Quick Navigation

Report Overview

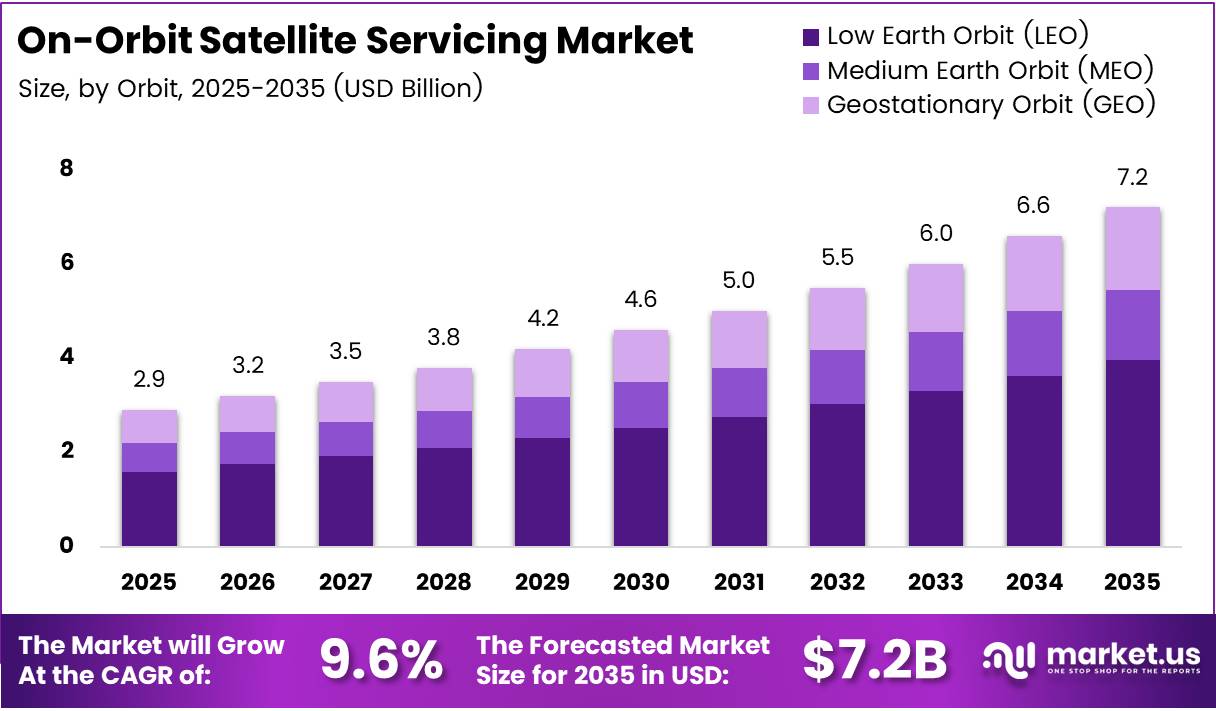

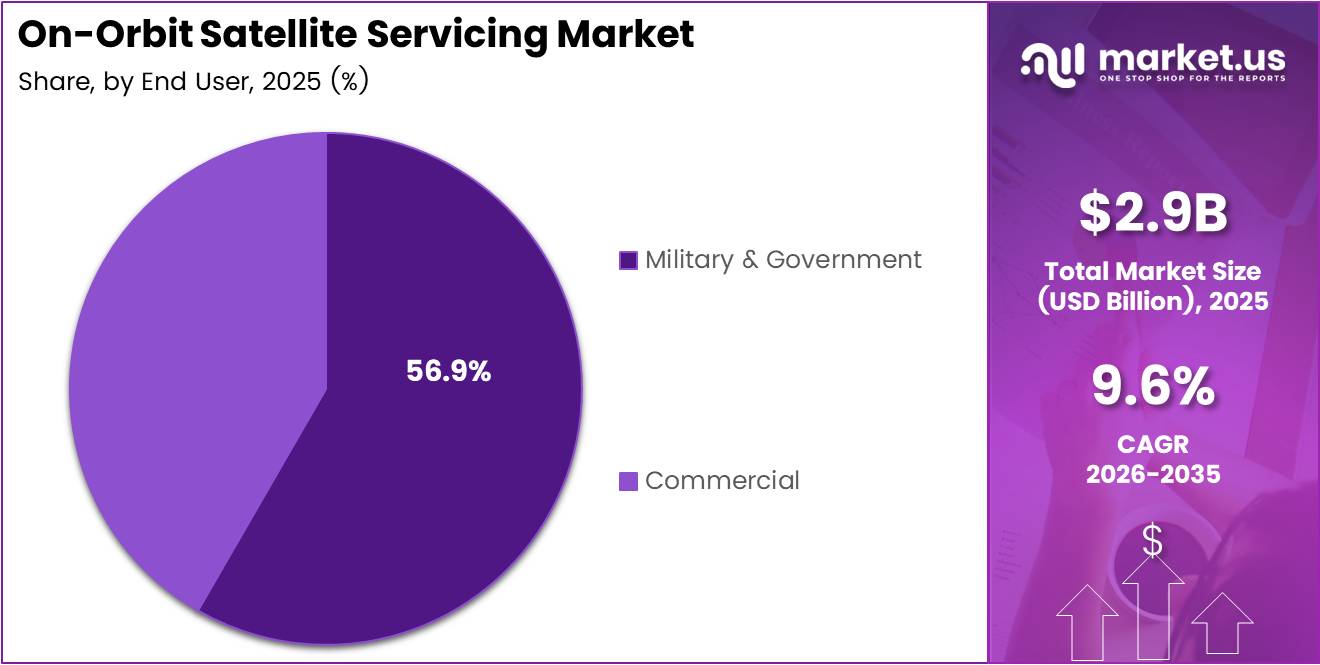

Global On-Orbit Satellite Servicing Market size is expected to be worth around USD 7.2 Billion by 2035 from USD 2.9 Billion in 2025, growing at a CAGR of 9.6% during the forecast period 2026 to 2035.

On-orbit satellite servicing covers a range of in-space operations — including life extension, refueling, active debris removal, robotic repair, and in-orbit assembly. These services address a structural gap in how satellite operators currently manage aging assets, replacing costly full-satellite replacements with targeted on-orbit interventions.

The economics of servicing are compelling. A GEO communications satellite costs $300–500 million to build and launch, yet retires solely due to propellant depletion — not hardware failure. A servicing mission priced at $50–100 million can extend that asset’s revenue-generating life by 5 years, during which it earns $20–30 million annually in transponder revenue. This cost structure makes on-orbit servicing one of the highest-ROI decisions a satellite operator can make.

Military and government buyers currently anchor demand, holding 56.9% of the end-user segment. Defense agencies treat satellite servicing as a strategic capability, not merely a cost-reduction tool. Consequently, government procurement timelines and budget cycles shape near-term market expansion more than commercial adoption rates.

Low Earth Orbit operations dominate by orbit type, reflecting the density of recently deployed constellations. Large satellites above 1,000 kg hold 52.7% of the By Type segment, since these high-value assets justify the cost of dedicated servicing missions. This concentration signals that service providers targeting GEO operators and large LEO constellation managers hold the highest near-term revenue potential.

According to Pixalytics, approximately 14,904 individual satellites orbited Earth as of early 2025 — a 31.54% increase since June 2023. This expansion directly widens the addressable client base for on-orbit servicing providers, as each additional active satellite represents a potential future servicing contract, particularly as propellant reserves deplete.

According to Our World in Data, a record 4,510 objects launched into space in 2025, with US entities responsible for 82% of the global total. This launch volume compounds the orbital congestion problem and validates long-term demand for debris removal and collision-avoidance services. In April 2025, Northrop Grumman’s MEV-1 completed the world’s first commercial 5-year satellite life-extension mission for Intelsat 901, establishing a proven commercial precedent for the market.

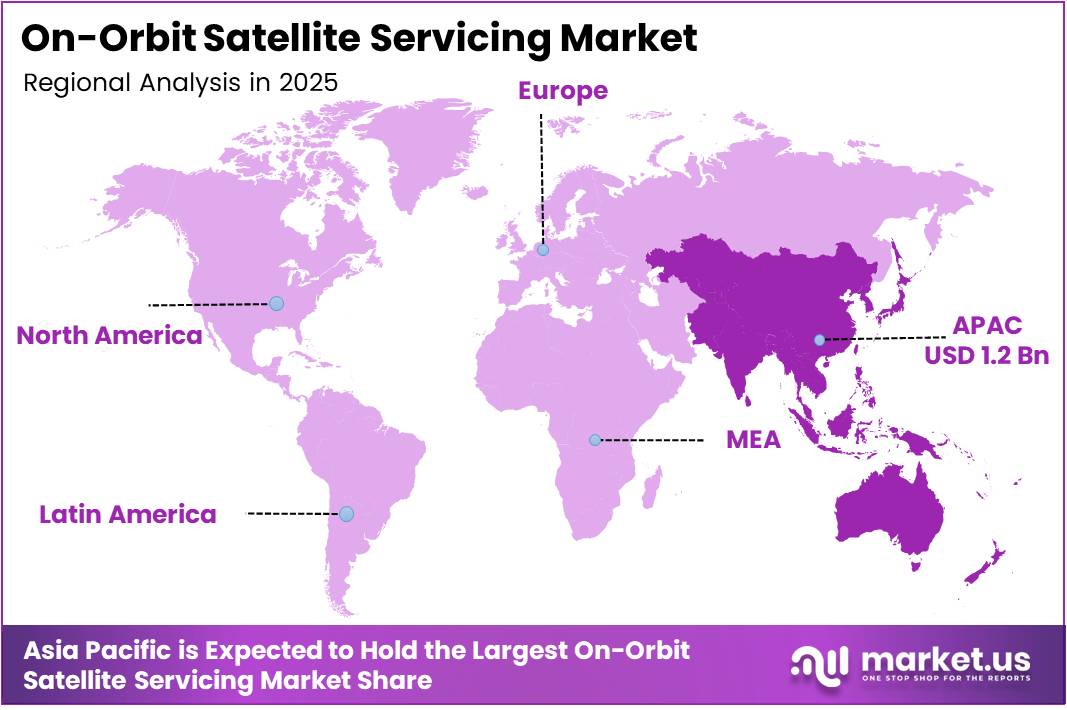

Asia Pacific leads all regions with a 44.4% share, valued at USD 1.2 billion, driven by significant government-backed space programs across China, Japan, and India. The regional dominance reflects state investment in both indigenous servicing technology and space sustainability infrastructure — conditions that attract private operators seeking government anchor contracts to validate new servicing platforms.

Key Takeaways

- The global On-Orbit Satellite Servicing Market was valued at USD 2.9 Billion in 2025 and is forecast to reach USD 7.2 Billion by 2035, at a CAGR of 9.6%.

- By Type, Large Satellites (>1,000 kg) lead with a 52.7% share, as high-asset-value satellites justify dedicated servicing mission costs.

- By Service, Active Debris Removal and Orbit Adjustment holds the dominant share at 32.5%, reflecting government-led mandates for orbital sustainability.

- By Orbit, Low Earth Orbit accounts for 52.8% of the market, driven by the concentration of recently deployed commercial and defense constellations.

- By End User, Military and Government commands 56.9% of demand, with defense agencies treating servicing as a strategic operational priority.

- Asia Pacific dominates regionally with a 44.4% market share, valued at USD 1.2 Billion, underpinned by state-funded space programs across China, India, and Japan.

- Approximately 14,904 satellites orbited Earth as of early 2025 — a 31.54% increase since June 2023 — sharply expanding the addressable client pool for servicing providers.

- A record 4,510 objects entered orbit in 2025, with US entities responsible for 82% of global launches, intensifying orbital congestion and debris removal requirements.

Type Analysis

Large Satellites (>1,000 kg) dominate with 52.7% due to high asset replacement cost justifying servicing.

In 2025, Large Satellites (>1,000 kg) held a dominant market position in the By Type segment of the On-Orbit Satellite Servicing Market, with a 52.7% share. These assets — primarily GEO communications and government defense satellites — carry replacement costs of $300–500 million, making even a $50–100 million servicing mission financially rational. Operators prioritize servicing large satellites because the economics are unambiguous.

Small Satellites (<500 kg) represent the fastest-emerging servicing opportunity, driven by the mass deployment of LEO constellations from commercial operators. However, current servicer economics — particularly the high cost of matching orbital planes — make dedicated small satellite servicing missions commercially marginal today. Providers are actively developing scalable, multi-client servicing architectures to address this cost barrier.

Medium Satellites (501–1,000 kg) occupy a transitional position in the servicing market. These platforms are common in government reconnaissance and scientific missions, where extended operational life carries strategic value beyond pure financial ROI. As servicing technology matures, medium satellite operators represent a natural next wave of commercial adoption after large satellite servicing achieves full commercial viability.

Service Analysis

Active Debris Removal (ADR) and Orbit Adjustment dominates with 32.5% due to government-mandated orbital sustainability requirements.

In 2025, Active Debris Removal (ADR) and Orbit Adjustment held a dominant market position in the By Service segment of the On-Orbit Satellite Servicing Market, with a 32.5% share. Government space agencies in Europe, Japan, the US, and the UK have moved from voluntary debris mitigation guidelines to funded demonstration programs, converting ADR from a research concept into a procured service with contract-backed revenue. This regulatory shift is what separates ADR from the other service categories in near-term commercial viability.

Robotic Servicing carries the highest technology complexity within the service categories and is increasingly funded through defense-aligned programs. Northrop Grumman’s Mission Robotic Vehicle, equipped with dual robotic arms and multi-sensor inspection capability, reflects how robotic servicing is evolving from single-mission tools into reusable, multi-client platforms — a structural shift that improves unit economics for providers over time.

Refueling services represent the single largest long-term revenue opportunity in the segment. Astroscale forecasts 20–30 large GEO-orbit satellites will retire per year due to propellant depletion — and China’s Shijian-25 conducted the world’s first satellite-to-satellite in-orbit refueling in GEO orbit in January 2025, transferring approximately 142 kg of hydrazine to extend Shijian-21’s operational life by approximately 8 years. This milestone confirms that GEO refueling is technically achievable, shifting the constraint from feasibility to commercial scale.

Assembly services remain the earliest-stage category, with most activity concentrated in government-funded research programs and modular satellite architecture development. However, the emergence of commercial space station development programs creates a concrete future demand pathway — operators building stations in orbit will require on-orbit assembly capabilities as a core operational service, not an experimental add-on.

Orbit Analysis

Low Earth Orbit (LEO) dominates with 52.8% due to concentrated commercial constellation deployment activity.

In 2025, Low Earth Orbit (LEO) held a dominant market position in the By Orbit segment of the On-Orbit Satellite Servicing Market, with a 52.8% share. The density of recently deployed commercial and government constellations at LEO altitudes creates the most immediate collision-avoidance and maintenance requirements of any orbit. As constellation operators scale to thousands of satellites, the operational cost of unserviced asset failures grows proportionally — making LEO servicing a volume-driven market.

Medium Earth Orbit (MEO) serves as home to navigation constellation assets — GPS, Galileo, GLONASS — where servicing demand is driven by government operators prioritizing continuity of positioning infrastructure. MEO servicing remains nascent commercially but carries strategic importance, as any disruption to navigation constellations carries economic consequences that far exceed the cost of preventive servicing missions.

Geostationary Orbit (GEO) hosts the highest-value individual satellite assets and represents the most commercially mature servicing segment today. The GEO belt carries approximately 550 operational commercial satellites — most operating on propellant budgets designed for 15–18 years of stationkeeping — making predictable retirement schedules visible to servicing providers years in advance. This forward visibility is a structural advantage for GEO-focused providers building pipeline revenue.

End-User Analysis

Military and Government dominates with 56.9% due to strategic satellite dependency and defense budget access.

In 2025, Military and Government held a dominant market position in the By End User segment of the On-Orbit Satellite Servicing Market, with a 56.9% share. Defense agencies operate satellites that are irreplaceable in short timeframes — particularly reconnaissance, communications, and navigation assets — making servicing a capability investment rather than a cost-reduction measure. US Department of Defense commitments, including four funded demonstration missions planned for 2026, confirm that government procurement sustains the early commercial market for on-orbit servicing providers.

Commercial end users represent the growth frontier for on-orbit satellite servicing, driven by the financial logic of life extension over replacement. As servicing providers accumulate mission heritage and demonstrated success rates, commercial satellite operators face a clearer procurement decision: pay for servicing or accept earlier asset retirement. The commercial segment’s expansion depends directly on the rate at which government-funded missions produce transferable technical proof points that lower perceived risk for private buyers.

Key Market Segments

By Type

- Small Satellites (<500 Kg)

- Medium Satellites (501–1000 Kg)

- Large Satellites (>1000 Kg)

By Service

- Active Debris Removal (ADR) and Orbit Adjustment

- Robotic Servicing

- Refueling

- Assembly

By Orbit

- Low Earth Orbit (LEO)

- Medium Earth Orbit (MEO)

- Geostationary Orbit (GEO)

By End User

- Military & Government

- Commercial

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East & Africa

Drivers

Orbital Congestion and Asset Replacement Economics Force On-Orbit Servicing Into Mainstream Space Operations

Satellite operators face a structural dilemma: LEO constellations now number in the thousands, orbital slots carry increasing collision risk, and replacing failed or fuel-depleted assets costs hundreds of millions of dollars per satellite. According to ESA’s Space Environment Report 2025, approximately 40,000 objects are tracked by space surveillance networks, with debris objects larger than 1 cm — sufficient to cause catastrophic satellite damage — estimated to exceed 1.2 million. This scale of orbital hazard converts on-orbit servicing from optional to operationally necessary.

The cost of satellite replacement directly drives life-extension demand. A GEO communications satellite costs $300–500 million to replace, while a servicing mission extends its life at $50–100 million. This 3x–5x cost advantage, combined with the satellite generating $20–30 million per year in transponder revenue, means operators lose significant revenue by retiring satellites prematurely. Consequently, servicing providers with demonstrated life-extension capability hold a clear commercial argument against every operator approaching asset end-of-life.

Advancements in robotic and autonomous systems amplify the market by making complex servicing missions technically executable at scale. India’s AayulSAT — the country’s first on-orbit refueling demonstrator — launched aboard ISRO’s PSLV-C62 on January 12, 2026, testing propane-based propellant transfer and satellite docking protocols. Each national program that validates a core servicing technology adds to the global pool of demonstrated capabilities, reducing the technical uncertainty that commercial buyers cite as a procurement barrier.

Restraints

High Mission Costs, Technical Complexity, and Regulatory Gaps Constrain Commercial Market Scale

On-orbit satellite servicing missions carry cost structures that remain prohibitive for most commercial operators outside the GEO life-extension use case. A 2025 peer-reviewed study in the AIAA Journal of Spacecraft and Rockets found that projected fuel mass ratios for servicer vehicles range from 46–54% of total servicer mass, with average delivered fuel costs of $277,000–$290,000 per kilogram. These economics restrict commercially viable refueling to high-value, large satellites — limiting addressable market size in the near term.

Technical complexity extends beyond cost. The COSMIC GEO Refueling Use Case report, published November 2025, assessed that most fluid transfer and propellant management technologies remain at Technology Readiness Level 2–7, with the majority still requiring dedicated in-space demonstration flights before reaching operational readiness. This gap between laboratory-validated technology and flight-proven systems creates multi-year delays between investment and revenue generation — a timing risk that suppresses private capital commitment.

Regulatory and liability frameworks for on-orbit servicing remain unresolved across most jurisdictions. No international standard governs liability when a servicer vehicle causes damage to a client satellite or third-party asset during proximity operations. This legal ambiguity raises insurance costs, complicates contract negotiation between operators and service providers, and creates political barriers to servicing missions that cross national satellite asset boundaries — a structural friction that slows procurement decisions across both commercial and government buyer segments.

Growth Factors

Government Defense Investment, Commercial Space Infrastructure, and Modular Satellite Design Open New Servicing Revenue Streams

Government defense agencies are converting on-orbit servicing from a research priority into a funded operational requirement. Four separate on-orbit satellite servicing demonstration missions — funded by different US Department of Defense entities and each involving commercial partners — are planned for launch in 2026, targeting in-orbit refueling, repair, inspection, and maneuvering capabilities for military satellites. This concentration of government-funded missions in a single year signals that defense procurement of commercial servicing is transitioning from pilot phase to program baseline.

The GEO belt holds approximately 550 operational commercial satellites, most dependent on chemical propulsion for stationkeeping and carrying propellant budgets designed for 15–18 years of service life. As these satellites approach retirement windows, satellite operators face a predictable and quantifiable demand for life-extension services. This forward visibility allows servicing providers to build contractual pipeline years in advance — a structural advantage that distinguishes GEO servicing from other space market segments where demand is less predictable.

Modular satellite architectures and commercial space station development create a new category of in-orbit servicing demand beyond life extension. As constellation operators design satellites with upgradeable payloads and replaceable subsystems, on-orbit assembly services become operationally necessary rather than experimental. Providers that develop both robotic manipulation and fluid transfer capabilities simultaneously position themselves for a broader service portfolio — capturing revenue from refueling, repair, and assembly across multiple client segments rather than competing on life extension alone.

Emerging Trends

Autonomous Rendezvous Technology and Space-as-a-Service Models Reshape Competitive Dynamics in On-Orbit Servicing

Autonomous Rendezvous, Proximity Operations, and Docking (RPOD) capability is becoming the defining technical differentiator in on-orbit satellite servicing. Starfish Space’s Otter Pup 2 mission, launched June 23, 2025 aboard SpaceX Transporter-14, demonstrated fully autonomous docking with an unprepared, unmodified client satellite in LEO — the first commercial attempt at this capability. This milestone matters because unmodified docking dramatically expands the serviceable satellite population, removing the requirement for future satellites to carry standardized docking interfaces as a prerequisite for servicing.

Space-as-a-Service business models are restructuring how satellite operators pay for on-orbit capabilities. Rather than purchasing a servicer vehicle outright, operators increasingly contract for specific mission outcomes — a defined number of life-extension years, a set debris removal target, or a guaranteed number of refueling transfers. According to the Innovation News Network, in the first weeks of 2026, 1,500 Conjunction Data Messages were published by space surveillance providers, with over 80% involving LEO objects. This volume of collision-avoidance activity converts servicing from a discretionary purchase into a recurring operational need — the precondition for subscription-based servicing contracts.

Private sector participation in space infrastructure is accelerating through strategic partnerships between established aerospace companies and mission-specialized startups. The COSMIC consortium — established by NASA to advance In-Space Servicing, Assembly, and Manufacturing capabilities — grew to more than 1,200 members from 306 organizations by August 2025. This collaborative model pools technical expertise and shared development costs across companies that would otherwise compete — a structure that speeds technology maturation without requiring any single firm to fund the full development cycle independently.

Regional Analysis

Asia Pacific Dominates the On-Orbit Satellite Servicing Market with a Market Share of 44.4%, Valued at USD 1.2 Billion

Asia Pacific commands 44.4% of the global On-Orbit Satellite Servicing Market, valued at USD 1.2 billion in 2025. China’s Shijian-25 refueling mission, Japan’s JAXA-backed debris removal programs, and India’s AayulSAT refueling demonstrator collectively represent state-directed investment in indigenous servicing capability. These programs signal that Asian governments treat on-orbit servicing as a sovereign infrastructure priority — not merely a commercial opportunity — which sustains funding independent of private market cycles.

North America On-Orbit Satellite Servicing Market Trends

North America holds the most commercially mature on-orbit servicing market globally, anchored by US Department of Defense procurement and private operator demand from large GEO satellite fleets. The US Space Force’s funded demonstration pipeline for 2026, combined with established commercial providers operating MEV-class vehicles, gives North American providers first-mover heritage that translates directly into contract incumbency advantages as the market scales.

Europe On-Orbit Satellite Servicing Market Trends

Europe’s on-orbit servicing market is shaped by ESA-funded active debris removal initiatives and regulatory pressure from EU space sustainability frameworks. Programs like ClearSpace’s CLEAR mission — the first multi-object ADR mission funded by the UK Space Agency — represent Europe’s strategy of using government contracts to de-risk commercial servicing technology. This approach creates viable early-revenue pathways for European startups without requiring immediate commercial-scale demand.

Latin America On-Orbit Satellite Servicing Market Trends

Latin America contributes a smaller but developing share of global on-orbit servicing activity, primarily through satellite operations managed by government agencies in Brazil and Mexico. Regional participation is concentrated on the end-user side — as operators of GEO communications satellites — rather than as service providers. As life-extension servicing economics become established globally, Latin American satellite operators represent a natural future buyer segment for GEO servicing contracts.

Middle East and Africa On-Orbit Satellite Servicing Market Trends

Middle East and Africa markets participate in on-orbit servicing primarily as satellite asset operators, with GCC governments running sovereign GEO communications and observation satellite fleets. UAE and Saudi Arabia space agency programs are expanding satellite portfolios, which progressively creates domestic demand for servicing contracts. The region’s trajectory follows the pattern of other government-led satellite markets — operator scale precedes servicing procurement by several years.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

Airbus SE positions itself as a full-spectrum satellite servicing provider, targeting both commercial and governmental operators through its dedicated servicing platform unveiled in August 2024. Airbus’s strategic advantage lies in combining satellite manufacturing heritage with servicing capability — allowing it to offer operators integrated life-cycle contracts that bundle original equipment supply with long-term maintenance, creating switching costs that reinforce long-term client retention in a market where repeat servicing relationships carry high value.

Altius Space Machines differentiates through capture mechanism technology designed for non-cooperative satellites — assets without built-in docking hardware. This technical focus addresses the largest segment of the existing satellite population, which was designed before standardized servicing interfaces existed. By solving the non-cooperative docking problem, Altius positions itself as a foundational technology supplier to larger servicing platforms rather than competing as an end-to-end mission operator — a lower-capital, higher-leverage market entry strategy.

Astroscale Holdings Inc. has built its market position around active debris removal and life-extension servicing for GEO operators, targeting the predictable retirement pipeline of 20–30 large GEO satellites per year. The company’s LEXI-P mission is designed to validate life-extension technology at commercial scale, with Astroscale targeting 1–2 life-extension contracts per year post-demonstration. This measured commercialization path reflects a strategy of building mission heritage before scaling contract volume — the credibility sequencing that government and institutional buyers require.

Atomos Space was acquired by Katalyst Space Technologies in April 2025, accelerating the combined entity’s in-space servicing capabilities for commercial and defense markets. This acquisition reflects a broader consolidation dynamic: well-capitalized players are absorbing specialized technology developers before the demonstration-to-deployment transition, securing proprietary IP and engineering talent at pre-revenue valuations. For buyers, consolidation reduces the number of credible servicing providers — concentrating procurement decisions around fewer, more capable platforms.

Key Players

- Airbus SE

- Altius Space Machines, Inc.

- Astroscale Holdings Inc.

- Atomos Space

- ClearSpace

- Future Space Industries

- High Earth Orbit Robotics

- Hyoristic Innovations

- Infinite Orbits

- Lúnasa Ltd.

- Maxar Technologies

Recent Developments

- February 2026 — Starfish Space was awarded a $54.5 million contract from the US Space Force’s Space Systems Command via the APFIT program to deliver a dedicated Otter satellite servicing vehicle for dynamic space operations in GEO, scheduled for delivery in 2028. This followed an earlier $37.5 million Space Force contract for a 2026 logistics servicing demonstration.

- April 2026 — Starfish Space raised over $100 million in Series B funding led by Point72 Ventures, with co-leads Activate Capital and Shield Capital. The round positions Starfish Space to accelerate development of its Otter servicing vehicle platform and scale commercial and defense mission capacity ahead of its 2026 demonstration target.

- November 2025 — Infinite Orbits secured €40 million in an oversubscribed financing round led by the European Innovation Council Fund, alongside Matterwave Ventures, Wind Capital, Balnord, IRDI, and Newfund Capital. The funding supports Infinite Orbits’ satellite life-extension service commercialization targeting the GEO operator segment.

- July 2025 — Orbit Fab won an ESA contract worth €750,000 and unveiled an in-orbit test of a new refueling port, advancing the standardization of satellite refueling interfaces. A common refueling port standard accelerates commercial adoption by removing the need for bespoke servicer-client hardware integration on each mission.

- June 2025 — Northrop Grumman’s Mission Robotic Vehicle integrated a robotics payload from the US Naval Research Laboratory as part of DARPA’s Robotic Servicing of Geosynchronous Satellites (RSGS) program. The MRV, equipped with 2 robotic arms, 2 visible cameras, 2 infrared cameras, and 2 LIDAR sensors, targets a GEO launch in 2026 with 3 client satellite servicing missions already booked.

- August 2024 — Airbus unveiled a new satellite servicing platform aimed at comprehensive maintenance solutions for commercial and governmental satellites. The platform launch signals Airbus’s intent to compete across the full servicing value chain — not merely as a technology supplier — expanding competitive pressure in a market previously concentrated among specialized servicing startups.

- August 2024 — Lockheed Martin acquired Terran Orbital for $450 million, adding small satellite manufacturing capability to its space portfolio. While primarily a manufacturing acquisition, the transaction reflects prime contractor appetite for vertical integration across the satellite lifecycle — a strategic precondition for competing in bundled manufacture-and-service contracts as the on-orbit servicing market matures.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 2.9 Billion |

| Forecast Revenue (2035) | USD 7.2 Billion |

| CAGR (2026-2035) | 9.6% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Type (Small Satellites <500 Kg, Medium Satellites 501–1000 Kg, Large Satellites >1000 Kg), By Service (Active Debris Removal and Orbit Adjustment, Robotic Servicing, Refueling, Assembly), By Orbit (Low Earth Orbit, Medium Earth Orbit, Geostationary Orbit), By End User (Military & Government, Commercial) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | Airbus SE, Altius Space Machines Inc., Astroscale Holdings Inc., Atomos Space, ClearSpace, Future Space Industries, High Earth Orbit Robotics, Hyoristic Innovations, Infinite Orbits, Lúnasa Ltd., Maxar Technologies |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |