Quick Navigation

Report Overview

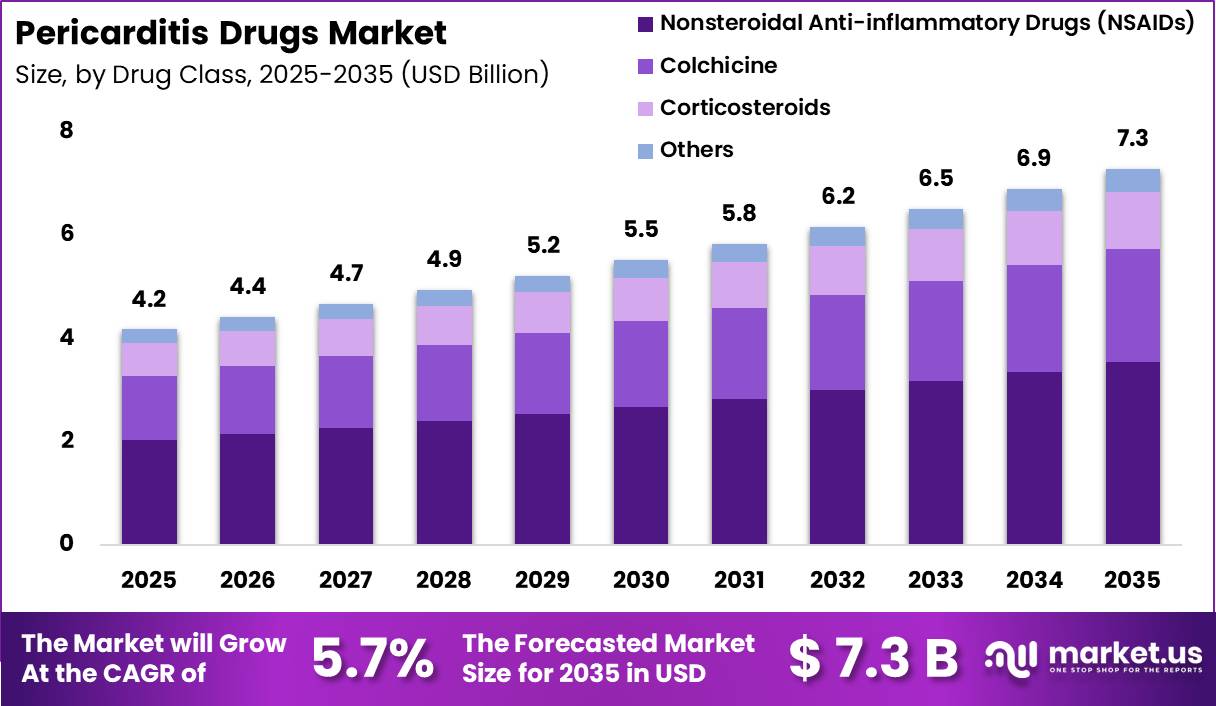

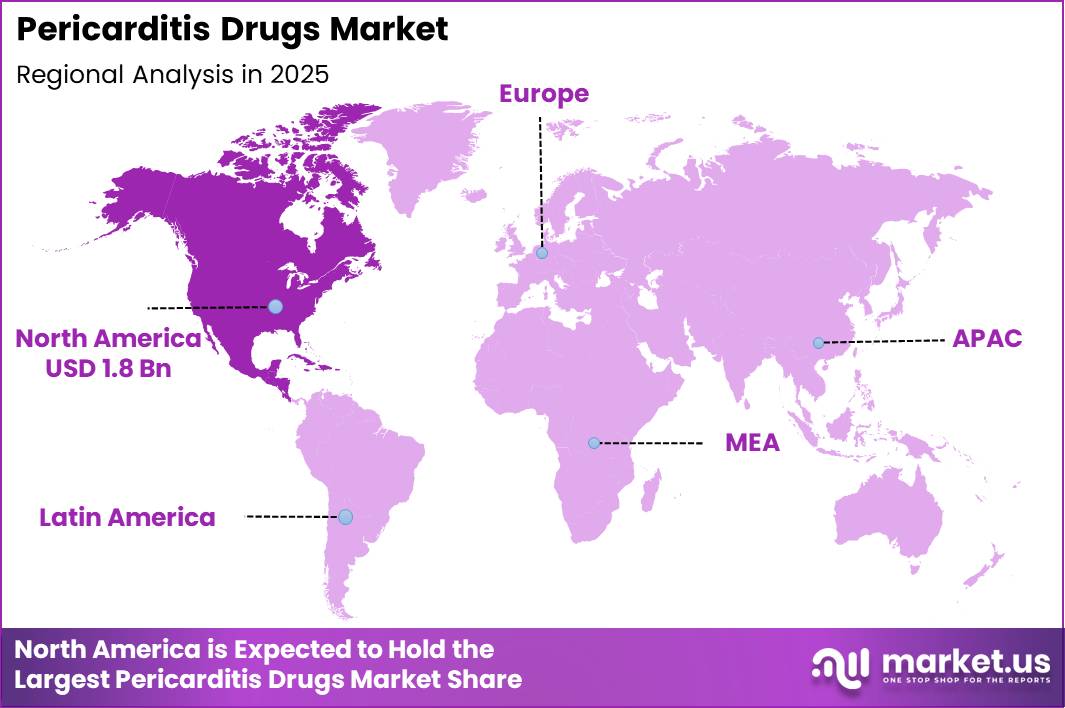

Global Pericarditis Drugs Market size is expected to be worth around US$ 7.3 Billion by 2035 from US$ 4.2 Billion in 2025, growing at a CAGR of 5.7% during the forecast period from 2026 to 2035. In 2025, North America led the market, achieving over 42.5% share with a revenue of US$ 1.8 Billion.

Pericarditis is an inflammatory disorder affecting the pericardium, the double-layered sac surrounding the heart. The condition may occur as acute, recurrent, chronic, or incessant pericarditis and is commonly associated with viral infections, autoimmune diseases, post-cardiac injury syndromes, and systemic inflammatory disorders. According to the U.S. National Heart, Lung, and Blood Institute (NHLBI), pericarditis can lead to serious complications such as pericardial effusion and cardiac tamponade if left untreated.

The pericarditis drugs market is driven by the growing diagnosis of inflammatory cardiovascular diseases, increasing awareness among healthcare professionals, and advancements in targeted anti-inflammatory therapies. Conventional treatment primarily consists of nonsteroidal anti-inflammatory drugs (NSAIDs), including ibuprofen and aspirin, combined with colchicine, which is widely recommended to reduce inflammation and lower recurrence rates. Corticosteroids are generally reserved for patients who do not respond adequately to first-line therapies or have specific underlying conditions.

From an epidemiological perspective, acute pericarditis has an annual incidence of approximately 0.03% in the general population and accounts for nearly 5% of chest pain admissions in emergency settings. Furthermore, about 15% to 30% of patients experience recurrent pericarditis, highlighting the need for long-term pharmacological management and creating sustained demand for effective therapeutic options. Approximately 10% of patients may require hospitalization, particularly in severe or recurrent cases.

Recent years have witnessed the emergence of novel biologic therapies targeting inflammatory pathways, particularly interleukin-1 (IL-1) inhibition, for recurrent and treatment-resistant pericarditis. These therapies are expanding treatment possibilities beyond traditional NSAIDs and corticosteroids and are improving disease management outcomes.

Increasing clinical research activities, favorable regulatory support for orphan and rare inflammatory conditions, and a growing focus on precision medicine are expected to support continued innovation in the pericarditis therapeutics landscape. As healthcare systems emphasize early diagnosis and recurrence prevention, demand for effective and targeted pericarditis drugs is anticipated to remain strong across both developed and emerging healthcare markets.

Key Takeaways

- Market Size: Global Pericarditis Drugs Market size is expected to be worth around US$ 7.3 Billion by 2035 from US$ 4.2 Billion in 2025.

- Market Share: The market growing at a CAGR of 5.7% during the forecast period from 2026 to 2035.

- Drug Class Analysis: NSAIDs dominated the market in 2025, accounting for 48.6% of the total market share.

- Route of Administration Analysis: The Oral segment dominated the market with a 76.4% share in 2025.

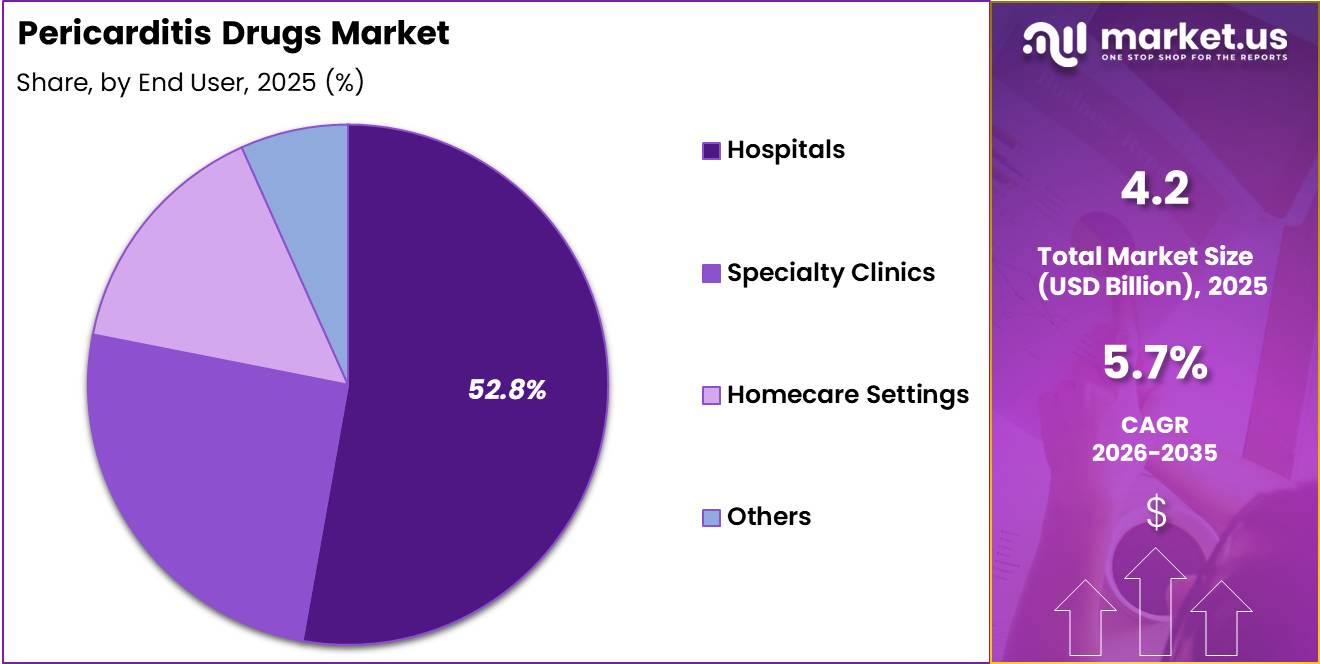

- End User Analysis: Hospitals dominated the market in 2025, accounting for 52.8% of total revenue.

- Regional Analysis: In 2025, North America dominated the global Pericarditis Drugs Market, accounting for over 42.5% of total market revenue and reaching approximately US$ 1.8 billion.

Drug Class Analysis

The drug class segment of the Pericarditis Drugs Market is categorized into Nonsteroidal Anti-inflammatory Drugs (NSAIDs), Colchicine, Corticosteroids, and Others. NSAIDs dominated the market in 2025, accounting for 48.6% of the total market share.

Their leading position is attributed to their role as the first-line treatment for acute pericarditis, owing to their proven effectiveness in reducing inflammation, chest pain, and associated symptoms. Widely prescribed agents such as ibuprofen and aspirin continue to be preferred because of their established safety profile, affordability, and broad clinical acceptance.

Colchicine represents the second-largest segment and is increasingly utilized in combination with NSAIDs to reduce recurrence rates and improve long-term patient outcomes. Growing clinical evidence supporting colchicine therapy has strengthened its adoption across treatment guidelines and healthcare settings.

The Corticosteroids segment maintains a significant market presence, particularly among patients who are intolerant to NSAIDs or colchicine or those with autoimmune-related pericarditis. Although effective, their use is generally reserved for specific cases due to concerns regarding adverse effects and higher recurrence risks.

The Others category includes emerging biologics, immunosuppressants, and supportive therapies. Continuous research into targeted anti-inflammatory treatments is expected to support segment expansion over the forecast period.

Route of Administration Analysis

Based on route of administration, the Pericarditis Drugs Market is segmented into Oral, Injectable, and Others. The Oral segment dominated the market with a 76.4% share in 2025, reflecting the widespread use of oral medications as the preferred treatment option for both acute and recurrent pericarditis.

Oral NSAIDs, colchicine, and corticosteroids offer convenient dosing, high patient compliance, ease of long-term therapy, and reduced healthcare costs compared with hospital-based treatment approaches. Their extensive availability across healthcare facilities and retail pharmacies further supports market leadership.

The Injectable segment holds a notable share of the market, primarily driven by its use in severe or complicated pericarditis cases requiring rapid therapeutic intervention. Injectable corticosteroids, biologics, and hospital-administered anti-inflammatory therapies are commonly utilized when oral administration is not feasible or when immediate symptom control is required. The increasing adoption of advanced injectable biologic therapies for recurrent and refractory pericarditis is contributing to segment growth.

The Others segment includes alternative administration methods utilized in specialized clinical scenarios. Although representing a smaller portion of the market, ongoing pharmaceutical innovation and the development of novel drug delivery systems are expected to create additional opportunities within this category during the forecast period.

End User Analysis

Based on end users, the Pericarditis Drugs Market is segmented into Hospitals, Specialty Clinics, Homecare Settings, and Others. Hospitals dominated the market in 2025, accounting for 52.8% of total revenue. Their leading position is primarily attributed to the high volume of pericarditis diagnoses and treatments conducted within hospital settings, particularly for acute, recurrent, and severe cases requiring comprehensive cardiac evaluation. Access to advanced diagnostic technologies, specialist cardiology teams, and emergency care services enables hospitals to remain the primary treatment centers for pericarditis management.

Specialty Clinics represent the second-largest segment, benefiting from increasing referrals to cardiology-focused centers for ongoing monitoring and management of recurrent pericarditis. These facilities provide specialized expertise, personalized treatment plans, and follow-up care, supporting improved patient outcomes and driving segment growth.

The Homecare Settings segment is experiencing steady expansion due to growing adoption of oral therapies and increased emphasis on outpatient disease management. Improved patient awareness, telemedicine integration, and healthcare cost-containment initiatives are encouraging treatment outside traditional hospital environments.

The Others category includes ambulatory care centers and community healthcare facilities. Rising accessibility to cardiovascular care services and expanding healthcare infrastructure in emerging economies are expected to contribute to the growth of this segment throughout the forecast period.

Key Market Segments

By Drug Class

- Nonsteroidal Anti-inflammatory Drugs (NSAIDs)

- Colchicine

- Corticosteroids

- Others

By Route of Administration

- Oral

- Injectable

- Others

By End User

- Hospitals

- Specialty Clinics

- Homecare Settings

- Others

Market Dynamics

Driving Factors - Increasing Burden of Recurrent Pericarditis Creating Demand for Advanced Therapies

The growth of the Pericarditis Drugs Market is being supported by the persistent clinical challenges associated with recurrent pericarditis. Despite the availability of standard treatment options, a subset of patients continues to experience repeated disease episodes, prolonged symptoms, and treatment dependency. This ongoing unmet medical need has encouraged the adoption of advanced therapeutic approaches aimed at improving long-term disease control.

Healthcare providers are increasingly focusing on recurrence prevention and sustained symptom management, creating greater demand for therapies that offer improved efficacy and reduced treatment-related complications. Growing awareness among cardiologists and enhanced disease recognition are further contributing to market expansion.

Trending Factors - Shift Toward Targeted Biologic and Precision-Based Treatment Approaches

A major trend shaping the Pericarditis Drugs Market is the growing preference for targeted biologic therapies designed to address specific inflammatory mechanisms involved in disease progression. Advances in the understanding of pericardial inflammation have accelerated the development of therapies that provide more precise disease control compared with conventional anti-inflammatory treatments.

The increasing emphasis on personalized medicine is encouraging the use of treatment strategies tailored to individual patient profiles. Healthcare providers are also seeking alternatives that minimize long-term corticosteroid exposure and associated adverse effects. As a result, pharmaceutical companies continue to invest in innovative cytokine-targeting therapies and next-generation immunomodulators, which are expected to transform future treatment practices.

Restraining Factors - High Cost and Limited Accessibility of Advanced Biologic Therapies

The market continues to face challenges related to the affordability and accessibility of advanced biologic treatments. Reimbursement limitations, healthcare budget constraints, and restricted availability across several developing regions can limit patient access to newer therapies.

In addition, safety monitoring requirements and concerns regarding potential treatment-related adverse events may affect prescribing decisions. The relatively specialized patient population associated with recurrent pericarditis may also influence commercial expansion opportunities, creating barriers to widespread adoption of premium therapeutic options.

Opportunity - Development of Next-Generation Immunomodulatory Therapies

Significant growth opportunities exist in the development of novel therapies that target the underlying inflammatory drivers of pericarditis. Ongoing research into disease mechanisms is supporting the discovery of innovative treatment approaches capable of delivering more durable clinical outcomes.

Advancements in biomarker identification, cardiac imaging technologies, and patient stratification methods are expected to enhance treatment selection and optimize therapeutic effectiveness. Furthermore, increasing investment in inflammatory cardiovascular disease research and the broader adoption of precision medicine approaches are creating favorable conditions for the introduction of new biologics, combination therapies, and personalized treatment solutions.

Regional Analysis

In 2025, North America dominated the global Pericarditis Drugs Market, accounting for over 42.5% of total market revenue and reaching approximately US$ 1.8 billion. The region’s leadership is primarily attributed to the high prevalence of cardiovascular and inflammatory disorders, advanced healthcare infrastructure, strong pharmaceutical research capabilities, and widespread access to innovative therapies. Favorable reimbursement policies, increased disease awareness, and the presence of major pharmaceutical companies further support market growth across the United States and Canada.

Europe represented the second-largest regional market, driven by a well-established healthcare system, growing adoption of targeted therapies, and increasing investments in cardiovascular disease management. Countries such as Germany, the United Kingdom, France, and Italy continue to witness steady demand for pericarditis treatments due to an aging population and rising healthcare expenditure.

The Asia Pacific region is expected to register the fastest growth during the forecast period. Rapid improvements in healthcare infrastructure, expanding patient populations, increasing healthcare spending, and greater awareness of inflammatory heart conditions are fueling market expansion across China, India, Japan, and South Korea. Additionally, government initiatives aimed at improving access to advanced treatments are creating new growth opportunities.

Latin America and the Middle East & Africa are anticipated to experience moderate growth. Expanding healthcare access, gradual improvements in diagnostic capabilities, and increasing investments in healthcare systems are expected to support the adoption of pericarditis drugs across these emerging markets.

Key Regions and Countries

North America

- The US

- Canada

Europe

- Germany

- France

- The U.K.

- Italy

- Spain

- Russia & CIS

- Rest of Europe

Asia Pacific

- China

- India

- Japan

- South Korea

- ASEAN

- Australia & New Zealand

- Rest of Asia Pacific

Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

Latin America

- Brazil

- Mexico

- Rest of Latin America

Key Players Analysis

The Pericarditis Drugs Market is characterized by the presence of several leading pharmaceutical companies focused on expanding their cardiovascular and anti-inflammatory treatment portfolios. Key market participants are actively investing in research and development activities to improve treatment efficacy, reduce recurrence rates, and address unmet clinical needs associated with recurrent and acute pericarditis. Strategic initiatives such as product approvals, clinical trials, partnerships, licensing agreements, and geographic expansion remain central to maintaining competitive positions.

Major players including Novartis, Pfizer, AbbVie, AstraZeneca are strengthening their market presence through innovative therapies targeting inflammatory pathways linked to pericarditis. The growing adoption of biologic drugs and interleukin-1 inhibitors has intensified competition, encouraging companies to develop advanced treatment options with improved safety profiles.

Furthermore, collaborations between pharmaceutical firms and research institutions are accelerating drug development activities. As awareness of pericarditis increases and diagnostic rates improve globally, leading companies are expected to benefit from expanding patient pools and growing demand for targeted therapies throughout the forecast period.

Market Key Players

- Bayer AG

- Pfizer Inc.

- Novartis AG

- Merck & Co., Inc.

- Takeda Pharmaceutical Company Limited

- Mylan N.V. (Viatris)

- Teva Pharmaceutical Industries Ltd.

- Sun Pharmaceutical Industries Ltd.

- Dr. Reddy’s Laboratories Ltd.

- Lupin Limited

- Cipla Inc.

- Apotex Inc.

- Hikma Pharmaceuticals PLC

- Fresenius Kabi AG

- Endo International plc

- Others

Recent Developments

- February 2025 – Novartis AG announced an agreement to acquire Anthos Therapeutics for an upfront payment of USD 925 million. The acquisition strengthens Novartis’ late-stage cardiovascular pipeline through the addition of abelacimab, a Phase III asset targeting thromboembolic disorders. The transaction reflects the company’s continued focus on expanding its cardiovascular and inflammation portfolio, which may support future opportunities in related cardiac inflammatory conditions.

- October 2025 – Takeda Pharmaceutical Company Limited expanded its long-standing collaboration with AI-driven biotechnology company Nabla Bio. The multi-year agreement includes upfront and research payments along with potential milestone payments exceeding USD 1 billion. The partnership is intended to accelerate the discovery of novel biologics across Takeda’s therapeutic pipeline, including inflammation-focused programs.

- May 2026 – Bayer AG announced the acquisition of Perfuse Therapeutics in a deal valued at up to USD 2.45 billion. The acquisition is designed to strengthen Bayer’s specialty pharmaceutical pipeline and expand its innovation capabilities in ophthalmology. The move demonstrates Bayer’s renewed focus on targeted acquisitions to enhance long-term growth and diversify its therapeutic portfolio.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | US$ 4.2 Billion |

| Forecast Revenue (2035) | US$ 7.3 Billion |

| CAGR (2026-2035) | 42.5% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Drug Class (Nonsteroidal Anti-inflammatory Drugs (NSAIDs), Colchicine, Corticosteroids, Others) By Route of Administration (Oral, Injectable, Others) By End User (Hospitals, Specialty Clinics, Homecare Settings, Others) |

| Regional Analysis | North America – The US, Canada; Europe – Germany, France, U.K., Italy, Spain, Russia & CIS, Rest of Europe; Asia Pacific – China, India, Japan, South Korea, ASEAN, Australia & New Zealand, Rest of Asia Pacific; Middle East & Africa – GCC, South Africa, Rest of Middle East & Africa; Latin America – Brazil, Mexico, Rest of Latin America |

| Competitive Landscape | Bayer AG, Pfizer Inc., Novartis AG, Merck & Co., Inc., Takeda Pharmaceutical Company Limited, Mylan N.V. (Viatris), Teva Pharmaceutical Industries Ltd., Sun Pharmaceutical Industries Ltd., Dr. Reddy’s Laboratories Ltd., Lupin Limited, Cipla Inc., Apotex Inc., Hikma Pharmaceuticals PLC, Fresenius Kabi AG, Endo International plc, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |