Quick Navigation

- Report Overview

- Key Takeaways

- Impacts of AI

- U.S. Next-Generation Display Market

- Key Technologies Driving

- Product Analysis

- Material Analysis

- Application Analysis

- Key Market Segments

- Driver

- Restraint

- Opportunity

- Challenge

- Emerging Trends

- Business Benefits

- Key Player Analysis

- Top Opportunities Awaiting for Players

- Recent Developments

- Report Scope

Report Overview

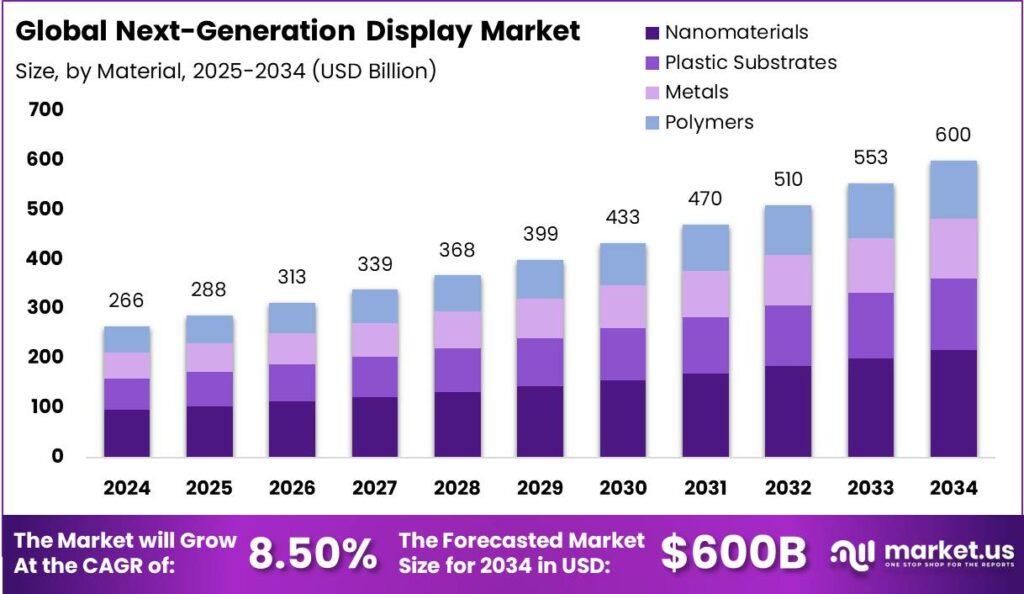

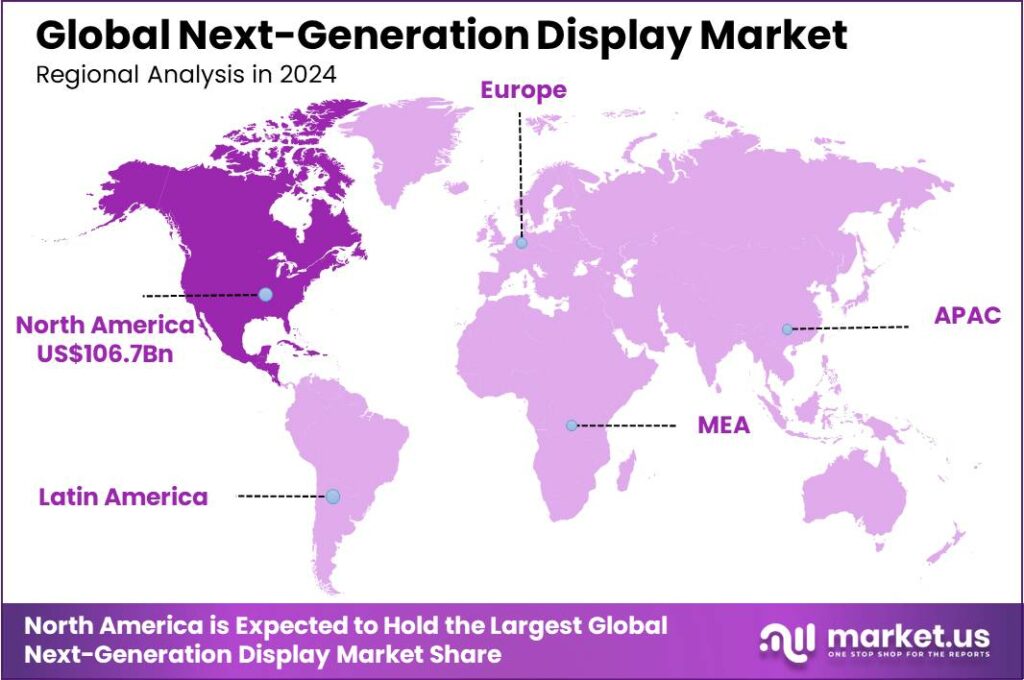

The Next-Generation Display Market size is expected to be worth around USD 600 Bn By 2034, from USD 265.5 Bn in 2024, growing at a CAGR of 8.50% during the forecast period from 2025 to 2034. In 2024, North America held a leading market share in the next-generation display sector, with a share of more than 40.2%, generating revenues of approximately USD 106.7 bn.

Next-generation displays represent a significant evolution in visual technology, encompassing a broad range of advanced display types including OLED, MicroLED, and quantum dot displays. These technologies are characterized by their superior brightness, color accuracy, and energy efficiency compared to traditional display solutions.

The next-generation display market meets the growing demand for enhanced visual experiences in applications such as smartphones, TVs, automotive, and digital signage. The growth of the next-generation display market is driven by several factors, including the consumer electronics industry’s demand for higher resolution and energy-efficient displays.

Innovations like OLED and MicroLED are making significant advancements in these areas, boosting their adoption and fueling market expansion. Advancements in material science, particularly with quantum dots and organic compounds, are enhancing the efficiency and quality of next-generation displays.

The main drivers of the next-generation display market include the increasing demand for high-quality displays in consumer electronics, the adoption of advanced display technologies by manufacturers, and the integration of displays in new applications such as automotive and wearable devices.

There is a rising demand for innovative displays that provide immersive experiences, especially in sectors like entertainment, automotive, and augmented/virtual reality. Investment opportunities are abundant in the development of displays that offer better color accuracy, energy efficiency, and flexibility. The expansion of high-resolution display applications across different consumer electronics further boosts market potential.

Adopting next-generation display technologies offers businesses several benefits, including differentiation through enhanced product quality, better user experience, and improved energy efficiency. These technologies also open new markets, such as foldable devices and high-end gaming displays, providing competitive advantages.

Key Takeaways

- The Global Next-Generation Display Market size is expected to reach USD 600 Billion by 2034, up from USD 265.5 Billion in 2024, growing at a CAGR of 8.50% during the forecast period from 2025 to 2034.

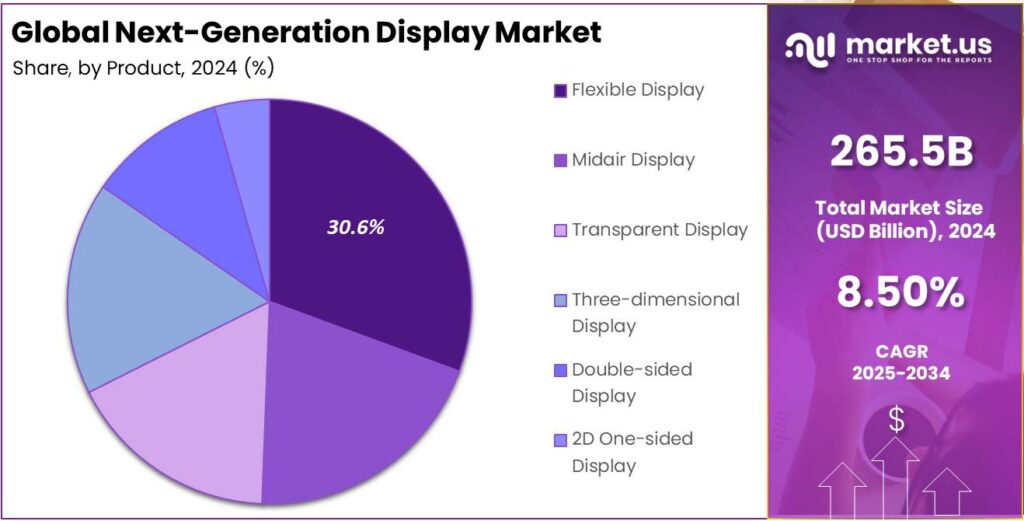

- In 2024, the Flexible Display segment dominated the market, holding more than 30.6% of the market share in the next-generation display industry.

- The Nanomaterials segment also had a dominant position in 2024, capturing more than 36.3% of the next-generation display market share.

- In 2024, the Consumer Electronics segment led the market, accounting for over 25.8% of the market share.

- In 2024, North America held a leading market share in the next-generation display sector, with a share of more than 40.2%, generating revenues of approximately USD 106.7 billion.

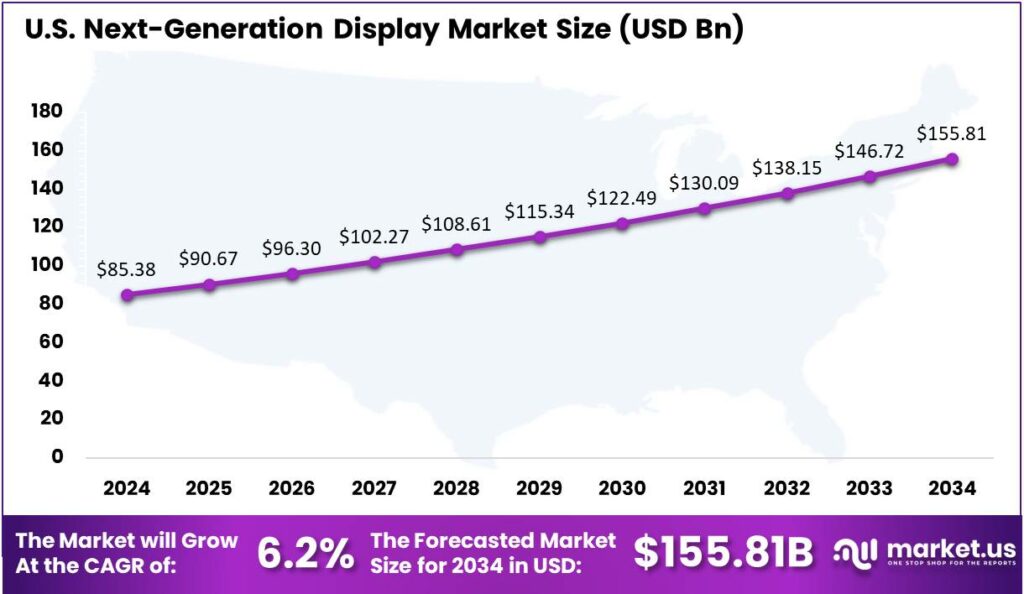

- The U.S. market for next-generation displays was valued at USD 85.38 billion in 2024, with a projected CAGR of 6.2%.

Impacts of AI

- Enhanced Reasoning and Autonomy: AI is advancing to include better reasoning capabilities, allowing it to make complex decisions autonomously. AI’s impact on interactive displays and interfaces allows dynamic content adjustment based on user interactions, making the experience more intuitive and efficient.

- Multimodal Interaction: Future displays will leverage AI to integrate text, audio, and video more seamlessly. This improves user interactions by enabling devices to communicate more naturally and responsively, understanding and synthesizing multimodal inputs for a richer, immersive experience.

- Improved Cybersecurity: As displays become smarter and more connected, the role of AI in cybersecurity becomes increasingly critical. AI’s real-time data analysis will help detect and prevent cyber threats, ensuring next-gen display technologies remain secure and trustworthy.

- Sustainability Concerns: The growth of AI technologies, including those in display tech, increases energy demands, potentially contributing to higher carbon footprints.This underscores the importance of creating sustainable AI practices to reduce its environmental impact as AI becomes integrated into technologies like displays.

- AI-driven Content Customization: In the realm of entertainment and gaming, AI is set to revolutionize how content is delivered and experienced. AI will enable more personalized and dynamic visual content on displays, adapting in real-time to user preferences and behaviors, thus enhancing user engagement and satisfaction.

U.S. Next-Generation Display Market

In 2024, the U.S. market for next-generation displays was valued at $85.38 billion, with a projected compound annual growth rate (CAGR) of 6.2%. This growth reflects the increasing demand for advanced display technologies, which include OLED, QLED, and various forms of flexible and wearable displays.

The next-generation display market is expanding due to technological advancements that enhance brightness, durability, and energy efficiency. Increased consumer demand for high-quality displays, along with higher disposable incomes, is driving growth. Additionally, ongoing R&D investments by tech companies aim to address challenges like screen burn-in and lifespan in OLED and other display technologies.

The U.S. next-generation display market is supported by digital transformation in corporate and educational sectors, increasing the demand for large, high-resolution displays. The integration of AI and IoT technologies with these displays is opening new growth opportunities, especially in smart homes and cities. As these trends progress, the market is expected to continue growing steadily, driven by technological innovation and consumer demand.

In 2024, North America held a dominant market position in the next-generation display market, capturing more than a 40.2% share with revenues reaching approximately USD 106.7 billion. This leadership can be primarily attributed to the robust presence of leading technology companies and high consumer adoption rates of advanced display technologies in the United States and Canada.

North America’s leadership in technological innovation is driven by significant R&D investments from major tech firms. The region’s robust consumer electronics sector and high demand for new technologies, especially in immersive entertainment and premium gadgets, reinforce its dominant position.

Key players like Apple, Google, and Microsoft strengthen North America’s display market through continuous investments in advanced technologies.These companies drive innovation in display quality and performance, enhancing user experiences. North America’s strong infrastructure supports the deployment of next-gen displays across education, commercial, and industrial sectors, increasing demand.

Additionally, North America’s regulatory environment fosters innovation with strong intellectual property rights and incentives for tech firms, creating a favorable climate for advancements and new product development. Economic stability and high consumer spending power further drive the adoption of new technologies, enabling companies to introduce advanced display solutions more effectively.

Key Technologies Driving

- Micro-LED Innovations: Achieves 4,000ppi resolution for VR headsets (Samsung) and over 4,000 cd/m² brightness (Sony) with individually controlled RGB LED backlights. Combines flexibility and ultra-high brightness for automotive and AR/VR applications. Projected to reach $35 billion market size by 2025.

- Mini LED Advancements: RGB-Mini LED with AI-driven backlight control (Hisense) enables 85% Rec.2020 color coverage and 30% energy savings. Quantum Dot Hybrids enhance 98% DCI-P3 color gamut and 20,000-hour lifespan.

- QD-OLED & WOLED Evolution: Samsung’s QD-OLED achieves 220ppi pixel density for 8K TVs, while LG’s 4-layer WOLED improves brightness and efficiency. UT OLED (ultra-thin) prototypes by Samsung enable paper-thin devices.

- QD-EL (NanoLED): TCL’s inkjet-printed QD-EL prototype delivers OLED-like contrast with 85% Rec.2020 coverage, challenging traditional OLED dominance.

Product Analysis

In 2024, the Flexible Display segment held a dominant market position, capturing more than a 30.6% share of the next-generation display market. The robust growth of this segment can be attributed to its widespread adoption across various consumer electronics such as smartphones, tablets, and wearables.

The superiority of Flexible Displays in the market is also underpinned by continuous innovation and investment by leading tech companies aiming to integrate flexibility with high functionality. The development of ultra-thin, energy-efficient, and high-resolution displays has made them particularly attractive for high-end consumer electronics where product differentiation is crucial.

Market dynamics show a shift towards sustainable and adaptable technologies, with Flexible Displays leading the way. Growth is driven by demand for compact, energy-efficient devices. OLED-based flexible displays offer energy savings and expanding applications in automotive and signage, broadening the market.

Looking ahead, the Flexible Display segment is poised to maintain its leadership, driven by its key role in next-gen electronics. Ongoing R&D to improve lifespan and reduce manufacturing costs will further enhance its appeal. Its adaptability to various applications and alignment with consumer demand for innovative, durable displays positions it for continued growth in the evolving market.

Material Analysis

In 2024, the Nanomaterials segment held a dominant market position within the next-generation display market, capturing more than a 36.3% share. This significant market share can be attributed to the exceptional properties that nanomaterials offer, such as superior conductivity, enhanced optical characteristics, and greater flexibility compared to conventional materials.

Nanomaterials have been leading the charge in the next-generation display market primarily due to their ability to significantly enhance display performance. Their small size allows for a high degree of control over the physical and chemical properties of the displays, which is essential for applications requiring high resolution and excellent optical performance.

The integration of nanomaterials in display technologies has enabled the creation of lightweight, flexible displays, ideal for the growing markets of wearable devices and foldable smartphones. This flexibility, not easily achieved with traditional materials like glass or polymers, provides a significant competitive edge in these innovative product categories.

The Nanomaterials segment leads due to its scalability and alignment with sustainability goals. Their efficiency in light emission reduces power consumption and extends device lifespans, supporting eco-friendly manufacturing. Continued innovation in this segment reinforces its crucial role in shaping the future of display technologies.

Application Analysis

In 2024, the Consumer Electronics segment held a dominant market position in the next-generation display market, capturing more than a 25.8% share. This segment’s leadership is largely due to the continuous demand for upgraded display technologies in devices such as smartphones, tablets, laptops, and other wearable technology.

The rapid adoption of OLED and AMOLED technologies in smartphones and televisions boosts growth in the Consumer Electronics segment. Their superior color reproduction and energy efficiency, essential for portable devices, have made these displays the standard in high-end electronics, influencing market trends and expectations.

The segment thrives on frequent product launches showcasing new display technologies, sparking consumer interest and boosting sales. Major tech companies compete to lead by introducing groundbreaking features that quickly set industry standards. This competition drives the segment and accelerates the adoption of next-gen display technologies across consumer electronics.

Market growth in consumer electronics is fueled by rising disposable income, enabling more consumers to invest in premium electronics. Increased digital media consumption, especially through streaming and gaming, boosts demand for advanced display devices. As technology evolves, the Consumer Electronics segment is poised to maintain its leadership by adapting to changing consumer preferences and emerging trends.

Key Market Segments

By Product

- Flexible Display

- Midair Display

- Transparent Display

- Three-dimensional Display

- Double-sided Display

- 2D One-sided Display

By Material

- Nanomaterials

- Plastic Substrates

- Metals

- Polymers

By Application

- Consumer Electronics

- Industrial

- Entertainment

- TV/Monitors

- Defense and Aerospace

- Automotive

- Medical

- Advertising

- Others

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Driver

Rising Consumer Demand for High-Resolution Displays

The next-generation display market is significantly propelled by the escalating consumer demand for high-resolution screens across various devices, including laptops, tablets, televisions, and smartphones. Consumers increasingly seek devices that offer sharper images, vibrant colors, and smoother motion rendering to enhance their viewing experiences.

This heightened demand has prompted manufacturers to invest substantially in research and development to produce displays with higher pixel densities, improved color accuracy, and faster refresh rates. Such advancements not only cater to consumer preferences but also drive the overall growth of the next-generation display market.

Restraint

High Manufacturing Costs and Environmental Concerns

Despite the promising advancements in display technologies, the next-generation display market faces significant restraints due to high manufacturing costs and environmental concerns. The production of advanced displays, such as Quantum Dot Displays (QDs), Carbon Nanotubes (CNTs), and Organic Light-Emitting Diodes (OLEDs), involves complex and expensive manufacturing processes.

These elevated production costs can substantially increase the overall price of end-user products, posing a barrier to widespread adoption, particularly in price-sensitive markets. Additionally, the production processes for these technologies often involve hazardous materials, leading to environmental challenges related to electronic waste management. Concerns about sustainability and the environmental impact of display manufacturing further hinder the market’s growth potential.

Opportunity

Expansion into Automotive and Industrial Applications

The next-generation display market presents substantial growth opportunities through its expansion into automotive and industrial applications. In the automotive sector, there is a growing focus on integrating advanced displays for in-car infotainment systems, augmented reality dashboards and smart rearview mirrors.

These applications require displays with enhanced durability and flexibility, aligning with the capabilities of next-generation display technologies. Similarly, industrial applications, such as wearable technology and smart factories, demand robust and efficient displays to improve operational efficiency and user experience.

The adoption of advanced display technologies in these sectors not only opens new revenue streams but also accelerates the development of innovative applications, driving the overall growth of the next-generation display market.

Challenge

Technological Limitations and Competition from Traditional Displays

The next-generation display market encounters challenges stemming from technological limitations and competition from established display technologies. For instance, while Quantum Dot displays offer superior color accuracy, they may face issues such as potential screen burn-in and limited lifespan for certain materials, similar to challenges observed in OLED displays.

Moreover, the lack of standardized communication protocols among various display technologies can impede seamless integration across different devices. Additionally, traditional display technologies, such as Liquid Crystal Displays (LCDs), continue to dominate the market due to their cost-effectiveness and established manufacturing processes. This entrenched position of conventional displays poses a significant challenge for the widespread adoption of next-generation display technologies.

Emerging Trends

One significant development is the emergence of MicroLED displays, which utilize microscopic LEDs as individual pixel elements. These displays offer superior brightness, energy efficiency, and longevity compared to traditional OLEDs. Major companies like Sony and Samsung have introduced MicroLED products, highlighting the industry’s shift towards this technology.

Another notable trend is the integration of quantum dots into display systems. Quantum dots are semiconductor nanocrystals that emit precise colors when illuminated. Incorporating them into displays enhances color accuracy and brightness, leading to more vibrant images.

Flexible and stretchable displays are also gaining traction, enabling new form factors for devices. These displays can bend or stretch without compromising functionality, paving the way for innovative applications such as wearable technology and foldable smartphones. Additionally, the development of transparent displays is opening new possibilities in augmented reality (AR) and retail environments.

Business Benefits

- Enhanced Visual Experience: Next-generation displays like OLED and MicroLED offer superior brightness and contrast, providing a more visually engaging experience. These technologies produce deeper blacks and more vibrant colors, enhancing clarity and detail which is crucial in areas such as advertising and consumer electronics.

- Energy Efficiency: Technologies like OLED and MicroLED are more energy-efficient than traditional displays, offering key advantages in longevity and durability. MicroLEDs, for instance, are less prone to burn-in and have a longer lifespan, making them ideal for continuous use in devices ranging from smartphones to public signage.

- Flexible and Transparent Display Options: Flexible and transparent displays are revolutionizing design possibilities, enabling applications like innovative storefront marketing and immersive augmented reality. These displays allow for interactive digital signage that blends seamlessly into environments, offering a futuristic appeal.

- Improved User Interaction: Advancements in touchscreen technology, including high-end interactive displays with multi-touch support, allow businesses to enhance customer engagement through interactive kiosks and educational tools.

- Cost-Effectiveness Over Time: While initial costs may be high, next-generation displays offer long-term benefits such as lower energy consumption and reduced maintenance costs due to their durability. As these technologies mature, production costs are expected to decrease, making them a more viable option for various business applications.

Key Player Analysis

Samsung has long been a dominant player in the display industry, known for its innovative work with OLED and QLED technologies. The company has revolutionized the market with its high-definition display panels used in smartphones, televisions, and wearables. Samsung continues to push boundaries by introducing new display types like microLED, offering improved brightness, color accuracy, and energy efficiency.

LG Display Co. Ltd is another industry leader, particularly renowned for its OLED technology. The company has made significant strides in developing flexible and transparent OLED panels, which have opened up new possibilities in the design and functionality of displays.

Panasonic Corporation has built a strong presence in the display sector by focusing on high-quality, energy-efficient solutions. The company is known for its development of OLED and LCD technologies, as well as innovations in microLED. Panasonic’s displays are used in various applications, from consumer electronics to automotive displays.

Top Key Players in the Market

- Samsung

- LG Display Co Ltd

- Panasonic Corporation

- Japan Display Inc.

- AUO Corporation

- BOE Technology Group Co., Ltd.

- Corning Incorporated

- FlexEnable Limited

- Kateeva

- Sony Corporation

- Pioneer Corporation

- WiseChip Semiconductor Inc.

- Others

Top Opportunities Awaiting for Players

The next-generation display market is poised for significant growth, driven by several key opportunities that market players can seize.

- Flexible Display Advancements: The evolution from rigid to flexible displays offers substantial market opportunities, particularly in consumer electronics where there is a growing demand for wearable devices and foldable smartphones. This technology not only enhances the user experience but also opens new avenues for product innovation.

- High-Definition Automotive Displays: There is an increasing demand for high-definition and interactive display solutions in the automotive sector. Next-generation displays such as OLED and MicroLED offer superior brightness and energy efficiency, making them ideal for use in vehicles for both navigation and entertainment systems.

- Innovative Applications in Retail and Advertising: The use of next-generation displays in digital signage and retail applications offers significant growth opportunities. High-resolution displays can enhance customer engagement and offer dynamic advertising solutions that attract more attention and deliver tailored messages effectively.

- Expansion in the Healthcare Sector: Next-generation displays are increasingly being incorporated into medical devices and healthcare systems for better diagnostics and patient care. Technologies like E-Ink and OLED provide clear benefits in terms of energy efficiency and superior display quality, which are crucial in medical environments.

- Growth in Consumer Electronics: The ongoing demand for better visual experiences in consumer electronics such as smartphones, tablets, and televisions continues to drive the market. Innovations in display technologies that offer higher resolution, enhanced color accuracy and power efficiency are key factors fueling this segment’s growth.

Recent Developments

- In January 2025, LG Display unveiled its 4th generation OLED TV panel, boasting a 33% brighter display (4,000 nits) than its predecessor, achieved through a new “Primary RGB Tandem” structure with four independent stacks of RGB elements.

- In January 2024, Kopin Corporation has teamed up with MICLEDI Microdisplays in a strategic partnership aimed at revolutionizing immersive AR experiences. Together, they are focused on developing and manufacturing cutting-edge microLED displays designed to perform seamlessly in bright environments.

- In April 2024, Samsung unveiled eco-friendly QD-OLED displays, offering improved energy efficiency and a reduced environmental impact. Combining OLED technology with Quantum Dots, these displays deliver superior picture quality while consuming 25% less energy compared to traditional OLED displays.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 265.5 Bn |

| Forecast Revenue (2034) | USD 600 Bn |

| CAGR (2025-2034) | 8.50% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue forecast, AI impact on market trends, Share Insights, Company ranking, competitive landscape, Recent Developments, Market Dynamics and Emerging Trends |

| Segments Covered | By Product (Flexible Display, Midair Display, Transparent Display, Three-dimensional Display, Double-sided Display, 2D One-sided Display), By Material (Nanomaterials, Plastic Substrates, Metals , Polymers), By Application (Consumer Electronics, Industrial, Entertainment, TV/Monitors, Defense and Aerospace, Automotive, Medical, Advertising, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Samsung, LG Display Co Ltd , Panasonic Corporation, Japan Display Inc., AUO Corporation, BOE Technology Group Co., Ltd., Corning Incorporated, FlexEnable Limited, Kateeva , Sony Corporation, Pioneer Corporation, WiseChip Semiconductor Inc. , Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three license to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |