Quick Navigation

- Report Overview

- Top Market Takeaways

- Drivers Impact Analysis

- Restraints Impact Analysis

- By Product Type Analysis

- By Application Analysis

- By End-User Analysis

- Investor Type Impact Analysis

- Technology Enablement Analysis

- Key Challenges

- Emerging Trends

- Growth Factors

- Key Market Segments

- Regional Analysis

- Competitive Analysis

- Future Outlook

- Recent Developments

- Report Scope

Report Overview

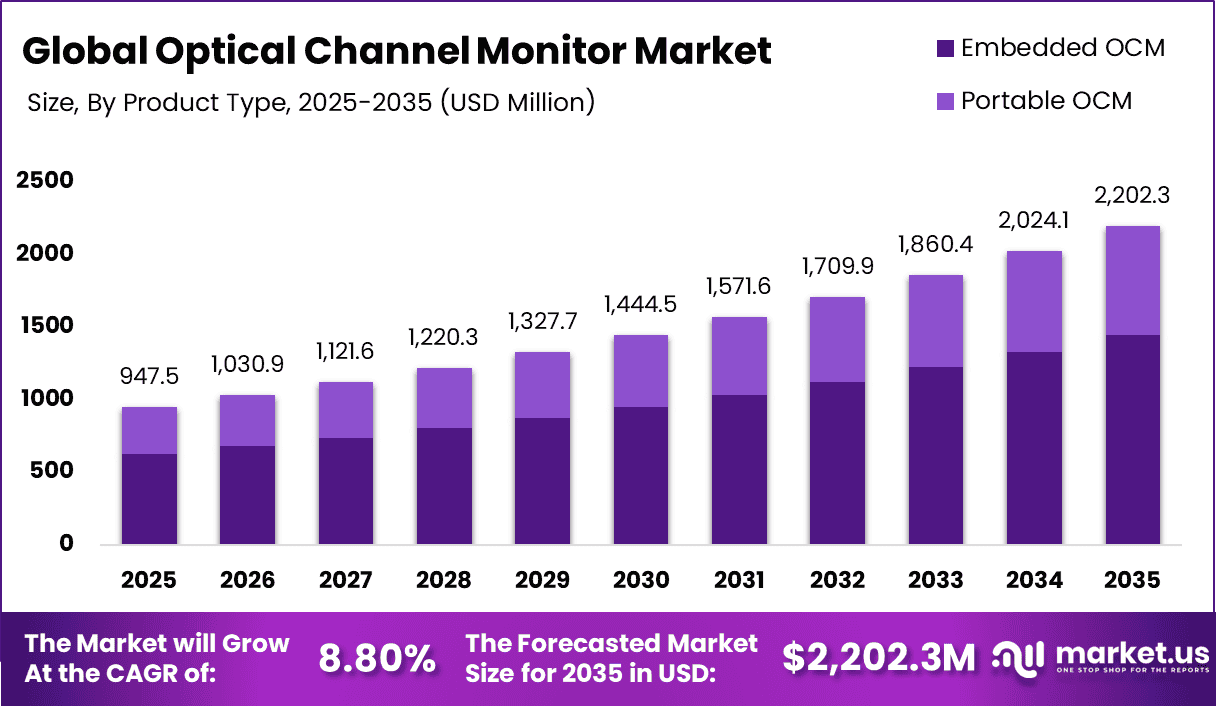

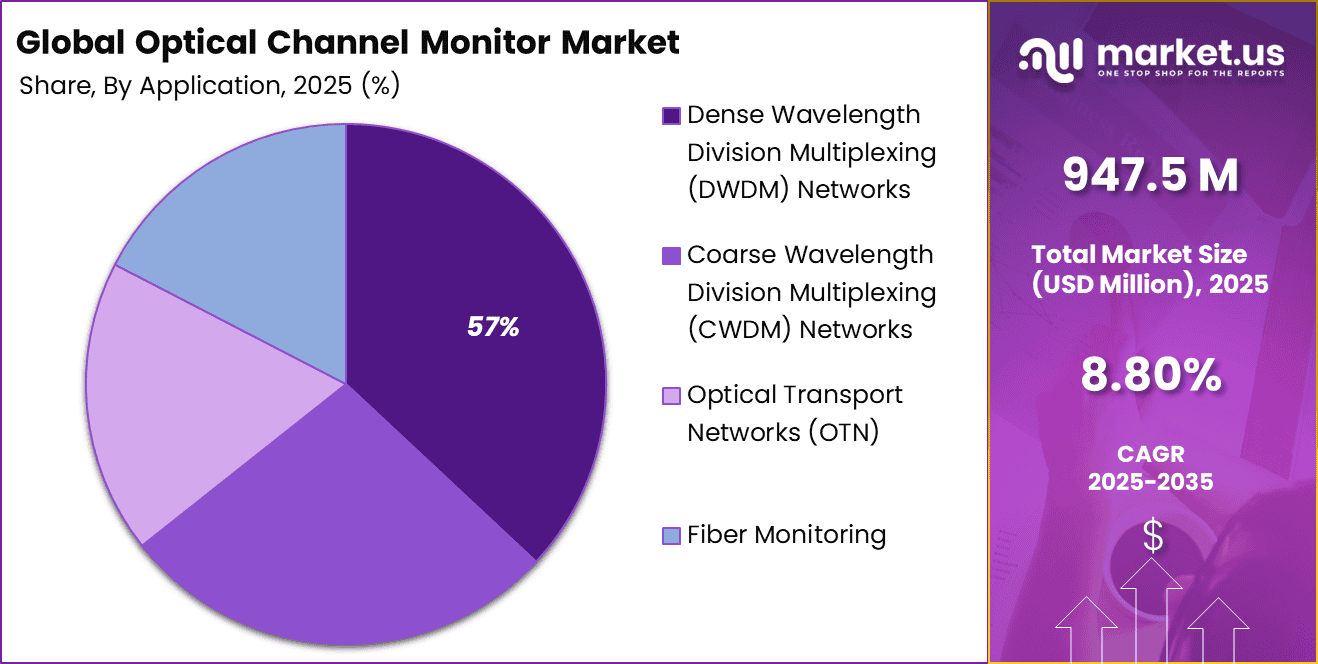

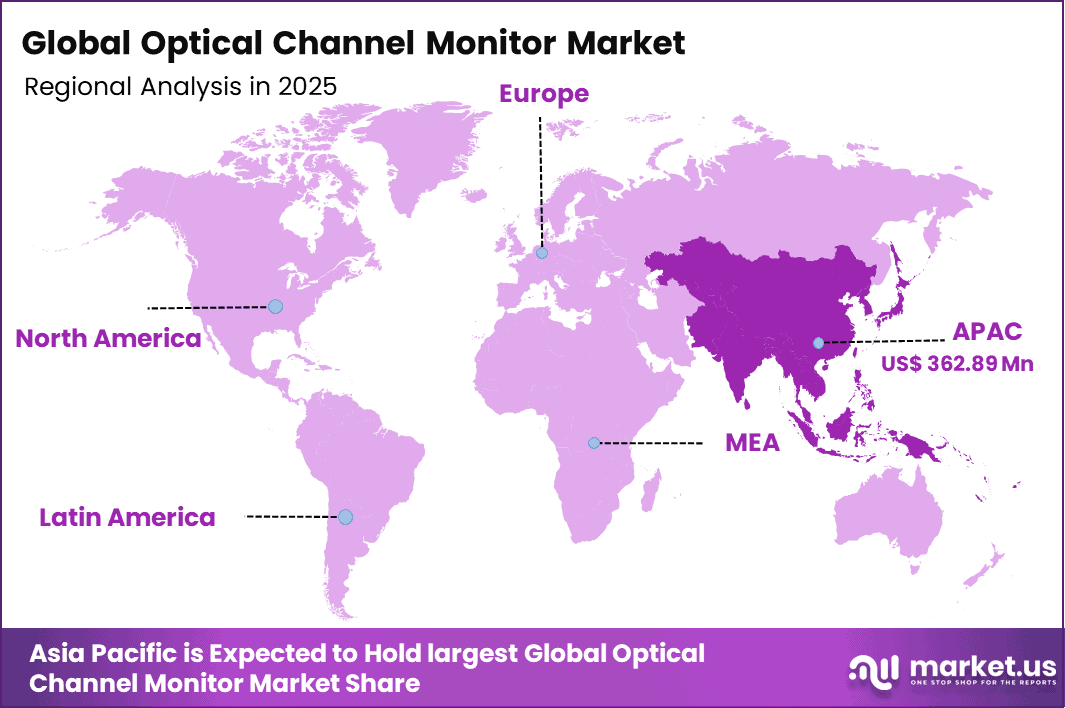

The Global Optical Channel Monitor Market generated USD 947.5 million in 2025 and is predicted to register growth from USD 1,030.9 million in 2026 to about USD 2,202.3 million by 2035, recording a CAGR of 8.80% throughout the forecast span. In 2025, Asia Pacific held a dominant market position, capturing more than a 38.3% share, holding USD 362.89 Million revenue.

Top Market Takeaways

- Embedded OCMs command 65.8% market share, delivering integrated wavelength monitoring, power leveling, and OSNR measurement within ROADM and EDFA systems for real-time channel performance.

- Dense Wavelength Division Multiplexing (DWDM) applications capture 56.7%, enabling C/L-band channel tracking, gain tilt compensation, and alien wavelength detection in high-capacity metro/long-haul networks.

- Telecommunications end-users hold 45.3%, leveraging OCMs for network optimization, fault isolation, and dynamic bandwidth allocation across multi-terabit optical infrastructures.

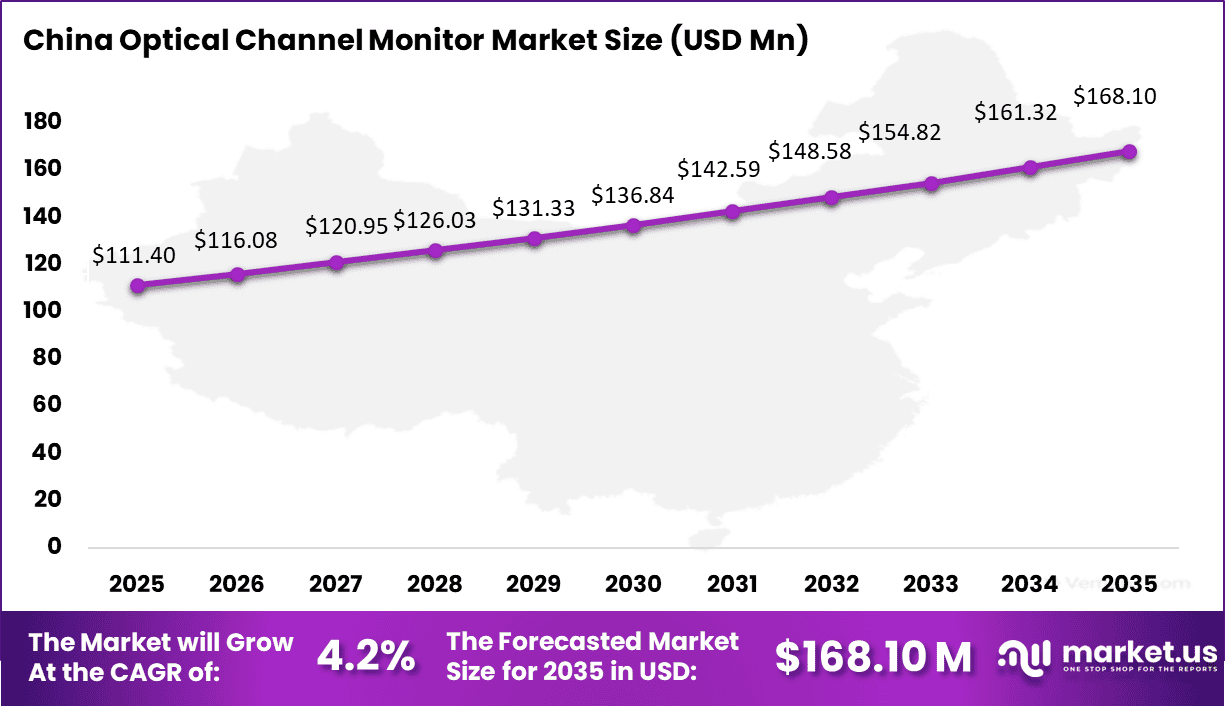

- APAC drives 38.3% global value, with China’s market at USD 111.4 million and 4.2% CAGR, fueled by state-backed fiber-to-the-x initiatives and submarine cable landings.

Optical channel monitors are used in fiber optic networks to measure and track signal performance across different wavelengths. These devices help operators monitor power levels, detect signal degradation, and maintain overall network quality.

As communication networks carry more data through high speed optical systems, the need for accurate monitoring has become more important. Optical channel monitoring is now a key part of network management, helping service providers ensure stable transmission and quickly identify faults before they impact performance.

One of the main driving factors is the rapid expansion of data traffic across telecom and data center networks. With growing use of cloud services, video streaming, and digital applications, network operators are under pressure to maintain high performance and reliability. Optical systems are becoming more complex, and this increases the need for tools that can provide detailed visibility into signal conditions.

In addition, the rollout of advanced network technologies and upgrades in fiber infrastructure are encouraging the use of monitoring solutions that can support higher capacity and longer transmission distances. The focus on reducing downtime and improving service quality is also pushing operators to invest in better monitoring systems.

Demand for optical channel monitors is increasing as network operators aim to improve efficiency and reduce operational risks. There is a strong preference for solutions that can provide real time data and support remote monitoring, allowing faster response to network issues.

Companies are also looking for systems that can integrate with existing network management platforms and provide clear insights for decision making. The need for automated monitoring is growing, as it reduces the reliance on manual checks and improves accuracy. As fiber networks continue to expand and evolve, the demand for reliable and precise optical monitoring solutions is expected to grow steadily.

Drivers Impact Analysis

| Key Driver | Impact on CAGR Forecast (~%) | Geographic Relevance | Impact Timeline | Additional Insight |

|---|---|---|---|---|

| Rising demand for high-capacity optical networks | +3.2% | North America, Europe, Asia Pacific | Medium to long term | Network upgrades increase monitoring needs |

| Growth in data traffic and bandwidth consumption | +3.0% | Global | Medium term | Higher traffic requires signal monitoring |

| Expansion of fiber optic infrastructure | +2.8% | Asia Pacific and North America | Medium to long term | Fiber rollout supports market growth |

| Increasing adoption of 5G and advanced telecom networks | +2.6% | Developed and emerging markets | Medium term | 5G drives need for optical performance tracking |

| Need for real-time network performance monitoring | +2.3% | Global | Short to medium term | Operators require continuous signal visibility |

Restraints Impact Analysis

| Key Restraint | Impact on CAGR Forecast (~%) | Geographic Relevance | Impact Timeline | Additional Insight |

|---|---|---|---|---|

| High cost of optical monitoring equipment | -2.7% | Emerging markets | Short to medium term | Cost limits widespread adoption |

| Complexity in integrating with existing network systems | -2.3% | Global | Medium term | Integration challenges delay deployment |

| Limited awareness in smaller telecom operators | -1.9% | Developing regions | Medium term | Smaller players adopt slowly |

| Requirement of skilled technical expertise | -1.6% | Global | Medium to long term | Skill gaps impact effective use |

| Maintenance and calibration challenges | -1.4% | Global | Long term | Regular upkeep increases operational burden |

By Product Type Analysis

The embedded OCM segment accounted for 65.8% of the market share, reflecting its strong role in enabling real-time monitoring within optical network systems. This dominance is supported by the ability of embedded solutions to be directly integrated into transmission equipment, which reduces the need for additional hardware and simplifies network architecture. Such integration improves operational efficiency and allows continuous performance tracking without disrupting network flow.

Another factor driving this segment is the increasing demand for compact and cost-effective monitoring solutions in high-capacity networks. Embedded OCM systems provide faster response times and better accuracy in detecting signal degradation. Their ability to support automated network management and fault detection makes them highly suitable for modern optical communication environments.

By Application Analysis

The dense wavelength division multiplexing segment held 57% share, driven by the growing need to transmit large volumes of data over long distances with high efficiency. DWDM technology enables multiple data signals to be transmitted simultaneously over a single optical fiber, which increases bandwidth capacity and network performance. Optical channel monitors play a critical role in ensuring signal quality and stability in such complex systems.

In addition, the expansion of high-speed data services and increasing internet traffic have strengthened the adoption of DWDM systems. Network operators rely on OCM solutions to monitor wavelength performance and prevent signal interference. This ensures reliable communication and supports the growing demand for high-capacity optical networks.

By End-User Analysis

The telecommunications segment captured 45.3% of the market, driven by the continuous expansion of communication infrastructure and rising demand for high-speed connectivity. Telecom operators require advanced monitoring tools to maintain network quality and ensure uninterrupted data transmission. Optical channel monitors help in detecting faults and optimizing network performance in real time.

Furthermore, the rapid growth of data consumption and the rollout of advanced communication technologies have increased the complexity of telecom networks. Operators are investing in efficient monitoring solutions to manage network loads and maintain service reliability. This has reinforced the importance of OCM systems in supporting large-scale telecommunications operations.

Investor Type Impact Analysis

| Investor Type | Growth Sensitivity | Risk Exposure | Geographic Focus | Investment Outlook |

|---|---|---|---|---|

| Venture capital firms | Moderate to high | High | US, Europe | Investing in advanced optical monitoring technologies |

| Private equity firms | Moderate | Moderate | North America and Europe | Scaling established telecom equipment providers |

| Corporate investors | High | Moderate | Global | Strategic investments in telecom infrastructure solutions |

| Institutional investors | Moderate | Low to moderate | Developed markets | Focus on stable telecom and network equipment firms |

| Government and public funding bodies | High | Low | Asia Pacific, EU | Supporting fiber expansion and telecom modernization |

Technology Enablement Analysis

| Technology | Impact on CAGR Forecast (~%) | Geographic Relevance | Impact Timeline | Additional Insight |

|---|---|---|---|---|

| AI-based optical signal analysis | +3.4% | US, Europe, Japan | Medium to long term | Improves accuracy of monitoring |

| Integration with software-defined networking (SDN) | +3.0% | Developed markets | Medium term | Enhances network control and flexibility |

| Cloud-based network monitoring platforms | +2.6% | North America and Europe | Short to medium term | Enables remote monitoring capabilities |

| Advanced wavelength monitoring technologies | +2.9% | Global | Medium to long term | Supports precise channel performance tracking |

| Automation in network diagnostics and fault detection | +2.5% | Global | Medium term | Reduces manual intervention and errors |

Key Challenges

- High cost of equipment makes it difficult for small operators to adopt.

- Complex installation and setup require skilled technicians.

- Integration challenges with existing optical network systems.

- Limited awareness in emerging markets slows adoption.

- Maintenance and calibration require regular effort and time.

- Data accuracy issues in high-density network environments.

- Dependence on advanced components increases supply chain risks.

- Rapid technology changes make systems outdated quickly.

- Power consumption adds to operational costs.

- Difficulty in real-time monitoring across large network infrastructures.

Emerging Trends

The optical channel monitor market is evolving with a strong focus on real time network visibility and intelligent performance tracking. One key emerging trend is the integration of advanced analytics within monitoring systems to detect signal degradation and performance issues at an early stage. These systems are becoming more proactive rather than reactive, allowing operators to maintain network quality without manual intervention.

Another important trend is the shift toward compact and embedded monitoring solutions that can be integrated directly into optical transport equipment, reducing the need for standalone devices. There is also growing adoption of software driven monitoring platforms that provide centralized control and remote diagnostics across complex fiber networks. In addition, the use of AI based fault detection is improving the accuracy of identifying network anomalies, helping operators respond faster to potential disruptions. The move toward high capacity optical networks is also driving demand for more precise and continuous channel monitoring capabilities.

Growth Factors

The growth of this market is driven by the increasing demand for high speed data transmission and reliable communication networks. As data traffic continues to rise due to cloud services, streaming, and enterprise connectivity, maintaining signal quality across optical networks has become critical. The expansion of fiber infrastructure across urban and rural areas is also supporting the need for effective monitoring solutions.

Another major factor is the growing complexity of optical networks, where multiple channels operate simultaneously and require accurate performance tracking to avoid service disruptions. Network operators are also focusing on reducing downtime and maintenance costs, which is encouraging the adoption of automated monitoring tools. Furthermore, the shift toward next generation communication technologies is increasing the need for advanced monitoring systems that can handle higher bandwidth and ensure consistent network performance across long distance transmissions.

Key Market Segments

By Product Type

- Embedded OCM

- Portable OCM

By Application

- Dense Wavelength Division Multiplexing (DWDM) Networks

- Coarse Wavelength Division Multiplexing (CWDM) Networks

- Optical Transport Networks (OTN)

- Fiber Monitoring

By End-User

- Telecommunications

- Data Centers

- IT & Networking

- Healthcare

- Government & Defense

- Others

Regional Analysis

Asia Pacific accounted for 38.3% of the Optical Channel Monitor market, reflecting strong expansion of fiber optic networks and rising demand for high-capacity data transmission. The region is witnessing continuous growth in telecom infrastructure, supported by increasing internet penetration, data traffic, and deployment of high-speed communication networks.

Optical channel monitors are gaining importance as network operators focus on maintaining signal quality, minimizing downtime, and ensuring efficient bandwidth utilization. Rapid rollout of advanced network technologies and growing investments in data centers have further strengthened the demand for monitoring solutions across the region.

China market reached USD 111.4 Million and is projected to grow at a CAGR of 4.2%, driven by large-scale fiber network deployments and ongoing upgrades in communication infrastructure. The country’s focus on expanding high-speed broadband and supporting data-intensive applications is encouraging telecom operators to adopt advanced optical monitoring systems.

In addition, increasing emphasis on network reliability and performance optimization is supporting steady demand for these solutions. As digital connectivity continues to expand across industries, the adoption of optical channel monitoring technologies in China is expected to remain consistent over the coming years.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherlands

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Thailand

- Vietnam

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Competitive Analysis

The competitive landscape of the Optical Channel Monitor Market is driven by a mix of established test and measurement companies and optical component manufacturers. Companies such as EXFO Inc., Viavi Solutions Inc., Yokogawa Electric Corporation, Keysight Technologies, and Anritsu Corporation focus on advanced optical testing and monitoring solutions for telecom networks.

These players emphasize high accuracy, real-time performance monitoring, and support for high-speed fiber networks. Their strong presence in network testing and measurement allows them to serve telecom operators and data center providers effectively, especially as demand for reliable and high-capacity optical networks continues to grow.

At the same time, optical component and subsystem providers such as Finisar Corporation (now part of II-VI Incorporated), NeoPhotonics Corporation, Lumentum Holdings Inc., Santec Corporation, Optoplex Corporation, and DiCon Fiberoptics compete by offering integrated optical monitoring modules and wavelength management solutions.

Companies like Lambda Quest, Enablence, Axsun, and Lightwaves2020 focus on specialized and niche applications, providing compact and cost-effective solutions for specific use cases. Overall, competition in this market is driven by innovation in optical sensing accuracy, integration with network management systems, and the ability to support next-generation high-speed optical communication networks.

Top Key Players in the Market

- EXFO Inc.

- Viavi Solutions Inc.

- Yokogawa Electric Corporation

- Finisar Corporation (now part of II-VI Incorporated)

- Keysight Technologies

- NeoPhotonics Corporation

- Optoplex Corporation

- Santec Corporation

- Lumentum Holdings Inc.

- Anritsu Corporation

- Lightwaves2020

- DiCon Fiberoptics

- II-VI Incorporated

- Lambda Quest

- Enablence

- Axsun

- Others

Future Outlook

The future outlook for the Optical Channel Monitor Market looks positive as demand for high-speed and reliable optical networks continues to grow. The market is expected to benefit from the expansion of data centers, increasing internet traffic, and the rollout of advanced communication technologies. Optical channel monitors are anticipated to become more important for real-time network monitoring, helping operators detect signal issues quickly and maintain performance. In the coming years, integration with automation and AI-based network management is expected to improve efficiency and reduce downtime, making these solutions a key part of modern optical communication systems.

Recent Developments

- March, 2026 – VIAVI ONELabPro validates 1.6T Ethernet at OFC with DCX-700 24-fiber tester. INX 700 microscopes inspect OSFP connectors and AI fabric test suite launches. Hyperscale data center focus with automated pass/fail.

- February, 2026 – Yokogawa AQ6380 upgrades to 160-channel C+L monitoring. Coherent optics resolution and field-service optimized design. Japan NTT deployments with battery operation for remote sites.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 947.5 Million |

| Forecast Revenue (2035) | USD 2,202.3 Million |

| CAGR(2025-2035) | 8.80% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue forecast, AI impact on Market trends, Share Insights, Company ranking, competitive landscape, Recent Developments, Market Dynamics and Emerging Trends |

| Segments Covered | By Product Type (Embedded OCM, Portable OCM), By Application (Dense Wavelength Division Multiplexing (DWDM) Networks, Coarse Wavelength Division Multiplexing (CWDM) Networks, Optical Transport Networks (OTN), Fiber Monitoring), By End-User (Telecommunications, Data Centers, IT & Networking, Healthcare, Government & Defense, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Latin America; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | EXFO Inc., Viavi Solutions Inc., Yokogawa Electric Corporation, Finisar Corporation (now part of II-VI Incorporated), Keysight Technologies, NeoPhotonics Corporation, Optoplex Corporation, Santec Corporation, Lumentum Holdings Inc., Anritsu Corporation, Lightwaves2020, DiCon Fiberoptics, II-VI Incorporated, Lambda Quest, Enablence, Axsun, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three license to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |