Quick Navigation

- Report Overview

- Top Market Takeaways

- Drivers Impact Analysis

- Restraints Impact Analysis

- By Component Analysis

- By Type Analysis

- By Product Type Analysis

- By End-User Industry Analysis

- Investor Type Impact Analysis

- Technology Enablement Analysis

- Key Challenges

- Emerging Trends

- Growth Factors

- Key Market Segments

- Regional Analysis

- Competitive Analysis

- Future Outlook

- Recent Developments

- Report Scope

Report Overview

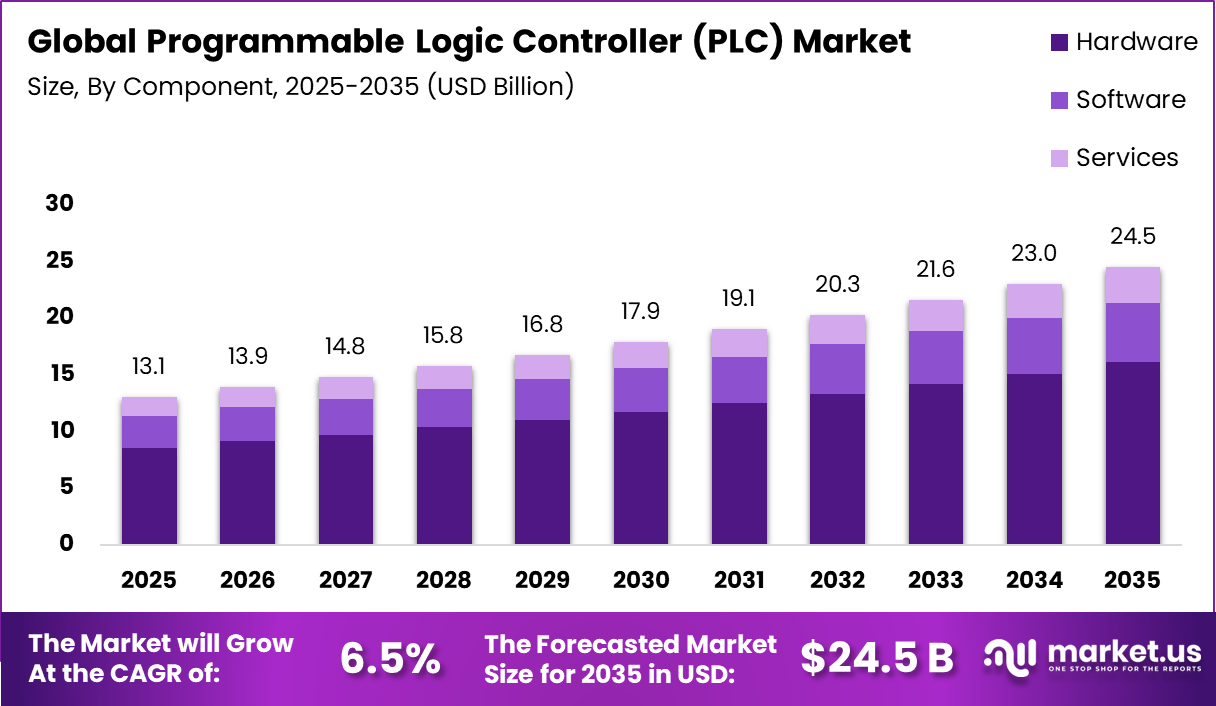

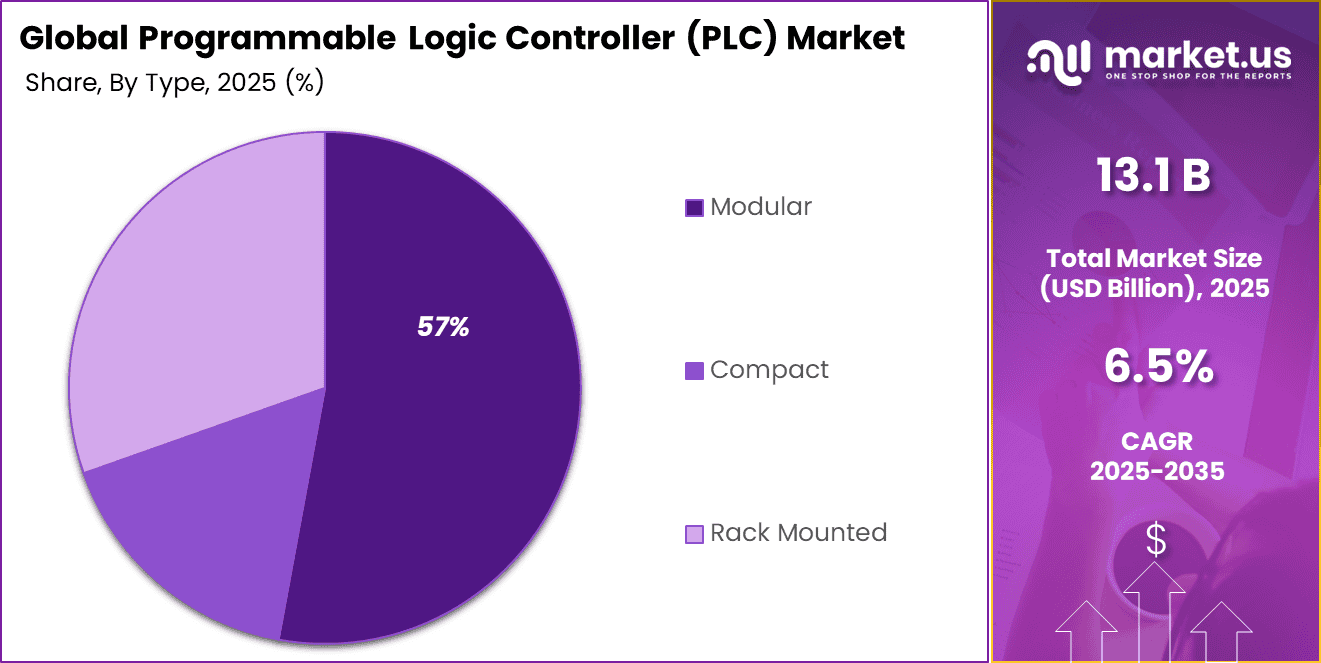

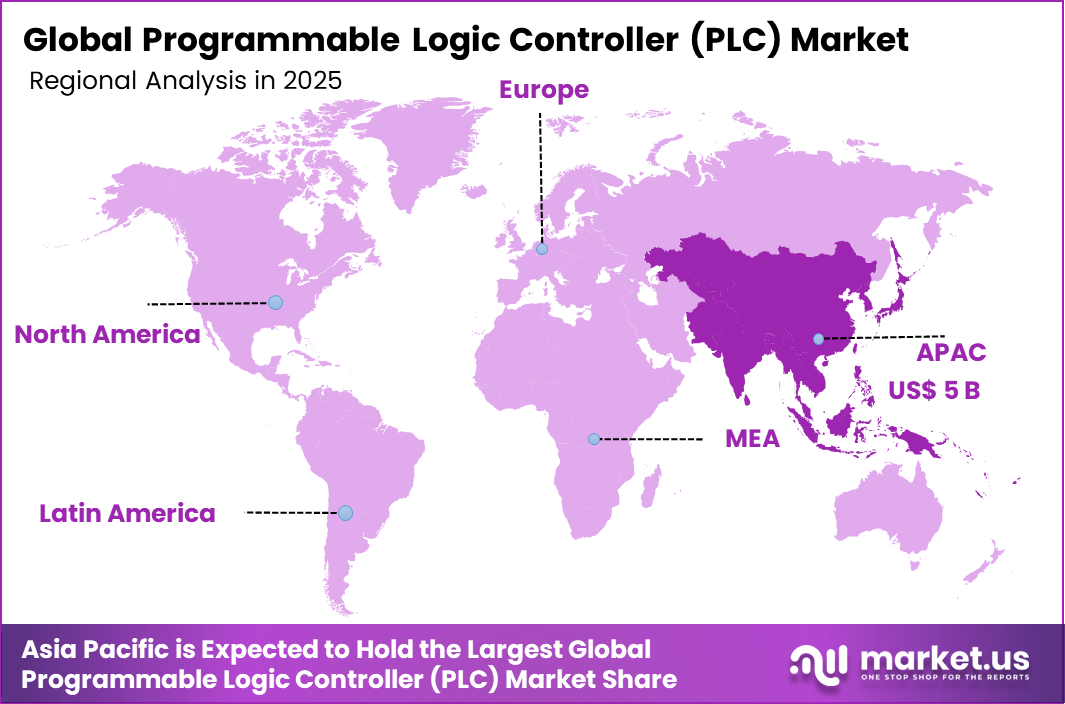

The Global Programmable Logic Controller (PLC) Market generated USD 13.1 billion in 2025 and is predicted to register growth from USD 13.9 billion in 2026 to about USD 24.5 billion by 2035, recording a CAGR of 6.5% throughout the forecast span. In 2025, North America held a dominant market position, capturing more than a 38.3% share, holding USD 5 Billion revenue.

Top Market Takeaways

- Component Hardware accounts for 65.7% of the Programmable Logic Controller (PLC) market, as most spending is directed toward physical PLC units, I/O modules, and related control hardware.

- Type Modular PLCs hold 57.4% of the market, because users prefer flexible systems that can be expanded or reconfigured easily by adding or removing modules.

- Product Type Large PLCs represent 41.5% of the market, reflecting strong use in complex, large-scale automation projects that require high processing power and many I/O points.

- End-User Industry The energy and utilities sector accounts for 31.8%, driven by the need for reliable automation in power plants, grids, water treatment, and other critical infrastructure.

- Region Asia-Pacific holds 38.3% of the global PLC market, supported by rapid industrialization and strong investments in manufacturing and infrastructure.

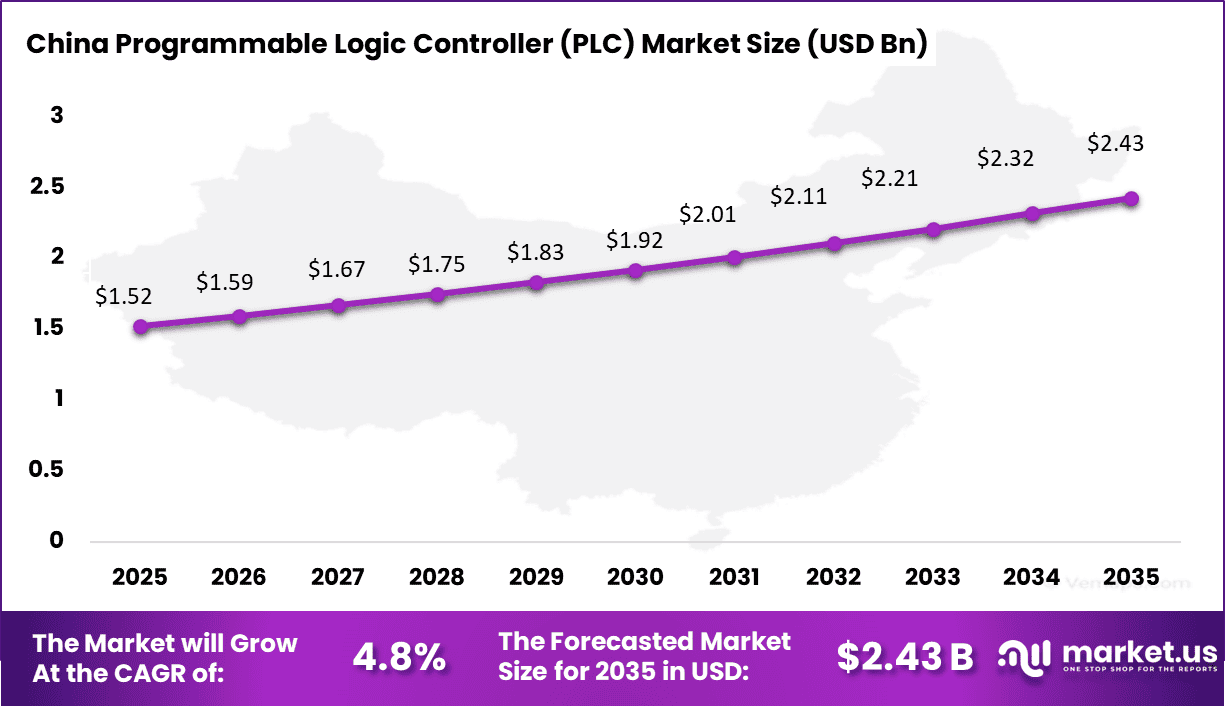

- Country China’s PLC market is valued at 1.52 billion and is expected to grow at a CAGR of 4.8%, as the country continues to modernize factories and expand its energy and utility networks.

Programmable logic controllers are industrial computers used to automate and control machines and processes in manufacturing, utilities, and infrastructure operations. They receive inputs from sensors, process logic based on programmed instructions, and send outputs to control motors, valves, and other equipment. PLCs are known for their reliability, fast response, and ability to operate in harsh industrial environments. As production systems become more connected and data driven, PLCs continue to serve as a core control layer within modern automation architectures.

One of the main driving factors is the increasing push toward industrial automation across sectors such as automotive, food processing, energy, and chemicals. Companies are focusing on improving productivity, reducing downtime, and maintaining consistent product quality, which drives the use of reliable control systems. In addition, the shift toward smart manufacturing is encouraging the integration of PLCs with sensors, networks, and software platforms for better visibility and control. The need for real time decision making on the shop floor is also supporting adoption, as PLCs provide fast and precise control over critical operations.

Demand for programmable logic controllers is rising as industries seek scalable and dependable automation solutions. There is a strong preference for systems that are easy to program, support flexible configuration, and integrate with existing equipment and digital platforms. Users are also looking for controllers that can handle complex processes while maintaining stability and uptime. The demand is particularly strong in sectors where continuous operation and safety are essential. As industrial environments continue to modernize and adopt connected technologies, the need for efficient and robust control systems is expected to grow steadily.

Drivers Impact Analysis

| Key Driver | Impact on CAGR Forecast (~%) | Geographic Relevance | Impact Timeline | Additional Insight |

|---|---|---|---|---|

| Rising adoption of industrial automation and smart manufacturing | +2.8% | North America, Europe, Asia Pacific | Medium to long term | Automation drives PLC demand |

| Growing implementation of Industry 4.0 technologies | +2.5% | Global | Medium term | Digital factories require PLC control |

| Increasing demand for energy-efficient and optimized operations | +2.2% | Global | Medium to long term | PLCs improve process efficiency |

| Expansion of manufacturing sectors such as automotive and electronics | +2.0% | Asia Pacific, North America | Medium term | Industrial growth supports adoption |

| Integration of PLCs with IoT and connected systems | +1.8% | Global | Medium to long term | Connectivity enhances control capabilities |

Restraints Impact Analysis

| Key Restraint | Impact on CAGR Forecast (~%) | Geographic Relevance | Impact Timeline | Additional Insight |

|---|---|---|---|---|

| High initial investment and upgrade costs | -2.3% | Emerging markets | Short to medium term | Costs slow adoption |

| Complexity in programming and system integration | -2.0% | Global | Medium term | Skill requirements limit usage |

| Cybersecurity concerns in connected PLC systems | -1.7% | Global | Medium to long term | Security risks affect confidence |

| Limited adoption among small and medium enterprises | -1.5% | Developing regions | Medium term | Smaller firms delay investment |

| Dependence on legacy infrastructure in older plants | -1.3% | Global | Long term | Old systems slow modernization |

By Component Analysis

The hardware segment accounted for 65.7% of the market share, reflecting its strong role in enabling reliable industrial automation and control. This dominance is supported by the growing demand for processors, input and output modules, power supplies, and communication interfaces that form the backbone of PLC systems. Hardware components are essential for executing control logic, monitoring processes, and ensuring stable system performance in industrial environments.

Another factor driving this segment is the expansion of automation across manufacturing, energy, and infrastructure sectors. Industries are investing in durable and high-performance hardware to support continuous operations and reduce downtime. The need for real-time control and system reliability continues to strengthen demand for PLC hardware solutions.

By Type Analysis

The modular PLCs segment held 57% share, driven by their flexibility, scalability, and ease of customization. Modular systems allow users to expand or modify configurations based on specific application needs, making them suitable for a wide range of industrial processes. This adaptability is highly valued in environments where operational requirements change over time.

In addition, modular PLCs support easier maintenance and system upgrades compared to fixed configurations. Users can replace or add individual modules without affecting the entire system, improving efficiency and reducing operational disruptions. These advantages continue to support strong adoption across industries.

By Product Type Analysis

The large PLCs segment captured 41.5% of the market, reflecting their importance in managing complex and large-scale industrial operations. These systems are designed to handle multiple inputs and outputs, high processing loads, and advanced control functions. Large PLCs are widely used in industries where precision and coordination across multiple processes are required.

Furthermore, the increasing scale of industrial automation projects has led to greater demand for high-capacity control systems. Large PLCs provide the performance and reliability needed for critical applications, supporting efficient process management and operational stability.

By End-User Industry Analysis

The energy and utilities segment accounted for 31.8% of the market share, driven by the need for reliable control systems in power generation, transmission, and distribution processes. PLCs are used to monitor equipment, manage operations, and ensure safety in complex energy systems. Their ability to support real-time control is essential for maintaining stable and efficient operations.

Moreover, the ongoing modernization of energy infrastructure and the integration of renewable energy sources have increased the demand for advanced automation solutions. PLC systems help improve system efficiency, reduce operational risks, and support continuous monitoring, reinforcing their importance in the energy and utilities sector.

Investor Type Impact Analysis

| Investor Type | Growth Sensitivity | Risk Exposure | Geographic Focus | Investment Outlook |

|---|---|---|---|---|

| Venture capital firms | Moderate | High | US, Europe | Investing in industrial automation startups |

| Private equity firms | Moderate to high | Moderate | North America and Europe | Scaling automation solution providers |

| Corporate investors | High | Moderate | Global | Strategic investments in smart manufacturing |

| Institutional investors | Moderate | Low to moderate | Developed markets | Prefer stable industrial technology firms |

| Government and public funding bodies | Moderate to high | Low | Global | Supporting industrial modernization |

Technology Enablement Analysis

| Technology | Impact on CAGR Forecast (~%) | Geographic Relevance | Impact Timeline | Additional Insight |

|---|---|---|---|---|

| Integration with industrial IoT platforms | +3.0% | Global | Medium to long term | Enables real-time monitoring |

| AI-based predictive maintenance systems | +2.7% | US, Europe, Asia Pacific | Medium term | Reduces downtime and failures |

| Cloud-connected PLC systems | +2.4% | Global | Short to medium term | Enables remote control and analytics |

| Advanced modular PLC architectures | +2.2% | Global | Medium term | Improves flexibility and scalability |

| Edge computing for real-time control | +1.9% | Global | Medium to long term | Enhances low-latency operations |

Key Challenges

- High initial cost makes adoption difficult for small industries.

- Complex programming requires skilled engineers.

- Integration challenges with legacy machines and systems.

- Limited flexibility in some older PLC models.

- Cybersecurity risks in connected industrial environments.

- Maintenance and upgrade costs increase over time.

- Vendor dependency limits switching options.

- Compatibility issues across different brands and devices.

- Downtime risks during system failures or updates.

- Slow adoption in traditional manufacturing sectors.

Emerging Trends

The programmable logic controller market is evolving toward more connected, flexible, and intelligent control systems that fit into modern industrial environments. One of the key emerging trends is the shift toward integration with industrial internet platforms, allowing PLCs to exchange data with cloud systems, analytics tools, and enterprise applications. This is improving visibility across production processes. Another important trend is the move toward compact and modular PLC designs that can be easily customized for different applications while saving space on factory floors.

There is also growing adoption of edge processing capabilities within PLCs, enabling faster decision making directly at the machine level without relying on centralized systems. In addition, enhanced cybersecurity features are becoming a priority as industrial networks become more connected. The use of software based configuration and remote programming is also increasing, making it easier to update and manage control systems across multiple locations.

Growth Factors

The growth of this market is driven by the rising demand for automation and efficiency across manufacturing and process industries. As companies aim to improve productivity and reduce manual intervention, PLCs are becoming essential for controlling and monitoring complex operations. The expansion of smart manufacturing and digitally connected factories is also supporting demand, as these environments require reliable and responsive control systems.

Another major factor is the need for consistent product quality and reduced downtime, which PLCs help achieve through precise control and real time monitoring. Industries are also focusing on optimizing energy use and operational costs, further encouraging the adoption of advanced control solutions. Furthermore, the increasing complexity of industrial processes and the push toward digital transformation are creating strong opportunities for modern PLC systems that can integrate seamlessly with broader automation ecosystems.

Key Market Segments

By Component

- Hardware

- Central Processing Unit (CPU)

- Memory Modules

- Input Modules

- Output Modules

- Communication Modules

- Power Supply Unit

- Others

- Software

- Services

- Installation and Integration

- Training and Support

- Maintenance

By Type

- Modular

- Compact

- Rack Mounted

By Product Type

- Large PLCs

- Micro PLCs

- Nano PLCs

- Others

By End-user Industry

- Automotive

- Food and Beverage

- Chemical and Petrochemical

- Oil and Gas

- Energy and Utilities

- Water and Wastewater Treatment

- Pharmaceutical

- Pulp and Paper

- Metals and Mining

- Others

Regional Analysis

Asia Pacific accounted for 38.3% of the Programmable Logic Controller (PLC) market, supported by strong industrial growth and increasing adoption of automation across manufacturing sectors. The region has a large base of factories in industries such as electronics, automotive, food processing, and chemicals, where PLCs are widely used for process control and operational efficiency.

Companies are focusing on improving production speed, reducing downtime, and enhancing quality, which is driving demand for reliable control systems. In addition, growing investments in smart manufacturing and industrial modernization are strengthening the adoption of PLC solutions across the region.

China market reached USD 1.52 Billion and is projected to grow at a CAGR of 4.8%, driven by its dominant manufacturing sector and continuous push toward automation. Industries are increasingly adopting PLC systems to support high-volume production, maintain process consistency, and improve energy efficiency.

The expansion of industrial infrastructure and the shift toward more advanced production technologies are also contributing to market growth. In addition, ongoing focus on factory digitization and productivity improvement is expected to support steady growth of the PLC market in China over the coming years.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherlands

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Thailand

- Vietnam

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Competitive Analysis

The competitive landscape of the Programmable Logic Controller (PLC) Market is led by global industrial automation companies with strong expertise in control systems and manufacturing technologies. Companies such as Siemens AG, Rockwell Automation Inc., Schneider Electric SE, Mitsubishi Electric Corporation, ABB Ltd., Omron Corporation, and Emerson Electric Co. focus on advanced PLC systems used in industrial automation, process control, and smart manufacturing. These players provide reliable, scalable, and high-performance controllers integrated with software platforms and industrial networks. Their strong global presence and continuous investment in Industry 4.0 technologies help them maintain a leading position in the market.

At the same time, companies such as Honeywell International Inc., Beckhoff Automation GmbH & Co. KG, Delta Electronics Inc., Bosch Rexroth AG, Panasonic Holdings Corporation, Fuji Electric Co. Ltd., Hitachi Ltd., IDEC Corporation, Keyence Corporation, Toshiba Corporation, General Electric Company, Parker Hannifin Corporation, Eaton Corporation plc, Yokogawa Electric Corporation, Inovance Technology Co. Ltd., Hollysys Automation Technologies Ltd., WAGO Kontakttechnik GmbH & Co. KG, and B&R Industrial Automation GmbH compete by offering specialized PLC solutions for different industrial applications.

These players focus on compact design, real-time control, easy integration, and cost efficiency. Competition in this market is driven by automation demand, system flexibility, and the ability to support connected and intelligent manufacturing environments.

Top Key Players in the Market

- Siemens AG

- Rockwell Automation Inc.

- Schneider Electric SE

- Mitsubishi Electric Corporation

- ABB Ltd.

- Omron Corporation

- Emerson Electric Co.

- Honeywell International Inc.

- Beckhoff Automation GmbH & Co. KG

- Delta Electronics Inc.

- Bosch Rexroth AG

- Panasonic Holdings Corporation

- Fuji Electric Co. Ltd.

- Hitachi Ltd.

- IDEC Corporation

- Keyence Corporation

- Toshiba Corporation

- General Electric Company

- Parker Hannifin Corporation

- Eaton Corporation plc

- Yokogawa Electric Corporation

- Inovance Technology Co. Ltd.

- Hollysys Automation Technologies Ltd.

- WAGO Kontakttechnik GmbH & Co. KG

- B&R Industrial Automation GmbH

- Others

Future Outlook

The future outlook for the Programmable Logic Controller (PLC) Market looks strong as industries continue to adopt automation and smart manufacturing systems. The market is expected to grow with increasing demand for reliable and flexible control systems in sectors like manufacturing, energy, and infrastructure. Companies are anticipated to upgrade to advanced PLCs to improve efficiency, reduce downtime, and support complex operations. In the coming years, integration with IoT, AI, and cloud platforms is expected to enhance real-time monitoring and decision making, making PLCs a key part of modern industrial automation.

Recent Developments

- March 2026, Siemens AG – Siemens promotes its SIMATIC S7‑1500 and new S7‑1200 G2 PLCs as top picks for 2026, emphasizing software‑defined automation, multi‑CPU performance, OPC UA/MQTT connectivity, and tight integration with TIA Portal and IT systems.

- March 2026, Schneider Electric SE – Schneider’s Modicon PLC family is highlighted as a major modular PLC line in 2026, used in machine and process automation with IIoT connectivity and EcoStruxure integration for energy and asset management.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 13.1 Billion |

| Forecast Revenue (2035) | USD 24.5 Billion |

| CAGR(2025-2035) | 6.5% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue forecast, AI impact on Market trends, Share Insights, Company ranking, competitive landscape, Recent Developments, Market Dynamics and Emerging Trends |

| Segments Covered | By Component (Hardware (Central Processing Unit (CPU), Memory Modules, Input Modules, Others), Software, Services (Installation and Integration, Training and Support, Maintenance)), By Type (Modular, Compact, Rack Mounted), By Product Type (Large PLCs, Micro PLCs, Others), By End-user Industry (Automotive, Food and Beverage, Chemical and Petrochemical,Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Latin America; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Siemens AG, Rockwell Automation Inc., Schneider Electric SE, Mitsubishi Electric Corporation, ABB Ltd., Omron Corporation, Emerson Electric Co., Honeywell International Inc., Beckhoff Automation GmbH & Co. KG, Delta Electronics Inc., Bosch Rexroth AG, Panasonic Holdings Corporation, Fuji Electric Co. Ltd., Hitachi Ltd., IDEC Corporation, Keyence Corporation, Toshiba Corporation, General Electric Company, Parker Hannifin Corporation, Eaton Corporation plc, Yokogawa Electric Corporation, Inovance Technology Co. Ltd., Hollysys Automation Technologies Ltd., WAGO Kontakttechnik GmbH & Co. KG, B&R Industrial Automation GmbH, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three license to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |

Market")