Global NWDAF Integration Services Market Size, Share, Growth Analysis By Service Type (Consulting, Implementation, Support & Maintenance, Others), By Deployment Mode (On-Premises, Cloud-Based, Hybrid), By Application (Network Optimization, Network Security, Quality of Service, Management, Traffic Analytics, Others), By End-User (Telecom Operators, Enterprises, Managed Service Providers, Others), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2025-2035

- Published date: Mar 2026

- Report ID: 182485

- Number of Pages: 362

- Format:

-

keyboard_arrow_up

Quick Navigation

- Report Overview

- Core Key Insights

- Market Outlook

- Future Predictions

- Key Market Segments

- Research-Based Segments

- By Service Type

- By Deployment Mode

- By Application

- By End-User

- Regional Analysis

- US Market Size

- Driving Factors

- Restraint Factors

- Growth Opportunities

- Trending Factors

- Competitive Analysis

- Recent Developments

- Report Scope

Report Overview

The NWDAF Integration Services Market is emerging as a critical segment within the telecom analytics ecosystem, driven by the increasing adoption of intelligent network functions and data-driven decision-making.

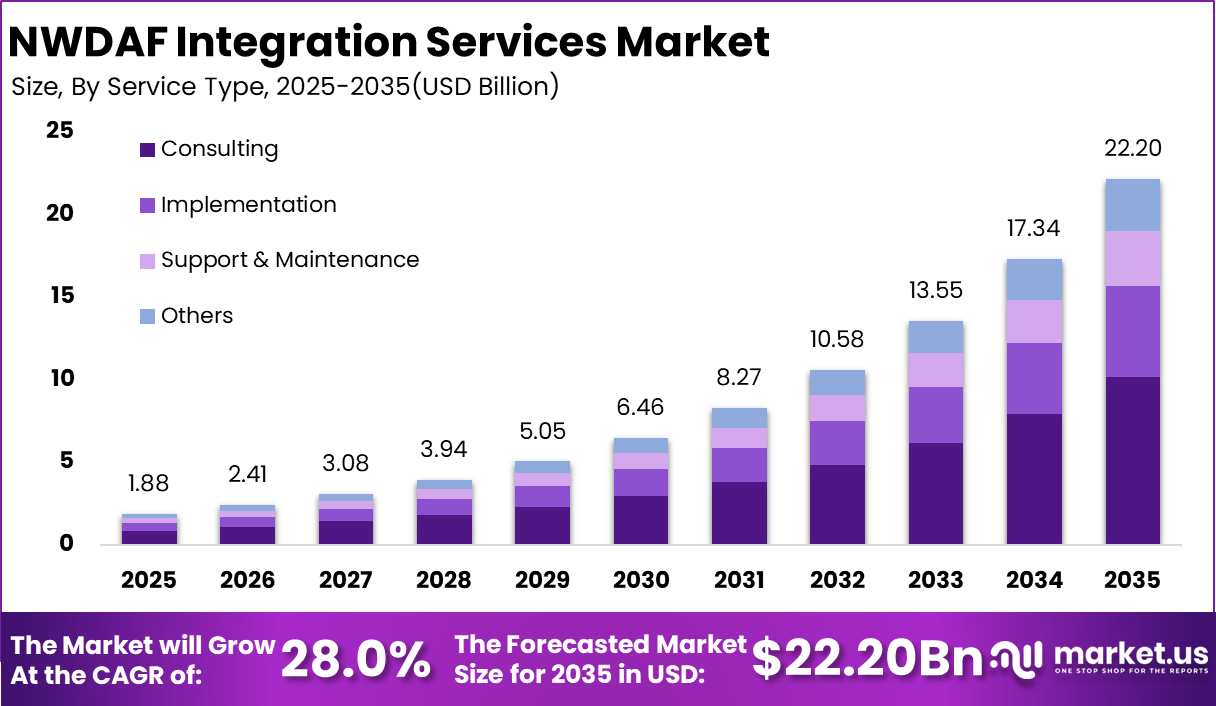

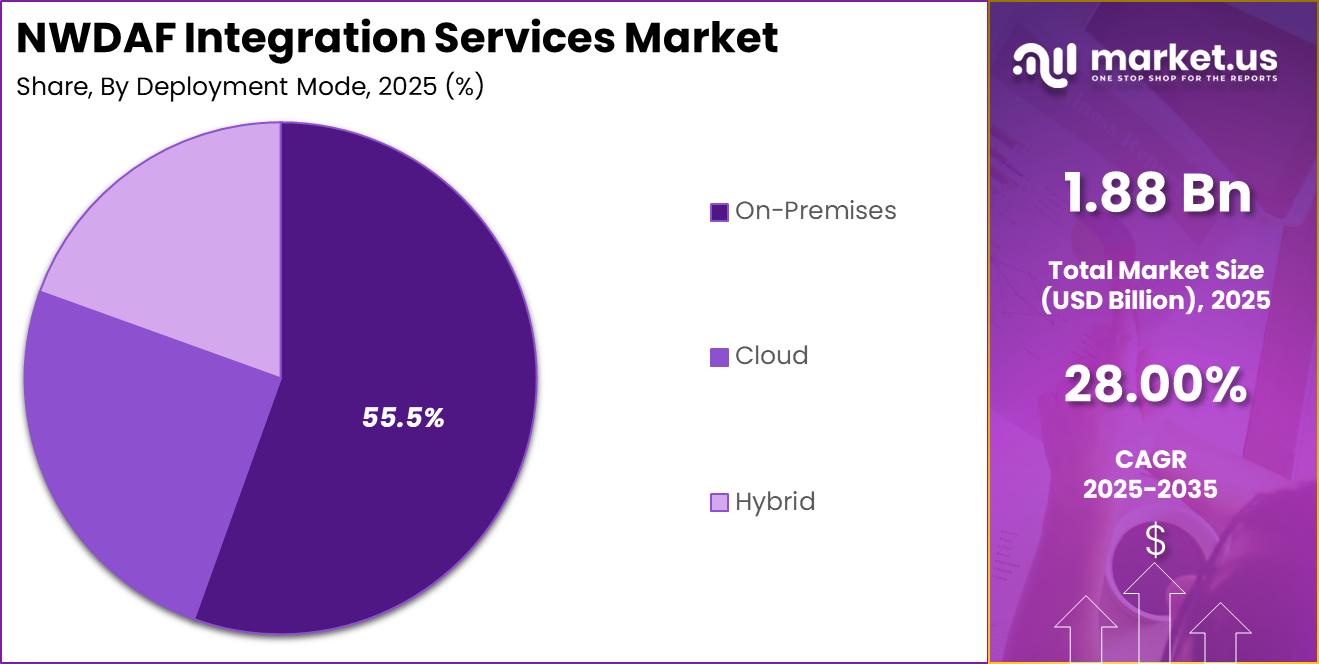

In 2025, the market is valued at USD 1.88 billion and is projected to reach USD 22.20 billion by 2035, reflecting a strong CAGR of 28%. This rapid growth highlights the rising importance of integrating Network Data Analytics Function capabilities into telecom networks to enable real-time insights, automation, and improved service quality.

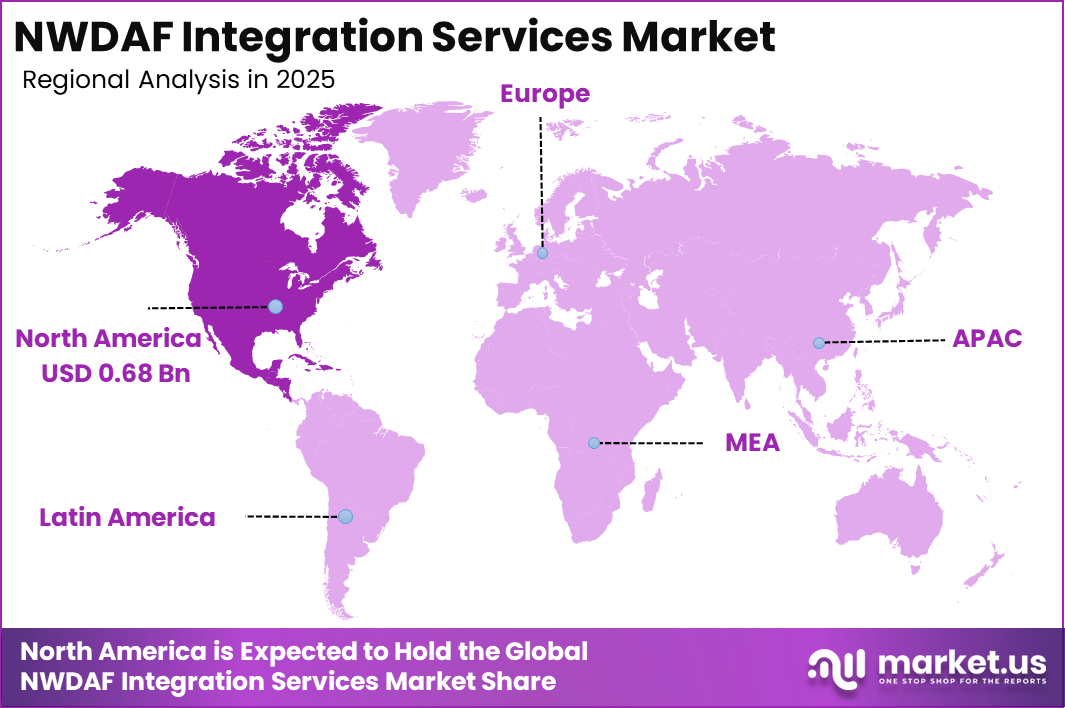

From a regional standpoint, North America leads with a 36.2% share, accounting for USD 0.68 billion in 2025. The region benefits from early deployment of advanced telecom technologies, including 5G standalone networks and cloud-native architectures, which require seamless integration of analytics-driven functions.

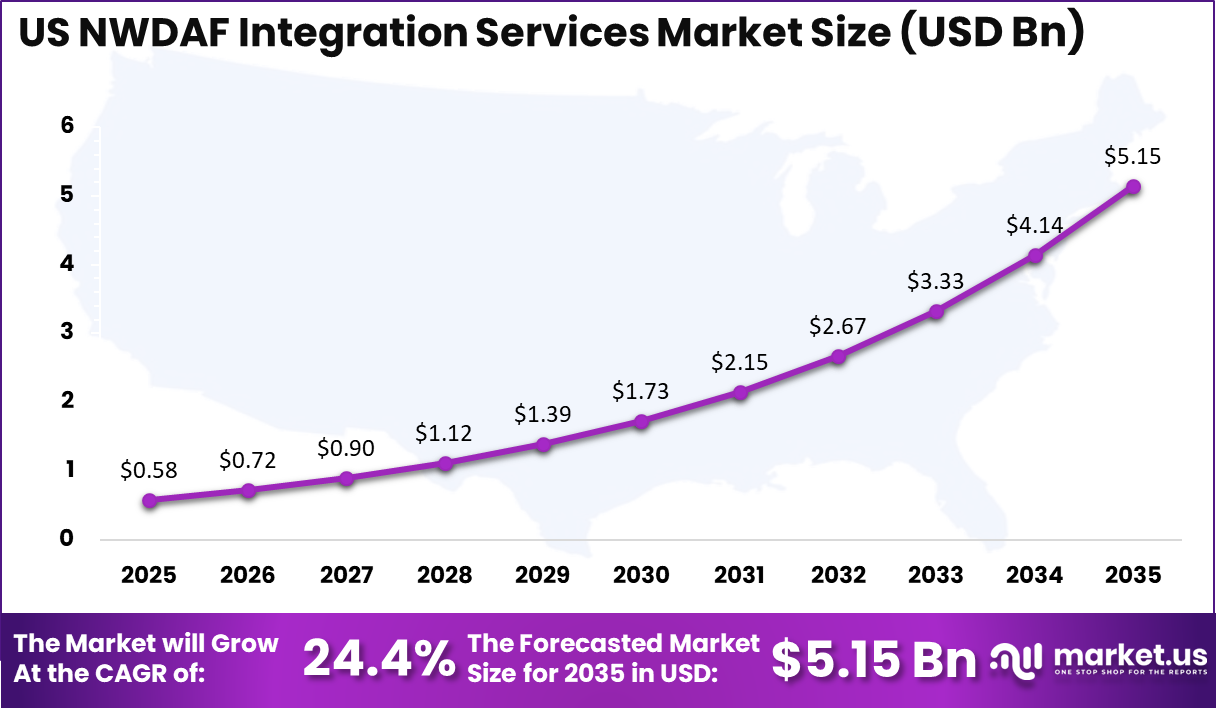

Within this region, the US plays a dominant role, with a market size of USD 0.58 billion in 2025 and projected to reach USD 5.15 billion by 2035, growing at a CAGR of 24.4%. This growth is supported by strong investments in telecom infrastructure, increasing demand for automated network management, and the need to handle complex, data-intensive network environments efficiently.

The growth of the NWDAF Integration Services Market is closely linked to the rapid expansion of 5G standalone networks and data-driven telecom operations. According to 3GPP, NWDAF is a core component of 5G architecture, enabling real-time analytics across network functions. Global 5G subscriptions surpassed 1.7 billion in 2024, and are expected to exceed 5 billion by the end of the decade, significantly increasing the need for integrated analytics capabilities within telecom networks.

Network data volumes are also rising sharply. Ericsson reports that mobile data traffic crossed 150 exabytes per month in 2024 and is projected to grow at around 20% annually. This surge in traffic requires advanced analytics frameworks like NWDAF to process, interpret, and optimize network performance in real time.

Additionally, GSMA highlights that over 240 commercial 5G networks have already been deployed worldwide, many of which are transitioning toward standalone architectures that rely heavily on analytics integration.

Cloud adoption is another key factor, with International Data Corporation indicating that more than 70% of telecom operators are investing in cloud-native network functions. This shift is increasing demand for integration services that can connect analytics platforms with distributed network environments, enabling automation, predictive insights, and improved service delivery.

Core Key Insights

- Global market size in 2025: USD 1.88 billion, projected to reach USD 22.20 billion by 2035, indicating strong expansion potential.

- Overall growth rate: 28% CAGR, reflecting rapid adoption of analytics-driven network integration.

- North America: 36.2% share, valued at USD 0.68 billion in 2025, showing regional leadership in advanced telecom integration.

- US market: USD 0.58 billion in 2025, projected to reach USD 5.15 billion by 2035, growing at 24.4% CAGR.

- By service type: Consulting: 45.7%, highlighting strong demand for expert guidance in NWDAF integration and deployment strategies.

- By deployment mode: On-premises: 55.5%, reflecting preference for control, security, and compatibility with existing telecom infrastructure.

- By application: Network optimization: 38.7%, driven by the need for real-time analytics and improved network efficiency.

- By end-user: Telecom operators: 52.6%, indicating their dominant role in adopting NWDAF integration services for advanced network management.

Market Outlook

The outlook for the NWDAF Integration Services Market is strongly shaped by the rapid evolution of 5G standalone networks and the growing reliance on real-time analytics within telecom operations. According to GSMA, more than 240 commercial 5G networks are already deployed worldwide, and standalone 5G adoption is steadily increasing as operators move toward fully cloud-native architectures.

This transition is expected to significantly expand the need for NWDAF integration services, as operators require seamless connectivity between network functions and analytics platforms. Data generation across telecom networks is also rising sharply. Ericsson reports that mobile data traffic exceeded 150 exabytes per month in 2024 and is growing at an annual rate of around 20%.

This surge is creating demand for advanced analytics frameworks that can process large volumes of network data in real time. In addition, International Data Corporation indicates that telecom spending on cloud infrastructure continues to grow steadily, with a significant share of operators investing in cloud-native network functions.

The increasing complexity of network environments, driven by virtualization, edge computing, and IoT expansion, is expected to further support market growth. As telecom operators aim to improve efficiency, automate operations, and enhance service quality, NWDAF integration services are anticipated to become a critical component of future network architectures.

Future Predictions

The future of the NWDAF Integration Services Market is expected to be shaped by the rapid scaling of intelligent and data-driven telecom networks. According to 3GPP, NWDAF is becoming a core element of standalone 5G architecture, and its role is expanding with each new release to support advanced analytics and automation.

As of 2025, more than 300 telecom operators worldwide are investing in 5G standalone deployments, which is expected to significantly increase the demand for integration services that connect analytics functions with core network elements.

Network data volumes are projected to grow exponentially. Ericsson estimates that global mobile data traffic could exceed 400 exabytes per month by 2029, creating a massive need for real-time processing and analytics capabilities. At the same time, the number of connected IoT devices is expected to approach 30 billion by 2030, according to IoT Analytics, further increasing the complexity of telecom networks.

Automation will also play a key role in shaping future demand. International Data Corporation indicates that a large share of telecom operators are prioritizing AI-driven network operations to reduce manual intervention. These trends are expected to position NWDAF integration services as a critical enabler of predictive analytics, automated decision-making, and efficient network management in the coming years.

Key Market Segments

The consulting segment accounted for 45.7% of the market, reflecting its critical role in guiding telecom operators through the complexity of NWDAF integration. This dominance is driven by the need for strategic planning, architecture design, and seamless implementation of analytics-driven network functions. Operators are expected to rely on consulting services to align NWDAF capabilities with existing infrastructure and ensure efficient deployment across evolving 5G environments.

The on-premises segment held 55.5% share, indicating a strong preference for deploying NWDAF integration within controlled environments. This is mainly due to data security concerns, regulatory requirements, and the need to integrate with legacy telecom systems. On-premises deployment is expected to remain relevant as operators prioritize performance reliability and direct control over sensitive network data.

The network optimization segment accounted for 38.7% of applications, driven by the growing need to improve network efficiency and manage increasing data traffic. NWDAF integration enables real-time insights that help operators optimize resource allocation, reduce congestion, and enhance overall network performance. This segment is expected to expand as networks become more dynamic and data-intensive.

Telecom operators represented 52.6% of end-users, as they are the primary adopters of NWDAF integration services. Their focus on automation, service quality, and operational efficiency is expected to drive continued investment in analytics-driven network management solutions.

Research-Based Segments

By Service Type

- Consulting

- Implementation

- Support & Maintenance

- Others

By Deployment Mode

- On-Premises

- Cloud-Based

- Hybrid

By Application

- Network Optimization

- Network Security

- Quality of Service Management

- Traffic Analytics

- Others

By End-User

- Telecom Operators

- Enterprises

- Managed Service Providers

- Others

By Service Type

The consulting segment accounted for 45.7% of the market, reflecting its leading role in enabling telecom operators to design and deploy NWDAF capabilities effectively. This dominance is driven by the need for expert guidance in aligning analytics functions with complex 5G core architectures and cloud-native environments.

Consulting services are expected to support operators in defining data strategies, selecting suitable frameworks, and ensuring seamless integration across network functions, making it a critical first step in NWDAF adoption.

The implementation segment plays a key role in translating strategies into operational systems. This includes system integration, configuration, and deployment of NWDAF across telecom networks. As operators move toward standalone 5G and service-based architectures, implementation services are expected to witness strong demand due to the complexity involved in connecting multiple network elements and ensuring interoperability.

The support and maintenance segment ensures the continuous performance and reliability of NWDAF systems after deployment. These services include monitoring, troubleshooting, updates, and optimization to keep analytics functions running efficiently. As networks evolve and data volumes increase, the need for ongoing support is expected to grow steadily.

The other segment includes training, customization, and managed services, which are expected to gain traction as telecom operators seek specialized solutions tailored to their unique network requirements and operational goals.

By Deployment Mode

The on-premises segment accounted for 55.5% of the market, reflecting the strong preference among telecom operators for maintaining direct control over NWDAF integration within their core network environments.

This dominance is driven by strict data security requirements, regulatory compliance, and the need to integrate with existing legacy systems. On-premises deployment is expected to ensure higher reliability, lower latency, and better customization, which are critical for managing sensitive network analytics and real-time decision-making processes.

The cloud-based segment is gaining traction as operators shift toward more flexible and scalable network architectures. Cloud deployment allows faster implementation, reduced infrastructure costs, and easier scalability across distributed environments.

It supports advanced analytics capabilities and enables operators to process large volumes of network data efficiently. As telecom companies increasingly adopt cloud-native network functions, demand for cloud-based NWDAF integration is expected to grow steadily.

The hybrid segment combines the benefits of both on-premises and cloud-based deployments, offering a balanced approach for telecom operators. This model allows sensitive data and critical functions to remain on-premises while leveraging cloud platforms for scalability and advanced analytics. Hybrid deployment is expected to witness increasing adoption as operators seek flexibility, cost efficiency, and seamless integration across diverse network infrastructures.

By Application

The network optimization segment accounted for 38.7% of the market, reflecting its central role in improving overall network efficiency and performance. Telecom operators are expected to rely on NWDAF integration to analyze traffic patterns, manage resource allocation, and reduce congestion across complex 5G core environments. This dominance is driven by the need to maintain consistent service quality while handling increasing data volumes and dynamic network conditions.

The network security segment is gaining importance as telecom networks face rising cyber threats and vulnerabilities. NWDAF integration enables real-time detection of anomalies, suspicious activities, and potential breaches within the network. Operators are expected to adopt advanced analytics to strengthen security frameworks and ensure compliance with regulatory requirements, making this segment an essential part of network management strategies.

The quality of service management segment focuses on maintaining a consistent user experience across different services and applications. NWDAF capabilities help operators monitor latency, packet loss, and service performance in real time. This segment is expected to grow steadily as telecom providers prioritize customer satisfaction and service reliability in highly competitive markets.

The traffic analytics segment plays a key role in understanding network usage patterns and forecasting demand. By leveraging NWDAF insights, operators can optimize capacity planning and improve decision-making. This segment is expected to expand as data consumption continues to rise.

The other segment includes applications such as predictive maintenance and network planning, which are expected to gain traction as operators adopt more proactive and data-driven network management approaches.

By End-User

The telecom operators segment accounted for 52.6% of the market, reflecting their dominant role in deploying NWDAF integration services across core network environments. This leadership is driven by the need to manage complex 5G standalone architectures, handle massive data volumes, and enable real-time analytics for network performance. Operators are expected to continue investing in NWDAF integration to support automation, improve service quality, and enhance operational efficiency.

The enterprises segment is gaining traction as organizations increasingly adopt private networks and advanced connectivity solutions. Industries such as manufacturing, healthcare, and logistics are expected to leverage NWDAF capabilities to monitor network behavior, optimize performance, and support data-driven operations. As enterprise networks become more sophisticated, demand for integration services is anticipated to grow steadily.

Managed service providers play a critical role in delivering outsourced network management and analytics capabilities. These providers are expected to support telecom operators and enterprises by offering end-to-end NWDAF integration, monitoring, and maintenance services. Their ability to reduce operational complexity and improve efficiency is driving increased adoption across different customer segments.

The other segment includes government agencies, system integrators, and smaller network operators that require tailored analytics and integration solutions. This segment is expected to witness gradual growth as digital infrastructure expands and more organizations seek advanced network intelligence and performance management capabilities.

Regional Analysis

North America accounted for 36.2% of the market, with a value of USD 0.68 billion in 2025, reflecting its leading position in the NWDAF Integration Services Market. This dominance is supported by early adoption of 5G standalone networks and strong investments in cloud-native telecom infrastructure.

Operators in the region are actively deploying advanced analytics capabilities to improve network intelligence, automation, and service delivery, which is expected to drive continued demand for NWDAF integration services.

The region benefits from a well-established telecom ecosystem, high data consumption, and a strong focus on digital transformation across industries. Enterprises and service providers are increasingly relying on intelligent network functions to manage complex and distributed environments. This is expected to accelerate the integration of analytics-driven solutions within core network architectures.

In addition, the presence of leading technology providers and continuous innovation in network technologies further strengthen market growth in North America. The rapid expansion of edge computing and private 5G networks is also expected to create new opportunities for NWDAF integration services.

The US plays a major role within the region, supported by ongoing investments in advanced telecom infrastructure and automation technologies. Overall, North America is expected to maintain its leadership due to strong technological capabilities and increasing demand for data-driven network management solutions.

US Market Size

The US NWDAF Integration Services Market was valued at USD 0.58 billion in 2025 and is projected to reach USD 5.15 billion by 2035, growing at a CAGR of 24.4%. This strong growth reflects the country’s rapid transition toward data-driven and automated telecom networks. Telecom operators in the US are increasingly investing in advanced analytics capabilities to manage complex 5G standalone architectures and support real-time decision-making across core networks.

The shift toward cloud-native infrastructure and service-based architectures is a key factor supporting market expansion. US telecom providers are actively modernizing their networks to enable virtualization, automation, and scalability. This transformation is expected to drive demand for NWDAF integration services, as operators require seamless connectivity between analytics platforms and network functions to optimize performance and reduce operational complexity.

Additionally, the growing adoption of edge computing and private 5G networks across industries is contributing to increased demand. Enterprises are expected to leverage NWDAF capabilities to gain insights into network behavior and improve operational efficiency.

The presence of a strong technology ecosystem and continuous innovation in telecom analytics further supports market growth. Overall, the US market is expected to remain highly dynamic, driven by increasing data volumes, advanced network deployments, and the need for intelligent, automated network management solutions.

Regional Analysis and Coverage

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherlands

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Thailand

- Vietnam

- Rest of Latin America

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Driving Factors

The NWDAF Integration Services Market is driven by the rapid rise in telecom data generation and the transition toward intelligent network operations. Global mobile data traffic crossed 150 exabytes per month in 2024 and continues to grow at nearly 20% annually, creating strong pressure on operators to adopt real-time analytics.

NWDAF plays a critical role in enabling data-driven decision-making across 5G standalone networks. Telecom operators are increasingly deploying cloud-native network functions, which require seamless integration of analytics frameworks to monitor performance and optimize resources. The growing use of video streaming, online gaming, and enterprise applications is further increasing network complexity.

Operators are expected to invest in NWDAF integration to improve service reliability and reduce latency. In addition, automation is becoming a key focus area, with many telecom providers aiming to reduce manual intervention in network management. This shift toward intelligent and self-optimizing networks is expected to significantly drive demand for integration services that can connect analytics engines with core network elements efficiently.

Restraint Factors

The market faces challenges due to the complexity of integrating NWDAF into existing telecom infrastructures. Many operators still rely on legacy systems that were not designed for real-time analytics or service-based architectures. This creates compatibility issues and increases the time required for deployment. Integration projects often involve multiple network functions, vendors, and protocols, making implementation highly complex.

Additionally, the cost of deploying NWDAF integration services can be high, particularly for operators in developing regions with limited budgets. Data privacy concerns also act as a restraint, as NWDAF requires access to large volumes of user and network data for analytics. Compliance with strict data protection regulations adds another layer of complexity.

The shortage of skilled professionals with expertise in 5G core networks, analytics platforms, and cloud-native technologies further slows adoption. These factors collectively limit the pace of market growth, especially among smaller telecom operators that may struggle with technical and financial constraints.

Growth Opportunities

The expansion of IoT and connected ecosystems presents significant growth opportunities for the NWDAF Integration Services Market. The number of connected devices is expected to approach 30 billion by 2030, generating massive volumes of network data that require continuous monitoring and analysis. NWDAF integration enables operators to process this data in real time, helping improve network performance and support new use cases.

The rise of private 5G networks across industries such as manufacturing, healthcare, and logistics is creating additional demand for analytics-driven network management. Enterprises are increasingly looking for solutions that provide visibility into network behavior and enable proactive optimization.

Edge computing is another area of opportunity, as data processing shifts closer to end users, requiring localized analytics capabilities. NWDAF integration services are expected to play a key role in connecting edge nodes with core network analytics. These developments are expected to open new revenue streams for service providers and expand the market beyond traditional telecom applications.

Trending Factors

A key trend shaping the market is the increasing adoption of artificial intelligence and machine learning in network analytics. Telecom operators are using AI-driven tools to predict network failures, automate resource allocation, and improve service quality. Global spending on AI technologies has already crossed USD 250 billion, indicating strong momentum toward intelligent systems.

Another major trend is the shift toward cloud-native and service-based architectures, which allow operators to deploy network functions more flexibly. This transformation is increasing the need for integration services that can connect analytics platforms with distributed network environments.

The rise of edge computing is also influencing market dynamics, as operators move analytics closer to users to reduce latency and improve performance. In addition, there is a growing focus on real-time insights and automation to support self-healing networks. These trends are expected to redefine how telecom networks operate, making NWDAF integration a critical component of future network strategies.

Competitive Analysis

The competitive landscape of the NWDAF Integration Services Market remains highly dynamic and fragmented, with no single vendor dominating the ecosystem. According to industry insights, both traditional telecom vendors and emerging analytics providers are actively developing NWDAF capabilities, creating a multi-vendor environment where interoperability and flexibility are key differentiators.

This fragmented structure is encouraging innovation, as companies compete to deliver scalable and standards-compliant integration solutions aligned with evolving 5G architectures. Leading telecom technology providers such as Ericsson and Nokia are leveraging their strong presence in core network infrastructure to integrate NWDAF within broader 5G solutions.

At the same time, software-focused and analytics-driven players such as IBM and Hewlett Packard Enterprise are focusing on AI-driven network automation and cloud-native integration platforms. Additionally, niche vendors such as Anodot and Amdocs are gaining traction by offering specialized analytics and real-time monitoring capabilities.

Competition is increasingly centered on real-time analytics, AI integration, and vendor-agnostic frameworks. NWDAF is designed to provide standardized data collection and analytics across network functions, enabling operators to avoid vendor lock-in and improve operational efficiency. Vendors that offer flexible integration, lower operational costs, and advanced automation capabilities are expected to strengthen their competitive positioning in the evolving telecom analytics ecosystem.

Top Key Players in the Market

- Ericsson

- Nokia

- Huawei

- ZTE Corporation

- Samsung Electronics

- NEC Corporation

- Cisco Systems

- Mavenir

- Amdocs

- HPE (Hewlett Packard Enterprise)

- Oracle

- IBM

- Capgemini

- Infosys

- Tech Mahindra

- Wipro

- Accenture

- Radisys

- Casa Systems

- Comarch

- Others

Recent Developments

- In 2025, the number of connected IoT devices is expected to exceed 20 billion globally, creating a surge in network data that requires continuous monitoring and advanced analytics integration capabilities.

- In 2025, telecom operators are expected to increase spending on cloud-native network functions, with over 70% adopting hybrid or multi-cloud strategies to support scalable and flexible network architectures.

- In 2025, edge computing adoption is expected to accelerate, with a significant share of telecom data processing shifting closer to end users, increasing the need for decentralized analytics and NWDAF integration solutions.

Report Scope

Report Features Description Market Value (2025) USD 1.88 Billion Forecast Revenue (2035) USD 22.20 Billion CAGR(2025-2035) 28.00% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue forecast, AI impact on Market trends, Share Insights, Company ranking, competitive landscape, Recent Developments, Market Dynamics, and Emerging Trends Segments Covered By Service Type (Consulting, Implementation, Support & Maintenance, Others), By Deployment Mode (On-Premises, Cloud-Based, Hybrid), By Application (Network Optimization, Network Security, Quality of Service, Management, Traffic Analytics, Others), By End-User (Telecom Operators, Enterprises, Managed Service Providers, Others) Regional Analysis North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Latin America; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA Competitive Landscape Ericsson, Nokia, Huawei, ZTE Corporation, Samsung Electronics, NEC Corporation, Cisco Systems, Mavenir, Amdocs, HPE (Hewlett Packard Enterprise), Oracle, IBM, Capgemini, Infosys, Tech Mahindra, Wipro, Accenture, Radisys, Casa Systems, Comarch, Others Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF)  NWDAF Integration Services MarketPublished date: Mar 2026add_shopping_cartBuy Now get_appDownload Sample

NWDAF Integration Services MarketPublished date: Mar 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- Ericsson

- Nokia

- Huawei

- ZTE Corporation

- Samsung Electronics

- NEC Corporation

- Cisco Systems

- Mavenir

- Amdocs

- HPE (Hewlett Packard Enterprise)

- Oracle

- IBM

- Capgemini

- Infosys

- Tech Mahindra

- Wipro

- Accenture

- Radisys

- Casa Systems

- Comarch

- Others

Our Clients

- 182485

- Mar 2026