Quick Navigation

Report Overview

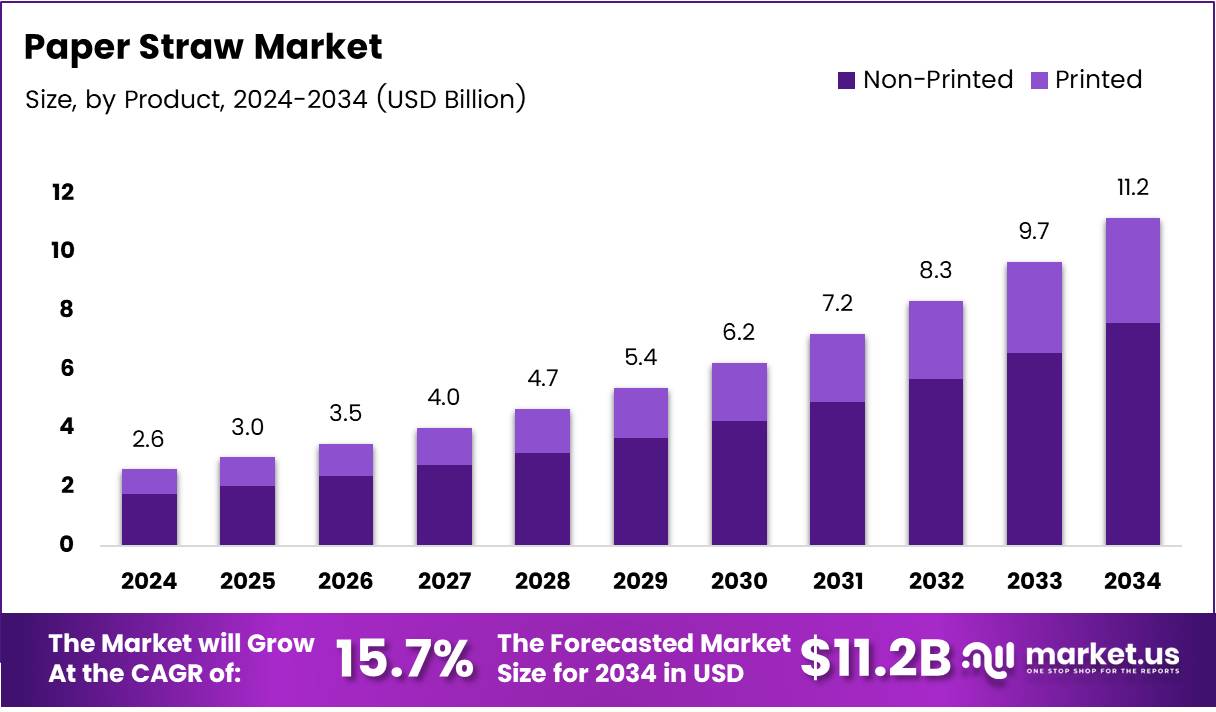

The Global Paper Straw Market size is expected to be worth around USD 11.2 Billion by 2034, from USD 2.6 Billion in 2024, growing at a CAGR of 15.7% during the forecast period from 2025 to 2034. This growth is primarily driven by increasing environmental awareness and the rising demand for sustainable alternatives to plastic straws across various industries.

Key Takeaways

- The global paper straw market is projected to reach USD 11.2 billion by 2034 from USD 2.6 billion in 2024, growing at a CAGR of 15.7%.

- Non-Printed paper straws held a dominant 57.2% share in the by product segment in 2024.

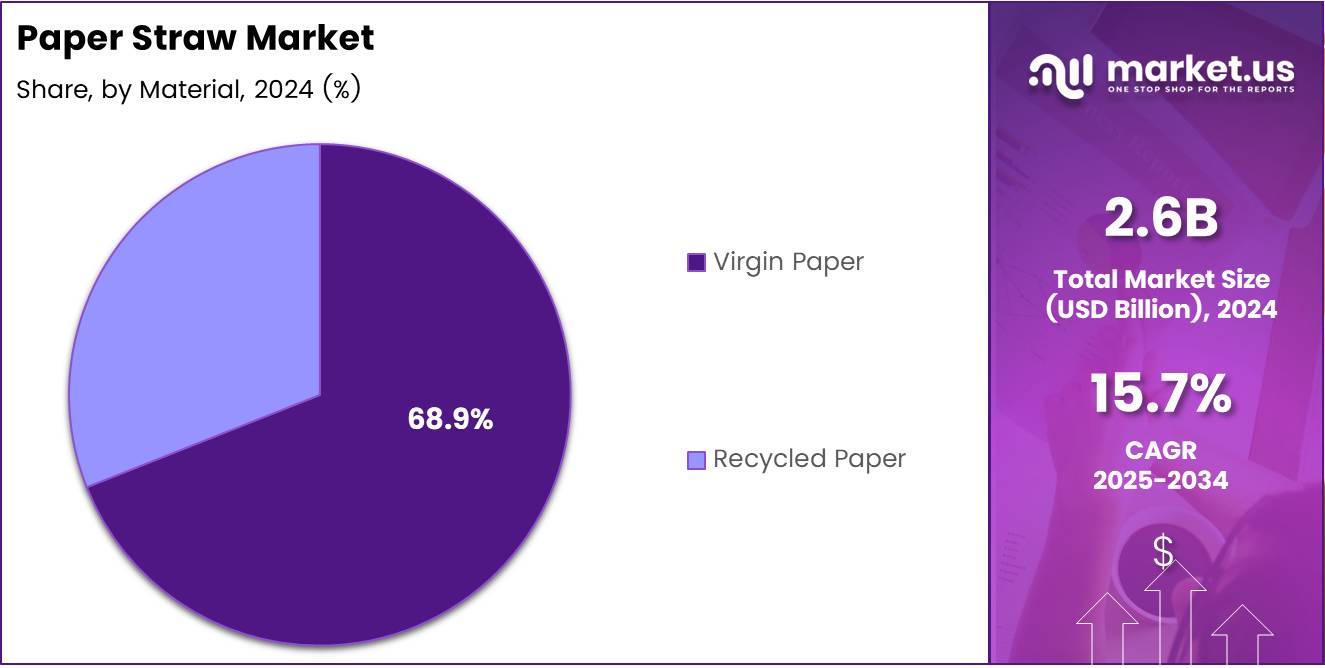

- Virgin Paper led the by material segment with a 68.9% market share in 2024.

- Straws with a diameter of 0.196 – 0.25 inches accounted for the largest 34.4% share in the by diameter segment in 2024.

- B2B sales channels dominated with a 68.2% share in the by sales channel segment in 2024.

- The 7.75-8.5 inch straw length segment captured 31.2% of the market in 2024.

- The foodservice sector led the by end-use segment with a 64.2% share in 2024.

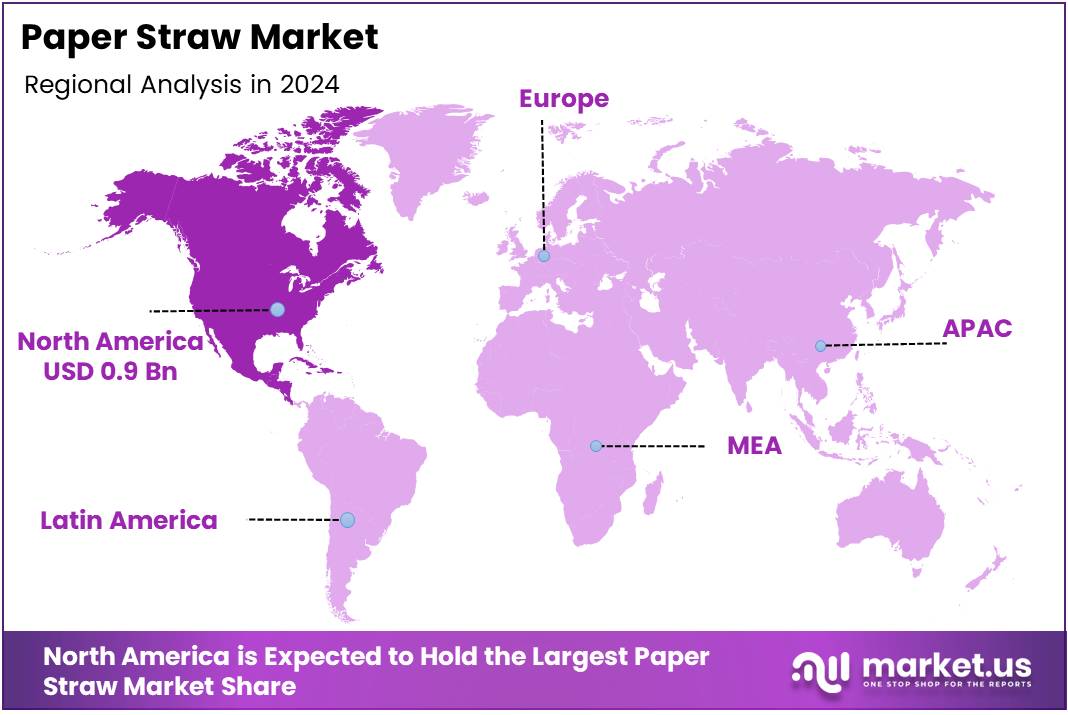

- North America dominated the regional market with a 35.6% share, valued at approximately USD 0.9 billion in 2024.

The paper straw market represents a growing segment within sustainable packaging, driven by increasing environmental concerns and regulatory pressure to reduce plastic waste. Paper straws serve as an eco-friendly alternative to plastic, addressing the urgent need to cut down on single-use plastics that harm ecosystems. This market is gaining traction globally as businesses and consumers prioritize sustainability.

According to Foopak, paper straws can function normally for up to 60 minutes at room temperature and 4 hours at a low temperature of around 4°C, making them practical for various beverage applications. This durability encourages wider adoption across foodservice sectors, supporting market growth. As such, the paper straw market is evolving with innovations focused on improving product lifespan and user experience.

Furthermore, the demand for paper straws is propelled by vast consumption patterns. According to EBSCO, Americans use 500 million straws daily, indicating a massive potential shift towards biodegradable options. This significant consumption volume presents a lucrative opportunity for manufacturers to capture a large share of the market by offering sustainable alternatives that meet consumer needs.

Environmental concerns also catalyze the paper straw market expansion. According to ClientEarth, over 50% of plastic is used once and then discarded, highlighting the urgency for alternatives. Additionally, over 98% of single-use plastic derives from fossil fuels, emphasizing the need for renewable and biodegradable substitutes. These facts strengthen the case for paper straws as part of the global push to reduce plastic pollution.

Government initiatives and regulations further support the paper straw market’s growth trajectory. Several countries and municipalities have implemented bans or restrictions on single-use plastics, compelling businesses to switch to paper-based solutions. This regulatory environment not only drives demand but also encourages innovation, investment, and expansion within the paper straw manufacturing sector.

Investors and manufacturers are increasingly recognizing the economic and environmental value of paper straws. The market offers opportunities in developing cost-effective, durable, and customizable products that appeal to both retail and foodservice clients. Growing awareness among consumers about the environmental impact of plastics fuels demand for sustainable packaging, which will continue to propel market growth.

Product Analysis

Non-Printed holds a dominant market position with a 57.2% share in the Paper Straw Market in 2024.

In 2024, the Paper Straw Market saw significant preference for Non-Printed paper straws, holding a substantial 57.2% share in the By Product Analysis segment. This category is favored due to its simple, environmentally friendly design, and widespread use across various industries, especially in food service and beverage sectors. Non-printed straws are often considered more sustainable, as they avoid the use of additional inks or coatings, making them a preferred choice for eco-conscious businesses and consumers.

In contrast, the Printed paper straw segment is smaller but still maintains a presence in the market, offering businesses the opportunity to brand their products with logos and designs. However, it lags behind Non-Printed in terms of market share, likely due to cost and sustainability concerns. While Printed straws appeal to businesses looking for brand customization, the shift towards cleaner and more eco-friendly alternatives keeps Non-Printed straws as the dominant force in the market.

Material Analysis

Virgin Paper holds a dominant market position with a 68.9% share in the Paper Straw Market in 2024.

In 2024, the By Material Analysis segment of the Paper Straw Market was led by Virgin Paper, commanding a significant 68.9% market share. Virgin Paper is preferred for its superior quality, durability, and reliability, ensuring that paper straws made from this material meet the performance standards required in the food and beverage industry. The higher percentage of Virgin Paper usage reflects its widespread acceptance in the market due to its better consistency and functionality.

On the other hand, Recycled Paper accounted for a smaller portion of the market. While this material has gained attention for its sustainability benefits, it still represents a less significant share compared to Virgin Paper. Recycled Paper offers a more environmentally friendly alternative, but its use in paper straws is still emerging, with challenges regarding strength and texture when compared to Virgin Paper. As sustainability continues to be a growing focus in the industry, Recycled Paper’s share may increase over time.

Diameter Analysis

0.196 – 0.25 Inches dominates with a 34.4% share in the Paper Straw Market in 2024.

In 2024, the Paper Straw Market’s By Diameter Analysis segment was dominated by straws ranging from 0.196 – 0.25 Inches, which held a notable 34.4% market share. This diameter range strikes a balance between functionality and consumer preference, making it the most popular choice in various industries, particularly for beverages. Straws in this range offer versatility, catering to different types of drinks while maintaining an optimal drinking experience.

Other diameter ranges, such as <0.15 Inches and >0.4 Inches, accounted for smaller portions of the market. The <0.15 Inches straws are typically used for smaller, more specialized applications, while the >0.4 Inches straws cater to larger, thicker drinks like smoothies or milkshakes. The dominance of the 0.196 – 0.25 Inches category reflects the general consumer preference for an average-size straw that suits a broad range of beverage types without being too narrow or too wide. As a result, it remains the top choice among various market segments.

Sales Channel Analysis

B2B holds a dominant market position with a 68.2% share in the Paper Straw Market in 2024.

In 2024, the Paper Straw Market saw B2B (Business-to-Business) channels leading the way with a dominant 68.2% market share in the By Sales Channel Analysis segment. The B2B market is primarily driven by large-scale buyers, such as restaurants, cafes, and foodservice chains, who require consistent and bulk orders of paper straws. B2B transactions also benefit from long-term contracts and partnerships with manufacturers, allowing businesses to secure competitive pricing and supply chain stability.

Meanwhile, the B2C (Business-to-Consumer) segment holds a smaller market share. While direct sales to consumers have grown, particularly in retail and online channels, they still lag behind the B2B sector. The B2C market typically caters to individual consumers purchasing smaller quantities, which limits its growth compared to the bulk-driven B2B segment. However, as consumer demand for eco-friendly products rises, the B2C market is expected to see gradual expansion in the coming years.

Straw Length Analysis

In 2024, 7.75-8.5 Inches held a dominant market position in By Straw Length Analysis segment of Paper Straw Market, with a 31.2% share.

In 2024, the 7.75-8.5-inch segment led the Paper Straw Market, capturing a significant 31.2% of the overall market share. This length range is most commonly preferred for a variety of beverage types and aligns well with consumer demand for practical and versatile straw lengths.

The 5.75-7.75-inch segment, while smaller in comparison, still held a solid market presence. The 5.75-7.75 Inches range caters to smaller-sized cups, making it popular for takeout beverages and specialty drinks. This length range is expected to maintain moderate growth.

The longer straw segments, such as the 8.5-10.5 Inches and >10.5 Inches, are less common but serve a niche market. These longer straws typically appeal to larger cups and specific drink types, holding a smaller portion of the market at 8.5-10.5 Inches and > 10.5 Inches respectively.

Lastly, the <5.75 Inches segment covers shorter options that are primarily used for smaller, single-serve drinks. It remains the smallest segment but continues to cater to niche demands.

End Use Analysis

In 2024, Foodservice held a dominant market position in By End Use Analysis segment of Paper Straw Market, with a 64.2% share.

In 2024, the Foodservice sector dominated the Paper Straw Market with a notable 64.2% share. This dominance can be attributed to the widespread use of paper straws in restaurants, cafes, and other foodservice establishments, driven by consumer demand for eco-friendly alternatives to plastic.

Institutional use came in second, although it held a significantly smaller market share. The Institutional sector is still growing, with many institutions such as schools and hospitals beginning to phase out plastic straws in favor of more sustainable options.

The Household segment, while present, made up the smallest portion of the market. Household use is gaining ground slowly, primarily due to increasing awareness about sustainability and the growing trend of eco-conscious living. However, its share remains relatively low compared to Foodservice and Institutional uses.

The Foodservice segment is expected to continue leading the market due to high consumption and demand for disposable, environmentally friendly products.

Key Market Segments

By Product

- Non-Printed

- Printed

By Material

- Virgin Paper

- Recycled Paper

By Diameter

- 0.196 – 0.25 Inches

- < 0.15 Inches

- 0.15 – 0.196 Inches

- > 0.4 Inches

- 0.25 – 0.4 Inches

By Sales Channel

- B2B 68.2

- B2C

By Straw Length

- 7.75 – 8.5 Inches

- 5.75 – 7.75 Inches

- 8.5 – 10.5 Inches

- > 10.5 Inches

- < 5.75 Inches

By End Use

- Foodservice

- Institutional

- Household

Drivers

Increasing Consumer Preference for Sustainable and Eco-Friendly Packaging Drives Paper Straw Market Growth

Consumers today are becoming more aware of environmental issues and prefer products that reduce plastic waste. This growing preference for sustainable and eco-friendly packaging has led to a higher demand for paper straws. People want alternatives that are biodegradable and less harmful to nature.

Government regulations worldwide are playing a key role in boosting the paper straw market. Many countries have started banning single-use plastic straws to curb pollution. These laws encourage businesses and consumers to switch to paper straws as a legal and eco-friendly option.

Awareness about marine pollution is also increasing globally. People understand that plastic straws often end up in oceans, harming marine life and ecosystems. This concern motivates customers and companies alike to adopt paper straws, which break down naturally and cause less damage to the environment.

Additionally, the foodservice industry is expanding rapidly, especially with the growth of cafes, restaurants, and delivery services. These businesses increasingly demand biodegradable products like paper straws to meet customer expectations and comply with environmental rules. This expansion is a significant driver for market growth.

Restraints

Higher Production Costs Compared to Conventional Plastic Straws Restrict Paper Straw Market Growth

One major challenge for the paper straw market is the higher cost of production. Compared to plastic straws, making paper straws requires more expensive materials and manufacturing processes. This cost difference affects pricing and may limit adoption by cost-sensitive buyers.

Paper straws also have limited durability and shelf life. They tend to become soggy or lose strength when exposed to liquids for extended periods. This drawback can reduce consumer satisfaction and restrict their use in certain beverage types.

Maintaining the structural integrity of paper straws in liquid beverages is another issue. Unlike plastic, paper can weaken quickly, which poses challenges for manufacturers to improve quality and performance without raising costs.

Furthermore, the paper straw market suffers from a lack of standardized quality certifications across regions. This inconsistency creates uncertainty for buyers and suppliers, making it difficult to guarantee product reliability and safety worldwide.

Growth Factors

Development of Advanced Coating Technologies Offers Growth Opportunities in the Paper Straw Market

The paper straw market stands to benefit greatly from advancements in coating technologies. New coatings that enhance water resistance can improve straw durability and usability, addressing one of the biggest current limitations of paper straws.

Emerging markets present significant growth potential due to increasing environmental awareness and stricter regulations on plastic use. As governments enforce new policies, demand for paper straws is expected to rise steadily in these regions.

Collaborations between paper straw manufacturers and fast-food chains offer promising opportunities. Such partnerships encourage bulk adoption of paper straws, helping scale production and lower costs while boosting visibility among consumers.

Innovation in customizable and branded paper straws also opens new marketing avenues. Businesses can use these designs as a promotional tool, increasing appeal to consumers who value unique and eco-friendly packaging.

Emerging Trends

Adoption of Compostable Paper Straw Alternatives by Major Beverage Brands Shapes Market Trends

Leading beverage brands are increasingly switching to compostable paper straws to meet consumer demand for sustainable products. This shift helps normalize the use of paper straws and pushes competitors to follow suit, strengthening market growth.

The integration of paper straws with smart packaging, such as QR codes, enhances consumer engagement. This trend allows brands to share information about sustainability efforts, improving transparency and building customer loyalty.

The rise of e-commerce channels focused on sustainable packaging is another important trend. Online sales platforms enable easier access to eco-friendly products, increasing the reach of paper straws beyond traditional retail outlets.

Additionally, growing markets for vegan and organic products contribute to higher demand for green packaging solutions. Paper straws align well with these lifestyles, making them a preferred choice among environmentally conscious consumers.

Regional Analysis

North America Dominates the Paper Straw Market with a Market Share of 35.6%, Valued at USD 0.9 Billion

In 2024, North America held a dominant position in the paper straw market, capturing a significant 35.6% share, equivalent to approximately USD 0.9 billion. This leadership stems from strict environmental regulations targeting single-use plastics and a strong consumer shift toward sustainable alternatives. The well-developed foodservice industry and government incentives further boost demand for paper straws in the region.

Europe Paper Straw Market Trends

Europe is a key market in the global paper straw industry, propelled by proactive government regulations aimed at banning plastic straws and promoting biodegradable packaging. The region’s market value has grown substantially due to increasing consumer awareness, supported by investments in sustainable packaging innovations, making it a critical growth area despite no specific revenue data available.

Asia Pacific Paper Straw Market Insights

Asia Pacific is emerging as a high-growth market driven by rapid urbanization and growing environmental concerns. Countries in this region are adopting stricter regulations on plastic use, which along with expanding foodservice sectors, contribute to increasing demand. While exact market values are unavailable, the region’s potential for growth remains strong amid challenges related to production costs.

Middle East and Africa Paper Straw Market Overview

The Middle East and Africa region exhibits gradual expansion in the paper straw market, backed by rising awareness about sustainability and initial regulatory frameworks supporting eco-friendly products. Although precise valuation figures are not provided, market growth is expected to continue steadily, constrained by infrastructure limitations and cost considerations.

Latin America Paper Straw Market Landscape

Latin America is progressing steadily in adopting paper straws as part of its environmental conservation efforts. Increasing regulatory focus on reducing plastic waste and growing consumer demand for green packaging solutions are key drivers. Despite lacking specific market value data, economic and supply chain challenges may temper the pace of growth in the near term.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Paper Straw Company Insights

The global Paper Straw Market in 2024 is dominated by key players offering innovative and sustainable solutions to replace single-use plastics.

Matrix Pack stands out for its commitment to providing eco-friendly alternatives with a focus on reducing the environmental impact of plastic straws. Their dedication to sustainable production processes places them at the forefront of the market.

Hoffmaster Group, Inc. has established itself as a leader in the disposable products industry, leveraging its strong brand presence and diversified product range. Their continuous investment in research and development for biodegradable paper straws highlights their efforts to align with growing consumer demand for sustainable products.

Transcend Packaging is known for its eco-conscious approach to manufacturing paper straws, with a strong emphasis on circular economy principles. Their ability to innovate in terms of product design and material sourcing allows them to meet both regulatory demands and environmental sustainability goals effectively.

Jinhua Suyang Plastic Material Co., Ltd. excels in offering high-quality paper straws tailored for a variety of markets globally. Their focus on producing durable, aesthetically pleasing, and food-safe paper straws ensures they remain a competitive player in an increasingly crowded market.

Top Key Players in the Market

- Matrix Pack

- Hoffmaster Group, Inc.

- Transcend Packaging

- Jinhua Suyang Plastic Material Co., Ltd.

- BioPak

- Strawland

- Novolex

- Footprint

- Huhtamaki Group

- Tetra Laval Group

Recent Developments

- In January 2024, Reedest secured €3 million in funding to develop and promote eco-friendly alternatives by replacing traditional paper straws with sustainable Estonian reed-based straws. This investment aims to boost greener packaging solutions in the beverage industry.

- In May 2025, a paper straw manufacturer in Illinois faced a severe decline in business following political pressure from former President Trump advocating a return to plastic straws. This shift impacted the regional demand for biodegradable straw products significantly.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 2.6 Billion |

| Forecast Revenue (2034) | USD 11.2 Billion |

| CAGR (2025-2034) | 15.7% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Product (Non-Printed, Printed), By Material (Virgin Paper, Recycled Paper), By Diameter (0.196 – 0.25 Inches, <0.15 Inches, 0.15 – 0.196 Inches, > 0.4 Inches, 0.25 – 0.4 Inches), By Sales Channel (B2B 68.2, B2C), By Straw Length (7.75-8.5 Inches, 5.75-7.75 Inches, 8.5-10.5 Inches, > 10.5 Inches, <5.75 Inches), By End Use (Foodservice, Institutional, Household) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | Matrix pack, Hoffmaster Group, Inc., Transcend Packaging, Jinhua Suyang Plastic Material Co., Ltd., BioPak, Strawland, Novolex, Footprint, Huhtamaki Group, Tetra Laval Group |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |