Quick Navigation

Report Overview

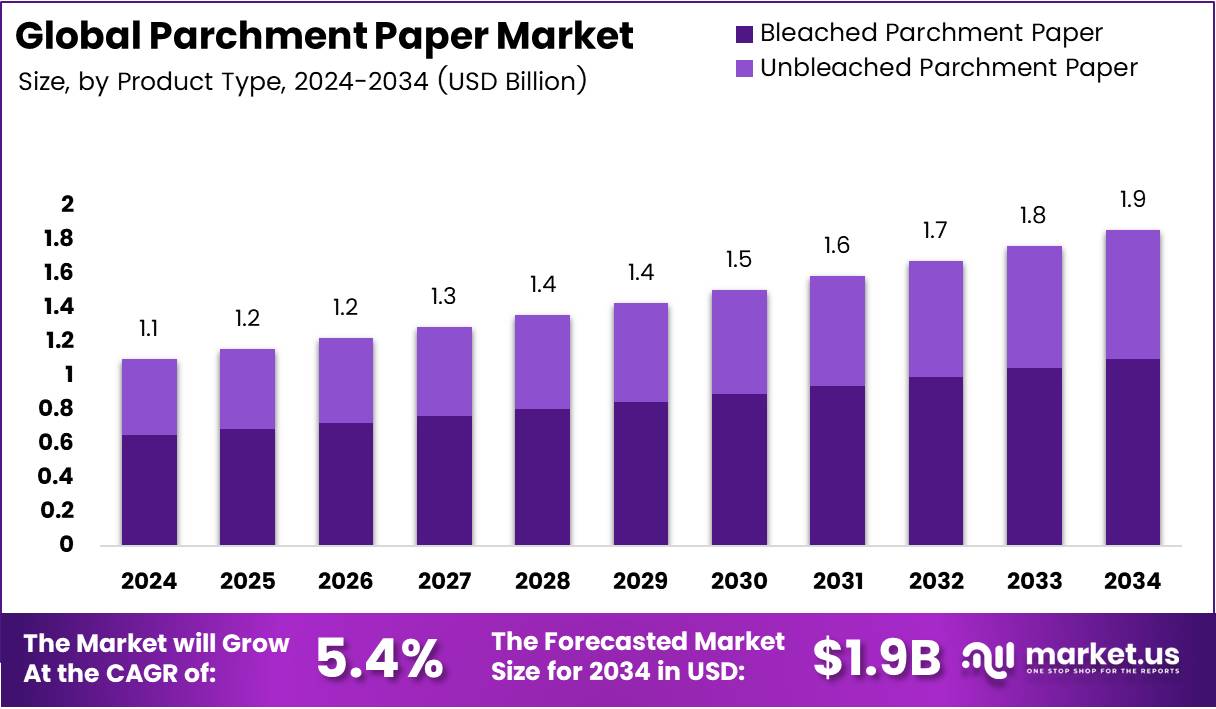

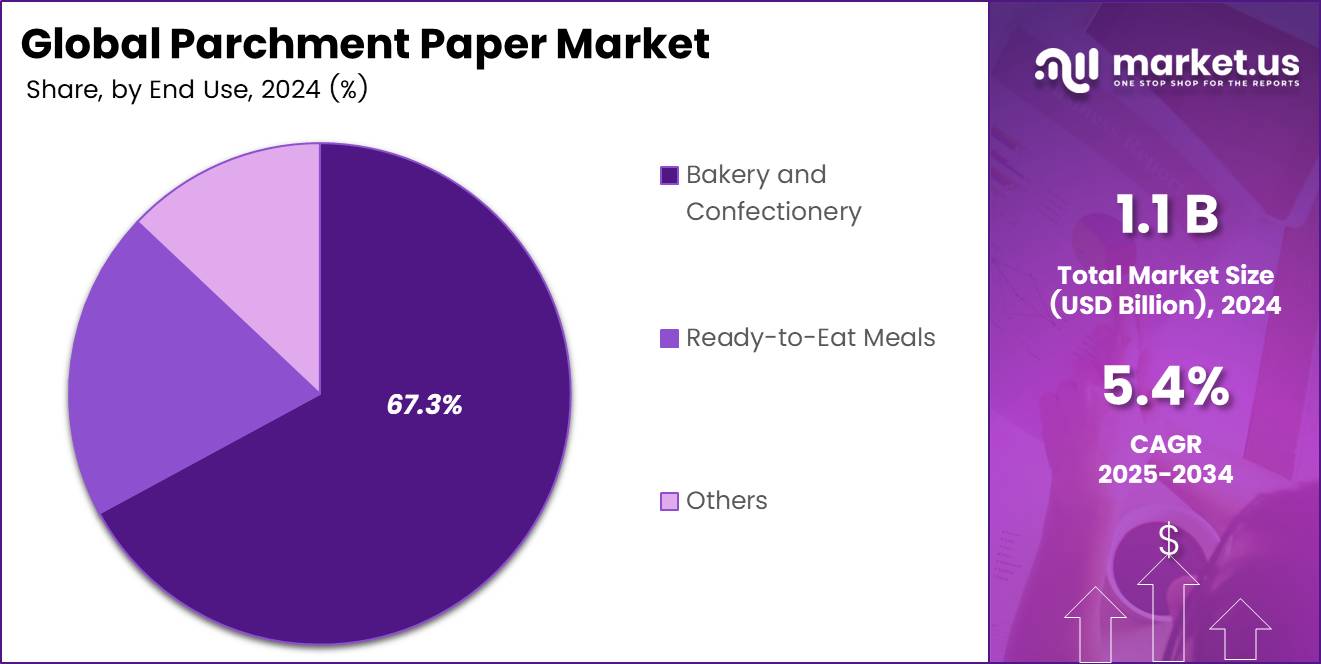

The Global Parchment Paper Market size is expected to be worth around USD 1.9 Billion by 2034, from USD 1.1 Billion in 2024, growing at a CAGR of 5.4% during the forecast period from 2025 to 2034.

The parchment paper market is an essential segment within the packaging and food industry, characterized by its diverse applications in baking, cooking, and food packaging. Made from cellulose, parchment paper is renowned for its heat-resistant and non-stick properties, making it an essential product in both home kitchens and commercial food establishments.

The demand for parchment paper has been driven by the growing preference for sustainable and eco-friendly packaging solutions. As consumers become more environmentally conscious, the market for parchment paper is expected to grow. Consumers are increasingly opting for products that align with their sustainability goals, a trend that is reshaping the packaging sector and further enhancing the popularity of parchment paper.

Government initiatives and regulations play a significant role in this growth. Numerous countries are enforcing stricter environmental policies, encouraging companies to shift to sustainable packaging materials. With government backing, the adoption of environmentally friendly products, including parchment paper, is becoming more widespread. This aligns with global efforts to reduce plastic usage and minimize the environmental impact of packaging.

Opportunities in the parchment paper market are abundant, particularly in the growing demand for sustainable alternatives to traditional plastic-based packaging. This shift presents a unique opportunity for manufacturers to capitalize on eco-conscious consumer preferences. Companies can gain a competitive edge by offering sustainable, biodegradable packaging solutions that meet the evolving demands of the market.

According to a recent industry report, 58% of consumers prefer brands that have publicly committed to sustainability goals, with 39% having switched to a competitor that offers sustainable packaging over one that does not. Additionally, 70% of consumers prefer packaging with clear sustainability labels, indicating a strong preference for transparency in eco-friendly practices.

These statistics underscore the growing importance of sustainability in consumer decision-making. As such, the parchment paper market is expected to expand as businesses respond to these shifting consumer preferences and adopt more sustainable practices in their product offerings. The market’s future growth hinges on innovation and alignment with consumer demands for eco-friendly, transparent packaging solutions.

Key Takeaways

- The Global Parchment Paper Market size is expected to reach USD 1.9 Billion by 2034, from USD 1.1 Billion in 2024, growing at a CAGR of 5.4%.

- Bleached parchment paper holds the largest market share at 59.2% due to its aesthetic appeal and enhanced food safety features.

- The less than 40 GSM segment dominates at 47.9%, favored for its lightweight and economical properties in basic baking applications.

- The bakery and confectionery segment leads with 67.3% market share, benefiting from rising consumer demand for baked goods and confections.

- Hypermarkets and supermarkets dominate distribution with 47.1% market share, offering competitive pricing and convenience to both consumers and businesses.

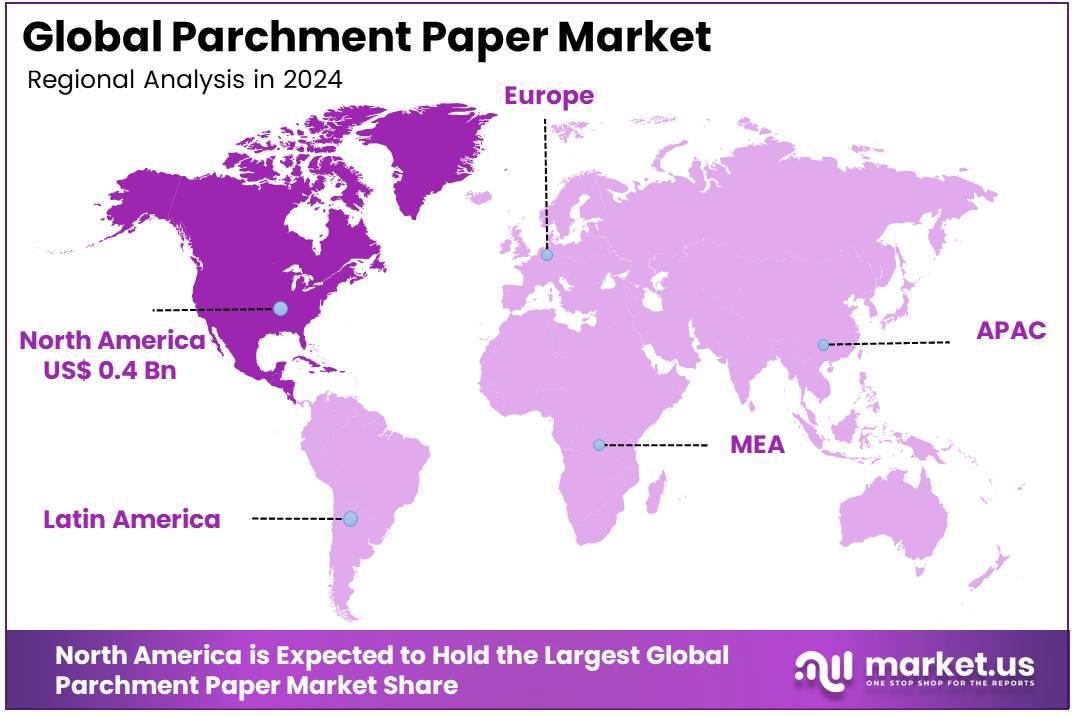

- North America holds the dominant market share at 45.3%, valued at USD 0.4 Billion, driven by demand for sustainable packaging solutions and a strong foodservice industry.

Product Type Analysis

Bleached Parchment Paper dominates with 59.2% due to its superior appearance and food safety properties.

Bleached parchment paper commands the largest market share at 59.2% primarily because of its pristine white appearance and enhanced food safety characteristics. This variant undergoes chemical bleaching processes that eliminate natural impurities, resulting in a clean, professional look that appeals to commercial bakeries and food service establishments.

Moreover, bleached parchment offers superior non-stick properties and heat resistance, making it ideal for high-temperature baking applications where presentation matters.

Unbleached parchment paper represents the remaining market segment, gaining traction among health-conscious consumers and eco-friendly establishments. This natural brown-colored alternative appeals to organic bakeries and sustainable food businesses seeking environmentally responsible packaging solutions. Additionally, unbleached variants often cost less than bleached options, making them attractive to price-sensitive consumers and small-scale baking operations.

Basis Weight Analysis

Less than 40 GSM dominates with 47.9% due to its lightweight nature and cost efficiency.

The less than 40 GSM segment holds the largest market share at 47.9%, driven by its lightweight characteristics and economical pricing. This category perfectly suits basic baking applications like cookies, pastries, and light confectionery items where heavy-duty strength isn’t essential. Furthermore, its thin profile ensures even heat distribution and prevents over-browning, making it preferred by professional bakers for delicate baked goods.

The 41 to 60 GSM category serves medium-weight applications, offering balanced performance for versatile baking needs. This segment attracts commercial kitchens requiring moderate strength for items like bread rolls, muffins, and medium-density confections. Additionally, this weight range provides adequate moisture barrier properties while maintaining reasonable costs.

The 61 to 80 GSM segment caters to heavy-duty applications requiring maximum strength and durability. This premium category appeals to industrial bakeries producing dense breads, meat preparations, and high-moisture content foods that demand superior barrier properties and structural integrity.

End Use Analysis

Bakery and Confectionery dominates with 67.3% due to widespread adoption in commercial baking operations.

The bakery and confectionery segment commands the dominant position with 67.3% market share, reflecting parchment paper’s essential role in professional baking environments. This segment benefits from increasing consumer demand for baked goods, artisanal pastries, and specialty confections across retail and foodservice channels.

Moreover, commercial bakeries rely heavily on parchment paper for its non-stick properties, easy release characteristics, and ability to withstand high oven temperatures without compromising food quality.

Ready-to-eat meals represent a growing segment, driven by busy lifestyles and convenience food trends. This category leverages parchment paper’s versatility for packaging pre-prepared foods, microwave-safe applications, and takeaway containers. Additionally, the segment benefits from increased demand for healthy, portion-controlled meal options that require safe, heat-resistant packaging solutions.

The others category encompasses diverse applications including food wrapping, industrial uses, and specialty packaging requirements. This segment serves niche markets requiring customized parchment solutions for unique food preparation and preservation needs across various industries.

Distribution Channel Analysis

Hypermarkets & Supermarkets dominates with 47.10% due to widespread accessibility and bulk purchasing options.

Hypermarkets and supermarkets lead the distribution landscape with 47.10% market share, capitalizing on their extensive retail networks and convenient shopping experiences. These large-format stores offer comprehensive parchment paper selections, competitive pricing, and bulk purchasing options that attract both household consumers and small businesses. Furthermore, their strategic locations and extended operating hours provide unmatched accessibility for customers seeking immediate product availability.

Specialty stores serve targeted customer segments requiring expert guidance and premium product offerings. This channel appeals to professional bakers, culinary enthusiasts, and businesses seeking specialized parchment varieties with specific performance characteristics. Additionally, specialty retailers provide personalized service and technical expertise that larger chains cannot match.

Online stores capture tech-savvy consumers seeking convenience and competitive pricing through e-commerce platforms. This rapidly growing channel offers extensive product catalogs, home delivery options, and subscription services that appeal to busy professionals and bulk buyers.

The others category includes foodservice distributors, wholesale channels, and direct manufacturer sales serving institutional customers and large-scale commercial operations requiring specialized procurement solutions.

Key Market Segments

By Product Type

- Bleached Parchment Paper

- Unbleached Parchment Paper

By Basis Weight

- Less than 40 GSM

- 41 to 60 GSM

- 61 to 80 GSM

By End Use

- Bakery and Confectionery

- Ready-to-Eat Meals

- Others

By Distribution Channel

- Hypermarkets & Supermarkets

- Specialty Stores

- Online Stores

- Others

Drivers

Increasing Demand for Sustainable Packaging Drives Growth in the Parchment Paper Market

Increasing consumer preference for sustainable packaging has significantly impacted the parchment paper market. With a growing shift towards eco-friendly solutions, consumers are increasingly choosing products that align with their values of reducing waste. As businesses seek to meet this demand, parchment paper, being biodegradable and recyclable, has gained popularity in packaging applications.

The rising demand for non-stick and easy-to-clean baking solutions also fuels the market. Parchment paper’s inherent non-stick properties make it a preferred choice for baking and cooking, as it simplifies cleanup and enhances food preparation. This feature has contributed to the widespread use of parchment paper in households and commercial kitchens alike.

The growing popularity of home baking and cooking activities has further driven demand for parchment paper. With more consumers engaged in these activities, there is a heightened need for tools and materials that make cooking easier and more convenient. Parchment paper, being a versatile and essential product, has become a staple in kitchens across various regions.

Finally, the expanding food service industry and catering demand provide a substantial growth opportunity for parchment paper. Catering services, restaurants, and other food-related businesses are increasingly adopting parchment paper for its ability to enhance food quality and streamline cooking processes, further contributing to market growth.

Restraints

Competition and Environmental Concerns Restrain Parchment Paper Market Growth

The competition from other packaging materials, such as aluminum foil, presents a challenge for the parchment paper market. Aluminum foil offers similar properties, such as non-stick and heat resistance, which makes it a strong alternative. Despite the environmental benefits of parchment paper, aluminum foil continues to be a preferred option due to its widespread availability and versatility.

Another restraint is the lack of awareness in emerging markets. While parchment paper is widely used in developed regions, many emerging markets are still unfamiliar with its benefits. The absence of awareness regarding the environmental impact and functionality of parchment paper limits its adoption in these regions, slowing market growth.

Environmental concerns over the disposal of single-use products further restrict the growth of parchment paper. Despite its biodegradable nature, many consumers still view parchment paper as a single-use product, contributing to waste. As sustainability concerns intensify, there is pressure to develop more eco-friendly alternatives and encourage consumers to use parchment paper responsibly.

Growth Factors

Growth Opportunities for the Parchment Paper Market Driven by Sustainable Innovations

The development of biodegradable and compostable parchment paper presents a significant growth opportunity. With increasing awareness of environmental issues, consumers and businesses alike are seeking packaging options that are not only sustainable but also contribute to waste reduction. Biodegradable parchment paper aligns with these demands, positioning itself as an attractive option for eco-conscious consumers.

The expansion of e-commerce platforms for parchment paper sales opens up new channels for market penetration. Online shopping provides consumers with convenient access to a wide variety of parchment paper products, including specialty sizes and brands. The growth of e-commerce is expected to drive demand and broaden the reach of parchment paper to a wider audience.

Rising demand for custom-sized and pre-cut parchment paper offers another opportunity. As consumers look for products that better fit their specific needs, offering custom-sized parchment paper could meet this demand. Additionally, pre-cut parchment paper offers convenience and time savings, further driving its appeal.

Lastly, the increased adoption of parchment paper in food packaging presents a notable growth opportunity. As the food industry continues to focus on sustainability, parchment paper’s role in reducing plastic usage and enhancing food safety positions it well for expansion in this sector.

Emerging Trends

Trending Factors Shaping the Parchment Paper Market with a Focus on Eco-friendly Solutions

The shift toward chemical-free and non-toxic baking paper is a key trend in the parchment paper market. Consumers are becoming more conscious of the materials used in food preparation, and parchment paper offers a safe, non-toxic alternative to other baking products. This trend is expected to grow as more people seek chemical-free solutions for their cooking and baking needs.

Innovations in parchment paper for cooking convenience are also gaining traction. Manufacturers are exploring new ways to enhance the functionality of parchment paper, such as introducing pre-greased or pre-flavored sheets. These innovations cater to the evolving demands of both home bakers and professional chefs.

The integration of parchment paper with smart cooking appliances represents a forward-looking trend. As smart kitchens become more common, there is potential for parchment paper to be used in conjunction with smart ovens and cooking devices. This integration could streamline cooking processes and further boost the appeal of parchment paper.

Finally, the growing interest in eco-friendly and zero-waste lifestyles is driving the popularity of parchment paper. As consumers become more environmentally conscious, they are increasingly turning to products that support sustainable living. Parchment paper, with its eco-friendly attributes, aligns well with this trend and is expected to see continued growth in the market.

Regional Analysis

North America Dominates the Parchment Paper Market with a Market Share of 45.3%, Valued at USD 0.4 Billion

North America is the leading region in the parchment paper market, holding a dominant share of 45.3%, valued at USD 0.4 Billion. The region’s high market share is driven by the growing consumer demand for sustainable packaging solutions, especially in the foodservice and retail sectors. Furthermore, North America’s well-established foodservice industry, along with stringent sustainability regulations, continues to support the market growth.

Europe Parchment Paper Market Trends

Europe follows closely as a significant player in the parchment paper market. The region is experiencing a shift toward eco-friendly packaging solutions, influenced by government regulations and consumer preferences for sustainability. European countries are increasingly adopting parchment paper in food packaging, driven by the rising demand for clean, non-toxic materials in food preparation and storage.

Asia Pacific Parchment Paper Market Trends

Asia Pacific is witnessing rapid growth in the parchment paper market, fueled by increasing consumer awareness of sustainability and rising disposable incomes. The region’s expanding foodservice industry and growing preference for home cooking are anticipated to drive the demand for parchment paper. Moreover, improving production capacities and investment in eco-friendly materials further support market expansion in this region.

Middle East and Africa Parchment Paper Market Trends

The Middle East and Africa (MEA) region is experiencing steady growth in the parchment paper market. While the market is still emerging, there is an increasing trend towards adopting sustainable packaging in both food and non-food sectors. The demand is anticipated to rise as more local manufacturers begin offering eco-friendly packaging solutions, aligned with the growing sustainability trends across the region.

Latin America Parchment Paper Market Trends

Latin America is seeing a gradual but steady increase in the adoption of parchment paper. The market is mainly driven by the foodservice sector, with growing interest in sustainable packaging materials. However, compared to other regions, the Latin American market is still in the early stages, and future growth will largely depend on increased consumer awareness and government incentives for sustainable practices.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Parchment Paper Company Insights

In 2024, Reynolds Consumer Products is expected to maintain its strong position in the global parchment paper market due to its widespread brand recognition and robust distribution network. The company continues to innovate with eco-friendly parchment solutions, catering to the increasing consumer demand for sustainable products.

Pactiv LLC is projected to capture a significant market share, driven by its expertise in manufacturing high-quality parchment paper for foodservice and packaging applications. Their focus on sustainable and cost-efficient materials positions them well to capitalize on the growing market for environmentally conscious packaging.

Delfort Group is expected to benefit from its strong presence in Europe and its ongoing commitment to advancing the quality of parchment paper. The company’s investments in enhancing production capabilities for high-performance papers ensure that it can meet the demands of both the food industry and other sectors requiring specialty papers.

Nordic Paper is anticipated to continue growing in 2024, leveraging its sustainable production methods and commitment to minimizing environmental impact. The company’s innovation in paper technology and its ability to produce high-quality parchment paper for diverse applications make it a key player in the industry, particularly in the European market.

Top Key Players in the Market

- Reynolds Consumer Products

- Pactiv LLC

- Delfort Group

- Nordic Paper

- Krpa Paper

- Ahlstrom-Munksjö

- Chemours Company

- McNairn Packaging

- Georgia-Pacific

- Metsa Board Corporation

Recent Developments

- In Jul 2025, Bambrew secures $10.3 million in funding to accelerate the development and expansion of its eco-friendly packaging solutions, aiming to scale production and meet growing demand for sustainable alternatives.

- In Jan 2025, Zerocircle raises ₹20 crores in a funding round led by Rainmatter, focusing on enhancing its innovative packaging solutions made from 100% post-consumer waste, aimed at reducing plastic waste.

- In Apr 2025, a German startup bags $15.5 million to bring its tech-led reusable food packaging to the US market, aiming to revolutionize the food packaging industry with environmentally sustainable products.

- In Sep 2025, Yangi secures €10 million in funding to advance its fibre-based packaging solutions, targeting sustainability-driven brands in the food and consumer goods sectors.

- In Oct 2024, Earthodic raises $6 million to support the development of bio-based coatings, focusing on innovative technologies to reduce the environmental impact of traditional packaging materials.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 1.1 Billion |

| Forecast Revenue (2034) | USD 1.9 Billion |

| CAGR (2025-2034) | 5.4% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Product Type (Bleached Parchment Paper, Unbleached Parchment Paper), By Basis Weight (Less than 40 GSM, 41 to 60 GSM, 61 to 80 GSM), By End Use (Bakery and Confectionery, Ready-to-Eat Meals, Others), By Distribution Channel (Hypermarkets & Supermarkets, Specialty Stores, Online Stores, Others) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | Reynolds Consumer Products, Pactiv LLC, Delfort Group, Nordic Paper, Krpa Paper, Ahlstrom-Munksjö, Chemours Company, McNairn Packaging, Georgia-Pacific, Metsa Board Corporation |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |