Quick Navigation

Report Overview

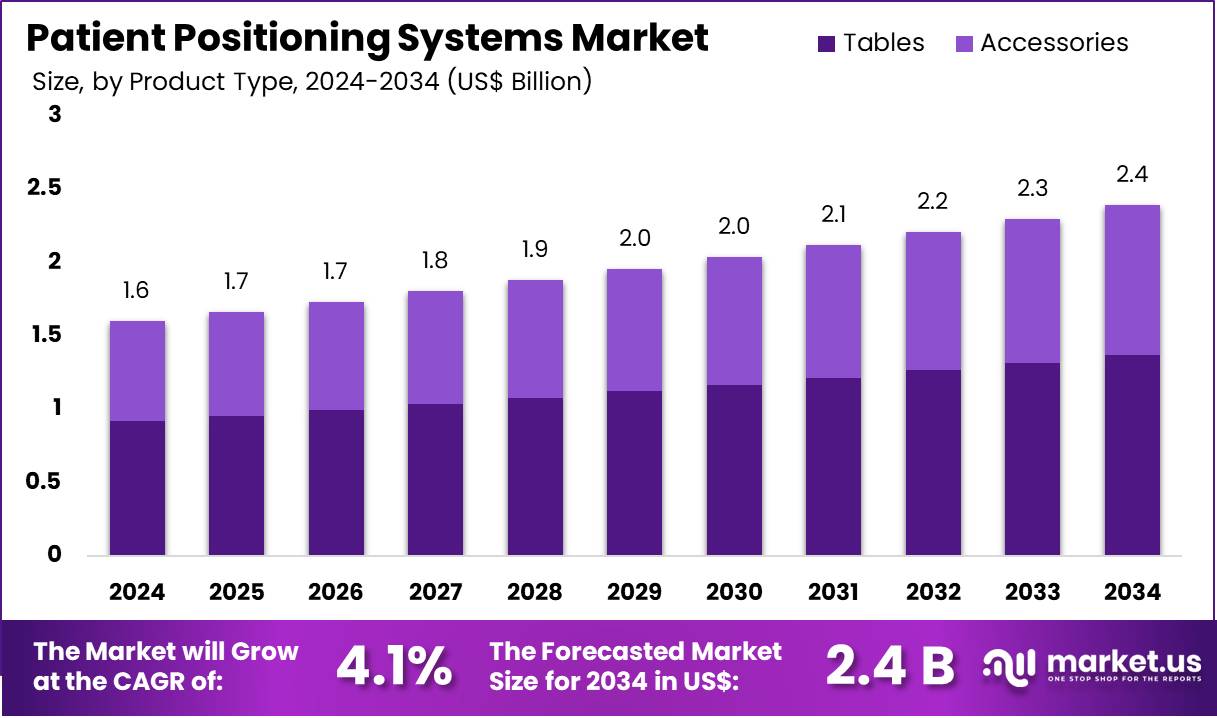

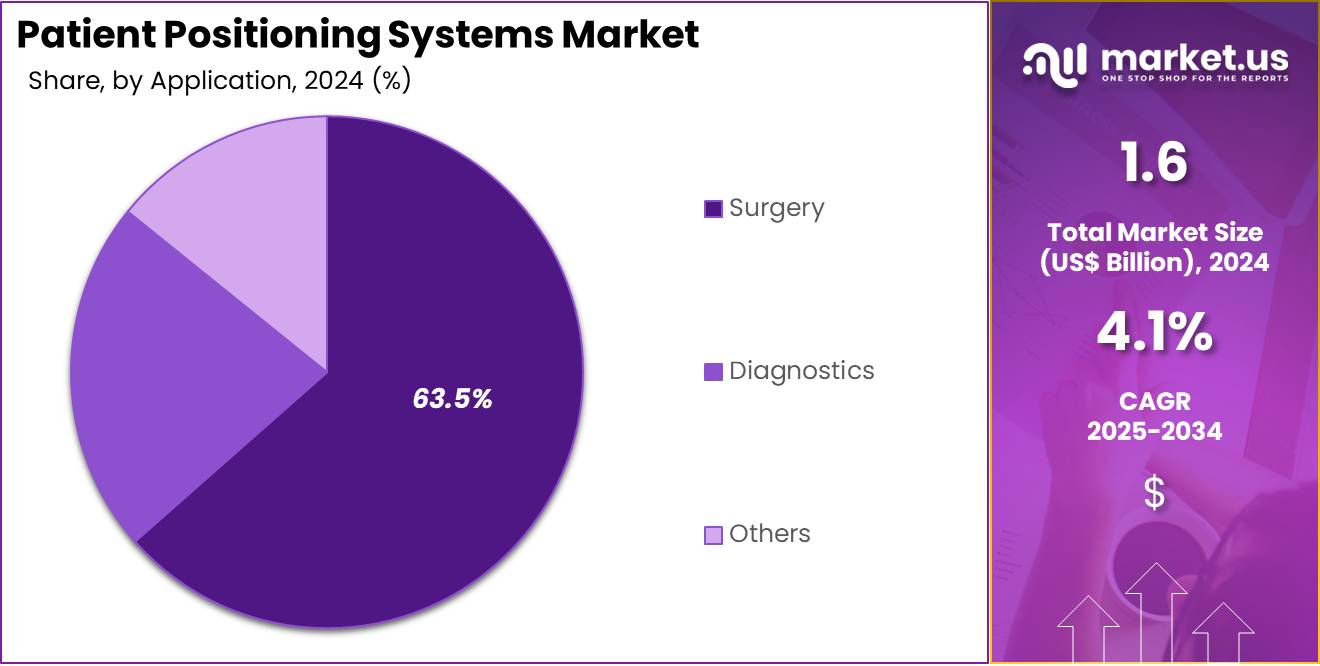

The Global Patient Positioning Systems Market size is expected to be worth around US$ 2.4 Billion by 2034, from US$ 1.6 Billion in 2024, growing at a CAGR of 4.1% during the forecast period from 2025 to 2034.

Increasing demand for precision and safety in medical procedures is driving the growth of the patient positioning systems market. As healthcare providers focus on improving patient care and outcomes, the need for advanced positioning systems has surged across various sectors, including radiology, surgery, and diagnostics. Patient positioning systems play a critical role in ensuring accurate imaging, reducing risks during procedures, and enhancing overall patient comfort.

Innovations in these systems focus on improving ease of use, durability, and compatibility with different medical imaging devices. Hospitals and outpatient centers increasingly rely on these systems to optimize workflow, improve recovery rates, and prevent complications during treatment. In February 2023, GMG Medical Equipment began supplying commercial-grade medical beds specifically designed to cater to outpatient care. These beds assist in the smooth transition from hospital to home, helping improve patient recovery and comfort during the process, thus supporting the growing demand for advanced patient positioning solutions.

Key Takeaways

- In 2024, the market for Patient Positioning Systems generated a revenue of US$ 1.6 billion, with a CAGR of 4.1%, and is expected to reach US$ 2.4 billion by the year 2034.

- The product type segment is divided into tables and accessories, with tables taking the lead in 2024with a market share of 57.4%.

- Considering application, the market is divided into surgery, diagnostics, and others. Among these, surgery held a significant share of 63.5%.

- Furthermore, concerning the end-user segment, the market is segregated into hospitals, ambulatory centers, and others. The hospitals sector stands out as the dominant player, holding the largest revenue share of 59.8% in the Patient Positioning Systems market.

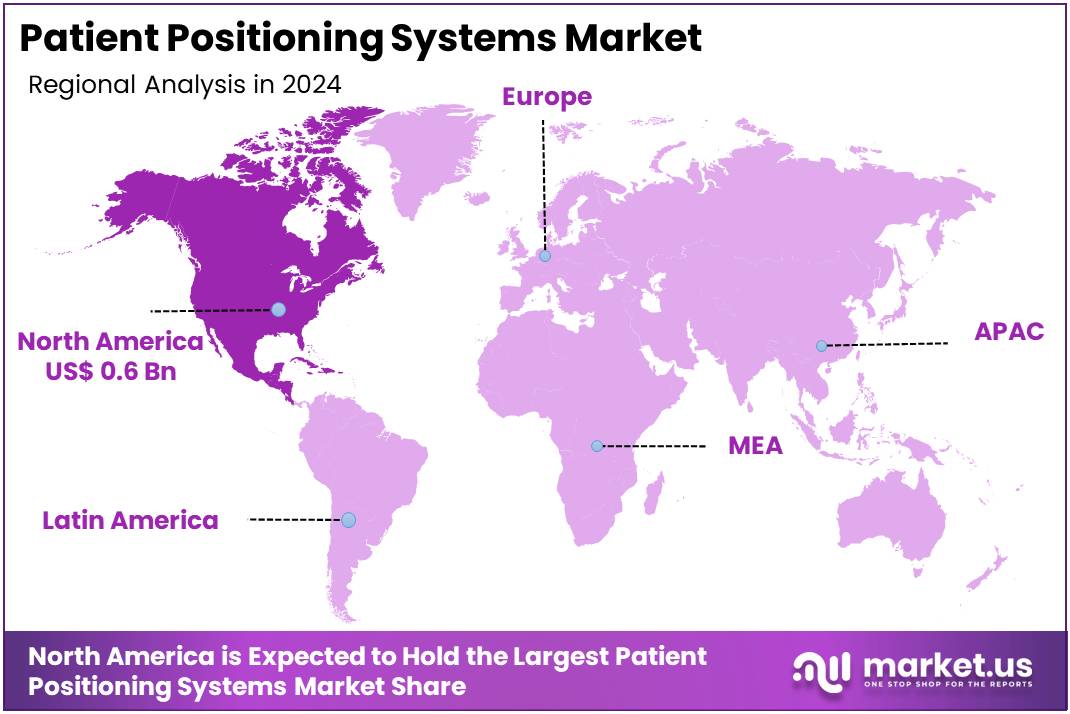

- North America led the market by securing a market share of 39.6% in 2024.

Product Type Analysis

The tables segment led in 2024, claiming a market share of 57.4% as the demand for advanced surgical tables continues to rise. Surgical tables play a crucial role in ensuring accurate positioning of patients during complex medical procedures, and advancements in these systems, including motorized and adjustable features, are anticipated to drive growth.

Hospitals and surgical centers are increasingly investing in innovative, ergonomic, and flexible positioning tables to enhance patient comfort and improve surgical outcomes. The growing number of surgical procedures and the increasing focus on precision in patient positioning are expected to propel the demand for high-quality surgical tables, making this segment a key driver of the patient positioning systems market.

Application Analysis

The surgery held a significant share of 63.5% due to the increasing number of surgeries being performed worldwide. As the global population ages and surgical procedures become more advanced, the need for accurate and reliable patient positioning during surgery is expected to rise.

The integration of patient positioning systems into operating rooms helps enhance precision, minimize surgical complications, and improve overall patient safety. Furthermore, technological advancements in surgical tools and robotics, combined with the increasing focus on minimally invasive procedures, are likely to contribute to the growth of the surgery segment within the patient positioning systems market.

End-User Analysis

The hospitals segment had a tremendous growth rate, with a revenue share of 59.8% as hospitals remain the primary consumers of patient positioning systems. As the demand for surgeries, particularly in orthopedic, cardiovascular, and neurological fields, continues to increase, hospitals are investing in advanced patient positioning systems to ensure the safety and comfort of patients during procedures.

The growing adoption of robotic surgeries and minimally invasive procedures further drives the need for precise and adjustable positioning systems. With rising healthcare costs and a focus on improving surgical outcomes, hospitals are expected to continue expanding their use of advanced patient positioning technologies, contributing to the overall growth of the market.

Key Market Segments

By Product Type

- Tables

- Surgical Tables

- Examination Tables

- Radiolucent Imaging Tables

- Accessories

By Application

- Surgery

- Diagnostics

- Others

By End-user

- Hospitals

- Ambulatory centers

- Others

Drivers

Technological Advancements in Surgical Procedures are Driving the Market

The rise of minimally invasive and robotic-assisted surgeries is significantly increasing the demand for advanced patient positioning systems. These innovations require precise, adaptable solutions to improve surgical outcomes. In 2022, Intuitive Surgical reported performing over 1.8 million robotic-assisted procedures globally, marking a 20% increase from the previous year. This growth has directly fueled the need for specialized positioning equipment.

Additionally, the American Hospital Association found that 85% of US hospitals now offer minimally invasive surgical options, further boosting the adoption of advanced positioning systems. Companies like Stryker and Hill-Rom have responded by introducing motorized surgical tables with enhanced adjustability to meet these demands. As robotic-assisted surgeries and minimally invasive procedures continue to rise, the need for precise, flexible patient positioning systems will keep driving market growth.

Restraints

High Costs and Budget Constraints are Restraining the Market

The high cost of advanced positioning systems remains a major restraint on the market, particularly in lower-income regions. A single automated surgical table can range from US$50,000 to US$150,000, which many healthcare facilities find unaffordable. In 2023, the World Health Organization reported that nearly 40% of hospitals in developing nations struggle to secure funding for such equipment. Even in developed countries like the US, financial pressures have led to postponed purchases.

A 2022 survey by the American College of Healthcare Executives found that 62% of US hospitals delayed capital expenditures due to budget constraints. Moreover, reimbursement challenges for positioning accessories further limit the market’s expansion, as healthcare systems face difficulties in covering the costs associated with these advanced surgical solutions. These financial barriers are particularly evident in regions where healthcare budgets are limited, restricting access to the latest technology.

Opportunities

Rising Geriatric Population is Creating Growth Opportunities

The growing aging population is driving the demand for surgical interventions, creating substantial opportunities for ergonomic positioning solutions. The United Nations projects that the global population of individuals aged 65 and older will double to 1.6 billion by 2050. A significant portion of this population will require various surgeries, further amplifying the need for advanced positioning systems that accommodate elderly patients.

A 2022 study by the National Institute on Aging revealed that 12% of hospital injuries among seniors occur due to falls during transfers, underscoring the need for safer and more ergonomic systems. Companies like Getinge and Mizuho OSI are responding to this demand by developing weight-sensitive tables and other specialized equipment to provide better support and minimize risks during surgery. With the rising incidence of age-related surgeries, this demographic shift is expected to fuel growth in the orthopedic and surgical positioning equipment market.

Impact of Macroeconomic / Geopolitical Factors

Macroeconomic and geopolitical factors have a profound impact on the market for surgical positioning systems, presenting both challenges and opportunities. Rising inflation and supply chain disruptions have increased production costs for medical device manufacturers, leading to higher prices for positioning systems. Geopolitical tensions, such as trade disputes between the US and China, have further delayed shipments of key components used in manufacturing these devices.

However, government initiatives in regions like Europe and Asia-Pacific are supporting market growth by offering subsidies and funding for advanced surgical equipment. For example, the US Inflation Reduction Act allocated US$1.5 billion for healthcare infrastructure in 2023, indirectly benefiting the sector.

Geopolitical conflicts have caused disruptions in raw material supplies but also prompted increased regional manufacturing efforts. While these short-term challenges pose hurdles, rising healthcare investments and continuous technological advancements are expected to drive long-term market growth, ensuring that the sector remains resilient and poised for continued expansion.

Trends

Increasing Adoption of Hybrid Operating Rooms is a Recent Trend

A recent trend driving the market is the increasing adoption of hybrid operating rooms, which combine imaging and surgical capabilities in a single space and require adaptable positioning systems. Siemens Healthineers reported a 30% increase in hybrid OR installations since 2021, with over 5,000 units now in use worldwide.

Additionally, Philips noted a 22% rise in sales of its hybrid-compatible tables in 2022, reflecting the growing demand for these advanced operating rooms. These hybrid systems improve procedural efficiency by enabling real-time imaging during surgery, thus enhancing patient outcomes. However, the high cost of setting up a hybrid operating room, which can reach up to US$3.5 million per room, remains a challenge for some healthcare institutions. Despite these high upfront costs, the integration of hybrid operating rooms is expected to continue growing, as they offer improved clinical outcomes and streamline complex surgical procedures.

Regional Analysis

North America is leading the Patient Positioning Systems Market

North America dominated the market with the highest revenue share of 39.6% owing to increasing surgical volumes, advancements in imaging technologies, and rising demand for precision in radiation therapy. According to the Centers for Disease Control and Prevention (CDC), hospital admissions for surgical procedures rose by 6.2% in 2023 compared to 2022, creating a higher demand for advanced positioning solutions to improve patient outcomes. The American Cancer Society reported that 1.9 million new cancer cases were diagnosed in the US in 2023, boosting the need for precise patient alignment in radiation therapy.

Additionally, the Food and Drug Administration (FDA) approved 12 new imaging and surgical navigation systems in 2023, accelerating the adoption of advanced positioning technologies. Hospitals also invested heavily in robotic-assisted surgery, with Intuitive Surgical reporting a 22% increase in da Vinci system installations in North America in 2023, which relies on precise patient positioning for optimal results. Government initiatives, such as Medicare expansion for outpatient surgeries, further contributed to market growth by increasing accessibility to advanced medical technologies.

The Asia Pacific region is expected to experience the highest CAGR during the forecast period

Asia Pacific is expected to grow with the fastest CAGR owing to rising healthcare investments, increasing cancer incidence, and government-led modernization of medical infrastructure. The World Health Organization (WHO) reported that cancer cases in the region surged to 9.8 million in 2023, up from 9.2 million in 2022, driving demand for accurate radiation therapy positioning.

Countries like China and India allocated US$32 billion and US$8.5 billion, respectively, in 2023 for hospital infrastructure upgrades, as per their respective health ministries. The Japan Medical Imaging and Radiological Systems Industries Association (JIRA) noted a 15% year-on-year increase in diagnostic imaging equipment sales in 2023, indicating higher adoption of positioning systems.

Furthermore, the Indian government’s Ayushman Bharat scheme added 1,500 new hospitals in 2023, increasing the need for surgical and imaging positioning solutions. With medical tourism growing at 18% annually in Thailand and Singapore, as reported by their tourism boards, hospitals in these countries are expected to invest further in advanced patient alignment technologies to meet international standards.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherland

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- New Zealand

- Singapore

- Thailand

- Vietnam

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

Key players in the patient positioning systems market focus on technological innovation, expanding their product portfolios, and increasing market reach to drive growth. They invest in developing advanced, ergonomic, and precise positioning solutions that enhance patient comfort and improve surgical accuracy. Companies also work to integrate their systems with other healthcare technologies, such as imaging and surgical robots, to improve overall workflow and efficiency in medical procedures.

Strategic partnerships with healthcare institutions and medical device manufacturers help broaden their product adoption. Additionally, they target emerging markets with growing healthcare infrastructure to expand their global footprint. IMRIS, headquartered in Winnipeg, Canada, is a global leader in providing advanced imaging and patient positioning solutions. The company offers a range of innovative products, including surgical tables and positioning systems, designed to improve accuracy and patient safety during surgeries.

IMRIS focuses on integrating its systems with advanced imaging technologies, such as MRI and CT, to enhance surgical precision. With a strong emphasis on research and development, IMRIS continues to expand its global market presence by collaborating with healthcare providers and medical institutions to deliver state-of-the-art positioning solutions.

Top Key Players in the Patient Positioning Systems Market

- Stryker Corporation

- STERIS plc

- Smith & Nephew

- Mizuho OSI

- Medtronic

- Medline Industries

- LEONI AG

- FluidAI Medical

Recent Developments

- In September 2023, FluidAI Medical, an AI-driven health tech startup, teamed up with Medtronic Canada to enhance post-surgical patient care through their Continuous Connected Patient Care initiative. Their collaboration leverages FluidAI’s Stream Platform, which integrates advanced artificial intelligence to monitor patients after surgery, marking a transformative step in healthcare innovation in Canada.

- In March 2023, Stryker launched SmartMedic in India, the country’s first ICU bed upgrade platform. This innovation is designed to enhance patient monitoring and safety, offering a more efficient and secure environment for both patients and healthcare providers.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | US$ 1.6 billion |

| Forecast Revenue (2034) | US$ 2.4 billion |

| CAGR (2025-2034) | 4.1% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments |

| Segments Covered | By Product Type (Tables (Surgical Tables, Examination Tables, and Radiolucent Imaging Tables), and Accessories), By Application (Surgery, Diagnostics, and Others), By End-user (Hospitals, Ambulatory Centers, and Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Stryker Corporation, STERIS plc, Smith & Nephew, Mizuho OSI, Medtronic, Medline Industries, LEONI AG, and FluidAI Medical. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |