Quick Navigation

- Report Overview

- Top Market Takeaways

- Drivers Impact Analysis

- Restraints Impact Analysis

- By Component Analysis

- By Application Analysis

- By End User Analysis

- Investor Type Impact Analysis

- Technology Enablement Analysis

- Key Challenges

- Emerging Trends

- Growth Factors

- Key Market Segments

- Regional Analysis

- Competitive Analysis

- Future Outlook

- Recent Developments

- Report Scope

Report Overview

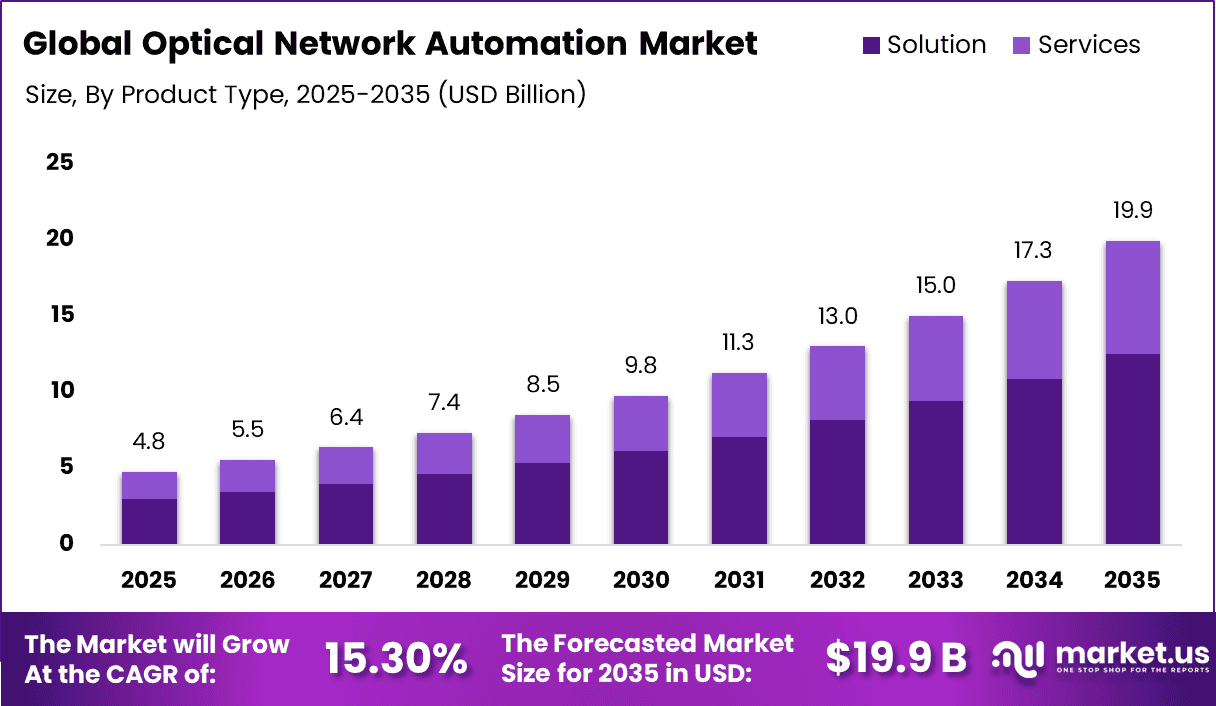

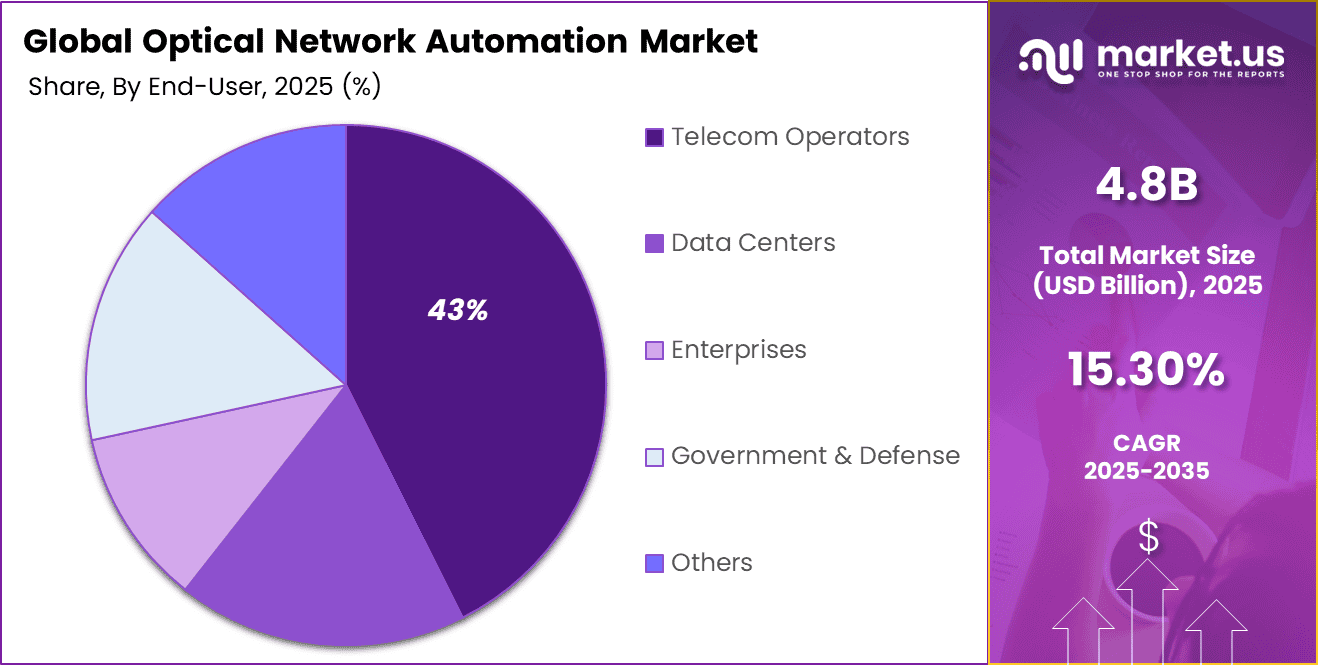

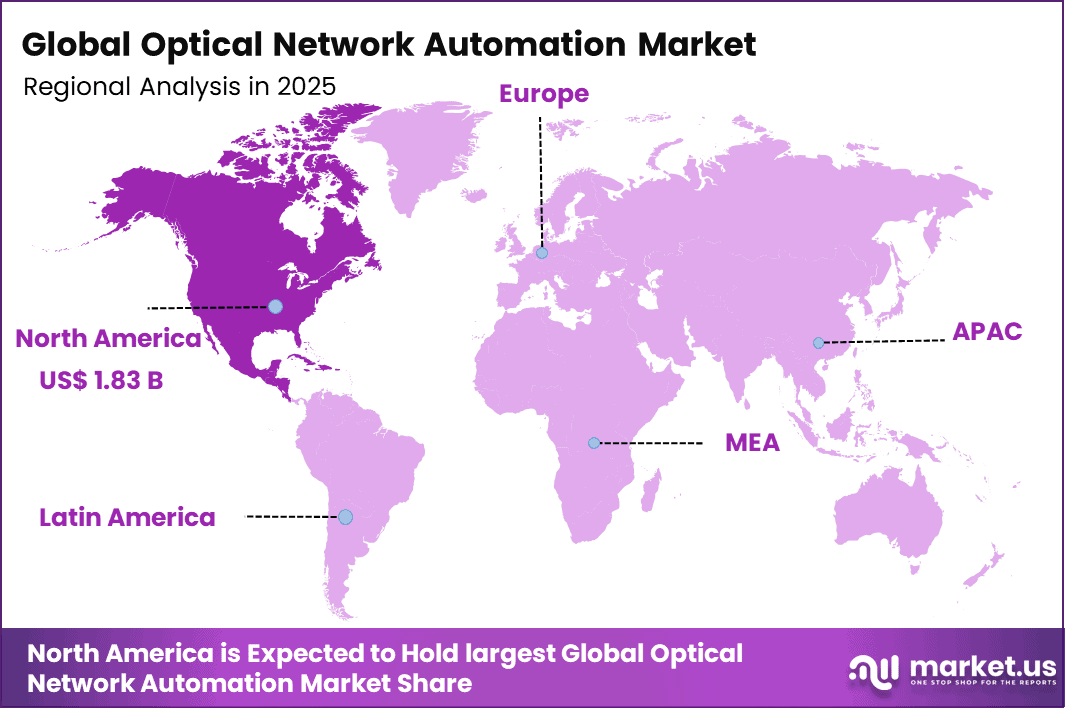

The Global Optical Network Automation Market generated USD 4.8 billion in 2025 and is predicted to register growth from USD 5.5 billion in 2026 to about USD 19.9 billion by 2035, recording a CAGR of 15.30% throughout the forecast span. In 2025, North America held a dominan market position, capturing more than a 38.3% share, holding USD 1.83 Billion revenue.

Top Market Takeaways

- Solution commands 62.9% market share, delivering intent-based controllers, closed-loop automation, and AIOps platforms for zero-touch optical layer management.

- Network provisioning applications capture 31.4%, enabling dynamic wavelength allocation, service turn-up automation, and bandwidth-on-demand across DWDM and coherent optics fabrics.

- Telecom operators hold 42.6%, leveraging automation for multi-vendor interoperability, submarine cable systems, and metro/regional network scalability.

- North America drives 38.3% global value, with U.S. market at USD 1.61 billion and 13.2% CAGR, fueled by hyperscaler dark fiber leases and Ciena/Nokia deployments.

Optical Network Automation market refers to software driven solutions that automate the provisioning, monitoring, control, and optimization of optical transport networks. These systems help operators manage fiber resources, service activation, fault handling, and traffic routing with less manual effort. The market is gaining importance as optical networks become more complex and operators look for faster, more efficient ways to manage high capacity transport infrastructure.

One of the main factors driving this market is the growing need to simplify optical network operations and improve service agility. Operators want automation that can reduce manual configuration work, speed up service delivery, and improve use of network resources.

Another important factor is the shift toward software based network management, which supports better coordination across transport layers and helps operators respond more quickly to changing bandwidth needs.

Demand for optical network automation is increasing among telecom operators, cloud network providers, and large enterprises that manage high capacity fiber networks. These users want practical tools that can improve network visibility, reduce operational workload, and support faster service changes. Demand is also rising because traffic patterns are becoming more dynamic, which makes automated control and optimization more important in daily network management.

Drivers Impact Analysis

| Key Driver | Impact on CAGR Forecast (~%) | Geographic Relevance | Impact Timeline | Strategic Effect |

|---|---|---|---|---|

| Increasing demand for high speed data transmission and bandwidth | +3.1% | North America, Europe, Asia Pacific | Short to Mid Term (2025–2031) | Enhances optical network efficiency |

| Rapid deployment of 5G and fiber optic infrastructure | +2.8% | Asia Pacific, North America, Europe | Mid Term (2026–2032) | Expands need for automated network control |

| Growing adoption of software defined and programmable networks | +2.6% | Global | Mid Term (2026–2032) | Improves network flexibility |

| Expansion of data centers and cloud services | +2.4% | Global | Mid to Long Term (2026–2035) | Drives demand for network automation |

| Telecom operators focus on reducing operational complexity | +2.2% | Global | Mid to Long Term (2026–2035) | Supports automation adoption |

Restraints Impact Analysis

| Key Restraint | Impact on CAGR Forecast (~%) | Geographic Relevance | Impact Timeline | Strategic Effect |

|---|---|---|---|---|

| High cost of deploying advanced automation solutions | -2.4% | Global | Mid Term (2026–2032) | Limits adoption among smaller operators |

| Complexity in integrating legacy optical systems | -2.2% | North America, Europe | Mid Term (2026–2032) | Delays modernization |

| Lack of skilled workforce in network automation | -2.0% | Global | Mid Term (2026–2032) | Slows implementation |

| Interoperability challenges across multi vendor environments | -1.8% | Global | Mid Term (2026–2032) | Creates deployment issues |

| Data security and compliance concerns | -1.6% | Europe, North America | Mid to Long Term (2026–2035) | Restricts adoption |

By Component Analysis

Solution accounted for 62.9% of the Optical Network Automation Market. This segment leads because organizations rely on software driven platforms to automate network configuration, monitoring, and performance management. These solutions reduce manual intervention and enable faster control over complex optical network operations.

The segment is also supported by the need for efficient network management as data traffic increases. Automated solutions help operators optimize resource allocation, detect issues early, and improve service reliability, which strengthens their adoption across modern communication networks.

By Application Analysis

Network provisioning represented 31.4% of the market. This segment dominates because automation plays a key role in setting up network services quickly and accurately. Automated provisioning reduces the time required to activate services and ensures consistent configuration across network infrastructure.

The segment is driven by growing demand for rapid service deployment. Telecom operators and enterprises use automated provisioning to improve operational efficiency and respond faster to customer requirements, which supports strong growth in this application area.

By End User Analysis

Telecom operators accounted for 43% of the market. This segment leads because telecom companies manage large scale optical networks and require automation to handle increasing data traffic and service complexity. Automation tools help improve network performance and reduce operational workload.

The segment is supported by continuous expansion of communication networks and rising demand for high speed connectivity. Telecom operators invest in automation solutions to enhance efficiency, maintain service quality, and manage network operations more effectively.

Investor Type Impact Analysis

| Investor Type | Growth Sensitivity | Risk Exposure | Geographic Focus | Investment Outlook |

|---|---|---|---|---|

| Venture Capital Firms | High | Medium | US, Europe | Growth in network automation startups |

| Private Equity Firms | High | Medium | North America, Europe | Expansion in telecom automation |

| Strategic Technology Investors | Very High | Medium | US, China, Japan | Strengthens optical networking ecosystem |

| Corporate Venture Arms | High | Medium | Global | Supports telecom partnerships |

| Government and Infrastructure Funds | Medium | Low | Asia Pacific, Europe | Supports digital connectivity initiatives |

Technology Enablement Analysis

| Technology Enabler | Impact on CAGR Forecast (~%) | Geographic Relevance | Impact Timeline | Implementation Significance |

|---|---|---|---|---|

| Software defined optical networking platforms | +3.2% | Global | Short to Mid Term (2025–2031) | Enables programmable control |

| AI driven network optimization and automation | +2.9% | Global | Mid Term (2026–2032) | Improves operational efficiency |

| Integration with 5G and high speed fiber networks | +2.7% | North America, Asia Pacific, Europe | Mid Term (2026–2032) | Enhances performance |

| Cloud based orchestration and management tools | +2.5% | Global | Mid Term (2026–2032) | Supports scalable deployment |

| Real time monitoring and analytics systems | +2.3% | Global | Mid to Long Term (2026–2035) | Improves network visibility |

Key Challenges

- Integration with existing optical network infrastructure is a major challenge because many operators still use older hardware, software, and vendor specific systems.

- Real time visibility is difficult because optical networks are complex, and automation tools must monitor traffic, faults, and performance across many links and nodes.

- Interoperability remains a key issue because automation platforms often need to work with equipment from different vendors that follow different interfaces and control methods.

- Deployment cost can be high because optical network automation may require software upgrades, system redesign, training, and skilled technical support.

- Cybersecurity is also a growing concern because automated optical networks depend on centralized control and connected systems that may face unauthorized access or service disruption.

Emerging Trends

A key trend in the Optical Network Automation market is the increasing shift toward intelligent network control systems that automate provisioning, monitoring, and optimization of optical infrastructure.

Operators are adopting solutions that can adjust bandwidth, reroute traffic, and detect issues in real time without manual intervention. These systems rely on advanced analytics to improve network visibility and responsiveness. This trend reflects a move toward self managing networks where operations become more efficient and adaptable to changing data demands.

Growth Factors

The growing demand for high capacity and reliable data transmission is supporting the expansion of optical network automation solutions. As data traffic continues to rise across enterprises and communication networks, operators require tools that can manage optical resources efficiently.

Automation helps reduce operational complexity and improves service quality by ensuring consistent performance. At the same time, the need to handle dynamic workloads and maintain network stability encourages the adoption of solutions that support faster and more efficient network operations.

Key Market Segments

By Component

- Solution

- Provisioning & Activation

- Fault Management

- Performance Monitoring

- Network Orchestration

- Others

- Services

- Managed Services

- Professional Services

By Application

- Network Provisioning

- Network Optimization

- Fault Management

- Performance Management

- Security Management

- Others

By End-User

- Telecom Operators

- Data Centers

- Enterprises

- Government & Defense

- Others

Regional Analysis

North America accounted for 38.3% of the Optical Network Automation Market, reflecting strong adoption of intelligent network management across telecom and data center environments. Service providers across the region increasingly deploy automation solutions to manage complex optical networks, optimize bandwidth usage, and improve service reliability. The rising demand for high speed connectivity, cloud services, and data traffic continues to drive the need for automated control and monitoring systems across North America.

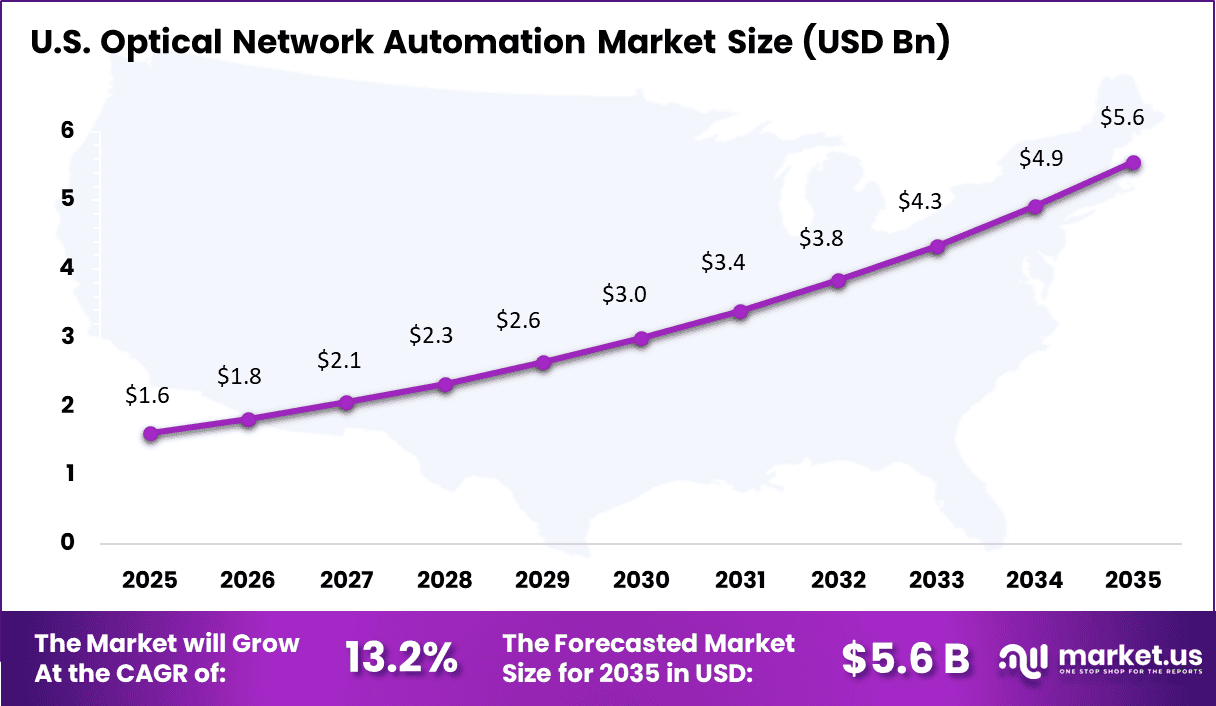

The U.S. generated about USD 1.61 Billion within the regional market and is projected to expand at a CAGR of 13.2%. Telecom operators and network providers across the country continue to invest in automation tools that enhance network visibility, reduce manual operations, and support faster service provisioning.

Optical network automation enables efficient fault detection, real time adjustments, and improved resource utilization. As digital infrastructure expands and network complexity increases, demand for automated optical network solutions continues to grow steadily across the US market.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherlands

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Thailand

- Vietnam

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Competitive Analysis

The competitive landscape of the Optical Network Automation market includes major telecom and optical networking companies that provide software, controllers, and transport systems for smarter network operations.

Ciena Corporation, Nokia Corporation, Huawei Technologies Co., Ltd., Infinera Corporation, ADVA Optical Networking SE, Cisco Systems, Inc., Fujitsu Limited, NEC Corporation, and Juniper Networks hold strong positions because they offer broad optical networking portfolios and strong expertise in automation, traffic management, and network efficiency.

Other companies such as Corning Incorporated, IIVI Incorporated, and Lumentum Holdings Inc. support competition through optical components, connectivity technologies, and transmission solutions that improve overall network performance.

The market is shaped by demand for lower operational complexity, faster service provisioning, better bandwidth control, and stronger network visibility. Overall, companies compete through automation strength, integration capability, and the ability to support high capacity fiber networks.

Top Key Players in the Market

- Ciena Corporation

- Nokia Corporation

- Huawei Technologies Co., Ltd.

- Infinera Corporation

- ADVA Optical Networking SE

- Corning Incorporated

- Cisco Systems, Inc.

- Fujitsu Limited

- NEC Corporation

- IIVI Incorporated

- Juniper Networks

- Lumentum Holdings Inc.

- Other Key Players

Future Outlook

The future outlook for the Optical Network Automation Market looks strong as telecom operators, cloud providers, and data center networks increasingly need faster service delivery, better visibility, and lower manual effort across complex optical infrastructure. Recent industry guidance shows growing focus on open and programmable optical networks, AI driven control, predictive operations, and centralized automation to handle rising traffic and more dynamic network demands. As bandwidth needs continue to grow with cloud services and AI workloads, demand for optical network automation solutions is expected to increase steadily in the coming years.

Recent Developments

- March,2026 – Ciena Navigator Network Control Suite integrated agentic AI across 500+ metro networks enabling hyper-rail photonics and 1.6T 160ZR pluggable optics with 2nm silicon design processing AI workloads at 70% lower TCO. Multi-layer automation eliminated IP/optical handoffs achieving 99.999% provisioning accuracy.

- February,2026 – Huawei iMaster NCE-FAN v6 orchestrated 800G DWDM across China Telecom spanning 1M+ km with ML fault prediction blocking 95% outages proactively. OTN Intent-Based Networking automated 10K+ services daily.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 4.8 Billion |

| Forecast Revenue (2035) | USD 19.9 Billion |

| CAGR(2025-2035) | 15.30% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue forecast, AI impact on Market trends, Share Insights, Company ranking, competitive landscape, Recent Developments, Market Dynamics and Emerging Trends |

| Segments Covered | By Component (Solution (Provisioning & Activation, Fault Management, Performance Monitoring, Network Orchestration, Others), Services (Managed Services, Professional Services)), By Application (Network Provisioning, Network Optimization, Fault Management, Others), By End-User (Telecom Operators, Data Centers, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Latin America; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Ciena Corporation, Nokia Corporation, Huawei Technologies Co., Ltd., Infinera Corporation, ADVA Optical Networking SE, Corning Incorporated, Cisco Systems, Inc., Fujitsu Limited, NEC Corporation, IIVI Incorporated, Juniper Networks, Lumentum Holdings Inc., Other Key Players |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three license to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |