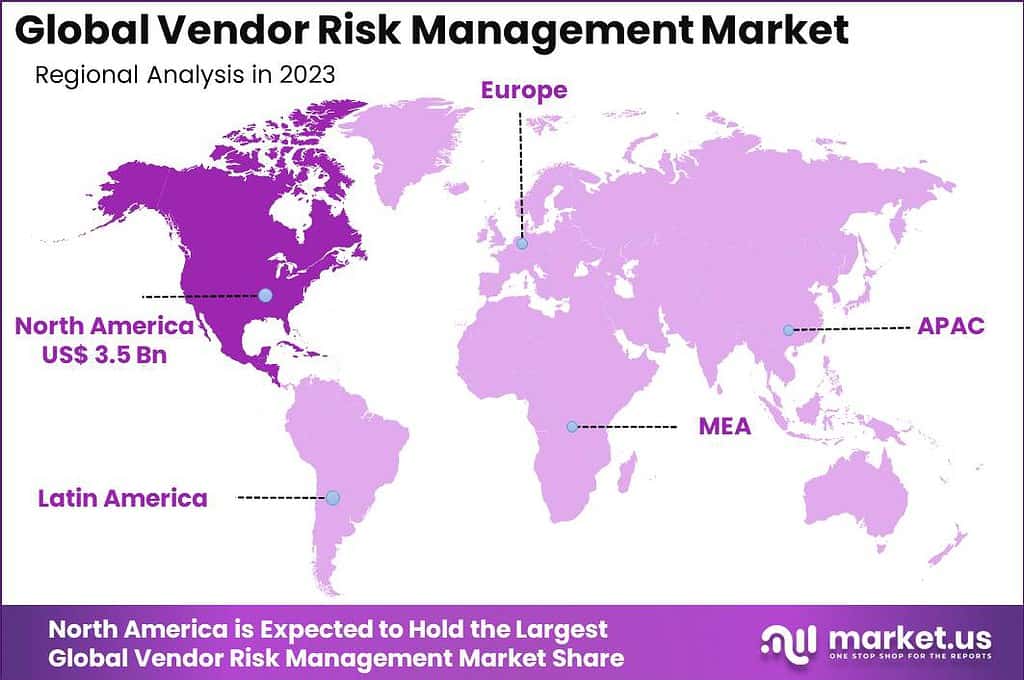

- In 2022, North America held a dominant market position, capturing more than a 36.1% share.

Solution Analysis

In 2022, the Financial Control segment secured a dominant position in the Vendor Risk Management market, commanding a share exceeding 23.7%. This is due to the growing need of companies to be aware of and manage the financial risks associated with their suppliers, driven by the increasing regulations and the complexities nature of supply chains across the globe. Financial Control solutions play a crucial role in ensuring financial stability and the reliability of vendors protecting companies from potential financial losses.

the Vendor Information Management segment is gaining momentum, providing organizations with a comprehensive platform to collect, manage, and analyze crucial data about their vendors, covering performance metrics and compliance status. The growth of this segment is driven by the increasing demand for transparency and efficiency in vendor interactions and operations.

Another crucial segment is Contract Management, which streamlines and automates the entire lifecycle of vendor contracts. It has become indispensable due to the growing complexity of contracts and the imperative for stringent compliance with regulatory standards. Quality Assurance Management comes next, ensuring that vendor-supplied products and services meet the required standards and specifications, critical for maintaining customer trust and a competitive edge.

Moreover, the Compliance Management segment addresses the growing need for vendors to adhere to various industry and government regulations. Its expansion is fueled by the rising legal and operational risks associated with non-compliance. Audit Management solutions, offering tools for regular and systematic reviews of vendor performance and compliance, are also essential, especially in industries where vendors directly impact product quality and safety.

Deployment Mode

In 2022, the Cloud-Based segment held a dominant market position in the Vendor Risk Management Market, capturing more than an 88.2% share. This significant majority is attributed to the growing adoption of cloud services across industries seeking scalable, flexible, and cost-effective solutions for managing vendor risks.

Cloud deployment offers numerous advantages, including real-time data access, reduced operational costs, and enhanced collaborative efficiencies, which are particularly beneficial for organizations aiming to streamline their vendor risk management processes. Additionally, the ability to rapidly update and deploy new features without substantial downtime is a critical factor driving the preference for cloud-based solutions.

On the other hand, the On-premises segment, while smaller, continues to be relevant for organizations prioritizing data control and security, particularly in sectors like finance and healthcare where regulatory compliance is non-negotiable. Despite a smaller market share, this segment benefits from firms that require customized solutions and those hesitant to migrate sensitive data to the cloud. However, with continuous improvements in cloud security and an increasing number of companies becoming comfortable with cloud services, the on-premises segment may see a gradual decline in its market share unless it evolves with more hybrid and secure solutions.

Overall, the Vendor Risk Management Market is experiencing a dynamic shift towards cloud-based solutions, driven by the demand for more efficient, scalable, and cost-effective risk management tools. As technology advances and the emphasis on cybersecurity intensifies, both segments are expected to innovate and adapt, offering more sophisticated and secure options for organizations looking to mitigate vendor-related risks.

Organization Size

In 2022, the Large Enterprises segment held a dominant market position in the Vendor Risk Management Market, capturing more than a 52.9% share. This prominence is primarily due to the extensive networks of vendors and partners that large organizations manage, coupled with the complexity and scale of their operations that necessitate robust risk management solutions.

Large enterprises often face heightened regulatory scrutiny and a more significant impact from potential vendor-related disruptions, driving the need for comprehensive and sophisticated vendor risk management tools. These organizations typically have the resources to invest in advanced solutions that provide in-depth risk assessment, continuous monitoring, and analytics-driven insights.

Conversely, the Small and Medium-sized Enterprises (SMEs) segment, while holding a smaller share of the market, is rapidly recognizing the importance of vendor risk management. As SMEs continue to integrate into global supply chains and their operational complexities grow, the need for effective risk management becomes critical.

The adoption rate in this segment is bolstered by the increasing availability of cost-effective and scalable cloud-based solutions, making advanced vendor risk management tools more accessible to smaller businesses. Additionally, as SMEs often face tighter resource constraints, the ability to efficiently manage vendor risks can significantly impact their resilience and competitive standing.

End-Use Industry

In 2022, the Manufacturing segment held a dominant market position in the Vendor Risk Management Market, capturing more than a 22.5% share. This sector’s leading stance is attributed to its extensive global supply chains and the critical need to mitigate disruptions, maintain quality, and ensure regulatory compliance. Manufacturing companies are increasingly investing in vendor risk management solutions to navigate these complexities and sustain their competitive edge.

The IT & Telecommunications sector also represents a significant portion of the market. As these industries are at the forefront of technological innovation and heavily reliant on a myriad of vendors for hardware, software, and services, managing these relationships and the associated risks is paramount. The rapid pace of technological change further amplifies the need for robust risk management to safeguard against data breaches, service disruptions, and compliance issues.

In the Banking, Financial Services, and Insurance (BFSI) sector, strict regulatory requirements and the high stakes involved in data security make vendor risk management essential. Financial institutions utilize these solutions to ensure their vendors adhere to the same stringent standards they are subjected to, thus protecting their assets and reputation.

Retail & Consumer Goods industries are increasingly recognizing the importance of vendor risk management as they navigate a complex web of suppliers and distributors. The focus here is on maintaining product quality, ensuring supply chain integrity, and protecting customer data, all of which are crucial for brand reputation and customer trust.

Healthcare is another critical sector where vendor risk management is vital. With the growing reliance on technology and third-party services, coupled with stringent regulatory requirements for patient data security and service quality, healthcare providers are turning to sophisticated risk management solutions to ensure compliance and safeguard patient care.

Government entities, with their unique and often sensitive operational requirements, also rely on vendor risk management to ensure service continuity, protect sensitive data, and comply with regulations. The complexity of public sector supply chains and the public scrutiny they are under further underscore the importance of effective vendor risk management.

Other End-Use Industries, including but not limited to energy, education, and transportation, each face their specific challenges and risks in vendor management. These sectors seek solutions that can be tailored to their unique environments and help them maintain operational integrity, compliance, and competitive advantage.

Key Market Segments

Solution

- Vendor Information Management

- Financial Control

- Contract Management

- Quality Assurance Management

- Compliance Management

- Audit Management

- Other Solutions

Deployment Mode

- Cloud-Based

- On-Premise

Organization Size

- Large Enterprises

- Small and Medium-Sized Enterprises (SMEs)

End-Use Industry

- IT & Telecommunications

- BFSI

- Retail & Consumer Goods

- Healthcare

- Manufacturing

- Government

- Other End-Use Industries

Driving Factors

- Globalization of Supply Chains: As businesses expand globally, they rely more on a complex web of international suppliers, increasing the need for effective vendor risk management to maintain supply chain integrity and operational continuity.

- Regulatory Compliance: Increasingly stringent regulations across industries, especially in sectors like healthcare and finance, are compelling companies to adopt vendor risk management solutions to ensure compliance and avoid hefty penalties.

- Technological Advancements: The proliferation of digital technologies has made it easier for companies to monitor and manage vendor risks effectively. Tools leveraging AI and machine learning for predictive analytics are particularly driving adoption.

- Increased Outsourcing: More companies are outsourcing parts of their business, increasing their reliance on third parties and, subsequently, the need for robust systems to manage the risks associated with these external partnerships.

Restraining Factors

- High Implementation Costs: For many small and medium-sized enterprises, the initial investment in vendor risk management solutions can be prohibitively expensive, hindering market growth.

- Complexity in Integration: Integrating vendor risk management solutions with existing systems can be complex and time-consuming, particularly for organizations with outdated or legacy systems.

- Lack of Skilled Professionals: There is a shortage of skilled professionals who understand both the technical aspects of risk management solutions and the specific needs of the industry, which can restrict market growth.

- Data Privacy Concerns: With rising data breaches and privacy concerns, companies may be hesitant to adopt new systems that require sharing sensitive information with third-party vendors and platforms.

Growth Opportunities

- Cloud-Based Solutions: The increasing availability of cloud-based vendor risk management solutions offers scalable and cost-effective options for businesses of all sizes, opening up significant market opportunities.

- SME Adoption: As solutions become more accessible and the awareness of risks grows, small and medium-sized enterprises are a burgeoning market for vendor risk management tools.

- Integration with Other Business Systems: There’s a growing opportunity for vendor risk management solutions that integrate seamlessly with other business systems, providing a more holistic approach to risk management.

- Industry-Specific Solutions: Customized solutions tailored to the unique needs of specific industries, like healthcare or finance, present a significant growth opportunity as these sectors have unique regulatory and operational requirements.

Challenges

- Rapid Technological Changes: The fast pace of technological advancement means that risk management solutions can quickly become outdated, requiring continuous investment and updates.

- Complex Global Regulations: Navigating the myriad of regulations across different countries and industries is a constant challenge for businesses and vendor risk management providers alike.

- Vendor Resistance: Some vendors may be resistant to the scrutiny and processes involved in risk management, making it challenging for businesses to implement comprehensive strategies.

- Cybersecurity Threats: As cyber threats evolve and become more sophisticated, keeping vendor risk management solutions ahead of potential security breaches is an ongoing challenge.

Key Market Trends

- Increased Use of Analytics and AI: Leveraging big data analytics and artificial intelligence to predict risks and automate parts of the risk management process is a growing trend.

- Focus on Cyber Risk Management: With cyber threats on the rise, there’s an increasing trend towards solutions that specifically address the cybersecurity aspects of vendor risk.

- Greater Emphasis on Real-Time Monitoring: The market is seeing a shift towards solutions that offer real-time monitoring of vendor activities and risks, providing businesses with the ability to respond swiftly to potential issues.

- Sustainability and CSR in Risk Assessment: Companies are increasingly considering sustainability and corporate social responsibility (CSR) factors in their vendor risk assessments, reflecting broader societal trends towards ethical and sustainable business practices.

Regional Analysis

In 2023, North America held a dominant market position, capturing more than a 36.1% share. The large presence of technology companies and extensive adoption of cloud-based solutions is driving substantial growth in the North American VRM market. Increased spending by organizations to protect against cyber risks and comply with regulations around data privacy and vendor management is also fueling market expansion. The US accounts for the majority share in the North American VRM market.

Europe held the second largest share of the VRM market in 2023. Stringent regulations such as GDPR are forcing companies across the EU to implement formal vendor risk management practices. Market growth is further driven by the rapid digital transformation of businesses and the need to secure vendor ecosystems against emerging cyber threats. Germany, the UK and France are top contributing countries.

The Asia Pacific VRM market is anticipated to witness the fastest growth over the forecast period. Rapid economic development in APAC economies and increased outsourcing of key business processes to vendors is expected to boost demand for VRM solutions. Government mandates surrounding data protection and privacy are also favorable factors. China, India and Australia are key markets in the APAC region.

Latin America and Middle East & Africa currently hold relatively smaller shares in the global VRM market, but growth potential is high due to increasing awareness of third-party risks and ongoing adoption of cloud-based vendor management platforms. Brazil and Mexico are major markets in Latin America while Saudi Arabia and the UAE lead in the MEA region.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherlands

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Thailand

- Vietnam

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

The Vendor Risk Management (VRM) market is characterized by the presence of several key players who are driving the market through collaborations, partnerships, and strategic alliances. These efforts aim to enhance their product offerings, expand their market presence, and address the evolving needs of their clients.

BitSight Technologies, Inc. has strengthened its market position through strategic partnerships with cybersecurity firms to provide comprehensive risk management solutions. Their collaborations aim to integrate advanced analytics for better risk assessment. RSA Security LLC continues to be a prominent player, leveraging partnerships to enhance its Archer Suite, which is widely used for risk management. Their focus on integrating with other cybersecurity tools has improved the overall efficiency of their solutions.

MetricStream has been proactive in forming alliances with technology providers to enhance their GRC (Governance, Risk, and Compliance) platform. These collaborations are designed to offer more robust and scalable risk management solutions. Optiv Security, Inc. focuses on strategic partnerships with cybersecurity vendors to offer comprehensive VRM services. Their alliances help in providing end-to-end security solutions, addressing a broad range of vendor-related risks.

Top Key Players

- BitSight Technologies, Inc.

- RSA Security LLC

- MetricStream

- Optiv Security, Inc.

- OneTrust, LLC

- Genpact

- NAVEX Global, Inc.

- Resolver, Inc.

- Rapid Ratings International, Inc.

- Prevalent, Inc.

- ProcessUnity

- Other Key Players

Recent Developments

- February 2024: Optiv Security announced a partnership with a leading cybersecurity firm to offer a comprehensive vendor risk management service, combining Optiv’s risk management framework with enhanced threat intelligence capabilities

- November 2023: BitSight introduced new enhancements to their Third-Party Risk Management (TPRM) solution, including advanced Third-Party Vulnerability Detection capabilities to help organizations respond to zero-day vulnerabilities and major security events more effectively.

- April 2023: OneTrust introduced new features to its Vendorpedia platform, including automated vendor risk assessments and a centralized repository for vendor risk data, aimed at streamlining the risk management process for organizations.

- March 2023: RSA introduced an updated version of its Archer Suite, including new features for improved vendor risk management and enhanced automation capabilities for risk assessments and reporting.

- May 2023: MetricStream launched a new version of their GRC platform, focusing on enhanced risk management functionalities. This update includes advanced analytics and improved integration capabilities with third-party risk management tools.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2023) | USD 11.5 Bn |

| Forecast Revenue (2032) | USD 42.6 Bn |

| CAGR (2023-2032) | 15.7% |

| Base Year for Estimation | 2023 |

| Historic Period | 2019-2022 |

| Forecast Period | 2023-2032 |

| Report Coverage | Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments |

| Segments Covered | By Solution (Vendor Information Management, Financial Control, Contract Management, Quality Assurance Management, Compliance Management, Audit Management, Other Solutions), By Deployment Mode (Cloud and On-premises), By Organization Size (SMEs, and Large Enterprises), By End-Use (IT & Telecommunications, BFSI, Retail & Consumer Goods, Healthcare, Manufacturing, Government, Other End-Use Industries) |

| Regional Analysis | North America – The US & Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, and Rest of Europe; APAC- China, Japan, South Korea, India, Australia, New Zealand, Singapore, Thailand, Vietnam, and Rest of APAC; Latin America- Brazil, Mexico & Rest of Latin America; Middle East & Africa- South Africa, Saudi Arabia, UAE & Rest of MEA |

| Competitive Landscape | BitSight Technologies Inc., RSA Security LLC, MetricStream, Optiv Security Inc., OneTrust, LLC, Genpact, NAVEX Global Inc., Resolver Inc., Rapid Ratings International Inc., Prevalent Inc., ProcessUnity, Other Key Players |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |

Frequently Asked Questions (FAQ)

Risks associated with vendor management include cybersecurity threats, data breaches, operational disruptions, compliance failures, reputational damage, and financial risks. Ineffective vendor management can lead to these risks impacting the business.

The Global Vendor Risk Management Market is estimated to be worth USD 11.5 billion in 2023 and projected to be valued at USD 42.6 billion in 2032. Between 2023 and 2032, the market is expected to register a growth rate of 15.7%.

The risk management market encompasses various solutions and services aimed at identifying, assessing, and mitigating risks across different aspects of business operations. This includes financial risk, operational risk, cybersecurity risk, and, relevant to vendor management, third-party or vendor-related risk.

A risk matrix for vendor management is a visual tool that helps organizations assess and prioritize risks associated with their vendors. It typically categorizes risks based on likelihood and impact, providing a structured way to prioritize risk mitigation efforts.

VRM is crucial for businesses as it helps in identifying and managing potential risks posed by third-party vendors, ensuring compliance with regulations, protecting sensitive data, and maintaining overall business continuity.

Challenges may include the complexity of managing a diverse vendor ecosystem, assessing the cybersecurity capabilities of vendors, keeping up with evolving regulatory requirements, and effectively communicating risk expectations to vendors.