Global Pen And Injector Drug Delivery Devices Market By Product (Pen Injectors (Disposable Pens and Reusable Pens), Autoinjectors, On-Body/Wearable Injectors, Needle-Free Injectors (Jet Injectors) and Others), By Therapeutic Use (Autoimmune Disorders, Hormonal Disorders, Oncology, Obesity, Diabetes Mellitus and Others), By End Use (Hospitals, Homecare Settings and Others), Region and Companies – Industry Segment Outlook, Market Assessment, Competition Scenario, Trends and Forecast 2026-2035

- Published date: March 2026

- Report ID: 180649

- Number of Pages: 386

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

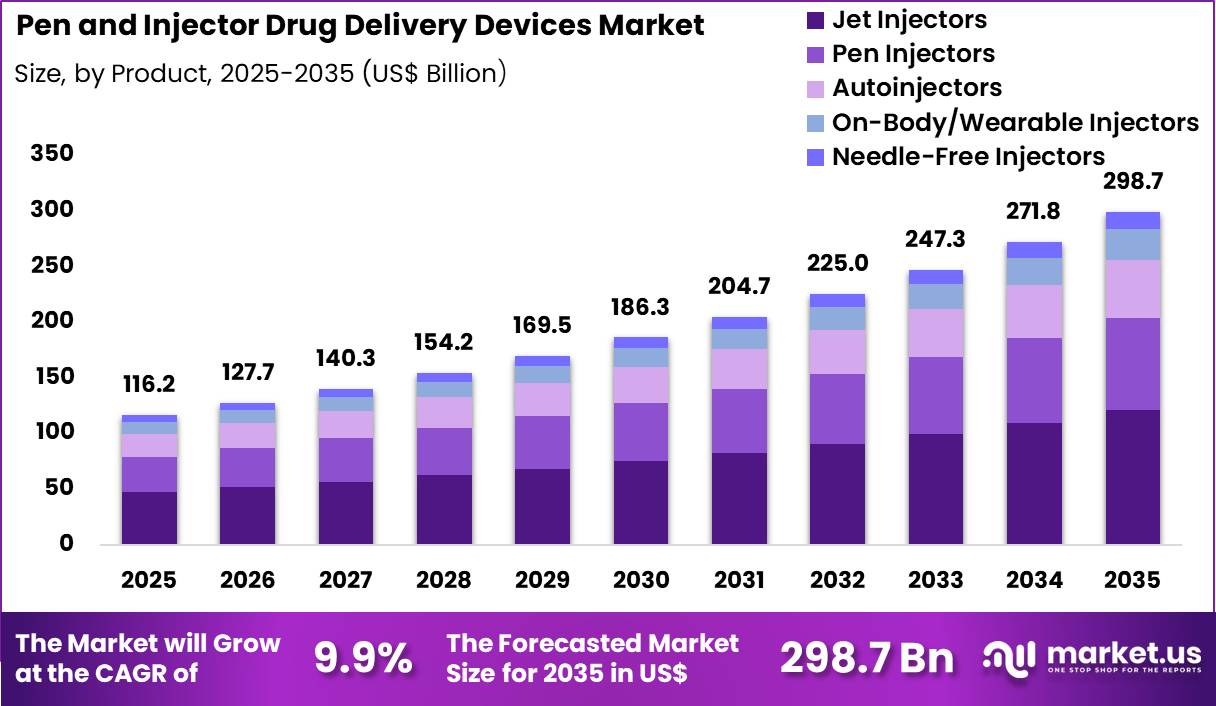

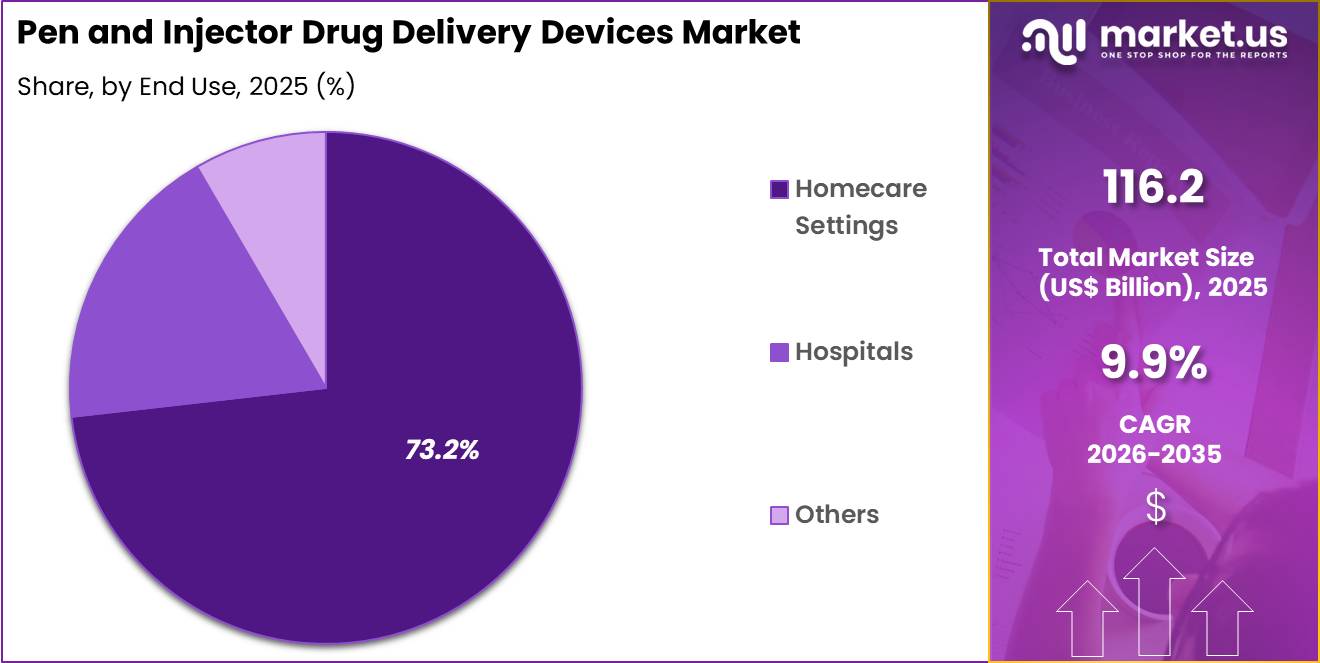

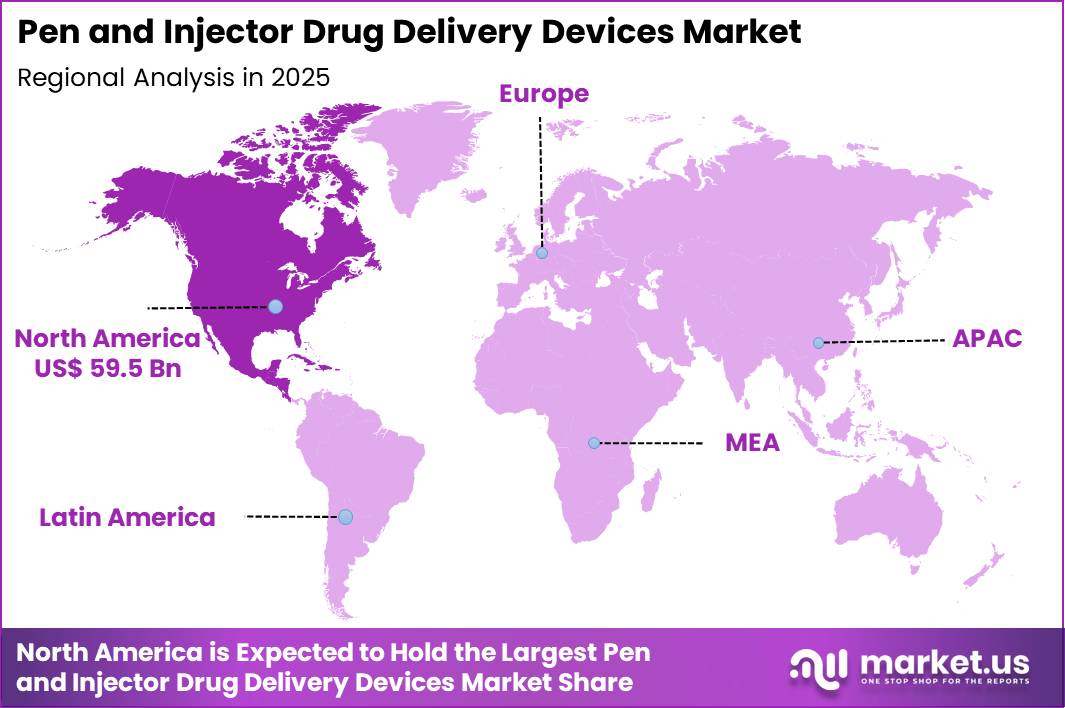

The Global Pen And Injector Drug Delivery Devices Market size is expected to be worth around US$ 298.7 Billion by 2035 from US$ 116.2 Billion in 2025, growing at a CAGR of 9.9% during the forecast period 2026-2035. In 2025, North America led the market, achieving over 51.2% share with a revenue of US$ 59.5 Billion.

Increasing demand for self-administered therapies and patient-centered treatment options propels the Pen and Injector Drug Delivery Devices market as pharmaceutical companies and healthcare providers prioritize convenient, accurate devices that enhance adherence and therapeutic outcomes.

Patients with diabetes increasingly rely on insulin pens to administer precise basal and bolus doses multiple times daily, enabling flexible meal-time adjustments and better glycemic control through dialable mechanisms and memory features. These devices support growth hormone therapy in pediatric and adult patients with deficiency disorders, where reusable or disposable pens deliver consistent subcutaneous injections with minimal discomfort.

Rheumatologists prescribe autoinjectors for biologic therapies in rheumatoid arthritis and psoriasis, allowing patients to self-administer TNF inhibitors or IL-17 antagonists at home with prefilled, spring-loaded systems that reduce injection anxiety.

In emergency settings, epinephrine autoinjectors provide rapid, life-saving treatment for anaphylaxis, delivering intramuscular doses with audible activation cues and safety mechanisms to prevent accidental needle sticks. Patients with migraine disorders utilize on-demand autoinjectors for CGRP antagonists or triptans, achieving fast relief from acute attacks through portable, ready-to-use designs.

Manufacturers pursue opportunities to develop smart pens and injectors with Bluetooth connectivity and dose-tracking apps, expanding applications in chronic disease management where real-time data sharing improves physician oversight and patient engagement.

Developers advance needle-free or microneedle-based injectors that minimize pain and tissue trauma, broadening utility in pediatric growth hormone administration and vaccine delivery. These innovations facilitate integration with digital health platforms for adherence reminders and telemedicine consultations.

Opportunities emerge in high-viscosity biologic formulations requiring powered injectors, addressing delivery challenges in autoimmune and oncology therapies. Companies invest in ergonomic, low-force activation designs that enhance usability for elderly or dexterity-impaired patients. In May 2025, IDE Group introduced OKO, an auto-injector designed for ophthalmic drug delivery.

Developed in collaboration with ophthalmology specialists from Australia, the US, and Europe, the system aims to improve dosing precision and streamline intravitreal injection procedures used in the treatment of retinal diseases, while also helping reduce treatment time and operational costs in clinical settings. Recent trends emphasize sustainability through recyclable components and user-centric features that support long-term self-administration across diverse therapeutic areas.

Key Takeaways

- In 2025, the market generated a revenue of US$ 116.2 Billion, with a CAGR of 9.9%, and is expected to reach US$ 298.7 Billion by the year 2035.

- The product segment is divided into pen injectors, autoinjectors, on-body/wearable injectors, needle-free injectors and others, with jet injectors taking the lead with a market share of 40.4%.

- Considering therapeutic use, the market is divided into autoimmune disorders, hormonal disorders, oncology, obesity, diabetes mellitus and others. Among these, diabetes mellitus held a significant share of 56.1%.

- Furthermore, concerning the end use segment, the market is segregated into hospitals, homecare settings and others. The homecare settings sector stands out as the dominant player, holding the largest revenue share of 73.2% in the market.

- North America led the market by securing a market share of 51.2%.

Product Analysis

Jet injectors accounted for 40.4% of growth within product and dominate the pen and injector drug delivery devices market due to their ability to deliver medications without traditional needles. Healthcare providers increasingly promote needle-free injection technologies to improve patient comfort and reduce needle-related anxiety.

Jet injectors deliver drugs through high-pressure streams that penetrate the skin and enable rapid absorption. Segment growth is expected to strengthen as pharmaceutical companies develop formulations compatible with needle-free systems. Rising demand for painless drug administration supports adoption among patients requiring frequent injections.

Public health agencies also encourage technologies that reduce accidental needle injuries and contamination risks. Manufacturers continue to enhance precision and dose control within modern jet injector systems. Demand is anticipated to expand as healthcare systems prioritize safer and more convenient drug delivery options.

Therapeutic Use Analysis

Diabetes mellitus accounted for 56.1% of growth within therapeutic use and dominate the market due to the widespread need for regular insulin administration. The International Diabetes Federation estimates that more than 500 million adults live with diabetes worldwide, which creates substantial demand for injection-based drug delivery solutions.

Patients require frequent insulin dosing to maintain stable blood glucose levels. Pen and injector devices support accurate dose delivery and improved treatment adherence. Segment growth is projected to strengthen as diabetes prevalence continues to rise due to aging populations and lifestyle factors.

Healthcare providers increasingly recommend advanced injector systems to improve patient self-management. Pharmaceutical companies also introduce user-friendly insulin delivery devices designed for home administration. Demand is likely to increase as diabetes treatment programs expand across both developed and emerging healthcare systems.

End-Use Analysis

Homecare settings accounted for 73.2% of growth within end use and dominate the pen and injector drug delivery devices market due to the increasing shift toward self-administration of medications. Patients increasingly prefer convenient drug delivery methods that support treatment outside hospital environments.

Homecare injection devices allow individuals to manage chronic diseases without frequent clinical visits. Segment growth is expected to accelerate as healthcare systems encourage home-based care to reduce treatment costs and hospital congestion. Many chronic conditions such as diabetes, autoimmune diseases, and hormonal disorders require long-term injectable therapies. Easy-to-use injector devices improve treatment adherence and patient independence.

Demand is anticipated to rise as remote healthcare services and telemedicine programs expand globally. Continuous improvements in device ergonomics and digital monitoring technologies further support the widespread adoption of injector devices in homecare settings.

Key Market Segments

By Product

- Pen Injectors

- Disposable Pens

- Reusable Pens

- Autoinjectors

- On-Body/Wearable Injectors

- Needle-Free Injectors

- Jet Injectors

- Others

By Therapeutic Use

- Autoimmune Disorders

- Hormonal Disorders

- Oncology

- Obesity

- Diabetes Mellitus

- Others

By End Use

- Hospitals

- Homecare Settings

- Others

Drivers

Strong growth in Ypsomed Delivery Systems revenue is driving the market.

Ypsomed AG’s Delivery Systems segment, encompassing pen injectors and auto-injectors, recorded revenue of CHF 308 million in fiscal year 2022/23. This advanced to CHF 385 million in fiscal year 2023/24, reflecting a 25% increase. Fiscal year 2024/25 revenue reached CHF 501 million, marking a 30% rise from the prior year.

The progression highlights escalating demand for user-friendly self-injection devices in diabetes and biologic therapies. Manufacturers capitalize on this momentum to scale production of customizable pen platforms. Healthcare providers favor these systems for enhancing patient adherence through precise dosing mechanisms.

The revenue trajectory supports research into ergonomic enhancements and digital integration. Global distribution networks expand to meet institutional procurement needs. Such financial performance validates the clinical efficacy of advanced injector designs. This driver underpins sustained innovation and market penetration for pen and injector technologies.

Restraints

Declining growth rates in Ozempic net sales is restraining the market.

Novo Nordisk A/S reported Ozempic net sales of DKK 59,750 million in 2022. The figure climbed to DKK 95,718 million in 2023, achieving approximately 60 percent year-over-year growth. In 2024, sales totaled DKK 120,342 million, with growth moderating to 26 percent. First-half 2025 sales reached DKK 9,456 million, suggesting full-year expansion below 10 percent based on trajectory.

The slowdown tempers expectations for proportional increases in associated pen device volumes. Supply chain optimizations face pressure from stabilized demand signals in mature markets. Producers adjust manufacturing forecasts to align with tempered biologic uptake.

Reimbursement dynamics contribute to cautious prescribing patterns for high-cost injectables. The pattern influences investment prioritization away from rapid scale-up initiatives. This restraint moderates the overall velocity of sector advancement during the 2022-2025 interval.

Opportunities

Collaboration between Ypsomed and Becton Dickinson for high-viscosity self-injection systems is creating growth opportunities.

Ypsomed AG and Becton Dickinson and Company announced a collaboration on October 23, 2024, to develop advanced self-injection platforms. The partnership targets delivery of high-viscosity biologics through optimized pen and injector designs. Opportunities arise for breakthrough solutions addressing formulation challenges in oncology and immunology.

Developers integrate force-minimizing mechanisms to improve user experience in subcutaneous administration. The alliance enables shared expertise in regulatory pathways for next-generation devices. Market segments underserved by current viscosity limits gain accessible innovations. Providers anticipate reduced injection-site reactions through refined needle technologies.

The initiative supports scalable manufacturing for emerging therapeutic pipelines. Such frameworks foster joint marketing efforts in global tenders. This opportunity enhances competitive positioning and long-term revenue diversification in drug delivery.

Impact of Macroeconomic / Geopolitical Factors

Macroeconomic conditions influence the pen and injector drug delivery devices market through healthcare spending patterns, insurance reimbursement, and pharmaceutical company investment decisions. Inflation raises costs for precision plastics, springs, needles, and assembly processes used in injector manufacturing.

Higher interest rates reduce capital flexibility for device developers and contract manufacturers, which can slow facility expansion and production scaling. Geopolitical tensions disrupt sourcing of specialized components and medical grade materials, creating uncertainty in supply continuity.

Current US tariffs on imported device parts and manufacturing equipment increase production expenses for suppliers serving the US market. These pressures can tighten margins and delay procurement agreements with pharmaceutical partners.

At the same time, companies expand domestic manufacturing capacity and strengthen supplier diversification to improve supply stability. Growing demand for self-administration therapies and chronic disease management continues to support steady and confident market growth.

Latest Trends

FDA clearance of the GO-PEN reusable insulin pen injector is driving the market.

The U.S. Food and Drug Administration issued 510(k) clearance for the GO-PEN on April 24, 2025. This reusable device facilitates self-injection of NovoLog insulin from 10 ml vials using a 1.3 ml reservoir. The clearance classifies it as a Class II medical device under product code FMF. Users can administer doses from 1 to 60 units in 1-unit increments over up to three days.

The pen employs standard luer lock needles and supports room-temperature storage up to 30°C. Substantial equivalence was demonstrated to the predicate HumaPen Savvio without clinical studies. This approval expands options for cost-effective, vial-to-pen transfer in diabetes management.

Practitioners value the durability and simplicity for patient empowerment. The 2025 milestone aligns with trends toward sustainable, refillable injectors. Overall, the clearance accelerates adoption of versatile pen systems in routine care.

Regional Analysis

North America is leading the Pen And Injector Drug Delivery Devices Market

North America accounted for 51.2% of the pen and injector drug delivery devices market in 2025 as healthcare systems increasingly adopted self-administration technologies for chronic disease management. The region has experienced strong demand for convenient injectable delivery solutions used in diabetes, autoimmune disorders, and hormone therapies.

According to the Centers for Disease Control and Prevention, about 38.4 million people in the United States were living with diabetes in 2023, creating sustained clinical demand for easy-to-use insulin administration tools that support long-term disease control.

Healthcare providers across the United States and Canada have encouraged patients to transition toward self-injectable therapies that reduce hospital visits and support home-based treatment models. Pharmaceutical companies are also expanding biologic and specialty drug portfolios that require precise and user-friendly injection systems.

Technological improvements such as dose memory, digital connectivity, and ergonomic designs have enhanced patient adherence and injection accuracy. Insurance reimbursement policies and patient assistance programs have improved access to advanced delivery systems.

Hospitals and diabetes education programs increasingly train patients to use pen-based devices safely and effectively. Strong collaboration between pharmaceutical firms and device manufacturers has further strengthened product innovation and clinical adoption across North America.

The Asia Pacific region is expected to experience the highest CAGR during the forecast period

Asia Pacific is expected to witness substantial expansion during the forecast period as rising chronic disease prevalence and healthcare modernization drive demand for convenient injectable therapies. The International Diabetes Federation reported that 206 million adults were living with diabetes in the Western Pacific region in 2023, representing one of the largest patient populations requiring regular insulin administration.

Rapid urbanization, changing dietary habits, and sedentary lifestyles are contributing to increasing diabetes incidence across countries such as China, India, and Indonesia. Healthcare providers across the region are promoting self-management strategies that encourage patients to administer medication at home rather than relying solely on hospital visits.

Governments are expanding national diabetes management programs and improving access to essential medicines and treatment technologies. Pharmaceutical companies are introducing more biologic therapies and insulin formulations that rely on precision injection systems for safe administration.

Medical device manufacturers are also developing affordable injection platforms tailored for regional healthcare settings. Growing digital health ecosystems are supporting patient education, medication tracking, and remote care guidance. These combined developments are expected to strengthen adoption of modern injectable therapy delivery technologies throughout Asia Pacific.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherland

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- New Zealand

- Singapore

- Thailand

- Vietnam

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

Leading companies in the Pen And Injector Drug Delivery Devices market pursue expansion through continuous technological innovation, wider global distribution, and strategic collaborations with pharmaceutical manufacturers that require advanced injection platforms.

Firms increasingly develop smart injector systems with digital connectivity, dose-tracking features, and improved safety mechanisms to enhance patient adherence and treatment accuracy. Rising demand for convenient self-administration devices for chronic conditions such as diabetes also encourages manufacturers to strengthen research and product design capabilities.

Novo Nordisk represents a prominent participant in the Pen And Injector Drug Delivery Devices market and operates as a Denmark-based pharmaceutical company that focuses on therapies for diabetes, obesity, and other chronic diseases. The company develops insulin pens and injection technologies designed to simplify medication delivery and support long-term disease management for patients worldwide.

Industry competitors also expand their market reach through product launches, digital health integration, and partnerships with healthcare providers to strengthen adoption of advanced injector platforms across global healthcare systems.

Top Key Players

- Novo Nordisk A/S

- Sanofi

- Eli Lilly and Company

- AstraZeneca plc

- Pfizer, Inc.

- Merck KGaA

- Teva Pharmaceuticals

- Amgen, Inc.

- Ferring Pharmaceuticals

- AbbVie Inc.

Recent Developments

- In October 2025, Stevanato Group expanded its drug delivery device manufacturing capabilities at its Bad Oeynhausen facility in Germany by adding more than 2,500 square meters of production space. The upgrade includes an ISO 8 cleanroom dedicated to injection molding and automated assembly operations, strengthening the company’s ability to support large-scale production of autoinjector and pen injector platforms while improving supply chain reliability in Europe.

- In September 2025, Apiject Systems submitted a New Drug Application to the US Food and Drug Administration for an injectable medicine delivered through its single-use, prefilled plastic syringe platform. The submission involved glycopyrrolate administered using Apiject’s proprietary device, which integrates Blow-Fill-Seal packaging with precision-molded needle hubs to enable scalable domestic manufacturing.

Report Scope

Report Features Description Market Value (2025) US$ 116.2 Billion Forecast Revenue (2035) US$ 298.7 Billion CAGR (2026-2035) 9.9% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments Segments Covered By Product (Pen Injectors (Disposable Pens and Reusable Pens), Autoinjectors, On-Body/Wearable Injectors, Needle-Free Injectors (Jet Injectors) and Others), By Therapeutic Use (Autoimmune Disorders, Hormonal Disorders, Oncology, Obesity, Diabetes Mellitus and Others), By End Use (Hospitals, Homecare Settings and Others) Regional Analysis North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA Competitive Landscape Novo Nordisk A/S, Sanofi, Eli Lilly and Company, AstraZeneca plc, Pfizer, Inc., Merck KGaA, Teva Pharmaceuticals, Amgen, Inc., Ferring Pharmaceuticals, AbbVie Inc. Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)  Pen And Injector Drug Delivery Devices MarketPublished date: March 2026add_shopping_cartBuy Now get_appDownload Sample

Pen And Injector Drug Delivery Devices MarketPublished date: March 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- Novo Nordisk A/S

- Sanofi

- Eli Lilly and Company

- AstraZeneca plc

- Pfizer, Inc.

- Merck KGaA

- Teva Pharmaceuticals

- Amgen, Inc.

- Ferring Pharmaceuticals

- AbbVie Inc.

Our Clients

- 180649

- March 2026