Quick Navigation

Report Overview

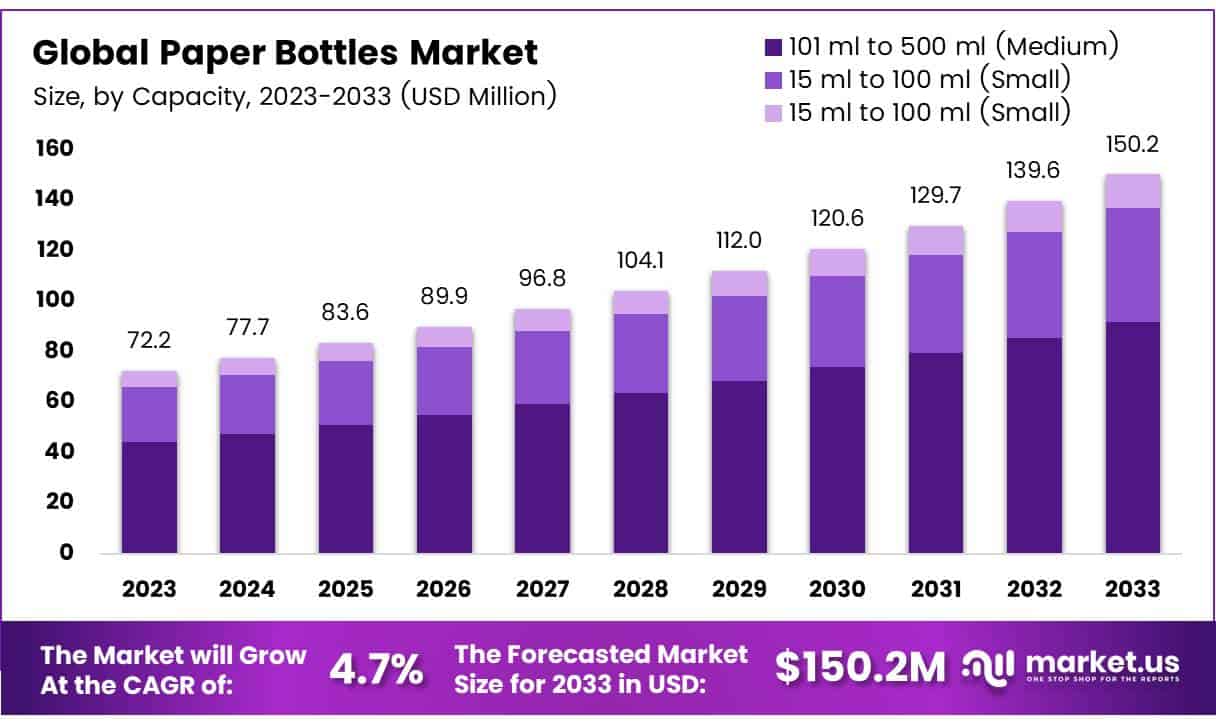

The Global Paper Bottles Market size is expected to be worth around USD 150.2 Million by 2033, from USD 72.2 Million in 2023, growing at a CAGR of 7.6% during the forecast period from 2024 to 2033.

Paper bottles are an innovative packaging solution, offering a sustainable alternative to traditional plastic and glass containers. Made primarily from biodegradable materials such as recycled paper and sugarcane, these bottles are designed to have a smaller environmental impact, degrading faster than plastics and reducing landfill waste.

The demand for paper bottles is rising, driven by growing consumer awareness and regulatory pressures for sustainable packaging options across various sectors including beverages, personal care, and household cleaning products. The global push for reducing plastic waste and preference for eco-friendly products are key factors fueling the growth of this market.

Significant opportunities exist for companies specializing in material technologies to develop more advanced paper bottle products suitable for a broader range of uses. Additionally, consumer goods companies can leverage these eco-friendly bottles to enhance their brand image and appeal to environmentally conscious consumers.

Government regulations limiting plastic use and encouraging greener alternatives are also advantageous for the paper bottle market. These may include financial incentives for companies that adopt sustainable packaging practices.

Furthermore, governmental investment in recycling infrastructure and technology research could hasten the development and adoption of paper bottles, supporting environmental objectives and fostering market expansion by creating a stronger sustainable packaging ecosystem.

The urgency for solutions like paper bottles is underscored by staggering statistics regarding plastic waste. In North Carolina alone, over $41 million worth of plastic is discarded annually, a clear indication of the financial and environmental costs associated with plastic waste. This waste represents a significant opportunity for the paper bottle market to offer a financially sensible and environmentally sustainable alternative.

Moreover, the vast consumption of single-use plastic bottles in the USA, where 50 billion are purchased each year and less than 30% are recycled, highlights the critical need for effective recycling systems and alternative packaging solutions like paper bottles. These figures not only demonstrate the scale of the problem but also the substantial market potential for alternatives.

Additionally, the fact that 85% of Americans now use reusable water bottles illustrates a significant shift in consumer behavior towards sustainability. This shift in consumer attitudes further opens the door for paper bottles, as both individuals and corporations seek out more sustainable, practical alternatives to traditional packaging materials.

Key Takeaways

- The global paper bottles market is projected to grow from USD 72.2 million in 2023 to USD 150.2 million by 2033, at a CAGR of 7.6%.

- In 2023, the 101 ml to 500 ml capacity segment led the market, catering to consumer preferences for moderate-sized, sustainable packaging solutions widely used in personal care, pharmaceuticals, and food and beverages.

- The Everyday category, covering daily use items like household cleaners and personal care products, has achieved significant market adoption, reflecting strong consumer demand for sustainable packaging.

- Water packaging dominates the paper bottles market’s end-use segment, highlighting increasing consumer focus on sustainable packaging driven by environmental concerns.

- North America leads the paper bottles market, with the U.S. and Canada pioneering in the adoption of sustainable packaging practices supported by technological advancements and regulatory incentives.

Capacity Analysis

101 ml to 500 ml (Medium) Sized Bottles Lead in 2023

In 2023, the 101 ml to 500 ml (Medium) category held a dominant market position in the By Capacity Analysis segment of the Paper Bottles Market. This size range effectively addresses consumer preferences for moderate quantity packaging solutions, which are extensively used in industries such as personal care, pharmaceuticals, and food and beverages.

The appeal of medium-sized paper bottles stems from their convenience for daily use products and their compatibility with emerging sustainability trends, which prioritize eco-friendly packaging solutions.

Conversely, the 15 ml to 100 ml (Small) capacity paper bottles cater primarily to niche markets that require smaller quantities, such as sample-sized beauty products or specialty beverages. Although smaller in market share, these bottles meet specific customer needs for portability and minimal product waste.

The Above 500 ml (Large) category serves markets requiring larger volumes, including bulk household items and industrial supplies. This segment, while less prevalent in consumer goods, plays a critical role in sectors focused on reducing plastic use in packaging bulk products.

Collectively, these segments underscore the diverse applications of paper bottles across different market sectors, highlighting their growing acceptance as sustainable alternatives to traditional packaging materials. The dominance of the medium-sized category reflects a balanced approach to practicality and sustainability, a key factor driving its widespread market acceptance.

Primary Usage Analysis

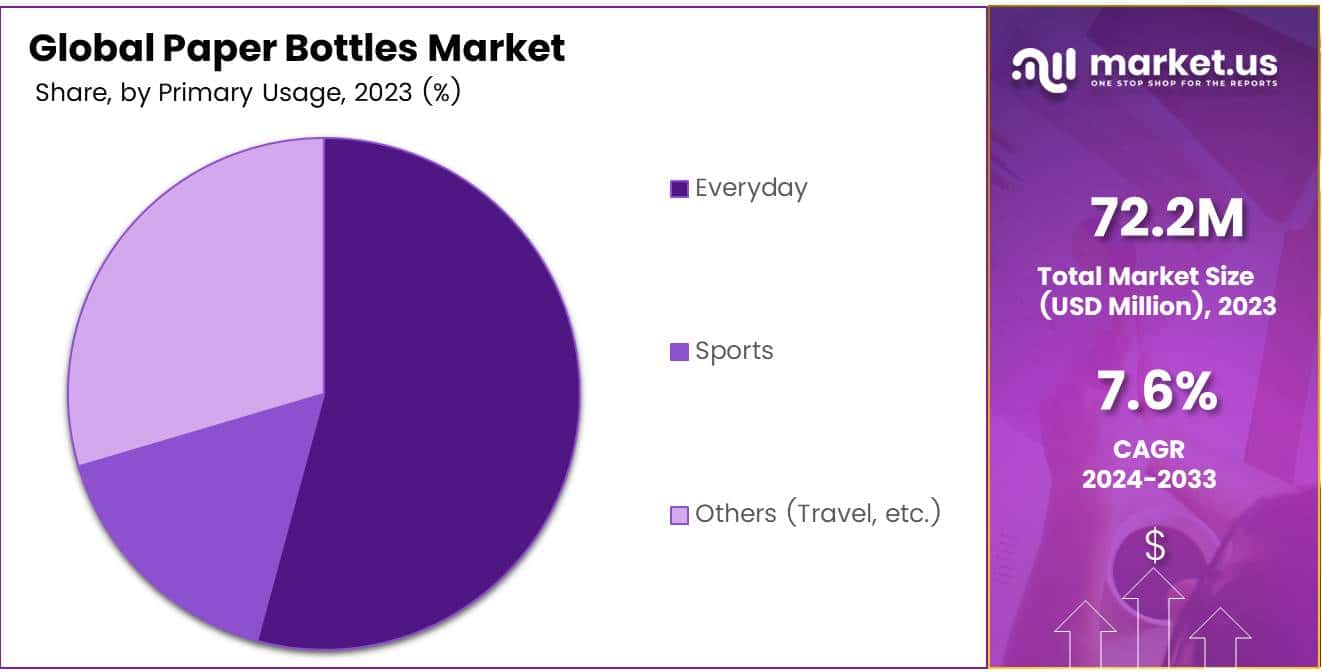

Everyday Leads in Paper Bottle Usage

In 2023, Everyday held a dominant market position in the By Primary Usage Analysis segment of the Paper Bottles Market. This segment has seen substantial growth due to increasing consumer demand for sustainable packaging solutions in daily use products.

The Everyday category, encompassing items routinely used by consumers, such as household cleaners and personal care products, has significantly outperformed other segments in terms of adoption and market penetration.

The Sports segment, though smaller, shows promising expansion, driven by the sports and fitness industry’s shift towards eco-friendly products. Paper bottles in this segment are primarily used for packaging nutritional supplements and hydrating beverages, aligning with consumers’ growing environmental consciousness and their demand for sustainable options.

The Others segment, which includes travel and miscellaneous uses, also demonstrates steady growth. Innovations in paper bottle durability and functionality have broadened their applicability in diverse fields such as travel-size toiletries and industrial products, enhancing their market presence.

Overall, the diverse applications of paper bottles across these segments underscore the market’s response to a global push for sustainability, with the Everyday segment leading the charge due to its broad consumer base and frequent product usage.

End Use Analysis

Water Leads in Paper Bottle End Use

In 2023, water held a dominant market position in the By End Use Analysis segment of the paper bottles market. This prominence can be attributed to escalating consumer demand for sustainable packaging solutions amidst rising environmental concerns.

Water brands, in their pursuit of eco-friendly alternatives, have increasingly adopted paper bottles to align with global sustainability targets and consumer preferences for greener products.

Further segments of the paper bottles market include beverages, which are subdivided into alcoholic and non-alcoholic categories. Alcoholic beverages in paper bottles are gradually gaining traction, driven by craft brands looking to differentiate themselves through sustainable packaging.

Non-alcoholic beverages, such as juices and soft drinks, are also transitioning towards paper-based solutions, although at a slower pace compared to water.

The personal care and cosmetics segment is emerging as a significant adopter of paper bottles, leveraging the packaging to enhance brand image and appeal to environmentally conscious consumers. Other areas, such as home care and toiletries, are exploring paper bottles, driven by similar motives of sustainability and consumer preference shifts.

Overall, the diverse application across these segments underscores the versatility and growing acceptance of paper bottles as a sustainable packaging alternative.

Key Market Segments

By Capacity

- 101 ml to 500 ml (Medium)

- 15 ml to 100 ml (Small)

- Above 500 ml (Large)

By Primary Usage

- Everyday

- Sports

- Others (Travel, etc.)

By End Use

- Water

- Beverage

- Alcoholic

- Non-alcoholic

- Personal Care &Cosmetics

- Others (Homecare & Toiletries, etc.)

Drivers

Eco-Conscious Packaging on the Rise

Driven by heightened environmental concerns, the market for paper bottles is expanding as individuals and companies alike seek sustainable alternatives to reduce plastic waste. As consumers increasingly favor environmentally friendly products, businesses are responding by adopting innovative, green packaging solutions.

Moreover, corporate commitments to sustainability goals are further propelling the adoption of paper bottles. This shift towards paper bottles represents a proactive effort by various industries to minimize their ecological footprint, aligning with broader global initiatives for environmental stewardship.

By leveraging eco-friendly materials, companies not only comply with regulatory pressures but also enhance their brand image among consumers who prioritize sustainability. This convergence of consumer preferences and corporate responsibility is catalyzing significant growth in the paper bottles market, marking a pivotal step in the packaging sector’s evolution towards sustainability.

Restraints

Cost Concerns Limit Paper Bottle Adoption

Paper bottles market, it is observed that there are significant restraints impacting its broader acceptance and integration. Primarily, cost concerns arise as a major hurdle; the initial production and material expenses for paper bottles are notably higher compared to conventional plastic packaging.

This economic disadvantage may deter manufacturers and consumers alike from transitioning to paper bottle solutions, especially in cost-sensitive markets.

Furthermore, there are performance issues to consider. Paper bottles, in their current stage of development, may not consistently offer the same durability and functionality as their plastic counterparts. This limitation can affect consumer confidence and adoption rates, particularly in sectors where product integrity and longevity are paramount.

These factors collectively pose challenges to the widespread adoption of paper bottles, as potential users weigh the trade-offs between environmental benefits and practical usability.

Growth Factors

Expansion into New Markets Tapping into Fresh Opportunities

As markets increasingly adopt stringent regulations against plastic use, the paper bottles market stands at the threshold of significant growth opportunities. Companies poised to penetrate these new regions can capitalize on the demand for sustainable packaging solutions.

Innovations in product design, such as multi-layered constructions and advanced protective coatings, are enhancing the functional appeal of paper bottles, aligning with consumer expectations for durability and quality.

Furthermore, vertical integration presents a strategic advantage; by managing more stages of the production and distribution chain, businesses can achieve greater operational efficiencies and cost reductions.

This integrated approach not only streamlines processes but also fortifies supply chain resilience, positioning market players as frontrunners in the eco-friendly packaging industry. These opportunities, if leveraged correctly, could redefine market dynamics and set new standards in sustainability and consumer satisfaction.

Emerging Trends

Eco-Design Innovations Drive Market Appeal

The paper bottles market is experiencing significant growth, primarily driven by advancements in eco-design that enhance both appeal and functionality. These innovations are pivotal in addressing consumer demands for sustainable packaging solutions, thereby expanding market penetration.

Additionally, the integration of recycled and upcycled materials in the manufacturing process is not only improving the environmental footprint of these products but also aligning with global sustainability targets.

This trend is further bolstered by the endorsement of celebrities and influencers, which has substantially increased consumer awareness and acceptance of paper bottles.

Such endorsements are crucial as they amplify the market visibility of paper bottles, potentially accelerating their adoption across various sectors including beverages, personal care, and household cleaners. Collectively, these factors are catalyzing the paper bottles market, making it a noteworthy contender in the sustainable packaging industry.

Regional Analysis

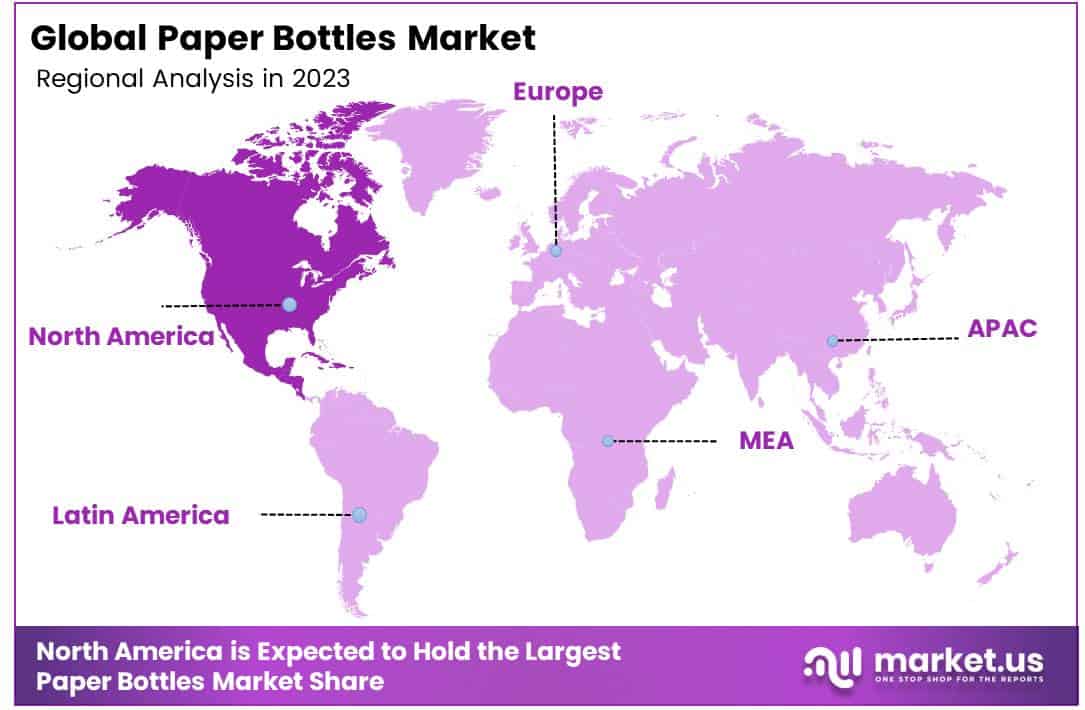

North America dominating region in the paper bottles market

In the dynamic landscape of the global paper bottles market, distinct regional variations reflect the diverse consumer preferences, regulatory environments, and economic conditions across North America, Europe, Asia Pacific, Middle East & Africa, and Latin America.

North America is the dominating region in the paper bottles market, driven by a robust shift towards sustainable packaging solutions among consumers and stringent regulatory standards advocating for environmental conservation.

The U.S. and Canada are at the forefront, with initiatives and incentives promoting the adoption of eco-friendly materials in packaging industries. This region’s market is characterized by high technological advancements and the presence of key market players focused on innovative, sustainable packaging solutions.

Regional Mentions:

Europe follows closely, with a significant emphasis on reducing plastic waste and carbon footprints, particularly in countries like Germany, the UK, and France. The European Union’s stringent regulations on single-use plastics and the overarching policy framework favoring circular economy models have catalyzed the adoption of paper bottles across various sectors including cosmetics, pharmaceuticals, and beverages.

In the Asia Pacific region, rapid urbanization and increasing consumer awareness about sustainable products are propelling the market forward. Countries such as China, Japan, and India are experiencing a surge in demand for eco-friendly packaging solutions, driven by both governmental policies and the growing middle-class consumer base demanding greener alternatives.

The Middle East & Africa region, although emerging in the paper bottles market, shows potential for growth due to increasing environmental concerns and economic diversification away from oil-dependent industries. Countries like UAE and Saudi Arabia are gradually adopting sustainable practices in various sectors including retail and hospitality, which in turn supports market growth in this region.

Latin America also presents a promising growth trajectory in the paper bottles market with countries like Brazil and Argentina leading the way. The region benefits from abundant raw materials and a growing inclination towards sustainable development, spurred by both local and international environmental campaigns.

Overall, while North America currently dominates the paper bottles market, other regions are also showing rapid progress, each contributing uniquely to the global market dynamics through regional trends, consumer behavior, and regulatory frameworks.

Key Regions and Countries covered іn thе rероrt

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

In the global Paper Bottles Market in 2023, several key players are shaping the competitive landscape, each contributing distinct technological advancements and strategic market initiatives.

Frugalpac stands out with its innovative approach towards recyclable paper-based packaging solutions. The company’s products are designed to reduce carbon footprint significantly, which aligns with the global push towards sustainable packaging solutions. Similarly, PAPACKS Sales GmbH excels in offering bespoke biodegradable packaging solutions, positioning itself as a frontrunner in the eco-friendly sector by prioritizing circular economy principles.

LYS Packaging ventures into the market with a unique angle, focusing on vegan bottles made from sugarcane, offering a compelling alternative to traditional paper packaging by reducing the use of wood pulp. This innovation not only enhances sustainability but also taps into the niche market of eco-conscious consumers.

Paper Water Bottle is another noteworthy competitor, pioneering the use of biocomposite materials derived from natural resources to create bottles. Their technology reflects a significant advancement in reducing reliance on plastics and promoting compostable alternatives.

Choose Packaging introduces another layer of innovation with its zero-plastic solutions that are both home-compostable and recyclable. This approach meets the increasing consumer demands for packaging that supports environmental stewardship without compromising functionality.

Lastly, Pulpex Ltd. collaborates with several global brands to produce paper bottles for a variety of liquids, showcasing scalability and versatility in applying paper bottle technology across different market segments.

These companies, along with others like Pulp Packaging International and Shruti Agro, are pivotal in driving forward the adoption of paper bottle solutions, each contributing to a more sustainable and innovative market landscape.

Top Key Players in the Market

- Frugalpac

- PAPACKS Sales GmbH

- LYS Packaging

- Paper Water Bottle

- Choose Packaging

- Pulp Packaging International

- Pulpex Ltd.

- Shruti Agro

- 3Epack Group

- Kagzi Bottles

- Just Water

- Paper Bottle Company

Recent Developments

- In February 2024, Paboco announced plans to escalate its production capacity, aiming to operate four production lines and deliver over 20 million paper bottles by the end of 2025, starting with at least 10,000 bottles.

- In September 2024, Diageo launched an on-trade trial of a 90% paper-based bottle for Johnnie Walker Black Label, marking a significant advancement in sustainable packaging for the beverage industry.

- In September 2024, Novvia Group expanded its market reach and capabilities by acquiring Liquid Bottles, enhancing its distribution and production in the packaging sector.

- In February 2024, Owens-Illinois announced an investment of R$300 million to increase glass bottle production amidst a significant bottle shortage, aiming to meet escalating market demand.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2023) | USD 72.2 Million |

| Forecast Revenue (2033) | USD 150.2 Million |

| CAGR (2024-2033) | 7.6% |

| Base Year for Estimation | 2023 |

| Historic Period | 2019-2022 |

| Forecast Period | 2024-2033 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Capacity (101 ml to 500 ml, 15 ml to 100 ml, Above 500 ml), By Primary Usage (Everyday, Sports, Others), By End Use (Water, Beverage(Alcoholic, Non-alcoholic), Personal Care and Cosmetics, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Frugalpac, PAPACKS Sales GmbH, LYS Packaging, Paper Water Bottle, Choose Packaging, Pulp Packaging International, Pulpex Ltd., Shruti Agro, 3Epack Group, Kagzi Bottles, Just Water, Paper Bottle Company |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |