Quick Navigation

Report Overview

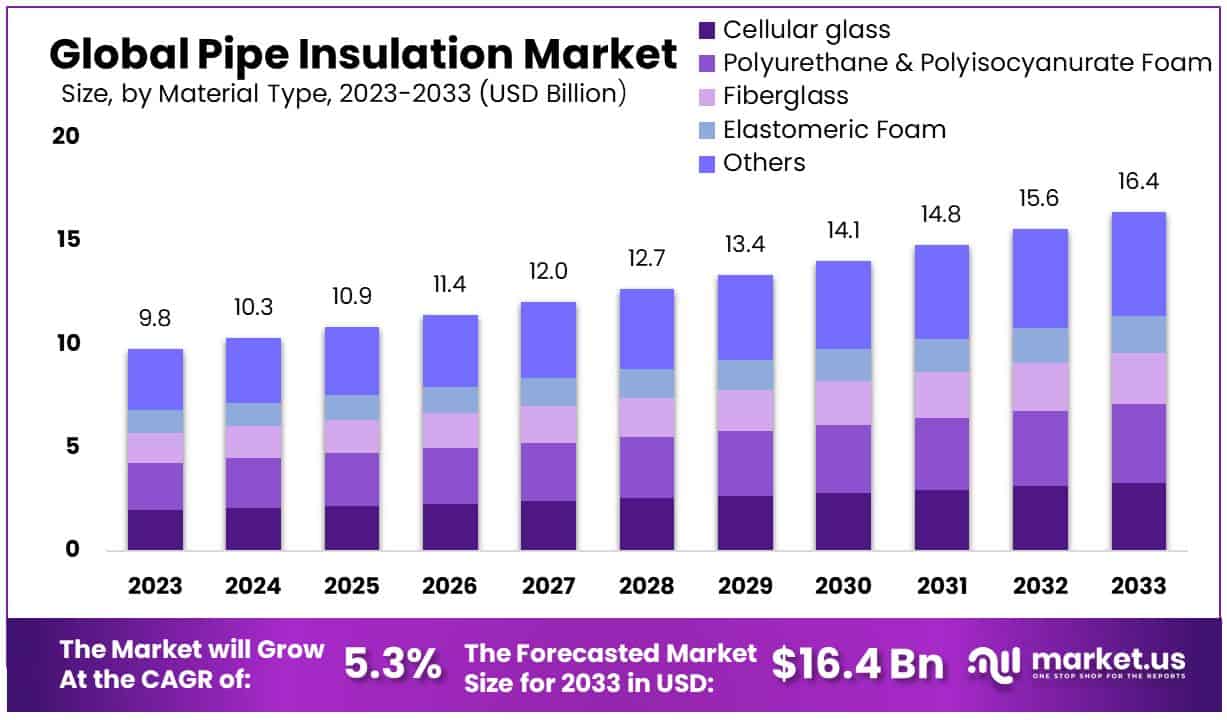

The Global Pipe Insulation Market size is expected to be worth around USD 16.4 Billion by 2033, from USD 9.8 Billion in 2023, growing at a CAGR of 5.30% during the forecast period from 2024 to 2033.

The Pipe Insulation Market is a segment within the construction and industrial sectors focusing on materials and technologies used to conserve energy and reduce heat loss in piping systems. This market serves to enhance safety, increase efficiency, and minimize energy costs in various applications, including residential, commercial, and industrial settings.

Key products include fiberglass, foam, and rubber insulation solutions, catering to the needs of piping systems for hot and cold services. The growth of this market is driven by global trends towards energy efficiency and sustainability, making it crucial for stakeholders to consider for strategic investments and product development.

In construction and industrial efficiency, the Pipe Insulation Market is emerging as a critical area of focus. This market, integral to the optimization of energy use and operational safety in buildings and infrastructure, is poised for substantial growth. The driving force behind this expansion is the global impetus on energy conservation, regulatory mandates for building efficiency, and the increasing awareness of the cost benefits associated with insulated piping systems.

Notably, the surge in infrastructure development is a significant catalyst for the market’s upward trajectory. Rapid urbanization and an escalating number of infrastructure projects—including roads, bridges, and high-rise buildings—are bolstering the demand for efficient pipe insulation solutions. This is especially pertinent in regions experiencing intense development activities.

For instance, the Asian Development Bank (ADB) has highlighted the immense investment needs for Asia, projecting that approximately US$1.7 trillion will be required annually through 2030 to meet the infrastructure demands of its burgeoning urban centers. This projection underscores the vast potential for growth in the Pipe Insulation Market, as these extensive infrastructure developments necessitate advanced insulation solutions to ensure energy efficiency and sustainability.

Moreover, the market is characterized by a diverse range of products, such as fiberglass, foam, and rubber insulation materials, each catering to specific environmental and operational requirements. This variety allows for tailored solutions that meet the stringent standards set forth by industries and governments alike.

Key Takeaways

- Market Value: The Global Pipe Insulation Market is projected to reach approximately USD 16.4 Billion by 2033, indicating substantial growth from USD 9.8 Billion in 2023, with a steady CAGR of 5.30% during the forecast period from 2024 to 2033.

- Dominant Segments:

- Material Type Analysis: Polyurethane & Polyisocyanurate Foam leads with a significant market share of 23.4%, owing to its exceptional thermal insulation properties, moisture resistance, and versatility across industrial and residential applications.

- Prefabricated Insulation Analysis: Prefabricated Insulation dominates with a substantial market share of 41.3%, driven by its ease of installation, consistent quality, and tailored fit for various piping systems, particularly favored in large-scale industrial projects.

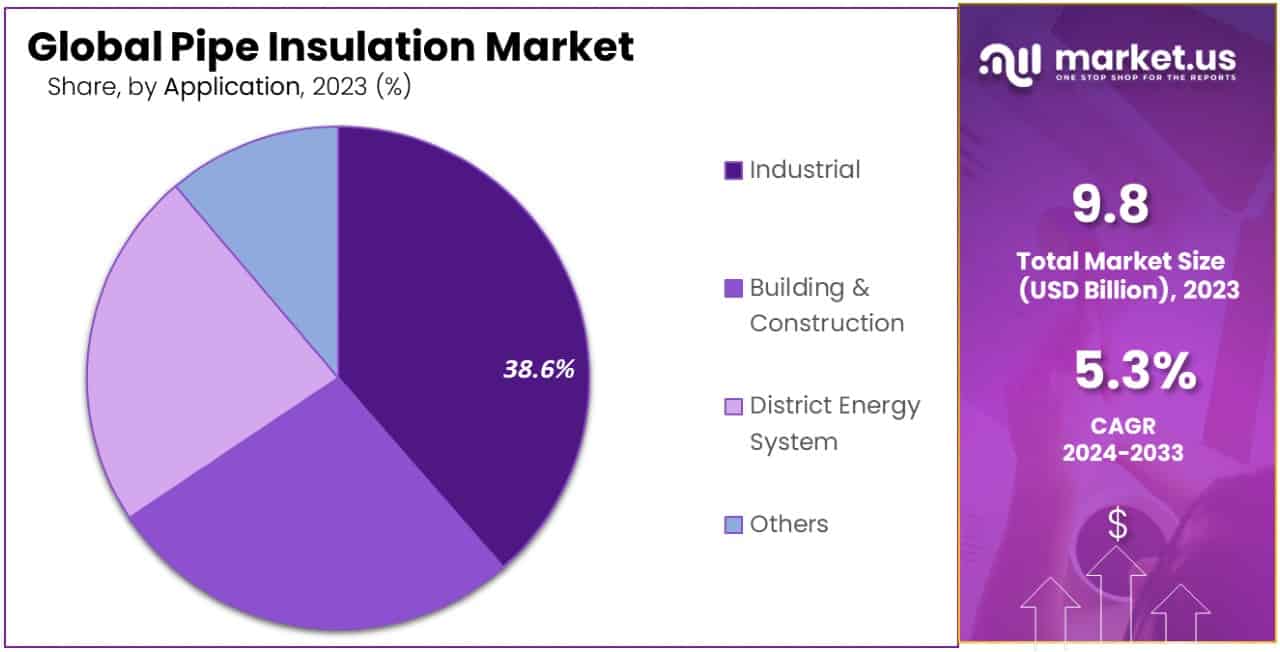

- Industrial Application Analysis: The Industrial segment commands a significant market share of 38.6%, emphasizing the critical need for efficient insulation in manufacturing, power generation, and chemical processing industries, driven by temperature control and energy conservation requirements.

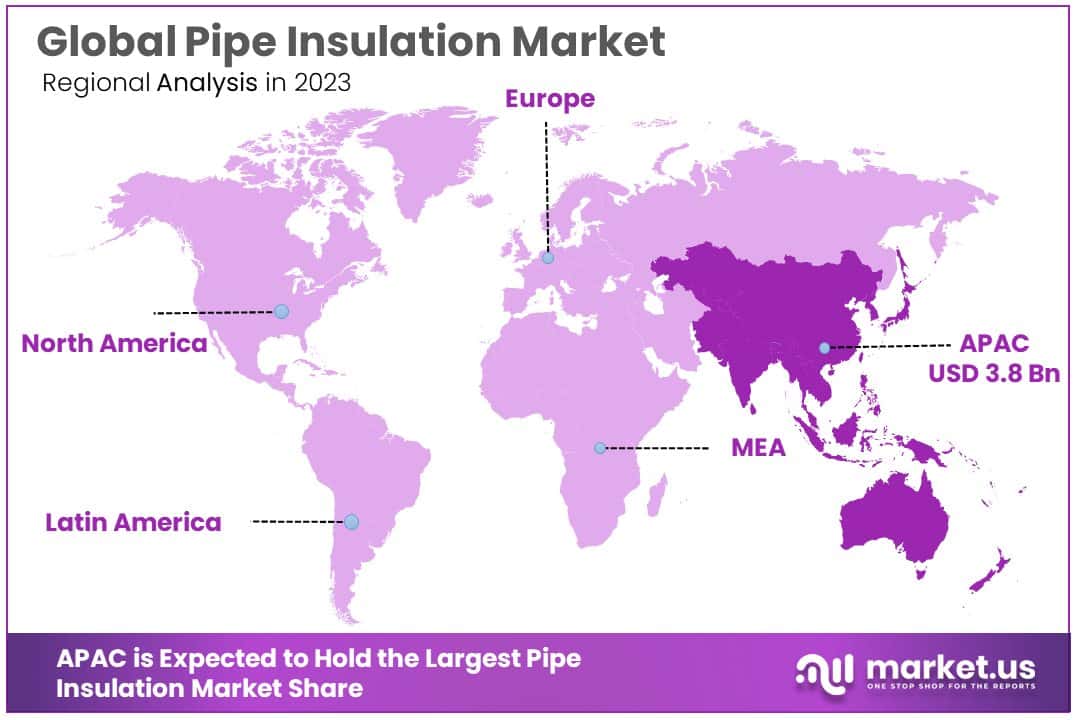

- Regional Analysis: APAC leads the market with a dominant 38.6% share, followed by North America with approximately 24.5%. APAC’s leadership is attributed to industrialization trends, while North America’s strong presence is fueled by stringent energy regulations and infrastructure retrofitting initiatives.

- Key Players: Major players in the Pipe Insulation Market include Armacell Group, Johns Manville Corporation, Owens Corning Inc., Compagnie de Saint-Gobain SA, Knauf Insulation GmbH, Rockwool International A/S, BASF SE, Kingspan Group plc, Huntsman Corporation, Thermaflex, Paroc Group Oy, and L’Isolante K-Flex S.p.A.

- Analyst Viewpoint: The market’s growth is fueled by increasing demand for energy-efficient insulation solutions, stringent regulatory requirements, and a focus on sustainability across industries.

- Growth Opportunity: Growth opportunities lie in material innovation, prefabrication advancements, and expanding applications in emerging sectors like renewable energy and smart infrastructure. Additionally, regional market dynamics, technological adoption, and strategic partnerships will influence market expansion and competitiveness in the coming years.

Driving Factors

Aging Infrastructure and Replacement Demand Catalyze Market Renewal

The challenge of aging infrastructure, especially in developed countries, significantly influences the Pipe Insulation Market. The American Society of Civil Engineers (ASCE) highlights a critical issue with its report of approximately 240,000 water main breaks annually in the United States, underscoring the pressing need for infrastructure renewal. This scenario extends beyond water systems to encompass a broad range of piping networks that are integral to residential, commercial, and industrial buildings.

The demand for pipe insulation materials is thus driven by the necessity to replace and upgrade these deteriorating systems. Such upgrades are essential not only for improving energy efficiency but also for ensuring operational safety and compliance with updated regulatory standards. The replacement demand catalyzed by aging infrastructure presents a unique growth avenue for the Pipe Insulation Market. It encourages the development of innovative insulation solutions that can be retrofitted into existing systems or integrated into new installations, highlighting the market’s adaptability and responsiveness to infrastructural challenges.

Energy Efficiency and Sustainability Initiatives Drive Market Growth

Energy efficiency and sustainability are at the forefront of global environmental efforts, profoundly impacting the Pipe Insulation Market. The role of pipe insulation in minimizing energy loss in heating and cooling systems is paramount. It significantly contributes to the overall energy efficiency of buildings and industrial facilities. By reducing the energy required to heat or cool spaces, insulation directly aligns with global initiatives aimed at conserving energy and promoting sustainability. This trend is bolstered by the increasing awareness and commitment of governments and corporations towards achieving net-zero emissions and reducing their carbon footprint.

As such, investments in energy-efficient solutions, including pipe insulation, are escalating. The global push for sustainability not only fosters a favorable regulatory environment but also drives consumer and business demand for green building practices. This convergence of factors creates a substantial growth opportunity for the Pipe Insulation Market, positioning it as a critical component in the pursuit of energy conservation and sustainability goals.

Stringent Building Codes and Regulations Mandate Market Expansion

The tightening of building codes and regulations worldwide serves as a pivotal driver for the Pipe Insulation Market. Governments and regulatory authorities are increasingly mandating the incorporation of energy-efficient materials, such as pipe insulation, to enhance building performances and mitigate greenhouse gas emissions. These regulations, aimed at new constructions and renovations, require builders and developers to adhere to specific insulation standards.

For instance, the integration of pipe insulation is no longer a matter of choice but a compliance requirement in many jurisdictions. This regulatory landscape not only ensures improved energy efficiency but also propels the demand for insulation materials. As a result, manufacturers and suppliers are motivated to innovate and expand their product offerings to meet these stringent standards. The direct impact of such regulations is evident in the accelerated market growth, as the industry adapts to meet the evolving demands of energy efficiency and environmental stewardship.

Restraining Factors

Flammability and Fire Safety Concerns Restrain Market Growth

Fire safety is a critical issue that impacts the Pipe Insulation Market, particularly when it comes to the use of certain foam insulation materials. These materials can be highly flammable, posing significant risks in scenarios where pipes operate at high temperatures or are located in confined spaces. The National Institute of Standards and Technology (NIST) has reported instances where foam plastic insulation contributed to the rapid spread of fire in high-rise buildings.

This has led to the implementation of stricter regulations and guidelines for the use of fire-resistant insulation materials. Such concerns limit the application of various insulation types and necessitate the development of safer, non-flammable alternatives, posing a challenge to market growth by narrowing the range of viable product offerings.

Moisture Absorption and Corrosion Issues Restrains Market Growth

The effectiveness and longevity of pipe insulation are critically undermined by moisture absorption and the subsequent corrosion of the piping system. Materials like fiberglass and mineral wool, though widely used for their insulative properties, are prone to absorbing moisture over time. This not only reduces the insulation’s effectiveness but also accelerates the corrosion of the pipes themselves.

According to research by the National Association of Corrosion Engineers (NACE), moisture ingress in insulation is a significant factor in corrosion-related failures in industrial settings. Such issues necessitate more frequent replacements and maintenance, increasing the total cost of ownership and limiting the market growth by making some insulation options less appealing to consumers seeking long-term, maintenance-free solutions.

Material Type Analysis

In the Pipe Insulation Market, material type plays a pivotal role in shaping market dynamics and growth trajectories. Among the array of materials, Polyurethane & Polyisocyanurate Foam emerges as the dominant sub-segment, holding a significant market share of 23.4%. This prominence can be attributed to the material’s exceptional thermal insulation properties, moisture resistance, and durability.

Polyurethane & Polyisocyanurate Foam is extensively utilized in both industrial and residential settings, offering versatile applications ranging from high-temperature pipes in industrial facilities to refrigeration systems and HVAC in buildings. The insulation’s lightweight nature, coupled with its ease of installation and compatibility with various piping systems, further bolsters its adoption.

While Polyurethane & Polyisocyanurate Foam leads the market, other segments like Cellular Glass, Fiberglass, Elastomeric Foam, and others also contribute to the market’s diversity and growth. Cellular Glass, known for its fire resistance and compressive strength, is preferred in applications requiring robust fire safety measures. Fiberglass, on the other hand, is valued for its cost-effectiveness and thermal efficiency, making it a popular choice for a wide range of temperatures and environments. Elastomeric Foam stands out for its flexibility and condensation control capabilities, ideal for preventing moisture intrusion and ensuring system longevity.

Manufacturers are increasingly focusing on eco-friendly and high-performance materials to meet the shifting preferences and regulatory standards, ensuring the Pipe Insulation Market’s sustained growth and adaptation to future challenges and opportunities.

Insulation Analysis

Prefabricated Insulation emerges as the dominant sub-segment in the Pipe Insulation Market, capturing a significant market share of 41.3%. This dominance can be attributed to its wide-ranging benefits, including ease of installation, consistent quality control, and tailored fit for a variety of piping systems.

Prefabricated insulation is particularly favored in large-scale industrial and commercial projects where time and accuracy are of the essence. The prefabrication process allows for insulation materials to be cut and shaped to fit specific pipe dimensions off-site, significantly reducing installation time and labor costs. This efficiency is crucial in sectors where operational downtime for maintenance or upgrades needs to be minimized.

The other segments within the insulation type category, such as Rigid Board, Flexible, Loose Fill, and Spray Foam Insulation, each play a pivotal role in market growth. Rigid Board Insulation offers robust support for high-temperature applications, Flexible Insulation caters to systems requiring complex fittings, Loose Fill Insulation is preferred for irregular spaces, and Spray Foam provides an airtight seal, enhancing energy efficiency.

Although these segments cater to different needs, Prefabricated Insulation’s market share underscores its broad applicability and demand across diverse industries. The increasing focus on energy efficiency, coupled with stringent building codes, propels the demand for prefabricated insulation solutions that meet these requirements effectively and efficiently. The integration of advanced materials and technologies in prefabrication processes further solidifies its market position, addressing both thermal performance and fire safety concerns.

Application Analysis

Within the Pipe Insulation Market, the Industrial segment stands out with a market share of 38.6%, underscoring its significant impact on overall market dynamics. This segment’s prominence is driven by the critical need for efficient insulation in manufacturing facilities, power plants, and chemical processing units, where temperature control and energy conservation are paramount. Industrial applications often involve extreme temperatures and hazardous materials, necessitating high-performance insulation to ensure safety, operational efficiency, and compliance with environmental standards.

The Building & Construction, District Energy System, and other application segments, while distinct, complement the growth seen in the industrial sector. Building & Construction focuses on thermal efficiency and noise reduction in residential and commercial buildings, District Energy Systems on the efficiency of heating and cooling networks, and other applications cover specialized needs such as refrigeration and cryogenics.

The Industrial segment’s dominance is further bolstered by the ongoing global industrialization and the push for more sustainable manufacturing practices. This drive towards sustainability encourages the adoption of advanced insulation solutions capable of minimizing energy consumption and reducing operational costs.

As industries continue to evolve, the demand for pipe insulation that can meet these stringent requirements—enhancing both environmental performance and economic viability—remains strong. The synergistic growth across these application segments highlights the diverse yet interconnected nature of the Pipe Insulation Market’s ecosystem.

Key Market Segments

By Material Type

- Cellular glass

- Polyurethane & Polyisocyanurate Foam

- Fiberglass

- Elastomeric Foam

- Others

By Insulation Type

- Prefabricated Insulation

- Rigid Board Insulation

- Flexible Insulation

- Loose Fill Insulation

- Spray Foam Insulation

By Application

- Industrial

- Building & Construction

- District Energy System

- Others

Growth Opportunities

Expansion of Industrial and Commercial Construction Offers Growth Opportunity

The burgeoning expansion in industrial and commercial construction is a powerful engine propelling the Pipe Insulation Market forward. With an upsurge in construction activities for data centers, power plants, and manufacturing facilities, the demand for effective pipe insulation is on the rise. These projects are not just about scaling operations; they’re about optimizing energy use and ensuring safety across complex systems.

Pipe insulation becomes indispensable in this context, providing a solution that significantly enhances energy efficiency and fire safety. As these sectors continue to grow, driven by digitalization, urbanization, and industrial advancements, the need for advanced insulation solutions becomes more pronounced. This trend does not only signify a growing market but also highlights the critical role of pipe insulation in modern infrastructures, marking a clear path for market expansion and innovation in product offerings.

Development of Advanced Insulation Materials Offers Growth Opportunity

The introduction of advanced insulation materials, such as aerogels and vacuum insulation panels (VIPs), marks a pivotal shift in the Pipe Insulation Market. These materials bring about a new era of thermal performance and energy efficiency. Aerogels, known for their low thermal conductivity and high heat resistance, and VIPs, offering superior insulation with minimal thickness, are revolutionizing the market. Their development drives innovation, opening up new avenues for applications where space is limited, and thermal efficiency is paramount.

As industries push for more sustainable and energy-efficient solutions, these advanced materials meet the demand head-on, offering significant improvements over traditional insulation products. This not only aligns with global sustainability goals but also presents substantial growth opportunities for manufacturers and suppliers in the Pipe Insulation Market, who are at the forefront of adopting and integrating these innovative materials into their solutions.

Trending Factors

Focus on Fire Safety and Regulatory Compliance Are Trending Factors

The increasing focus on fire safety and regulatory compliance has become a significant trending factor within the Pipe Insulation Market. With stringent building codes and regulations being implemented globally, there’s a heightened demand for pipe insulation solutions that are not only effective in thermal management but also offer fire resistance. This trend is driven by the need to minimize fire hazards in buildings and industrial settings, especially in high-risk areas where the insulation material can contribute to the spread of fire.

The market is responding with innovations in fire-resistant materials and designs that meet or exceed regulatory standards, ensuring safety and compliance. This trend reflects a broader industry shift towards safer, more sustainable building practices, positioning fire safety and compliance as key considerations in product development and selection.

Integration of Digital Technologies Are Trending Factors

The integration of digital technologies, notably Building Information Modeling (BIM) and asset management software, represents another key trending factor in the Pipe Insulation Market. These technologies are revolutionizing the way pipe insulation projects are planned, executed, and maintained. BIM allows for the detailed 3D printing and modeling of insulation systems within the broader context of a building’s architecture and mechanical systems, facilitating better design and coordination.

Asset management software enhances the maintenance aspect, enabling the tracking of insulation performance over time and optimizing operational efficiency. This digital transformation is driving efficiencies across the board, from reduced installation errors and project costs to improved lifetime performance of insulation systems. The adoption of these technologies signifies a shift towards more integrated, intelligent approaches to insulation, underscoring the industry’s readiness to embrace innovation for enhanced outcomes.

Regional Analysis

APAC Dominates with 38.6% Market Share

The Asia-Pacific (APAC) region, commanding a formidable 38.6% share of the Pipe Insulation Market, stands out due to its dynamic economic growth, rapid urbanization, and significant infrastructure development. The region’s dominance is underpinned by several key factors including booming construction activities, especially in emerging economies like China and India, which demand high volumes of pipe insulation for energy efficiency and fire safety in buildings and industrial facilities.

Additionally, the push towards greener buildings and the need for efficient energy management systems in the face of growing environmental concerns further fuel the demand for advanced pipe insulation solutions in APAC.

The regional market dynamics are shaped by the vast manufacturing base in APAC, coupled with increasing investments in infrastructure projects across residential, commercial, and industrial sectors. The presence of a large number of manufacturers and the availability of cost-effective labor also contribute to the region’s competitive advantage, making it a hotbed for pipe insulation products and technologies.

APAC’s influence on the global Pipe Insulation Market is expected to grow even further. The ongoing industrialization, along with stringent energy conservation regulations, will likely spur more innovations and demand within the market. This region’s aggressive pursuit of sustainability and energy efficiency, backed by government policies and incentives, positions it as a critical area for future market expansion and technological advancements.

Regional Market Shares

- North America: Following APAC, North America holds a significant market share, driven by stringent energy regulations and a focus on retrofitting aging infrastructure. Its market share is approximately 24.5%, underpinned by the region’s advanced technological adoption and focus on sustainability.

- Europe: Europe commands a market share of 21.9%, influenced by its aggressive energy efficiency directives and the renovation of old buildings to meet current insulation standards. The emphasis on reducing carbon emissions and enhancing building efficiencies contributes to the steady demand for pipe insulation.

- Middle East & Africa: This region, with a growing focus on infrastructure development and energy-efficient buildings, especially in the Gulf Cooperation Council (GCC) countries, holds a market share of 8.2%. The market is expected to see robust growth, driven by the construction boom and regulatory policies favoring energy conservation.

- Latin America: Latin America, though smaller in comparison, shows promise with a market share of 6.8%. The demand in this region is gradually increasing with urbanization and the need for energy-efficient infrastructure in countries like Brazil and Mexico.

Key Regions and Countries

- North America

- The US

- Canada

- Mexico

- Western Europe

- Germany

- France

- The UK

- Spain

- Italy

- Portugal

- Ireland

- Austria

- Switzerland

- Benelux

- Nordic

- Rest of Western Europe

- Eastern Europe

- Russia

- Poland

- The Czech Republic

- Greece

- Rest of Eastern Europe

- APAC

- China

- Japan

- South Korea

- India

- Australia & New Zealand

- Indonesia

- Malaysia

- Philippines

- Singapore

- Thailand

- Vietnam

- Rest of APAC

- Latin America

- Brazil

- Colombia

- Chile

- Argentina

- Costa Rica

- Rest of Latin America

- Middle East & Africa

- Algeria

- Egypt

- Israel

- Kuwait

- Nigeria

- Saudi Arabia

- South Africa

- Turkey

- United Arab Emirates

- Rest of MEA

Key Players Analysis

In the Pipe Insulation Market, the landscape is shaped by a diverse array of key players, each contributing to the industry’s growth and innovation. Companies like Armacell Group and Johns Manville Corporation lead with advanced insulation solutions, leveraging their extensive portfolios and global reach to meet the evolving needs of various industries. Owens Corning Inc. and Compagnie de Saint-Gobain SA stand out for their commitment to sustainability and energy efficiency, aligning their product offerings with global environmental standards.

Knauf Insulation GmbH and Rockwool International A/S focus on delivering high-quality, fire-resistant materials, catering to stringent building codes and fire safety requirements. BASF SE and Kingspan Group plc are recognized for their innovative approaches, integrating cutting-edge technologies and materials to enhance thermal performance and durability. Huntsman Corporation, Thermaflex, Paroc Group Oy, and L’Isolante K-Flex S.p.A. contribute with specialized products and solutions, targeting specific market segments and applications.

This competitive environment is characterized by strategic positioning aimed at sustainability, technological advancements, and global expansion. The impact of these companies is profound, driving forward the market with continuous product development and strategic alliances. Their market influence is further bolstered by a strong focus on R&D, customer-centric approaches, and adherence to regulatory standards. Together, these key players not only dominate the market landscape but also set the pace for future trends and market dynamics.

Market Key Players

- Armacell

- Johns Manville Corporation

- Owens Corning Inc.

- Compagnie de Saint-Gobain SA

- Knauf Insulation GmbH

- Rockwool International A/S

- BASF SE

- Kingspan Group plc

- Huntsman Corporation

- Thermaflex

- Paroc Group Oy

- L’Isolante K-Flex S.p.A.

Recent Developments

- On March 2024, ROCKWOOL Technical Insulation introduced ProRox® PS 965 with CR-TechTM, marking the industry’s first stone wool insulation with a built-in corrosion inhibitor.

- On September 2023, Perma-Pipe International Holdings, Inc. announced the opening of its second pipe insulating facility in Canada. The 37,000 square foot facility sits on three acres and is equipped with cutting-edge pipe insulating technology capable of producing a diverse range of pipe insulating products for various pipe sizes.

- On May 2023, Kingspan launched a new carbon calculator for pipe insulation, aiming to assist consultants in understanding how pipe insulation specifications can impact whole life carbon emissions and operating costs related to heat losses from pipework systems.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2023) | USD 9.8 Billion |

| Forecast Revenue (2033) | USD 16.4 Billion |

| CAGR (2024-2033) | 5.30% |

| Base Year for Estimation | 2023 |

| Historic Period | 2018-2023 |

| Forecast Period | 2024-2033 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Material Type (Cellular glass, Polyurethane & Polyisocyanurate Foam, Fiberglass, Elastomeric Foam, Others), By Insulation Type (Prefabricated Insulation, Rigid Board Insulation, Flexible Insulation, Loose Fill Insulation, Spray Foam Insulation), By Application (Industrial, Building & Construction, District Energy System, Others) |

| Regional Analysis | North America – The US, Canada, & Mexico; Western Europe – Germany, France, The UK, Spain, Italy, Portugal, Ireland, Austria, Switzerland, Benelux, Nordic, & Rest of Western Europe; Eastern Europe – Russia, Poland, The Czech Republic, Greece, & Rest of Eastern Europe; APAC – China, Japan, South Korea, India, Australia & New Zealand, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, & Rest of APAC; Latin America – Brazil, Colombia, Chile, Argentina, Costa Rica, & Rest of Latin America; Middle East & Africa – Algeria, Egypt, Israel, Kuwait, Nigeria, Saudi Arabia, South Africa, Turkey, United Arab Emirates, & Rest of MEA |

| Competitive Landscape | Armacell Group, Johns Manville Corporation, Owens Corning Inc., Compagnie de Saint-Gobain SA, Knauf Insulation GmbH, Rockwool International A/S, BASF SE, Kingspan Group plc, Huntsman Corporation, Thermaflex, Paroc Group Oy, L’Isolante K-Flex S.p.A. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |

Frequently Asked Questions (FAQ)

The Global Pipe Insulation Market is projected to be worth approximately USD 16.4 Billion by 2033, reflecting significant growth from USD 9.8 Billion in 2023, with a steady CAGR of 5.30% during the forecast period from 2024 to 2033.

The Pipe Insulation Market primarily serves the construction and industrial sectors, focusing on materials and technologies used to conserve energy and reduce heat loss in piping systems.

Key products in the Pipe Insulation Market include fiberglass, foam, and rubber insulation solutions, catering to the needs of piping systems for hot and cold services.

APAC leads the market with a dominant share, followed by North America and Europe. APAC's leadership is attributed to industrialization trends, while North America's strong presence is fueled by stringent energy regulations.

Major players in the Pipe Insulation Market include Armacell Group, Johns Manville Corporation, Owens Corning Inc., Compagnie de Saint-Gobain SA, Knauf Insulation GmbH, Rockwool International A/S, BASF SE, Kingspan Group plc, Huntsman Corporation, Thermaflex, Paroc Group Oy, and L'Isolante K-Flex S.p.A.